Running a fleet in Arizona means managing multiple vehicles, drivers, and risks simultaneously. Commercial fleet insurance Arizona protects your business from accidents, liability claims, and vehicle damage that could otherwise drain your budget.

At Insurance Brokers of Arizona®, we’ve helped dozens of fleet operators find policies that actually fit their needs. This guide walks you through what coverage matters, how to pick the right policy, and where you can cut costs without cutting corners.

What Your Fleet Insurance Actually Covers

Commercial fleet insurance in Arizona splits into three core protection areas, and understanding each one prevents costly gaps in coverage. Vehicle damage and collision coverage pays for repairs or replacement when your vehicles hit something or get hit, with costs varying based on the deductible you choose. Liability protection covers medical bills, legal fees, and property damage when one of your drivers causes an accident that injures someone or damages their property. Cargo and specialty equipment protection shields high-value items your fleet carries, from tools to materials to specialized machinery mounted on vehicles.

Physical Damage Matters More Than You Think

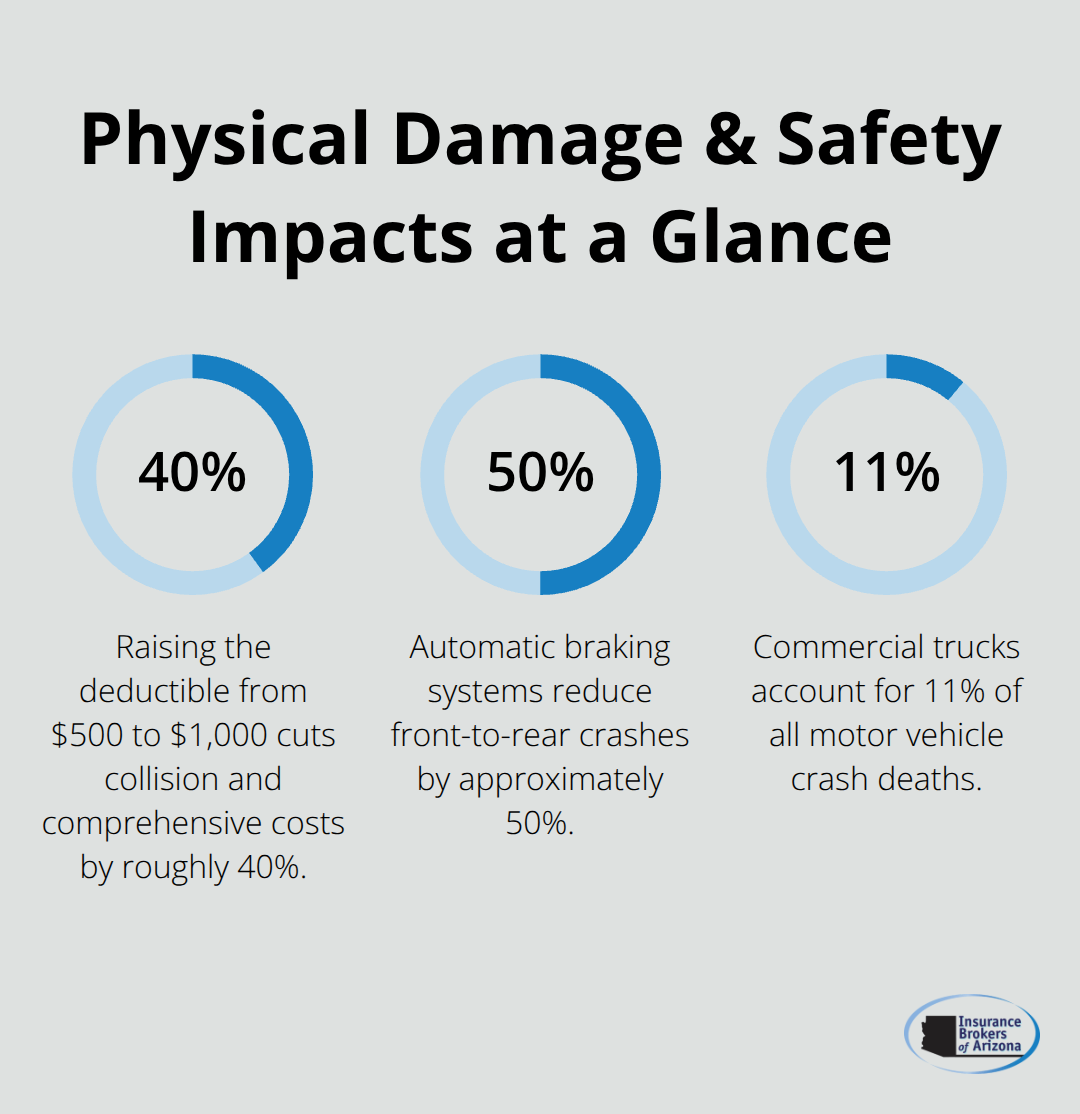

Collision coverage handles accidents your drivers cause, while comprehensive coverage protects against theft, weather, vandalism, and other non-collision damage. The Insurance Information Institute reports that commercial trucks account for 11% of all motor vehicle crash deaths despite representing only 8% of vehicle miles traveled, which explains why Arizona insurers price physical damage coverage seriously. Raising your deductible from $500 to $1,000 cuts collision and comprehensive costs by roughly 40%, making this one of the fastest ways to lower premiums without sacrificing meaningful protection. Newer vehicles with automatic braking systems qualify for better rates because the Insurance Information Institute notes these systems reduce front-to-rear crashes by approximately 50%.

If your fleet includes older vehicles, dropping comprehensive coverage on paid-off units can save money, but only if those vehicles carry lower asset value than the premium cost justifies.

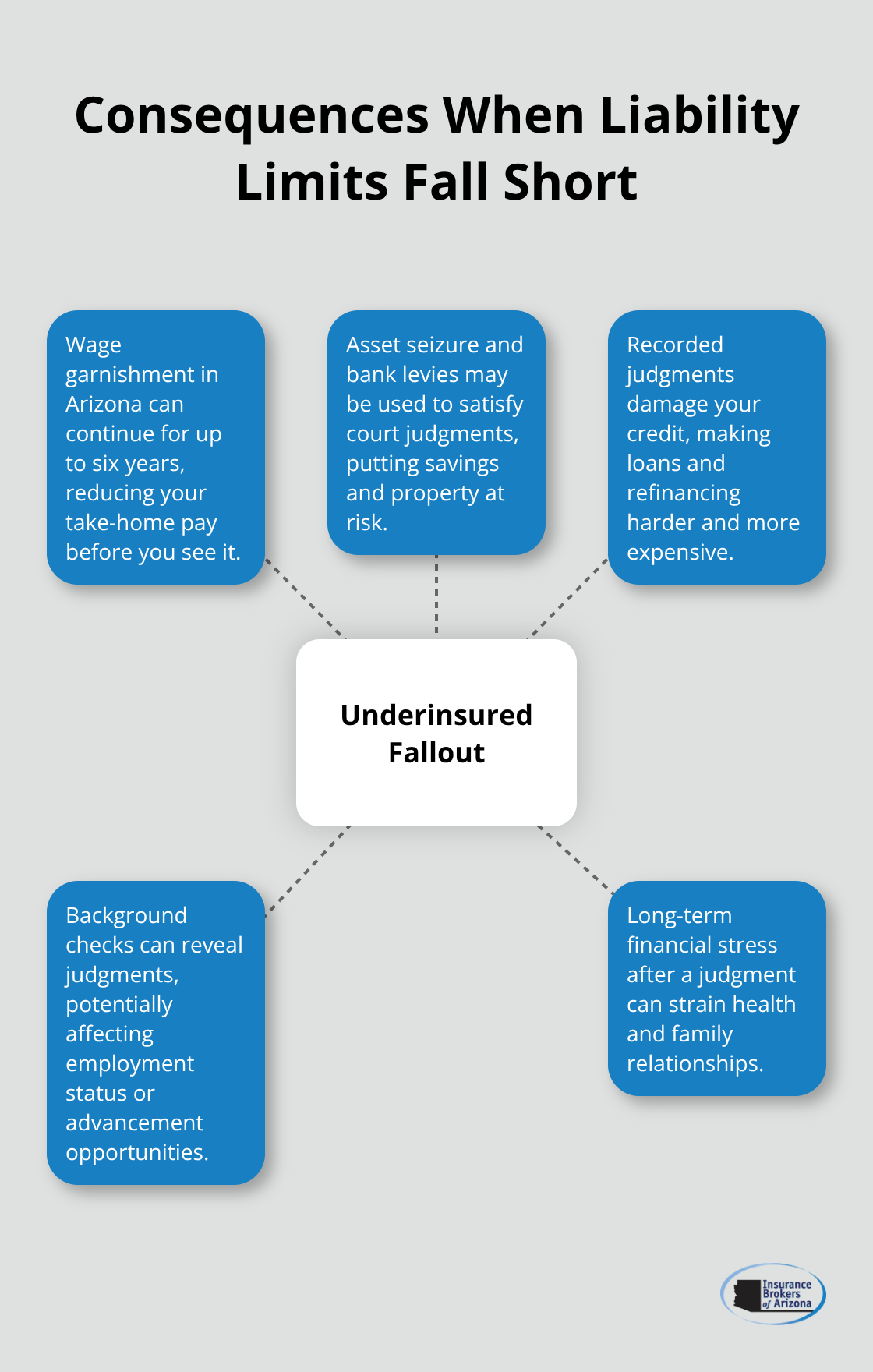

Liability Is Where Arizona Gets Expensive

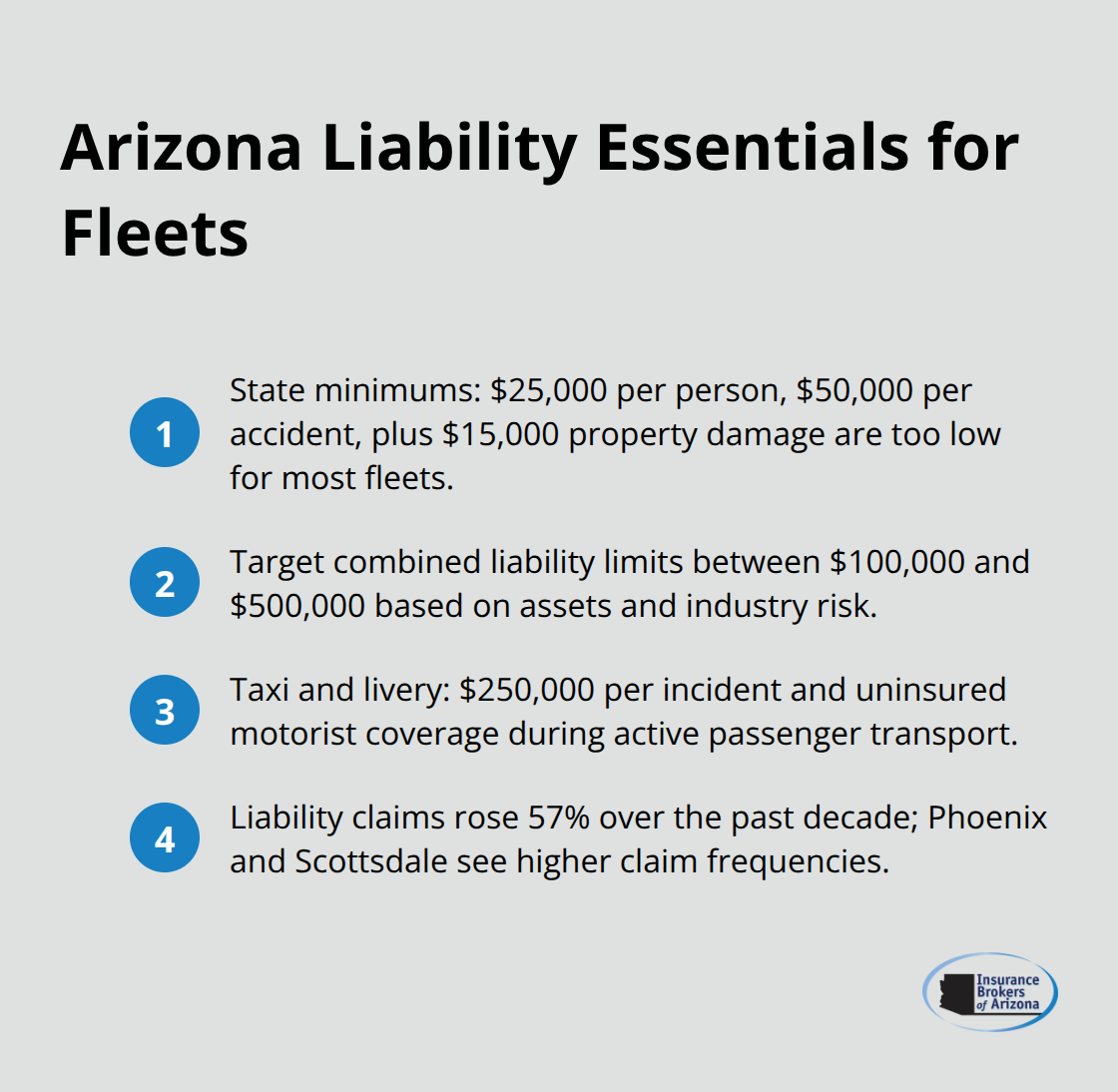

Arizona’s minimum liability limits are $25,000 per person and $50,000 per accident for bodily injury, plus $15,000 for property damage, but these minimums are dangerously low for most fleets. A single serious commercial vehicle accident easily produces verdicts over $100,000, particularly with severe injuries or multiple parties involved, making the state minimums virtually useless for real protection. Try targeting combined liability limits between $100,000 and $500,000 depending on your asset value and industry type.

Taxi and livery operations face stricter requirements: $250,000 per incident for primary commercial liability and uninsured motorist coverage during active passenger transport. Liability claims across the U.S. rose 57% over the past decade according to the Insurance Information Institute, with Phoenix and Scottsdale experiencing higher claim frequencies due to traffic density.

Cargo and Equipment Need Specific Attention

Standard commercial auto policies exclude cargo and specialized equipment, which means your tools, materials, or mounted machinery sit unprotected unless you add endorsements. Equipment-heavy operations absolutely need cargo coverage because replacement costs for specialized machinery or tool inventories can exceed vehicle value itself. Volume discounts apply across carriers when you insure five or more vehicles, but cargo endorsements often require separate quotes and specific item documentation to price accurately. The next step involves assessing your fleet size and vehicle types so you can match coverage to actual risk and avoid overpaying for protection you don’t need.

Picking the Right Fleet Policy for Your Arizona Business

Start with a Complete Fleet Inventory

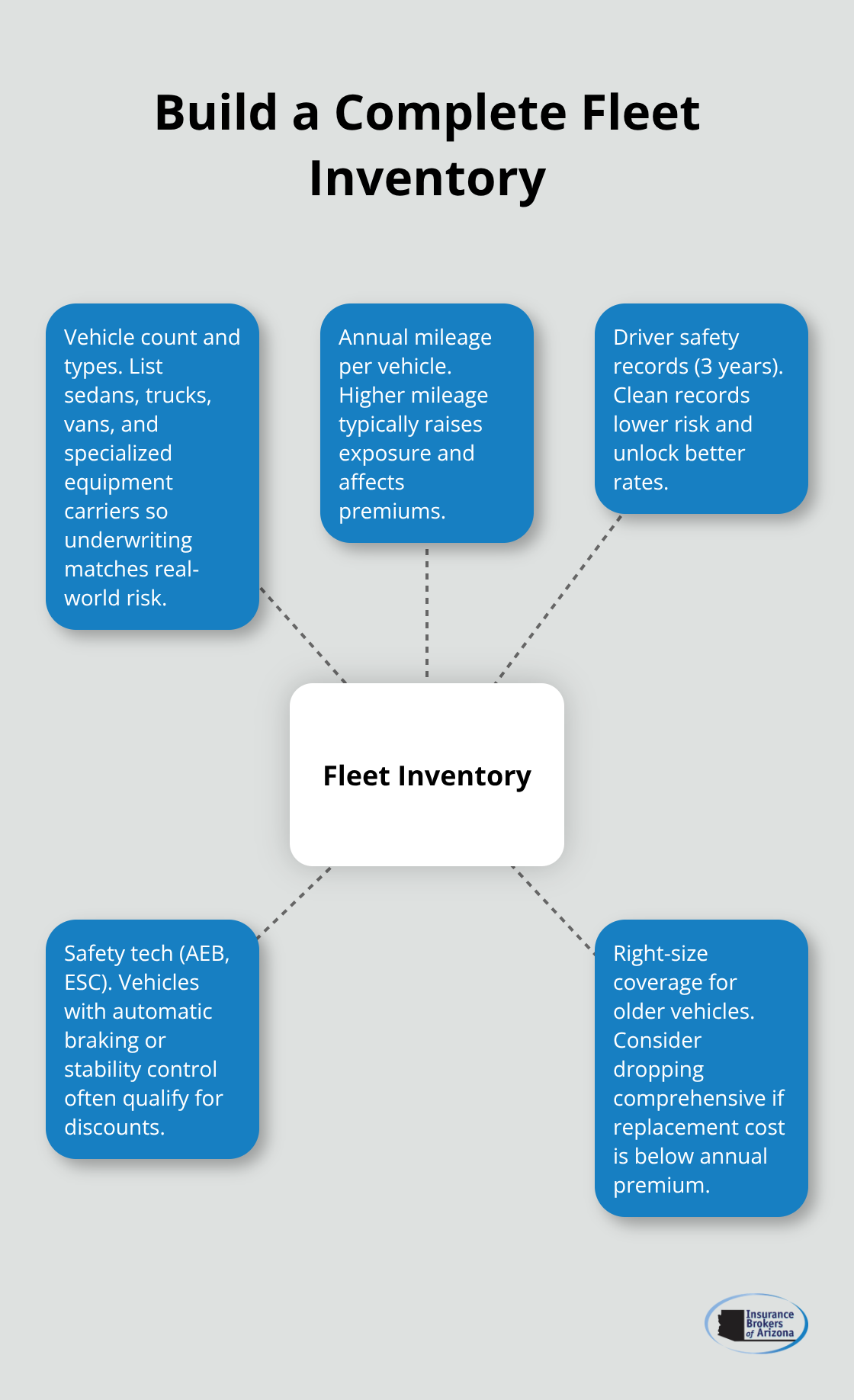

An honest inventory of your fleet separates policies that actually protect you from ones that waste money. Document every vehicle you operate: count them, note their types (sedans, trucks, vans, specialized equipment carriers), record annual mileage per vehicle, and pull three years of driver safety records.

Newer vehicles with automatic braking or electronic stability control already qualify for better rates because insurers recognize these systems cut accident frequency. Older vehicles may not justify comprehensive coverage if their replacement cost falls below annual premium expense.

Vehicle type matters significantly-commercial trucks cost more to insure than sedans because they cause proportionally higher damage when involved in accidents. Location within Arizona affects pricing too: Phoenix and Scottsdale operations pay more than rural areas due to traffic density and higher claim frequencies. Once you have this inventory, you shop intelligently rather than accept whatever quote arrives first.

Compare Quotes Across Multiple Carriers

Comparison shopping across carriers saves real money, with JD Power research showing customers who compare quotes save approximately $388 per year on average. Progressive Commercial holds about 15.21% of the commercial auto market and offers telematics discounts through Snapshot ProView, while Geico Commercial Auto maintains a user-friendly platform with average full-coverage policies around $1,939 annually. State Farm Business Auto emphasizes customizable coverage and bundling discounts, whereas Nationwide Commercial Auto provides the Vantage 360 telematics program for driver monitoring.

When requesting quotes, provide identical coverage specifications to each carrier so you’re comparing apples to apples-same deductibles, same liability limits, same vehicle list. Larger fleets typically qualify for volume discounts that lower per-vehicle premiums by 15–25% depending on fleet size and safety record. Bundling your fleet policy with property coverage generates an additional 12–15% savings, making it worth requesting quotes that combine auto with general liability and property protection.

Review Limits and Deductibles Carefully

After collecting quotes, review the actual limits and deductibles rather than just the premium amount. Arizona’s minimum liability of $25,000 per person and $50,000 per accident won’t cover serious accidents, so your quotes should reflect higher limits-typically $100,000 to $500,000 depending on your asset value. Increasing your comprehensive and collision deductible from $500 to $1,000 cuts those costs by roughly 40%, a straightforward way to lower premiums if your cash reserves can absorb larger out-of-pocket costs after a claim.

Insurance Brokers of Arizona® works with over 40 reputable carriers, which means we can match your specific fleet needs against multiple options simultaneously rather than forcing you into one carrier’s standard approach. This multi-carrier access helps you find coverage that fits both your budget and your actual risk profile. Once you’ve selected a policy that covers your vehicles and drivers adequately, the real savings come from implementing the strategies that insurers reward-safety programs, driver training, and claims management that keep your premiums down year after year.

How to Cut Fleet Insurance Costs Without Sacrificing Protection

Safety Programs Deliver the Fastest Savings

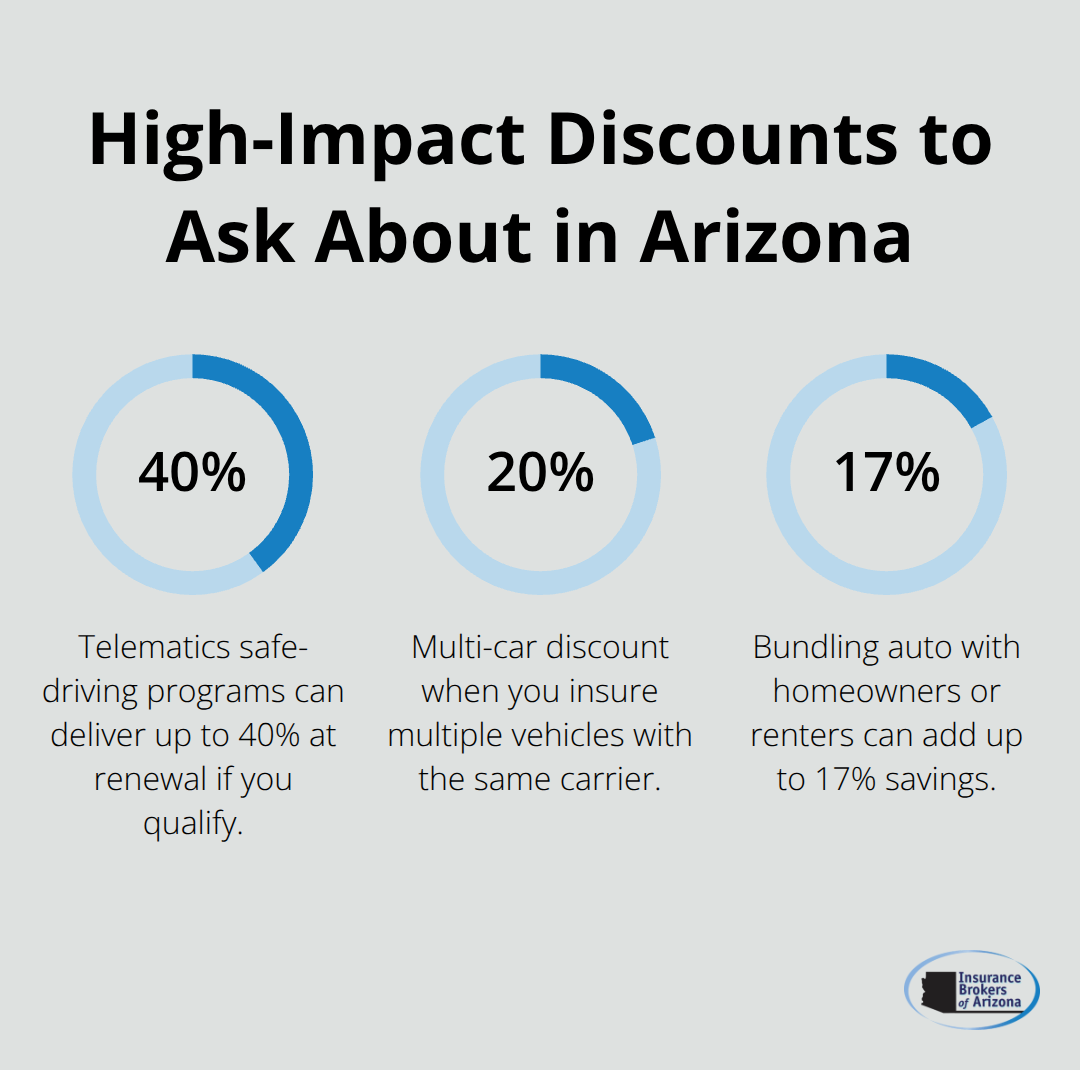

Safety programs and driver training represent the fastest return on investment for fleet operators in Arizona. The National Safety Council reports that safety-focused cultures cut crash rates by as much as 50%, which translates directly into lower insurance premiums year after year. Formal driver training programs cost money upfront, but insurers reward this commitment with meaningful discounts. Telematics systems monitor driving behavior and identify unsafe habits like hard braking, speeding, and rapid acceleration, allowing you to coach drivers toward improvement.

Studies show telematics adoption yields premium savings up to 18% when driving behavior actually improves, and some insurers offer discounts up to 25% for safety-focused fleets. Distracted driving policies with clear consequences reduce accident frequency significantly. Hiring qualified drivers through a rigorous onboarding process prevents high-risk operators from entering your fleet. These investments cost less than a single serious accident claim, which explains why Progressive Commercial and State Farm Business Auto both offer premium reductions for documented safety programs.

Bundle Coverage to Unlock Hidden Discounts

Bundling your fleet auto policy with general liability and property coverage generates 12–15% additional savings compared to buying policies separately, making this the single most effective cost-reduction tactic available. Adjusting your deductible structure from $500 to $1,000 cuts those specific costs by roughly 40%, assuming your business reserves can absorb the higher out-of-pocket expense after a claim. Request quotes from at least three carriers using identical coverage specifications so you see true price differences rather than comparing different protection levels.

Average per-vehicle premiums on individual policies range from $1,200 to $2,400 yearly, while fleet insurance typically reduces per-vehicle costs by 15–25% depending on fleet size, making the administrative consolidation of multiple vehicles under one policy both cheaper and simpler.

Review and Adjust Coverage Annually

Monitor your claims history annually and adjust coverage accordingly because older vehicles with low replacement value may not justify full comprehensive coverage at current premium rates. This annual review prevents you from overpaying for protection that no longer matches your fleet composition. Carriers with partnerships across multiple insurers can identify which combination of bundled coverage and safety discounts produces the lowest premium for your specific fleet composition and loss history without forcing you into a one-size-fits-all approach.

Final Thoughts

Selecting the right commercial fleet insurance Arizona requires honest assessment of your vehicles, drivers, and actual risk exposure rather than accepting whatever quote arrives first. Document your fleet completely, compare quotes across multiple carriers using identical coverage specifications, and implement safety programs that insurers reward with meaningful discounts. Arizona’s minimum liability limits won’t protect you in serious accidents, so target $100,000 to $500,000 in combined coverage depending on your asset value and prevent catastrophic financial exposure.

Start your quote process by gathering your fleet inventory: vehicle count, types, annual mileage per vehicle, and three years of driver safety records. Request quotes from at least three carriers with identical coverage details so you compare true price differences rather than different protection levels. Comparison shopping saves approximately $388 per year on average according to JD Power research, making this effort worthwhile even for smaller fleets.

Insurance Brokers of Arizona® partners with over 40 reputable carriers, which means we match your specific fleet needs against multiple options and identify which combination of bundled coverage and safety discounts produces the lowest premium for your composition and loss history. We focus on tailoring coverage to your actual needs, preventing overpaying for protection you don’t need while ensuring you stay protected for risks that remain. Contact us to start your quote process and get commercial fleet insurance Arizona that actually fits your business.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.