How to Find Low Cost Auto Insurance in Arizona

Auto insurance costs in Arizona can feel overwhelming, especially when you’re juggling multiple coverage options and trying to stay within budget.

At Insurance Brokers of Arizona®, we know that finding low cost auto insurance doesn’t mean settling for poor coverage. The right combination of smart choices and comparison shopping can cut your premiums significantly without sacrificing protection.

What Really Drives Your Auto Insurance Costs in Arizona

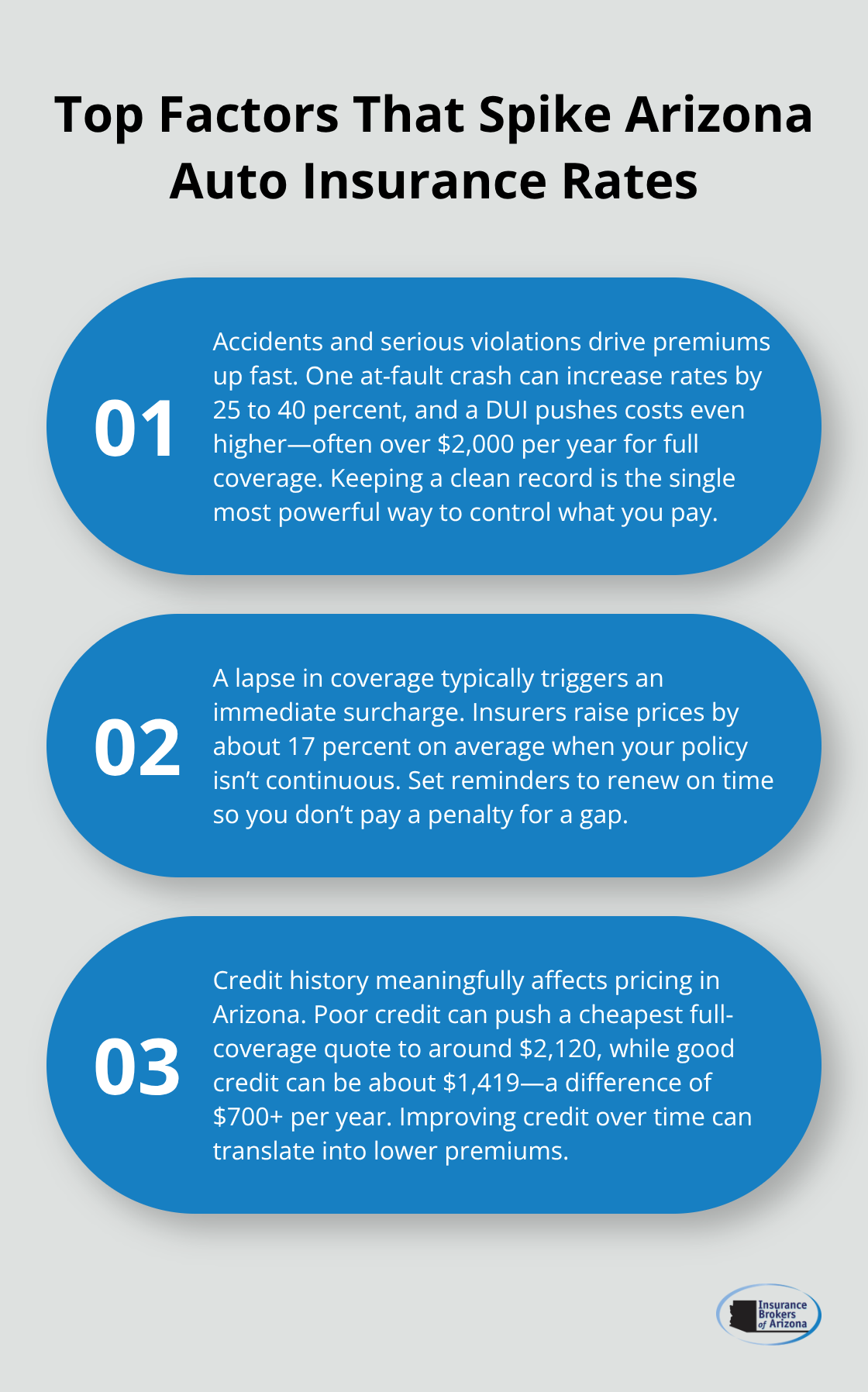

Your driving record is the single biggest factor that determines what you pay for auto insurance in Arizona, and it matters far more than most drivers realize. According to the Insurance Information Institute, one at-fault accident increases your premiums by 25 to 40 percent, while a DUI pushes costs even higher-the cheapest full-coverage rate after a DUI in Arizona jumps to around $2,038 per year with American Family, compared to $1,419 for a clean record.

A lapse in coverage damages your rates equally, raising them by about 17 percent on average, so maintaining continuous insurance is non-negotiable. Credit history also plays a substantial role that many Arizonans overlook. Poor credit pushes your cheapest full-coverage rate to approximately $2,120 per year, while good credit drops that same rate to $1,419-a difference of over $700 annually.

Teen Drivers Face the Harshest Rate Increases

Teen drivers encounter the harshest rates because the Insurance Institute for Highway Safety reports they are about three times more likely to be involved in a fatal crash than drivers aged 20 and over. Adding a 16-year-old to a parent’s policy costs around $6,874 per year nationally, though Arizona carriers vary dramatically. Auto-Owners quotes around $3,266 per year while Geico charges roughly $5,507, a difference of $2,200 for identical coverage. This variation means shopping across multiple carriers matters even more for young drivers.

How Your Vehicle Choice Impacts Monthly Payments

The vehicle you drive directly determines your insurance cost, and this decision should happen before you buy the car, not after. High-performance vehicles push teen premiums toward $1,200 or more per month, while a used sedan insures for a fraction of that cost. Cars with strong safety features and anti-theft technology receive lower premiums because they have better claims records. When you shop for a vehicle, check IIHS safety ratings and ask your insurer for a quote on the specific model before you sign paperwork.

Control Your Costs Through Deductibles and Coverage Limits

Coverage limits and deductibles are levers you control directly. Raising your collision and comprehensive deductibles from $250 to $1,000 saves approximately $440 per year on average, making this one of the fastest ways to cut costs without dropping essential protection. Arizona’s minimum liability requirement is $25,000 bodily injury per person, $50,000 per accident, and $15,000 property damage, but this barely protects your assets. Moving to higher limits like $100,000 per person and $300,000 per accident costs more upfront but shields you from catastrophic liability if you cause a serious accident. Uninsured motorist coverage is inexpensive and absolutely worth including since many Arizona drivers carry only minimum coverage or none at all.

Now that you understand what drives your rates, the next section shows you how to actively reduce those costs through strategic choices and smart comparison shopping.

How to Cut Your Auto Insurance Premiums Without Sacrificing Coverage

Bundle Policies to Unlock Immediate Savings

Consolidating your auto insurance with homeowners or renters coverage produces one of the fastest ways to lower your overall costs, and the savings are substantial. According to AAA and the National Association of Insurance Commissioners, bundling auto with home or renters insurance saves over $950 per year, and many carriers offer additional multi-policy discounts on top of that base saving. In Arizona, this means your auto premium could drop by $75 to $100 monthly just from consolidating policies with one insurer. When you request quotes, ask specifically what bundling discounts apply in your ZIP code, because carriers offer different discount levels. The math works in your favor: if your current auto insurance costs $1,500 annually and bundling saves $950 across all policies, your auto portion drops significantly while your home coverage becomes cheaper too.

Leverage Telematics and Low-Mileage Programs

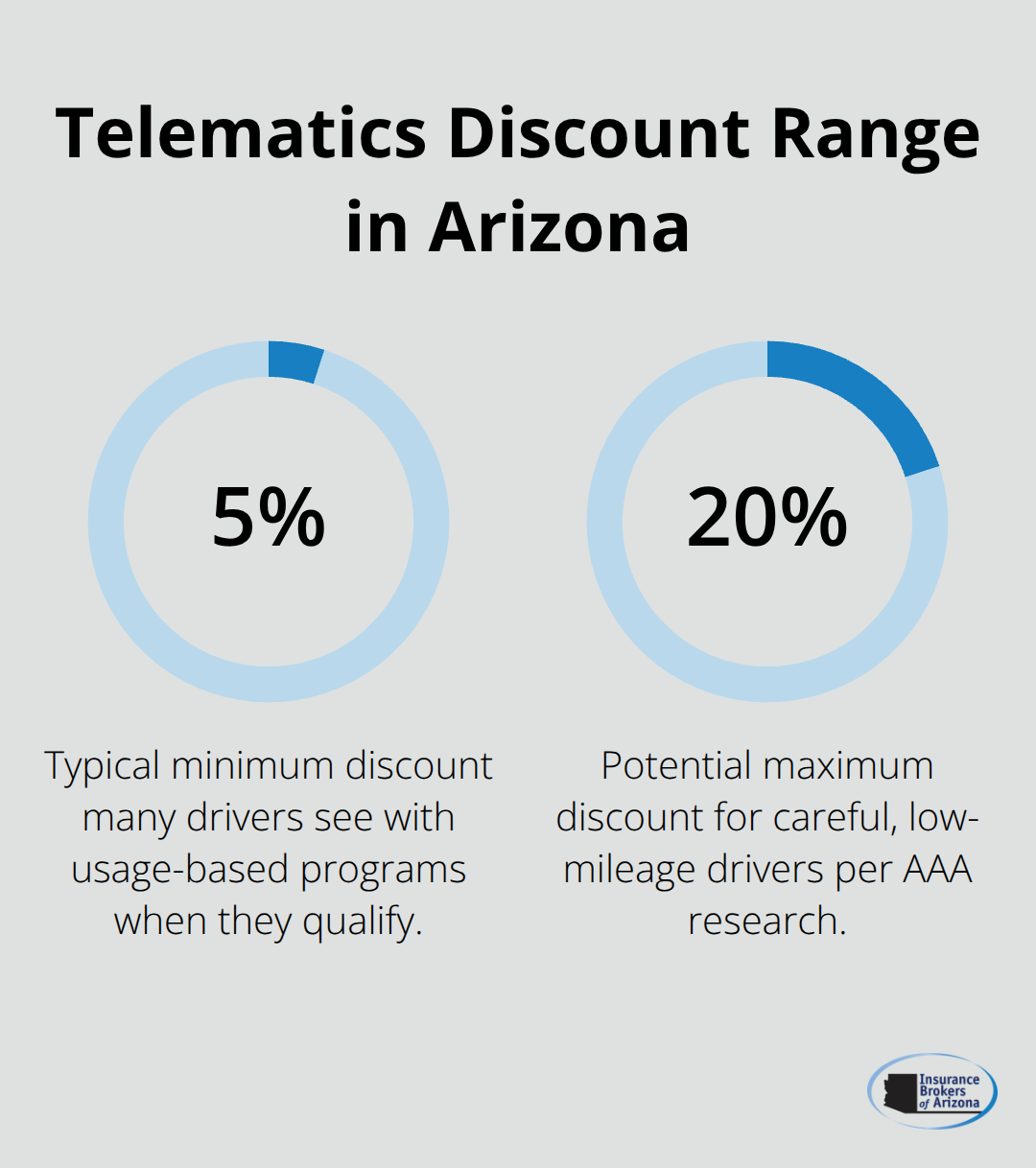

Your driving behavior and vehicle usage patterns control another set of discounts that most drivers never claim. Usage-based or telematics programs like State Farm’s Drive Safe & Save reward careful driving and low mileage with 5 to 20 percent premium reductions for qualifying drivers, according to AAA research.

If you drive under 10,000 miles annually, ask your insurer about low-mileage policies, which some carriers offer as separate products with meaningful savings. Vehicle safety features also matter more than you think. Cars equipped with automatic emergency braking, lane-keeping assist, or anti-theft systems receive lower premiums because they have better claims records across seven prior model years, as insurers track safety performance. When comparing quotes, mention every safety feature your vehicle has, from airbags to stability control, because insurers often miss these details and you could qualify for discounts you didn’t apply for.

Adjust Your Deductible to Match Your Budget

Your deductible choice separates smart shoppers from those who overpay. Raising your collision and comprehensive deductibles from $250 to $1,000 saves approximately $440 per year on average, making this single adjustment one of the fastest ways to cut costs without dropping essential protection. The key is selecting a deductible you can actually afford to pay if a claim happens, so calculate your emergency fund first before deciding. Many Arizona drivers find the $500 deductible hits the sweet spot, saving $200 to $250 annually while remaining manageable if an accident occurs. These three strategies combined can easily trim $800 to $1,200 off your annual premiums, which is why taking time to evaluate each one matters far more than hoping your insurer notices them on renewal.

Now that you understand how to reduce your premiums through active choices, the next section shows you how to compare quotes across multiple carriers to find the lowest rates available in your area.

How to Compare Auto Insurance Quotes Across Arizona Carriers

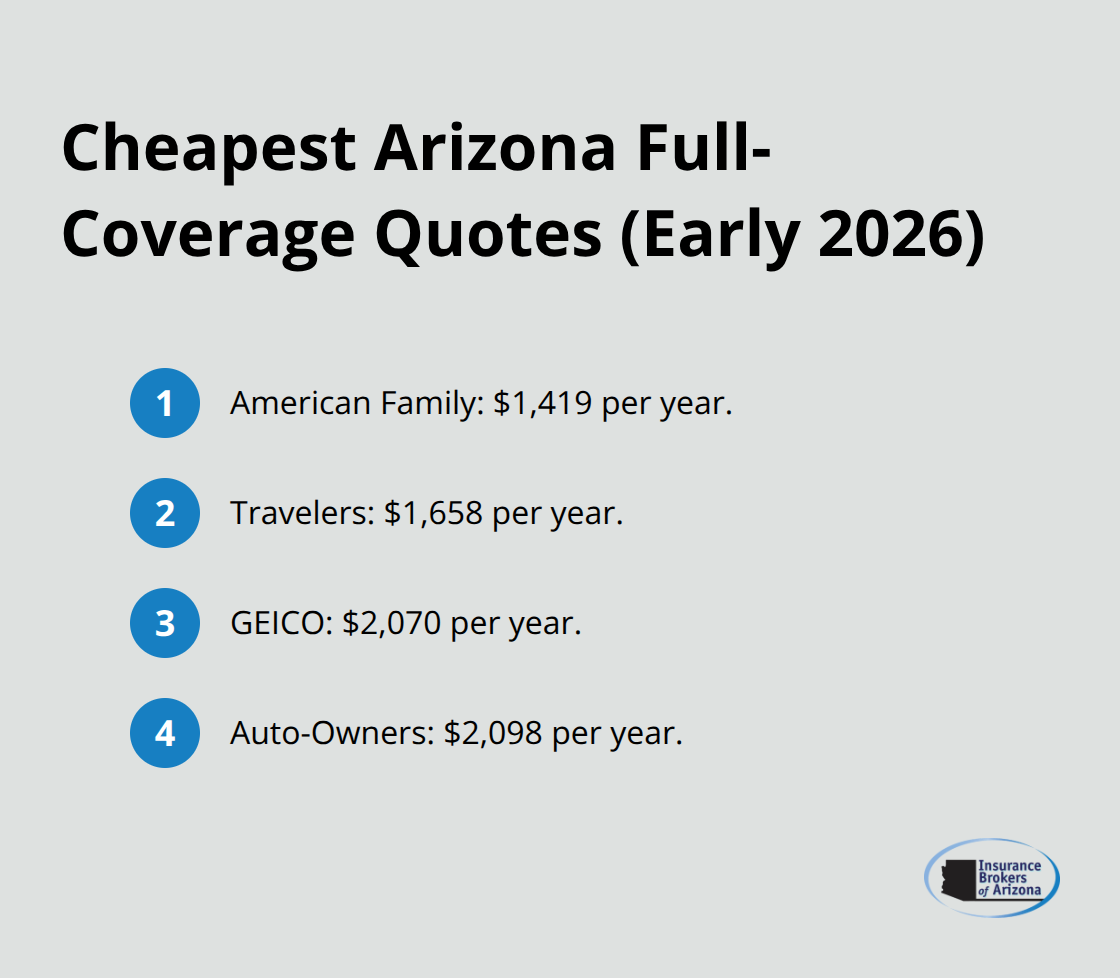

Requesting quotes from at least three to five insurers with identical coverage limits reveals the true price gaps in Arizona’s auto insurance market. The National Association of Insurance Commissioners data shows quotes vary dramatically between insurers for the same driver, and shopping around can save hundreds of dollars annually. When you request quotes, use the exact same liability limits, deductibles, and coverage types across every carrier so you’re comparing apples to apples. Many insurers offer free online quotes in under five minutes, so there’s no reason to check only one company. Arizona’s cheapest full-coverage option as of early 2026 is American Family at around $1,419 per year, but that rate only applies if you meet their underwriting criteria. Travelers charges $1,658 annually for full coverage, GEICO $2,070, and Auto-Owners $2,098, meaning the difference between the cheapest and fourth-cheapest option exceeds $600 per year for identical drivers.

Location Matters More Than Most Drivers Realize

Your ZIP code determines a significant portion of your premium because urban areas like Phoenix and Mesa have higher rates than Tucson due to theft and crash frequency. In Phoenix, American Family’s cheapest full-coverage rate reaches $1,736 annually, while the same coverage in Tucson drops to $1,458, a $278 difference that reflects local risk patterns. Request quotes for your specific ZIP code and the exact vehicle you drive, because generic quotes online won’t capture these location-based variations. The variation between cities proves that one-size-fits-all rate estimates mislead drivers into thinking they understand their actual costs.

Verify Coverage Details Match Across All Quotes

When carriers provide quotes, verify they’ve applied the same deductible, liability limits, uninsured motorist coverage, and add-ons to each proposal. Some insurers automatically quote with lower deductibles or higher liability limits than you requested, inflating their premium and making the comparison useless. Call each company and explicitly state that you want quotes with $500 or $1,000 deductibles and your chosen liability limits, then ask them to confirm these details in writing before you compare. Insurance Information Institute research confirms that consumers who compare side-by-side coverage see price differences that surprise them, and many realize they’ve been overpaying for years. During your comparison, don’t just look at the annual premium-check the monthly payment option, because some carriers charge significantly higher fees for monthly installments than others, sometimes adding $50 to $100 per year for the convenience. Review what each insurer includes with their base coverage, like roadside assistance or rental car reimbursement, because these add-ons affect the true value of the quote even if they don’t change the premium number.

Check Financial Strength and Claims-Handling Reputation

An insurer’s ability to pay your claim matters more than saving $200 annually on a carrier that struggles financially. Check A.M. Best ratings, which grade insurers from A++ down to D based on financial stability and claims-paying ability. Every carrier you’re considering should hold at least an A or A+ rating from A.M. Best to ensure they can actually pay claims when you need them. Read customer reviews on independent sites, not just the carrier’s own website, because consumer experiences with claims processing reveal whether an insurer honors its promises. Arizona drivers report widely different experiences with the same carriers, so read reviews specific to your state and look for patterns about claims handling speed and fairness. If an insurer has hundreds of complaints about claim denials or slow payment, that’s a red flag worth taking seriously even if their premium is $300 cheaper per year. Many Arizona drivers overlook this step and discover too late that they chose an insurer that fights claims or processes them slowly, which defeats the entire purpose of carrying insurance.

Final Thoughts

Finding low cost auto insurance in Arizona requires you to compare quotes across multiple carriers with identical coverage, adjust deductibles to match your budget, and bundle policies whenever possible. Shopping around saves hundreds of dollars annually, yet most Arizona drivers accept their renewal quote without checking competitors. Your driving record, vehicle choice, and ZIP code influence your rates, but you control the comparison process, the coverage you select, and the discounts you claim.

We at Insurance Brokers of Arizona® partner with over 40 reputable carriers, which means we access pricing and options that individual drivers never see shopping alone online. Rather than spending hours requesting quotes from five different companies and verifying coverage details match across each one, we pull quotes from our entire network and present side-by-side comparisons tailored to your specific situation. This saves you time and typically uncovers lower rates than you’d find independently because we understand which companies offer the best rates for your particular profile.

Gather your current policy details, including your coverage limits, deductibles, and annual premium, then contact Insurance Brokers of Arizona® for a free quote comparison. We’ll request quotes from multiple carriers using your exact coverage specifications and show you what you’re actually paying versus what’s available in the Arizona market. Many drivers discover they can cut $500 to $1,000 annually just by switching carriers or adjusting their deductible, and bundling home and auto coverage often adds another $950 in savings.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.