Your homeowners policy rates explained depends on far more than just your home’s square footage. Insurance companies weigh dozens of factors-from your location and claims history to your credit score and the age of your roof.

At Insurance Brokers of Arizona®, we’ve helped thousands of homeowners understand why their premiums cost what they do. This guide breaks down exactly how insurers calculate your rate and shows you concrete ways to lower it.

What Actually Drives Your Homeowners Insurance Premium

Location Sets Your Rate More Than Anything Else

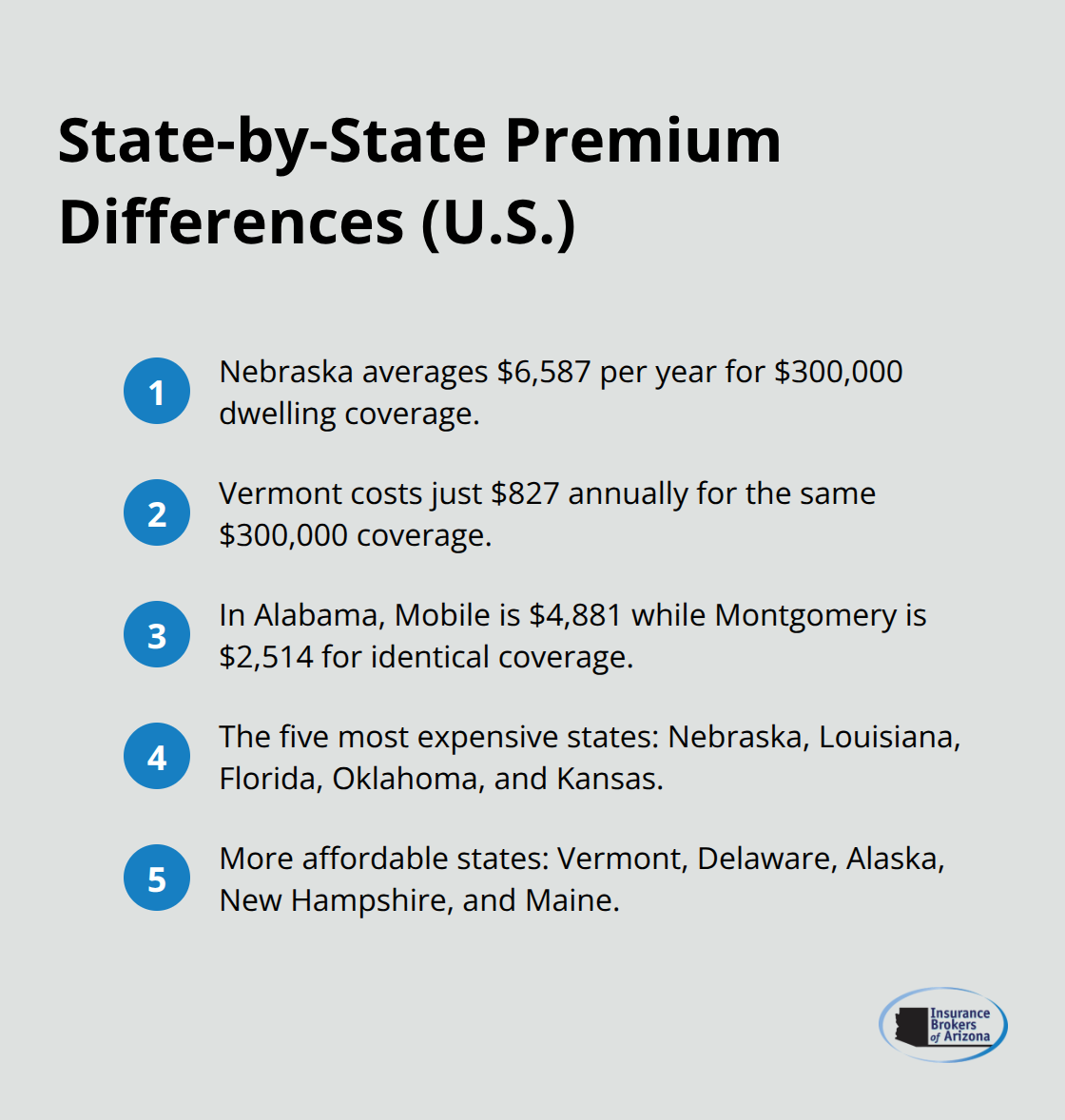

Your location is the single biggest factor determining what you pay for homeowners insurance, and it’s not even close. If you live in Nebraska, you pay an average of $6,587 per year for a $300,000 dwelling, according to Quadrant Information Services data from November 2025. Move to Vermont and that same coverage costs just $827 annually. That’s a difference of nearly $5,760 per year based purely on geography. The reason is straightforward: some states face constant hurricane, tornado, hail, and wildfire exposure.

Nebraska, Louisiana, Florida, Oklahoma, and Kansas consistently rank as the five most expensive states because of their disaster history. Meanwhile, Vermont, Delaware, Alaska, New Hampshire, and Maine stay affordable due to lower catastrophe risk. Even within states, variation is dramatic. In Alabama, Mobile homeowners pay $4,881 annually while Montgomery residents pay $2,514 for identical coverage-a $2,367 swing based on local fire protection, crime rates, and neighborhood risk.

Replacement Cost Trumps Purchase Price

Your home’s replacement cost forms the foundation of your rate, not your purchase price. If your home cost $256,000 to buy but would cost $450,000 to rebuild due to current labor and material costs, your dwelling coverage should reflect the rebuild figure. Bankrate’s data shows that $150,000 coverage averages $1,459 per year, while $300,000 coverage averages $2,424, and $450,000 coverage averages $3,374. Older homes cost significantly more to insure. A 1959 home runs about $3,285 annually while a 2020 home with the same coverage costs roughly $2,182-a $1,103 penalty for age due to outdated electrical systems, plumbing, and roofing materials. Construction type matters too. Brick structures cost less to insure for fire than wood-frame homes.

Claims History and Credit Shape Your Premium

Your claims history directly impacts rates. After a fire claim, expect premiums around $2,561; after theft, roughly $2,574. Credit history also affects pricing in most states. Moving from poor to average credit can save approximately $1,389 annually. A $1,000 deductible generates a $2,050 annual premium, but jumping to $5,000 drops it to $1,989. These factors work together-one won’t fix an expensive rate, but controlling what you can control makes a real difference.

Now that you understand what drives your rate, the next section reveals how insurance companies actually calculate your premium and where you can find meaningful savings.

How Insurers Price Your Policy

Risk Assessment Methods Vary Across Carriers

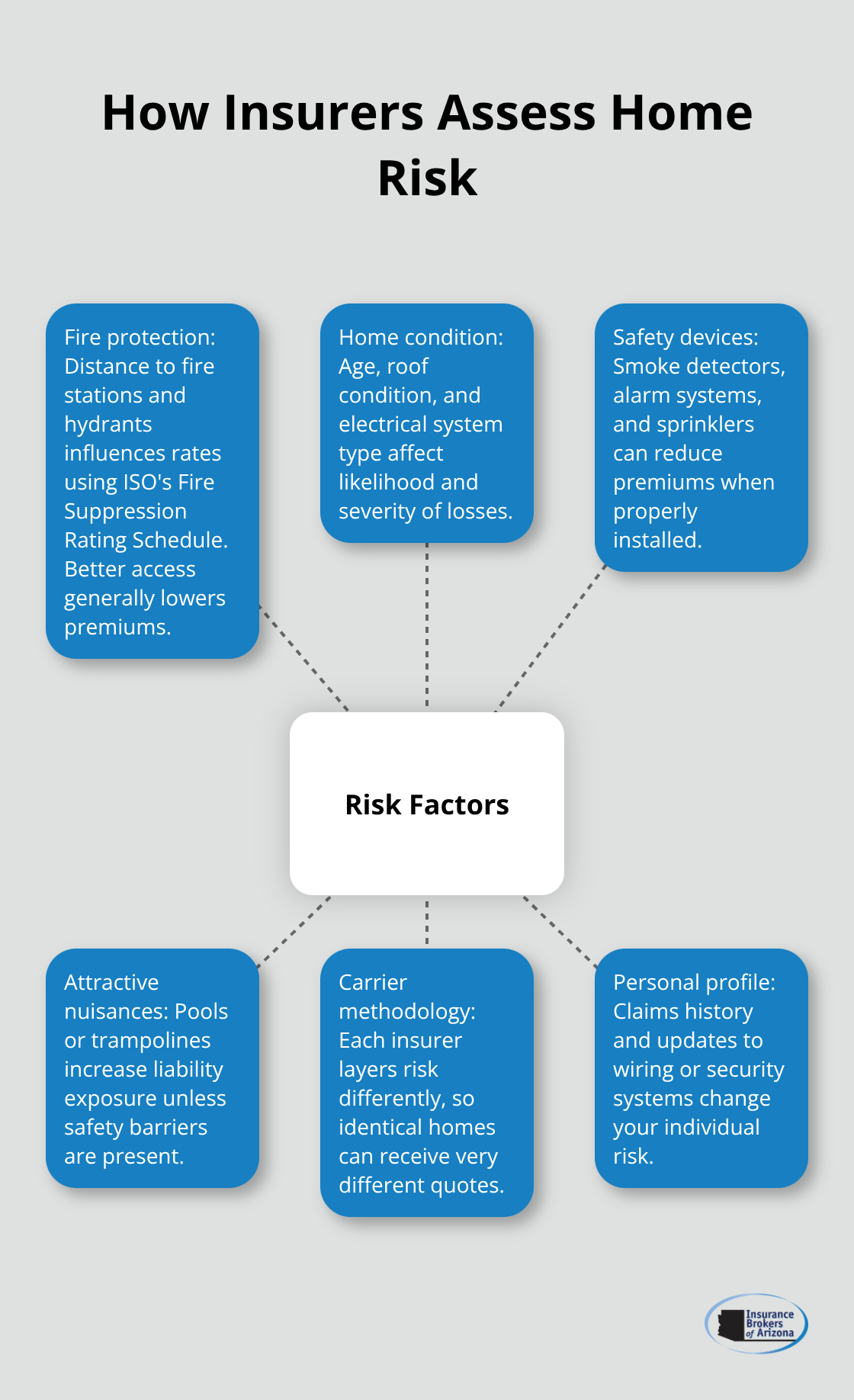

Insurance companies do not calculate premiums from a single formula-they layer risk assessments that vary significantly between carriers, which is why shopping around produces wildly different quotes for identical coverage. Most insurers use ISO’s Fire Suppression Rating Schedule to evaluate fire risk based on proximity to fire stations and hydrants, then layer in your personal risk profile including age of home, roof condition, electrical system type, and whether you have safety devices like smoke detectors or alarm systems. A home with updated wiring and a monitored security system costs less to insure than an identical home without these features. Some insurers also assess attractive nuisances like pools or trampolines, which increase liability exposure and can raise your premium or limit your eligibility unless proper safety barriers exist.

How Credit and Personal Factors Influence Your Rate

Credit-based insurance scores influence rates in most states-insurers justify this because credit behavior correlates with claims likelihood, though California, Maryland, and Massachusetts prohibit using credit for rate setting. The interaction of these factors means your premium reflects a customized risk calculation that another insurer might assess completely differently. Your marital status can also affect pricing; married homeowners typically pay less than single homeowners in states that allow this rating factor.

Why Comparison Shopping Produces Substantial Savings

Comparing quotes across multiple carriers yields substantial savings. Bankrate data shows that a standard $300,000 dwelling coverage generates an average premium of $2,424, but actual quotes can swing hundreds of dollars depending on which insurer evaluates your specific risk profile. The gap between your highest and lowest quote for identical coverage often exceeds $500 annually, meaning a single phone call to request quotes from three different carriers could save more than the time investment required.

Discounts That Lower Your Premium

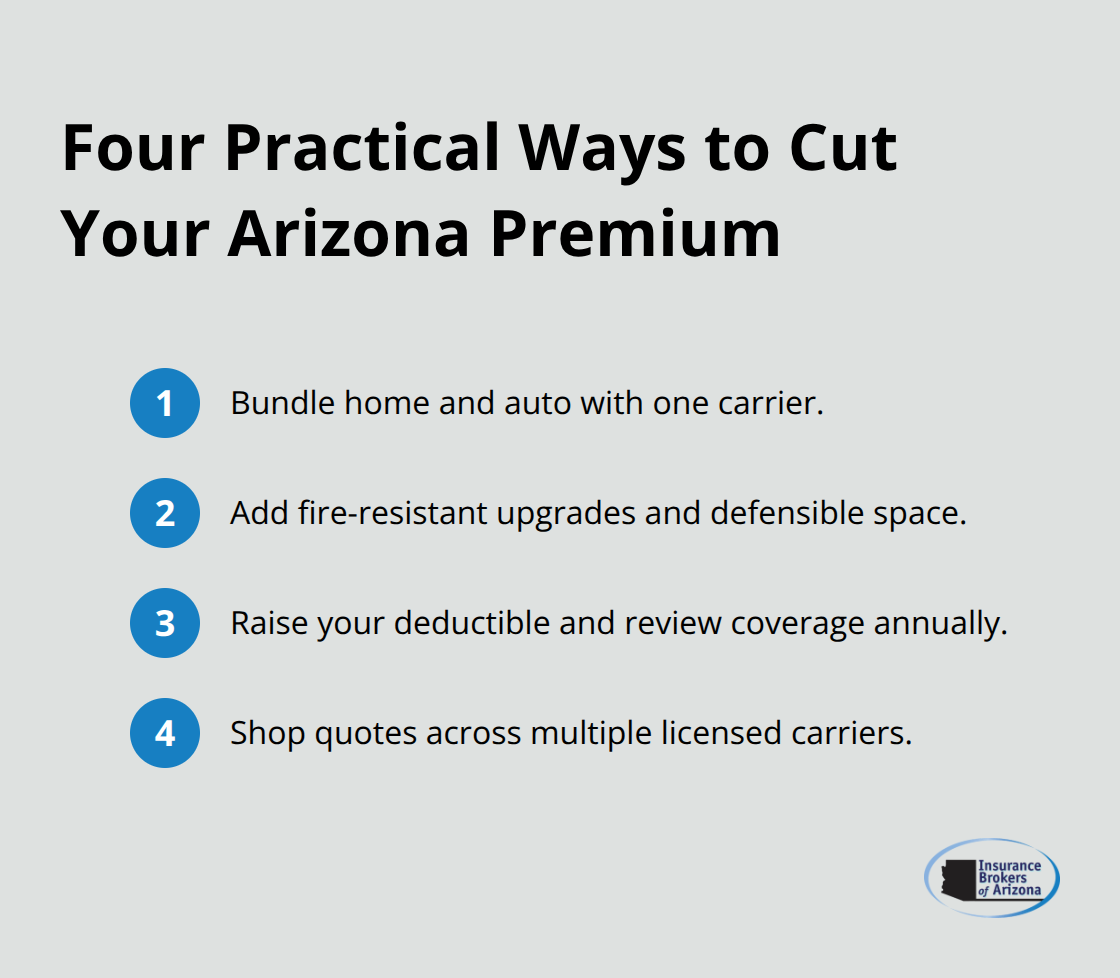

Discounts vary dramatically by carrier. Bundling home and auto with the same insurer typically saves 15 to 25 percent on your combined premium, making it one of the highest-impact moves you can make. Other discounts include installing hurricane shutters or impact-resistant windows in disaster-prone areas, which insurers must offer according to state law, and maintaining a claims-free history for three years, which can trigger loyalty discounts at renewal. Safety devices like deadbolt locks, fire extinguishers, and sprinkler systems generate smaller but cumulative savings.

Understanding how insurers calculate your rate explains why your neighbor pays a different premium for similar coverage. The next section reveals concrete actions you can take to lower your costs.

Cut Your Premium Without Cutting Coverage

Adjust Your Deductible to Match Your Emergency Fund

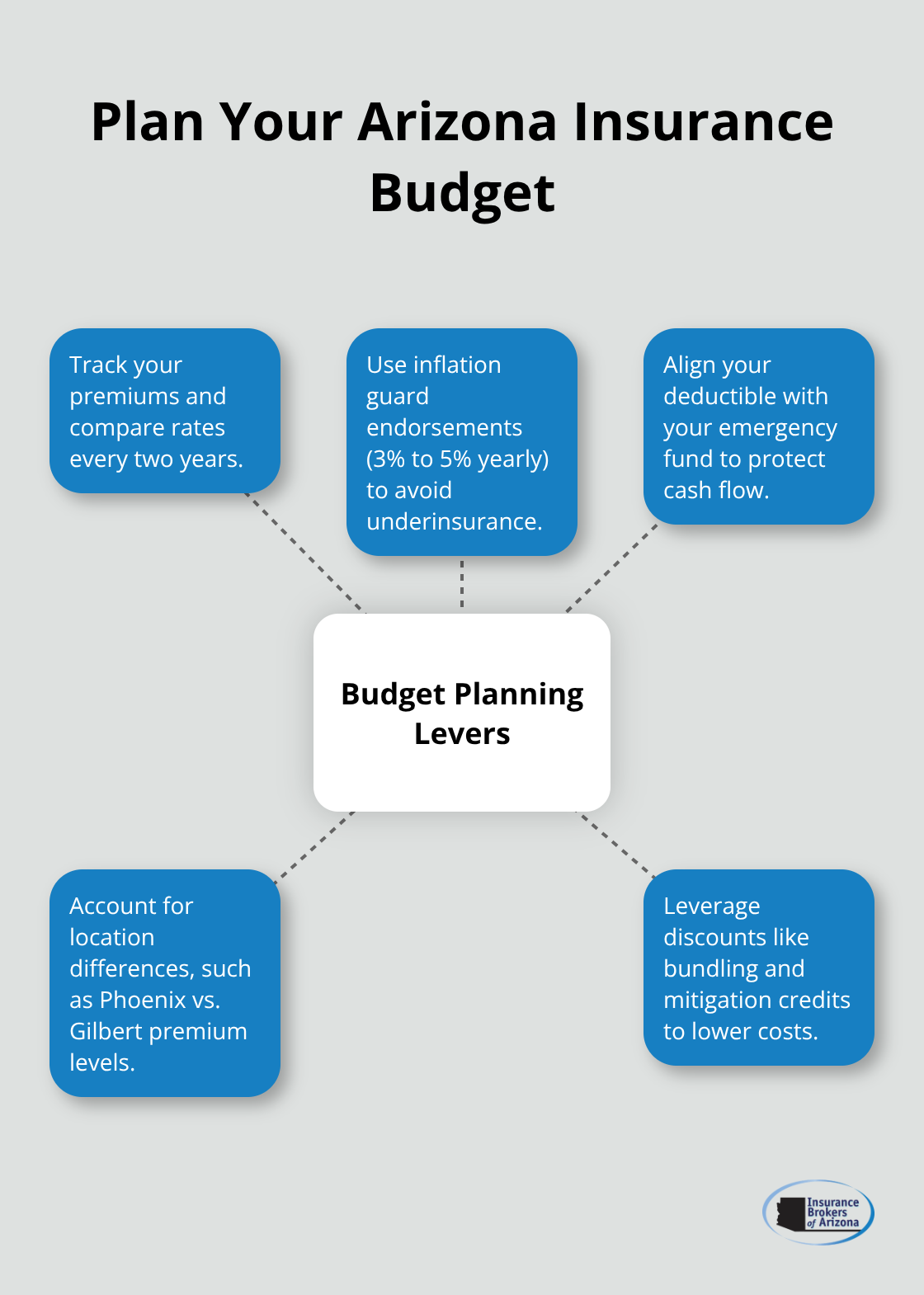

The gap between what you pay now and what you could pay sits somewhere between $500 and $1,500 annually for most homeowners. That gap exists because most people never adjust the levers that actually move their rates. A $1,000 deductible generates a $2,050 annual premium according to Bankrate data, but shifting to $5,000 drops your cost to $1,989-a $61 savings that compounds over years. The practical question isn’t whether you can afford a higher deductible; it’s whether you can cover that amount from savings if a claim happens. If your emergency fund sits at $10,000, a $2,500 deductible makes sense. If it’s $2,000, stick with $1,000.

The math only works when the deductible aligns with what you can actually pay out of pocket. A higher deductible reduces your insurer’s risk, so they reward you with lower premiums. However, you must have cash reserves to cover that deductible when you file a claim. This strategy fails if you deplete your savings to raise the deductible.

Bundle Home and Auto for Maximum Savings

Bundling home and auto with the same insurer produces the most dramatic savings available to you. Bankrate data shows bundling typically reduces your combined premium by 15 to 25 percent, which translates to $300 to $600 annually on a $2,400 homeowners policy. This isn’t a discount that requires special negotiation-carriers actively compete for bundled customers because keeping you for multiple policies reduces their acquisition costs. Call three carriers today and ask for bundled quotes covering both your home and car. The difference between the highest and lowest bundled quote often exceeds $800.

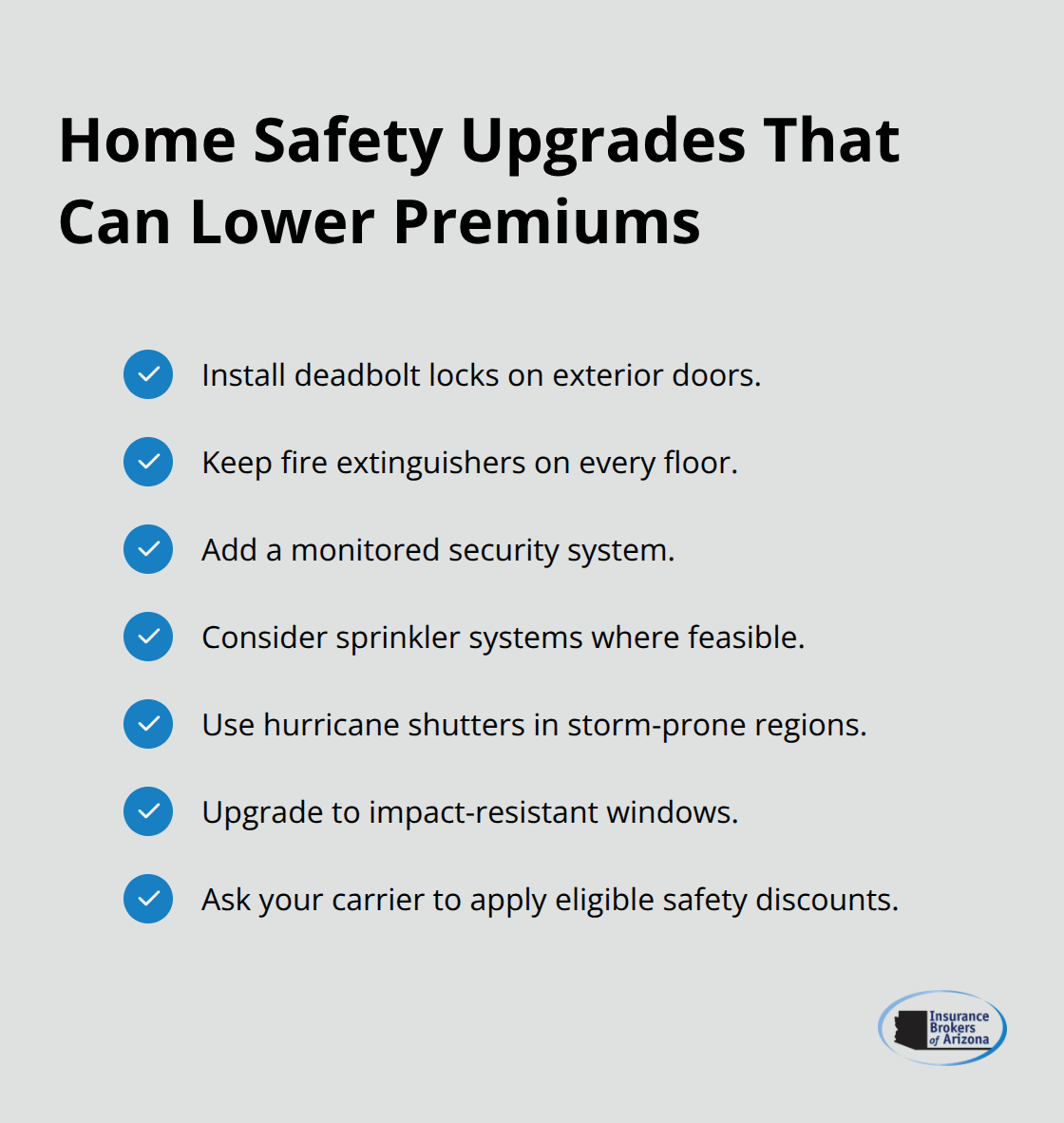

Install Safety Devices and Home Improvements

Home safety improvements generate smaller but legitimate savings. Installing deadbolt locks, fire extinguishers, and monitored alarm systems typically reduce premiums by 5 to 15 percent depending on your carrier. A monitored security system costs roughly $40 to $100 monthly but can lower your homeowners premium by $15 to $30 monthly, making it revenue-neutral or profitable over time.

In disaster-prone areas, hurricane shutters and impact-resistant windows qualify for mandatory discounts under state law-insurers must offer these reductions even if you don’t ask.

Maintain a Clean Claims History

The real leverage comes from claims history. Three years without a claim positions you for loyalty discounts at renewal, and some carriers offer accident forgiveness programs that prevent one claim from permanently raising your rate. If you filed a claim two years ago, waiting another year before filing again lets you reset that clock. This strategy requires patience, but the payoff justifies the wait.

Combine Multiple Strategies for Substantial Reductions

The interaction between these factors matters more than any single action. Increasing your deductible from $1,000 to $2,500 while bundling policies and installing a security system can reduce your annual cost by $400 to $700. That’s the difference between paying $2,050 and paying $1,350 for identical coverage.

Final Thoughts

Your homeowners policy rates explained comes down to location driving your cost more than anything else, yet the factors you control matter far more than you think. Nebraska homeowners pay $6,587 annually while Vermont residents pay $827 for identical coverage, and within those states, individual choices around deductibles, bundling, and claims history create savings of $400 to $700 per year. The gap between your current premium and what you could pay sits waiting for you to close it.

Start by requesting quotes from multiple carriers right now, since the difference between your highest and lowest quote for identical coverage often exceeds $500 annually. Bundling home and auto with the same insurer typically saves 15 to 25 percent on your combined premium, and these represent real money in your pocket based on how different insurers assess your specific risk profile. Next, evaluate your deductible against your emergency fund and raise it to $2,500 or $5,000 if you can comfortably cover that amount without depleting savings.

We at Insurance Brokers of Arizona® work with over 40 reputable carriers, which means we can show you quotes that reflect how different insurers actually price your home. Rather than calling each company individually, let us compare rates across multiple carriers and identify which combination of coverage, deductible, and discounts fits your budget and protects your home. Your homeowners policy rates explained by someone who understands your specific situation beats generic online quotes every time.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.