What is Deductible in Auto Insurance?

Auto insurance can feel overwhelming, especially when deductibles enter the conversation. At Insurance Brokers of Arizona®, we’ve helped countless drivers understand what a deductible in auto insurance actually means and how it affects their coverage and costs.

The right deductible can save you money, but the wrong choice creates real financial stress when accidents happen. This guide walks you through everything you need to know to make a decision that fits your situation.

How Deductibles Work in Your Auto Insurance Claim

What You Actually Pay When You File a Claim

A deductible is the amount you pay out of your own pocket when you file a claim before your insurance company covers the rest. If your windshield costs $1,200 to replace and you have a $300 comprehensive deductible, you pay $300 and your insurer covers $900. That $300 comes directly from your bank account before the insurer processes anything. This is not an annual fee or something that resets yearly-you pay it per claim, meaning if you file two claims in one year, you pay the deductible twice. The most common deductible choice among drivers is $500, according to data from WalletHub, which reflects a practical balance between manageable out-of-pocket costs and reasonable premiums. Typical deductible options range from $250 to $2,000, though some insurers offer lower or higher amounts depending on your state and policy type. Your deductible directly affects how much money leaves your wallet when accidents happen, so choosing an amount you can actually afford matters more than chasing the lowest premium.

Why Insurers Require Deductibles

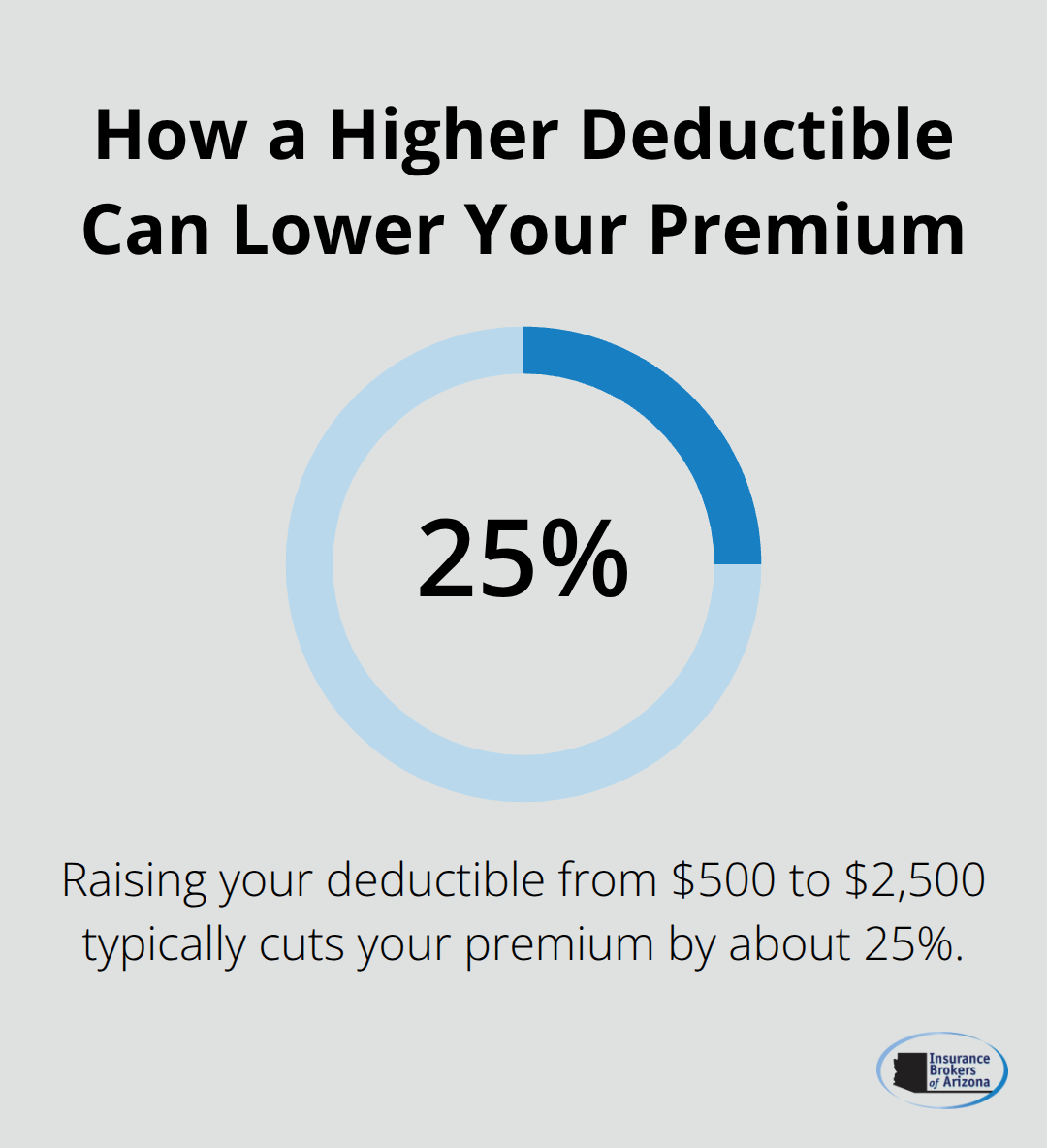

Insurers use deductibles to discourage frivolous claims and share risk with policyholders. If you had zero deductible, you would file claims for minor $200 damages, which costs the insurer more in administrative expenses than the actual repair. The deductible makes you think twice before filing small claims. This risk-sharing approach also helps insurers price premiums more accurately-drivers who can absorb higher deductibles demonstrate financial stability and typically file fewer claims. Raising your deductible from $500 to $2,500 typically cuts your premium by about 25%, making this one of the most effective ways to lower your monthly costs. This savings compounds over years: if you avoid filing claims, a higher deductible pays for itself through lower monthly costs.

However, the math works differently if you live in an area prone to hail, theft, or frequent accidents. Deductibles exist partly to manage insurer costs, which explains why they’re non-negotiable on most policies and why your choice directly influences your rate.

When and How You Pay Your Deductible

When you file a claim, the deductible payment happens after the claim is approved, not upfront. The insurer’s adjuster inspects the damage, approves coverage, and then subtracts your deductible from the payout. In some cases, the repair shop receives payment directly from the insurer minus your deductible, so you never handle the money. In other cases, you pay the shop first and the insurer reimburses you later, minus the deductible. If you’re not at fault in an accident, you might still pay your deductible initially, then recover it later when the other driver’s insurer reimburses you through a process called subrogation-but this can take months. Car and Driver notes that if you cannot pay the deductible, the insurer will still pay the damage estimate minus the deductible amount, but repairs may be delayed and your vehicle’s value could be affected. This timing reality makes building an emergency fund equal to your chosen deductible genuinely important, not just a suggestion.

Understanding how deductibles function in real claims helps you prepare financially and avoid surprises when accidents occur. The next section examines how to select a deductible that aligns with your personal finances and risk tolerance.

Picking a Deductible That Fits Your Budget

The Real Cost of Choosing Wrong

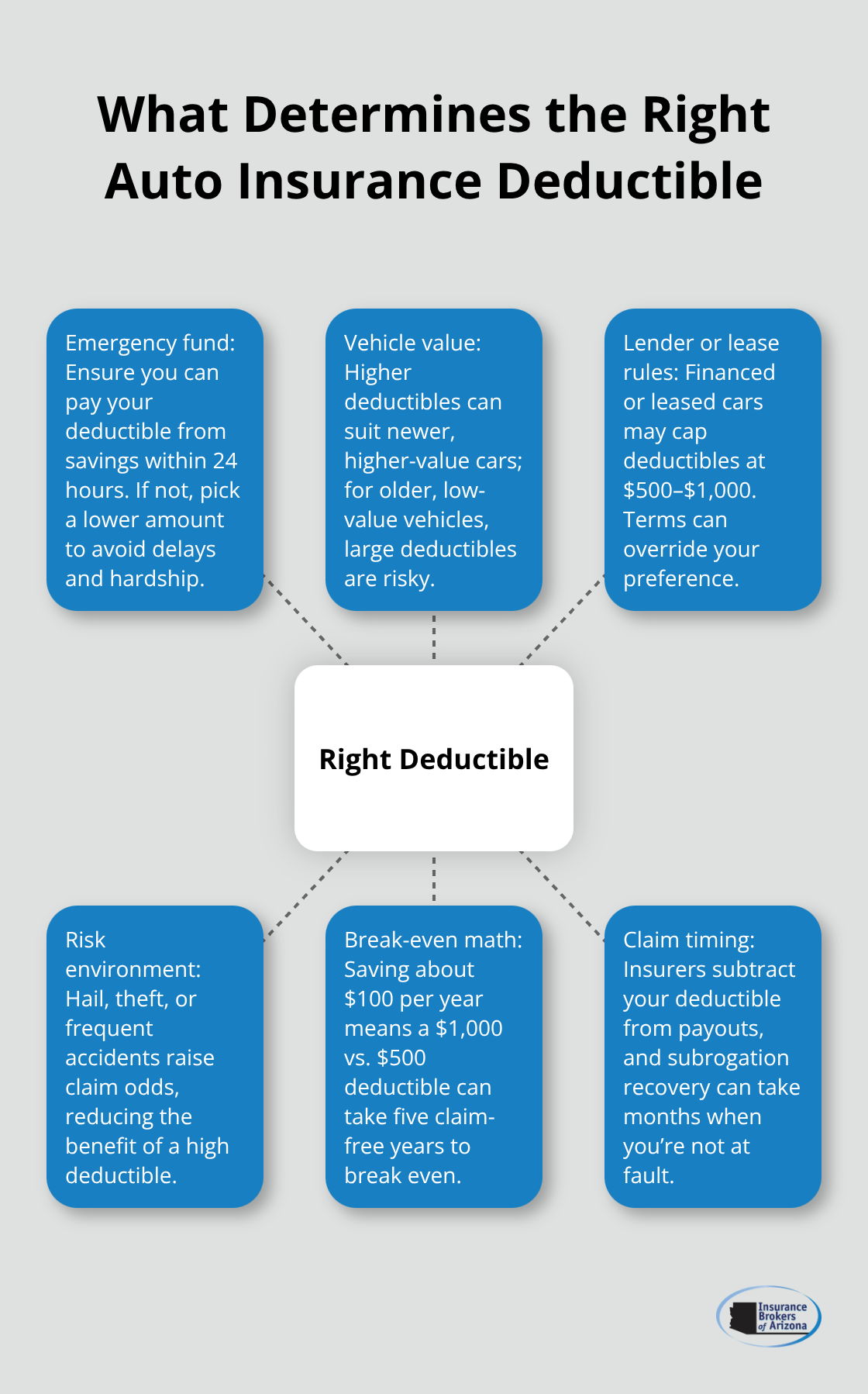

The gap between a $250 deductible and a $1,000 deductible is not just about numbers on paper-it’s about whether you can actually pay that amount when your car needs repairs. Drivers often prioritize the lowest monthly premium without considering whether they have $1,000 sitting in a bank account if an accident happens. Moving from a $500 to a higher deductible typically saves around $8 to $15 per month, but that savings only matters if you can absorb the extra $500 out-of-pocket cost when a claim occurs.

The math becomes critical here: if you save $100 per year by choosing a $1,000 deductible instead of $500, it takes five years of accident-free driving to break even on that higher deductible. If you live in an area with frequent hail storms or high theft rates, that break-even timeline stretches even longer because you’re more likely to file a claim within those five years. The practical reality is this-if you cannot comfortably write a check for your deductible amount within 24 hours, that deductible is too high.

Vehicle Value Changes Everything

Your vehicle’s age and value shift the deductible equation dramatically. A $2,000 deductible might make sense for a 2023 sedan worth $25,000, where the premium savings are substantial, but that same deductible on a 2010 Honda Civic worth $6,000 is financially reckless. If the car suffers $4,000 in damage, you’d pay $2,000 out of pocket to fix a vehicle that might not be worth repairing.

Financed or leased vehicles add another layer: your lender likely requires collision coverage and may mandate a maximum deductible of $500 or $1,000 regardless of what you prefer. Once you own the car outright, you gain flexibility, but until then, your deductible choice is partially constrained by loan terms.

Building Your Financial Safety Net

The average driver experiences an accident roughly once every seven years according to insurance industry data, which means most drivers will face a deductible claim at some point during vehicle ownership. This seven-year window is your planning horizon-not whether you’ll have an accident, but when.

Building an emergency fund equal to your deductible is not optional financial advice; it’s a requirement for choosing any deductible above $250. If your current savings cannot cover your chosen deductible, lower it immediately and allocate the premium difference toward building that emergency fund. Your financial situation matters more than premium savings, and choosing a deductible you cannot afford creates genuine hardship when accidents happen.

The next section examines how your driving habits and claim history influence which deductible amount actually protects your wallet over time.

Common Deductible Mistakes That Drain Your Wallet

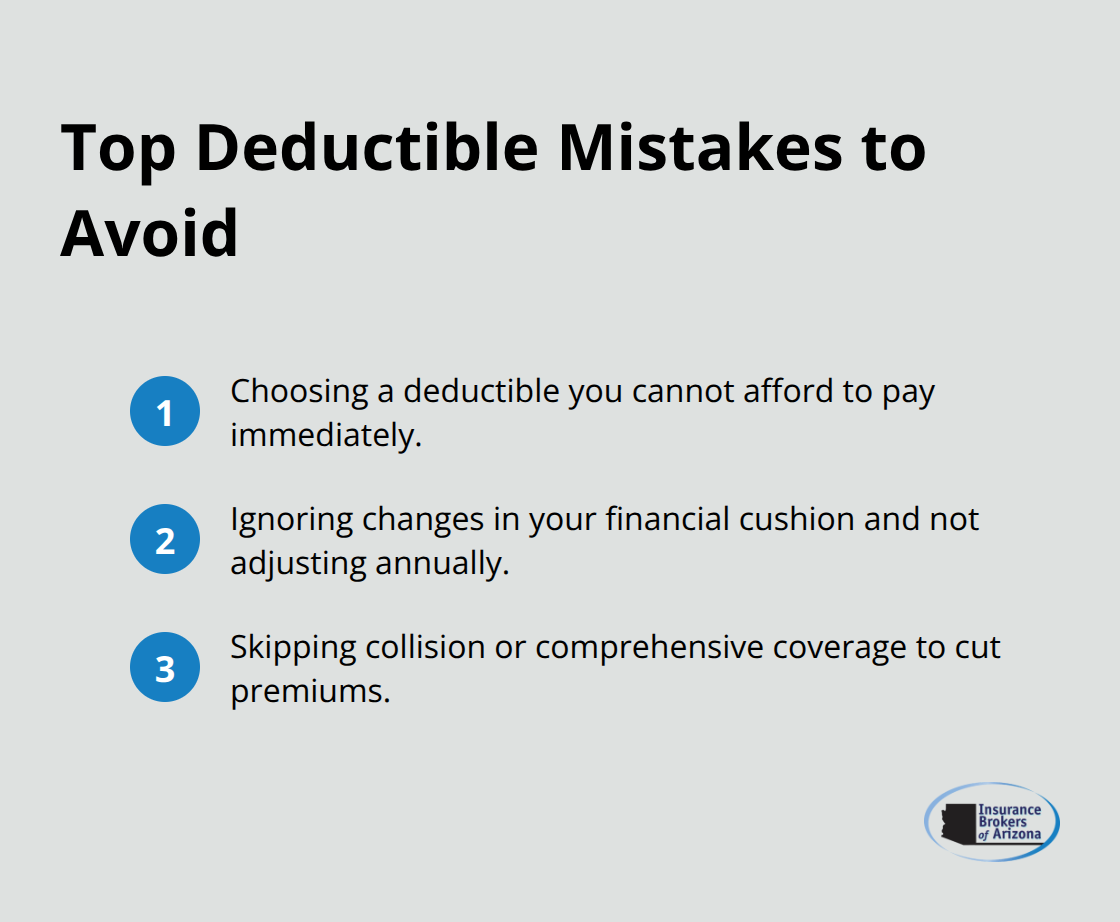

Selecting a Deductible You Cannot Afford

The most destructive deductible mistake happens long before an accident occurs: choosing an amount you cannot actually afford to pay. Drivers routinely select a $1,000 or $1,500 deductible to save $10 or $15 monthly on premiums, then panic when a claim arrives because they have no emergency savings. This creates a cascading problem-if you cannot pay the deductible within 24 hours, repairs get delayed, your vehicle sits unusable, and you may face additional expenses like rental car costs that exceed the premium savings you gained.

The insurer will still pay the claim minus your deductible, but you’ll be in financial distress waiting for reimbursement. Car and Driver reports that when drivers cannot pay their deductible, the repair shop may refuse to proceed, leaving you stranded. This is not a minor inconvenience; it’s a financial crisis triggered by selecting the wrong deductible.

The solution is straightforward: if you cannot write a check for your deductible amount right now from your savings account, that deductible is too high. Lower it to $500 or $250 and accept the slightly higher monthly premium. The premium difference between a $500 and $1,000 deductible is typically $8 to $15 per month according to industry data, which means you protect yourself from financial hardship for less than $200 per year.

Ignoring Changes in Your Financial Circumstances

The second critical mistake is assuming your financial situation remains constant throughout your policy year. Life changes rapidly: job loss, medical emergencies, reduced hours, or unexpected expenses can eliminate your emergency fund within weeks. Drivers who had comfortable savings when they chose a $1,000 deductible may face genuine hardship six months later if circumstances shift.

You must review your deductible annually and adjust it if your financial cushion shrinks. Your insurance policy is not locked in stone; you can contact your insurer to lower your deductible without penalty, and the rate adjustment applies immediately to your next billing cycle. Set a calendar reminder each year to assess whether your current deductible still matches your financial reality, your vehicle’s value, and your driving patterns.

The False Economy of Skipping Coverage

Avoid the temptation to skip collision or comprehensive coverage altogether to lower premiums. This creates a false economy because one accident costs far more than years of premium savings. A single uninsured claim can result in thousands of dollars in out-of-pocket expenses that dwarf any monthly savings you achieved. The real mistake is not reviewing your coverage annually as your life changes. This single habit prevents the financial devastation that follows when deductibles become unaffordable and leaves you exposed to catastrophic losses.

Final Thoughts

Your deductible choice determines how much financial stress you face when accidents happen, which is why this decision deserves serious attention rather than a quick glance at premium quotes. Understanding what a deductible in auto insurance means-recognizing that this single number affects both your monthly costs and your ability to recover from unexpected damage-helps you make decisions that protect your wallet over time. The most common deductible of $500 exists for a reason: it balances affordability with meaningful premium savings, though your personal situation may justify a different amount.

Select an amount you can actually pay from your savings account within 24 hours, because premium savings mean nothing if they force you into financial hardship when a claim arrives. Your vehicle’s value, your emergency fund, your driving patterns, and your lender’s requirements all influence which deductible truly protects you. A $1,000 deductible saves money only if you avoid filing claims for several years and have the cash reserves to cover it immediately.

Review your deductible annually as your life changes, since job transitions, medical expenses, or shifts in your financial cushion may require adjusting your coverage. Lowering a deductible takes minutes and applies immediately to your next billing cycle without penalties. Contact Insurance Brokers of Arizona® to review your current deductible and explore whether your coverage aligns with your actual financial situation and vehicle value.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.