Auto insurance quotes in Arizona are more than just numbers on a page. They’re the foundation for understanding what coverage you actually need and how much you’ll pay for protection.

At Insurance Brokers of Arizona®, we’ve seen countless drivers make coverage decisions based on price alone, only to discover gaps when they need their policy most. This guide walks you through what those quotes really mean and how to use them to build a policy that actually protects you.

What’s Actually in Your Auto Insurance Quote

Breaking Down Quote Components

An Arizona auto insurance quote breaks down into specific components that directly shape your final premium and coverage options. The quote shows your liability limits, deductible amounts, and optional coverages like comprehensive and collision, each with its own cost. Arizona’s minimum liability requirement of 25/50/15 sets the baseline for quotes, meaning $25,000 bodily injury per person, $50,000 per accident for bodily injury, and $15,000 property damage. However, most quotes also display what happens when you increase these limits or add extras like uninsured motorist coverage or no-deductible glass coverage.

The average six-month full-coverage premium in Arizona sits around $1,282 according to The Zebra, but this varies dramatically based on your specific situation. Your driving history carries enormous weight in pricing. A clean record keeps premiums reasonable, while a single at-fault accident or traffic violation can push a six-month premium significantly higher. For perspective, a speeding violation in a school zone averages around $1,596 for six months, while a DUI can reach $2,494 or more depending on the insurer.

How Vehicle and Location Factors Shape Your Quote

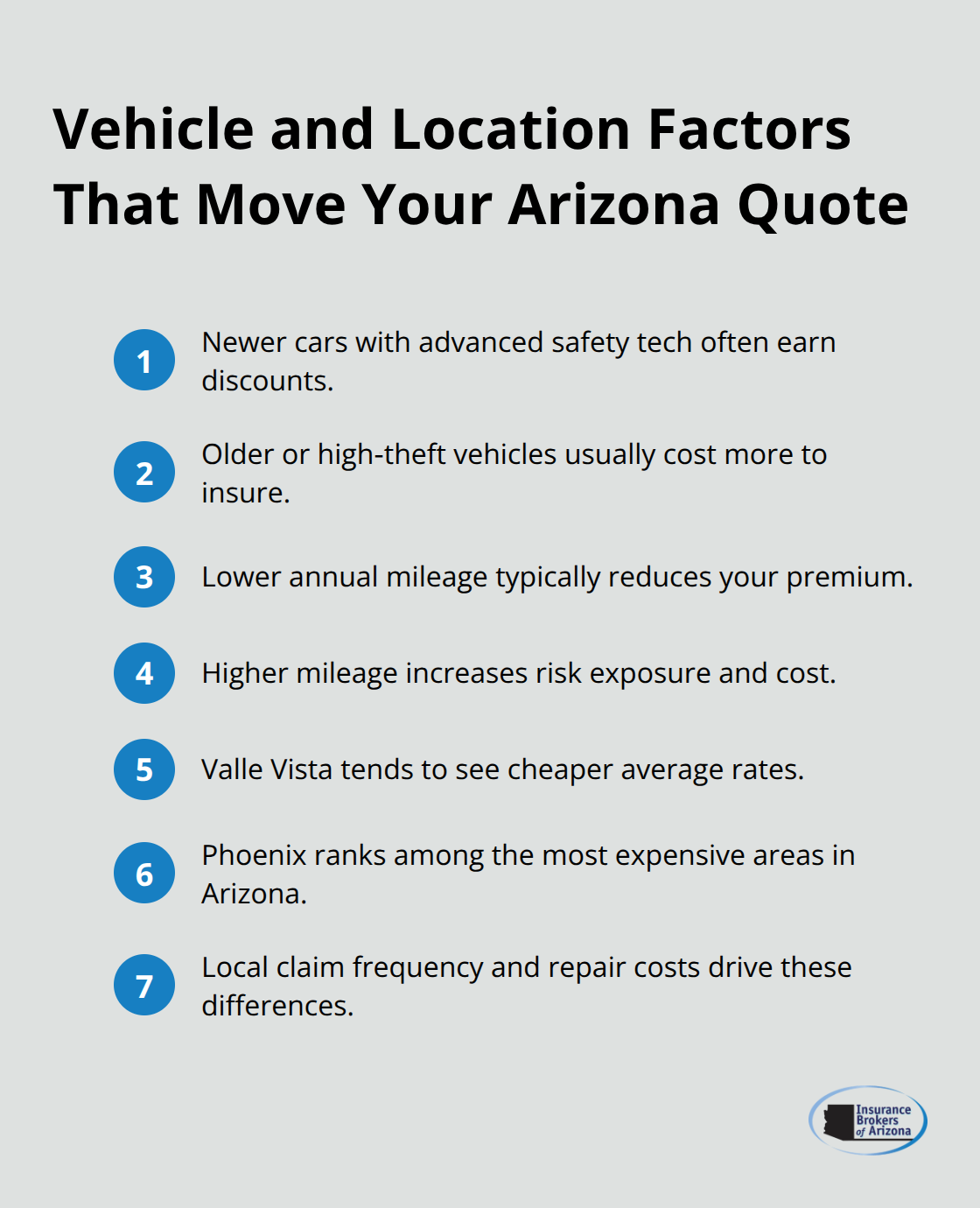

Vehicle age and safety features matter just as much as your driving record. Newer cars with advanced safety systems typically qualify for discounts, while older vehicles or those with higher theft risk command higher premiums. Your annual mileage also influences quotes substantially. Lower mileage translates to lower risk and often lower costs.

Arizona location within the state creates meaningful differences too. Valle Vista residents tend to see cheaper average rates, while Phoenix ranks among the most expensive areas in the state. These variations reflect local claim frequency and repair costs that insurers factor into their pricing models.

Arizona-Specific Regulations and Credit Scoring

Arizona-specific regulations inject several unique factors into your quote that don’t appear in other states. The state’s pure comparative negligence law means fault gets allocated by percentage, which insurers account for in their risk models. Arizona also allows you to add full glass coverage with no deductible under state law, a feature many quotes highlight as an optional add-on. Credit-based insurance scoring influences pricing at many Arizona insurers, so you should check your credit report before shopping.

Comparing Quotes Across Multiple Carriers

When you compare quotes from multiple carriers, resist the temptation to pick the cheapest option without context. Travelers offers the lowest liability-only coverage at roughly $64 monthly and the cheapest full-coverage policy at around $121 monthly, but lowest price doesn’t mean best fit. CSAA Insurance Group, which operates as AAA in Arizona, ranks as the state’s top car insurer according to JD Power, reflecting their balance of discounts, coverage options, and service quality.

Six-month premiums from major Arizona insurers range from approximately $727 with Travelers to nearly $1,880 with Safeway for full coverage, with USAA around $1,075 and Hartford around $1,430. Try collecting three to five quotes from different carriers to get a reliable picture of market rates for your exact situation. When you request quotes, match the coverage limits and deductibles across each one so you compare apples to apples.

The Renewal Shopping Advantage

Many Arizona drivers fail to re-shop at renewal time, missing opportunities to lock in better rates. Renewal pricing can shift even when your coverage stays identical, making periodic comparison essential for avoiding overpayment. This is where the real power of quotes emerges-they reveal not just what you pay today, but what you could pay tomorrow if you take action. The next section shows you how to use these quotes to identify coverage gaps and make decisions that actually protect your assets.

What Really Drives Your Quote Higher or Lower

Your Driving History Sets the Foundation

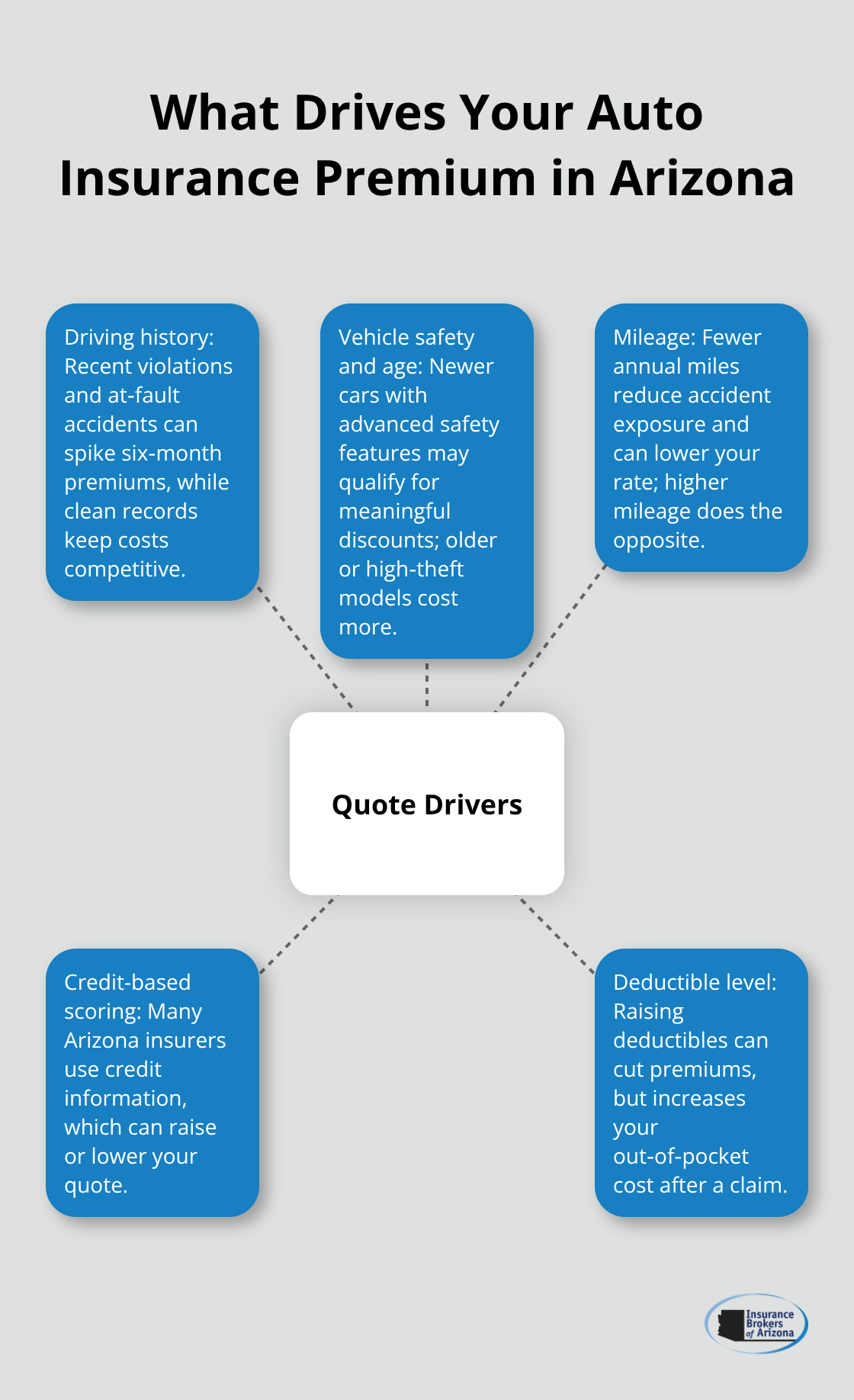

Your driving history is the single most powerful force shaping your quote, and it’s not even close. A clean record for the past three to five years keeps your premiums competitive, but one mistake costs you thousands. The Zebra data shows that a single at-fault accident adds roughly $400 to $600 to your six-month premium, while a not-at-fault accident adds only a small bump. However, serious violations hit much harder: a speeding ticket in a school zone averages $1,596 for six months, a reckless driving charge reaches $2,538, and a DUI climbs to $2,494 or higher depending on your insurer.

What matters most is that these increases fall largely within your control. One clean year begins to lower your rates, and after three to five years of safe driving, many insurers will drop the violation from their pricing calculations entirely. This means your current quote isn’t your permanent quote-it’s a snapshot that improves when you drive safely.

Vehicle Characteristics and Mileage Impact

Vehicle characteristics matter just as much as your past behavior, and Arizona insurers weight them heavily in their models. Newer vehicles with advanced safety features like automatic emergency braking and collision avoidance systems qualify for meaningful discounts, sometimes 10 to 15 percent off your premium. Conversely, older vehicles or those with high theft rates in Arizona cost more to insure because repair costs and theft risk are higher.

Your annual mileage directly affects your quote too; drivers averaging 10,000 miles per year pay significantly less than those driving 15,000 or 20,000 miles annually. Lower mileage means less time on Arizona’s highways and desert roads, reducing accident exposure substantially.

Credit Scoring and Deductible Trade-Offs

Credit-based insurance scoring influences your final quote at many Arizona carriers, though this factor varies by insurer. Check your credit report before shopping for quotes, since errors can artificially inflate your premium. Finally, deductible selection creates a direct trade-off: raising your deductible from $500 to $1,000 typically cuts your six-month premium by $100 to $200, but you’ll pay that higher amount out-of-pocket after a claim.

The question isn’t which deductible is best in general-it’s which one you can actually afford if you need to file a claim tomorrow. Understanding these three factors (driving history, vehicle traits, and deductible choice) positions you to request quotes that reflect your real situation. The next section shows you how to use those quotes to identify coverage gaps and make decisions that actually protect your assets.

How Quotes Reveal What Your Coverage Actually Costs

The Price Gap Between Liability-Only and Full Coverage

Your quotes expose something most Arizona drivers miss: the real price of leaving coverage gaps unfilled. When you request quotes from multiple carriers, you’ll notice that liability-only policies cost dramatically less than full coverage. A liability-only quote from Travelers might show $64 monthly, while their full-coverage option jumps to $121 monthly. That $57 difference seems minor until you total it across a year-roughly $684 more for comprehensive and collision protection. But here’s where most drivers make a critical mistake: they focus on that monthly number instead of asking what happens if they hit someone’s car or their vehicle gets damaged.

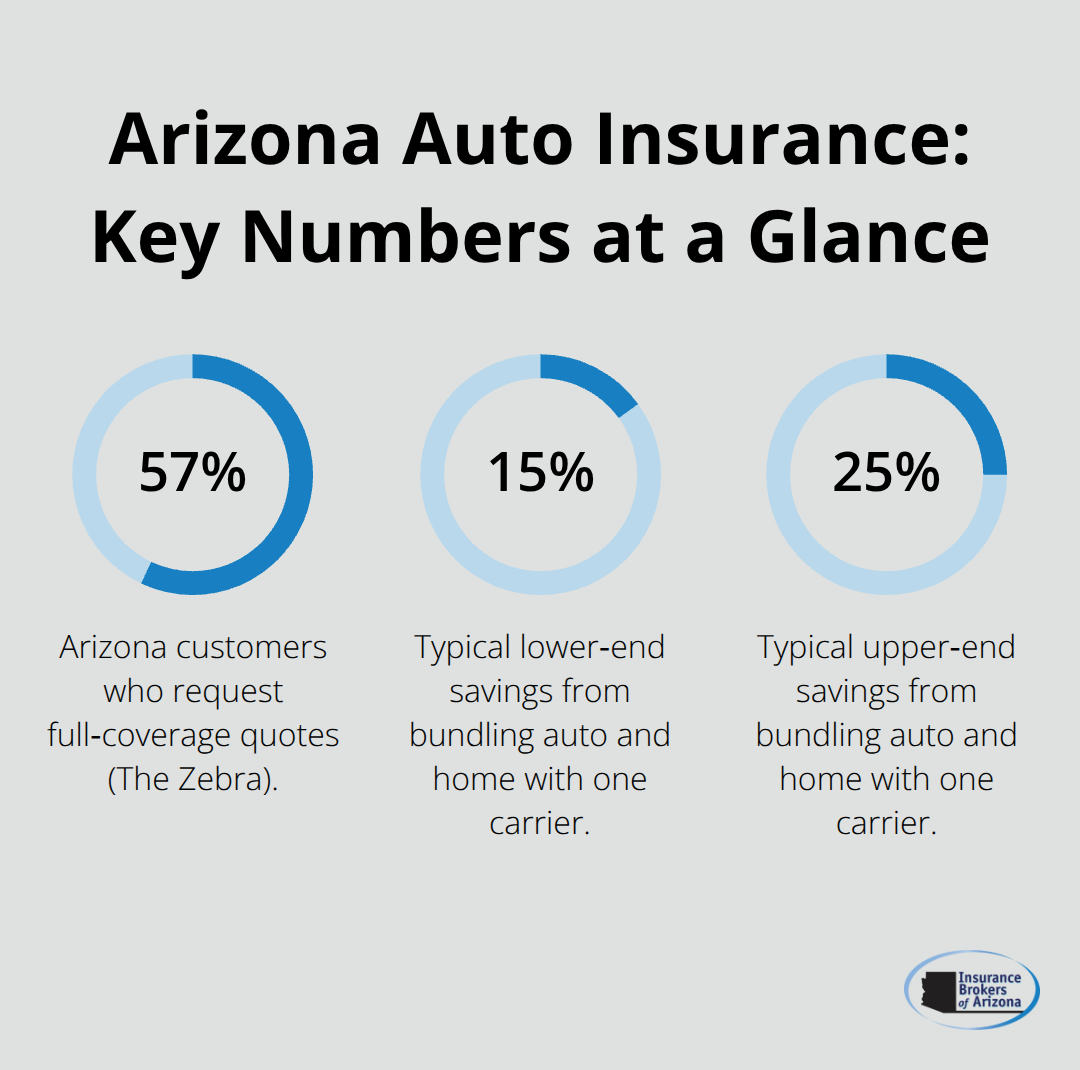

The Zebra reports that 57% of Arizona customers request full-coverage quotes, and those drivers understand something essential that liability-only buyers often don’t-the cost of a single accident or theft claim far exceeds years of premiums. Your quote shows you exactly what gap exists between your current coverage and actual protection.

Identifying Coverage Limits and Optional Add-Ons

If your liability limits sit at Arizona’s minimum of 25/50/15, your quote demonstrates what adding higher limits costs. Moving to 50/100/50 typically adds $15 to $30 monthly depending on your insurer, a modest increase that shields your assets if you cause serious injury. Your quote also reveals whether you’re paying for coverage you don’t need versus missing coverage you should have.

Uninsured motorist protection costs roughly $8 to $15 monthly but protects you against drivers with no insurance-essential in Arizona where uninsured motorist accidents remain common. No-deductible glass coverage, an Arizona-specific option, costs $10 to $20 extra but eliminates out-of-pocket costs for windshield damage. Your quote functions as a menu of what protection costs; comparing options across carriers shows you which insurers price these extras competitively and which ones overcharge.

Matching Coverage to Your Financial Situation

The real power of quotes emerges when you match them against your actual financial situation and asset value. If you owe $25,000 on your vehicle, your lender requires comprehensive and collision coverage, and your quote shows exactly how much that costs at different deductible levels. A $500 deductible might add $200 to your six-month premium compared to a $1,000 deductible, but only you know whether you can afford a $1,000 out-of-pocket expense after an accident.

Your quotes from multiple carriers reveal which insurers offer accident forgiveness programs-coverage that prevents your rate from jumping after your first at-fault crash. CSAA Insurance Group (AAA) in Arizona, ranked as the state’s top insurer by JD Power, offers competitive pricing on accident forgiveness, while other carriers charge extra for this protection or exclude it entirely.

Using Quotes as Negotiation Tools

This is where quotes become negotiation tools. Once you’ve collected three to five quotes and identified the carrier offering the best combination of price and features, contact that insurer directly and mention competing offers. Many Arizona insurers will match or beat a competitor’s quote, especially if you’re bundling auto with home insurance-bundling typically reduces your total cost by 15% to 25% according to standard industry practices.

Ask specifically whether the insurer offers discounts you haven’t claimed yet: good-student discounts, military service discounts, or usage-based telematics programs that track safe driving habits. The Zebra data shows that usage-based programs can yield 10% to 30% savings for low-mileage or consistently safe drivers. Your quote is a starting point for negotiation, not a final price.

Final Thoughts

Auto insurance quotes Arizona drivers collect today shape the coverage decisions that protect them tomorrow. Throughout this guide, we’ve shown you that quotes reveal far more than surface-level prices-they expose exactly what protection costs and where gaps exist in your current coverage. When you understand what drives your premium higher or lower, you control both your costs and your actual protection level.

Accurate quotes require specificity on your part. Provide identical vehicle information, driving history details, and coverage preferences to each carrier so you compare the same scenario across different insurers. Try collecting three to five quotes minimum to establish a realistic market range for your situation, and match your coverage limits and deductibles across all quotes so you’re truly comparing apples to apples rather than being misled by surface-level price differences.

At Insurance Brokers of Arizona®, we partner with over 40 reputable carriers, which means we access quotes and coverage options that individual shopping often misses. Contact Insurance Brokers of Arizona® with your vehicle information, driving history, and current coverage details, and we’ll translate those numbers into a policy that actually protects your assets while keeping your premiums competitive.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.