Cheapest Arizona Auto Insurance: Find the Best Deals

Arizona drivers pay an average of $1,547 annually for auto insurance, but rates vary dramatically based on your driving record, vehicle type, and personal factors. Finding the cheapest Arizona auto insurance requires understanding what insurers charge for and knowing how to compare quotes effectively.

At Insurance Brokers of Arizona®, we’ve helped countless drivers reduce their premiums through smart strategies like bundling policies, claiming available discounts, and adjusting coverage limits. This guide walks you through the exact steps to lower your costs without sacrificing the protection you need.

What Drives Your Arizona Auto Insurance Costs

Your Driving Record Shapes Your Premium Most

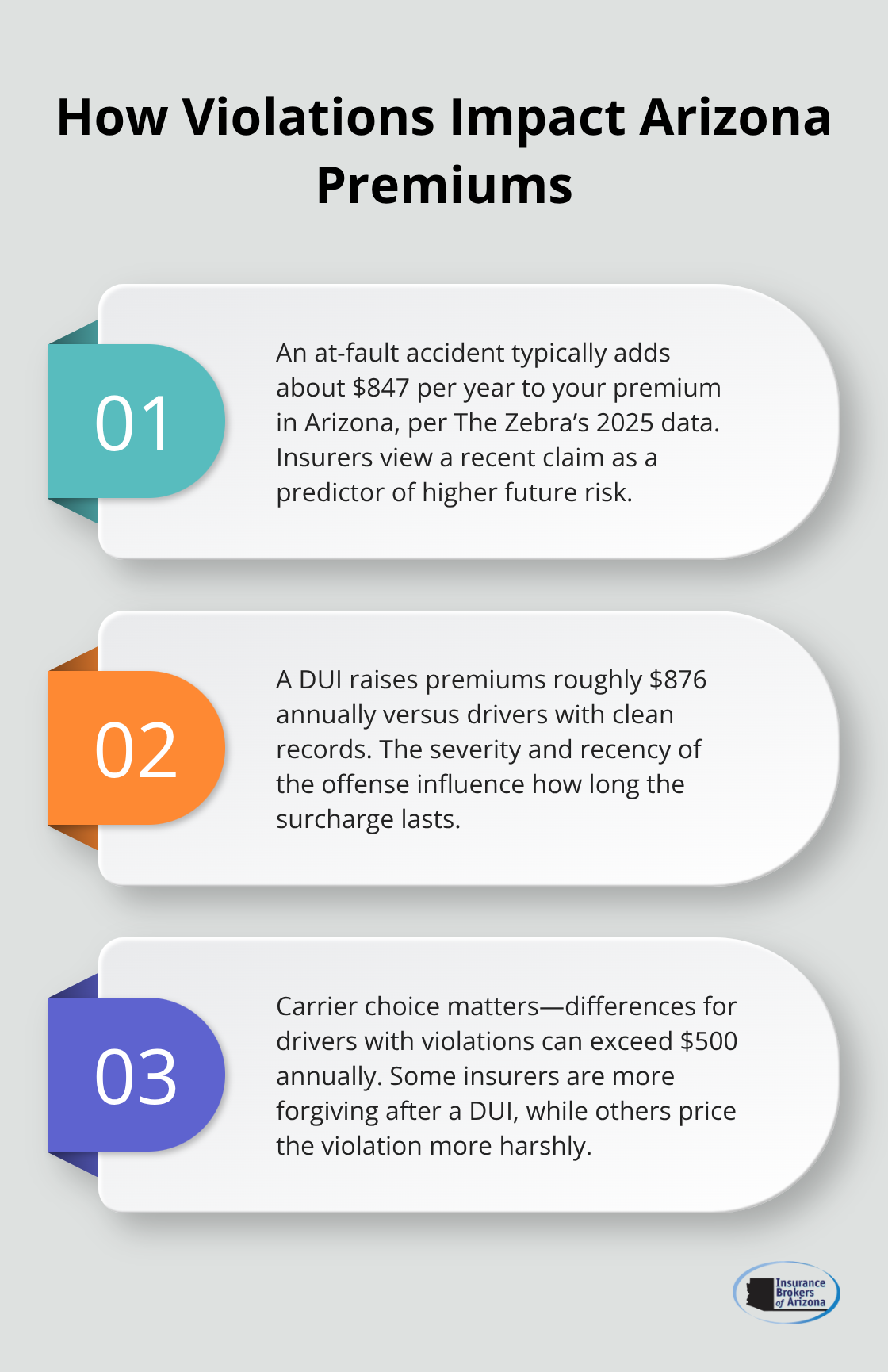

Your driving record stands as the single biggest factor insurers examine when calculating your premium. One at-fault accident raises your annual costs by roughly $847 on average, according to The Zebra’s 2025 data. A DUI conviction pushes premiums even higher-drivers with a DUI pay around $876 per year more than clean drivers. Insurers scrutinize your history carefully because they price in the statistical likelihood you’ll file another claim. Different carriers weight violations differently.

Progressive tends to be more forgiving after a DUI, while GEICO often charges more for the same violation. If your record has blemishes, shop aggressively-the difference between carriers can exceed $500 annually for drivers with violations.

Vehicle Type and Safety Features Lower Your Costs

The car you drive shapes your insurance cost dramatically. Safety features lower your premium because they reduce claim frequency. Anti-theft devices, forward collision warning systems, and automatic braking all signal lower risk to underwriters. Vehicle age and type also factor heavily; insuring a 2010 sedan costs substantially less than covering a brand-new sports car or luxury vehicle. If you’re shopping for a car specifically to reduce insurance costs, avoid high-performance models and recent model years. Older, practical vehicles with strong safety ratings deliver the lowest premiums. Before purchasing any vehicle, request insurance quotes for that specific make, model, and year. Some vehicles carry premiums 40 percent higher than similar alternatives simply due to repair costs or theft rates.

Age, Gender, and Credit Create Real Price Gaps

Teen drivers face astronomical rates-a 17-year-old male in Arizona pays roughly $3,176 annually on average, while a 17-year-old female pays $3,138 (The Zebra’s analysis). Adding a teen to a parent’s policy costs more than a solo teen policy but remains cheaper than insuring them separately. At age 25, premiums drop significantly; a 25-year-old male pays around $1,377 annually while a 25-year-old female pays $1,431. Gender pricing persists across age groups, though the gap narrows with maturity. Marital status also influences rates-married drivers typically qualify for lower premiums than single drivers of the same age. Credit score matters too; drivers with poor credit pay roughly $368 more annually than those with good credit (The Zebra). These demographic factors aren’t negotiable, but understanding them helps you anticipate your baseline cost and focus on the controllable factors like discounts and coverage choices.

Now that you understand what insurers charge for, the next step involves collecting quotes from multiple carriers to find where you’ll actually save the most money.

How to Compare Auto Insurance Quotes in Arizona

Comparing quotes from multiple carriers is where most Arizona drivers leave money on the table. You need the right information upfront, quotes from the right insurers, and the ability to spot which coverage levels actually make sense for your situation. Most drivers waste hours collecting quotes that aren’t apples-to-apples comparisons, then pick the wrong option. Here’s how to avoid that mistake.

Prepare Your Vehicle and Driving Details First

Before you request a single quote, gather your vehicle’s VIN, current mileage, and annual miles driven. Insurers need the exact make, model, year, and trim level because a 2020 Honda Civic EX costs differently than a 2020 Civic LX. Have your current insurance declarations page handy if you’re switching carriers. For your driving history, know exactly what violations appear on your record. The Zebra’s data shows one at-fault accident costs roughly $847 annually in increased premiums, but different carriers apply different surcharges. If you have a speeding ticket or DUI, know the date and severity. Some insurers offer more forgiveness for older violations than others. Write down your desired coverage limits before you request quotes. Arizona’s minimum liability is 25/50/15, but knowing whether you want $100,000 bodily injury limits or $300,000 helps you compare identical scenarios across carriers. Decide on deductible amounts too-typically $500 or $1,000 for collision and comprehensive. These details ensure quotes reflect your actual situation, not hypothetical scenarios.

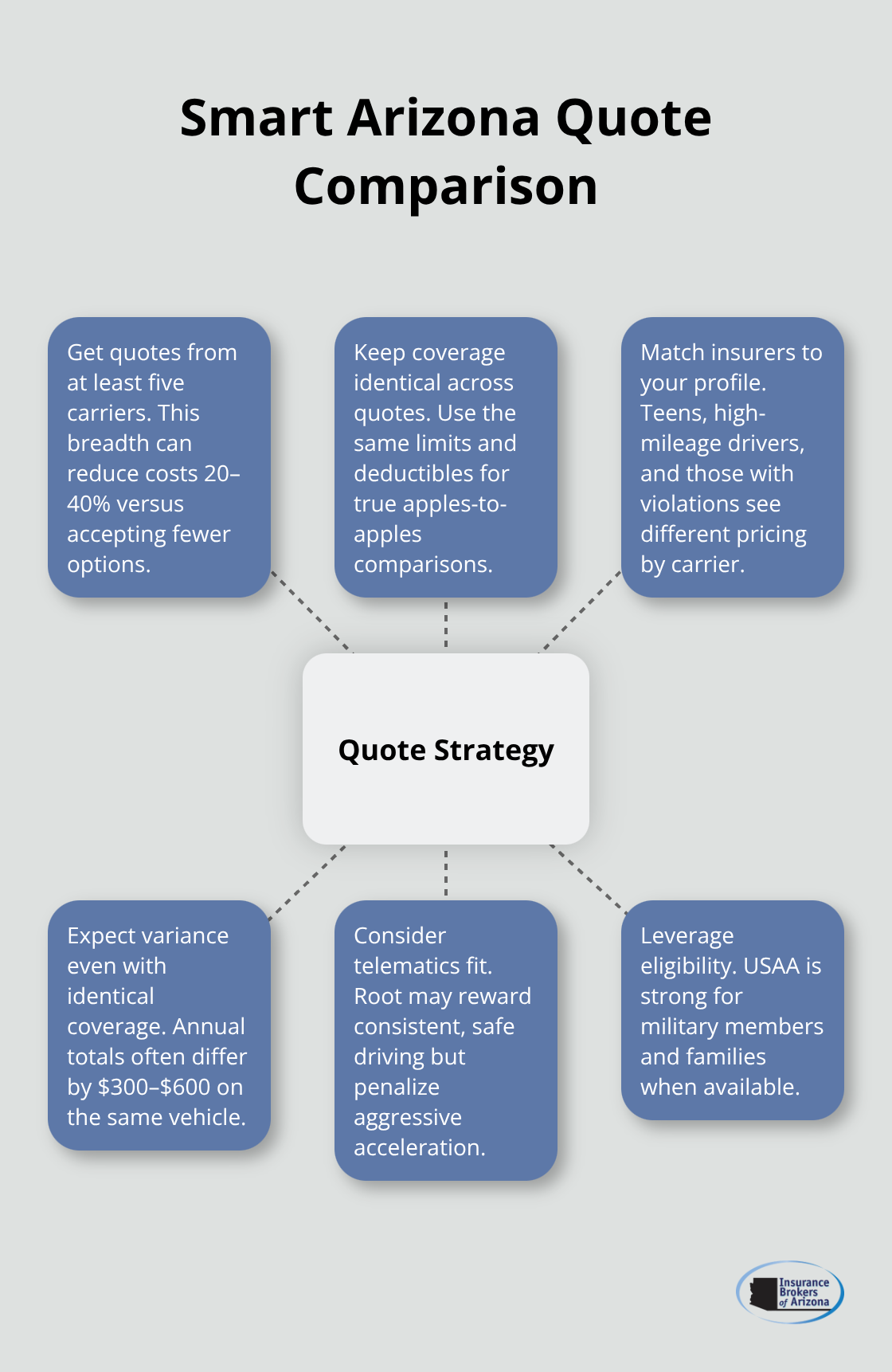

Request Quotes from At Least Five Carriers

Requesting quotes from at least five different insurance companies can reduce your costs by 20-40% compared to accepting fewer options. Root, Travelers, Progressive, GEICO, and USAA represent different pricing models and risk assessment strategies. Root’s telematics-based approach works well for safe drivers but may penalize aggressive acceleration patterns. Travelers offers competitive rates across multiple driver profiles and age groups. USAA exclusively serves military members and their families but typically delivers strong pricing for that population. You should get quotes from carriers that serve your specific situation. Teen drivers should compare Travelers, which averages roughly $315 monthly for Arizona teens, against Root and other carriers. High-mileage drivers should request quotes from Travelers, which often prices low-mileage drivers at around $1,334 annually. Drivers with violations need Progressive and Root quotes specifically because they handle surcharges differently than other carriers. You must request quotes using identical coverage levels, deductibles, and limits across all carriers. A quote comparison fails if you’re comparing $100,000 liability limits at one insurer against $50,000 at another. Most insurers provide online quote tools that take 10 minutes. Some require phone calls.

Expect quotes to vary by $300 to $600 annually for identical coverage on the same vehicle-that’s real money worth the time investment.

Compare Total Cost, Not Just Monthly Payment

The lowest monthly payment often masks higher annual costs or inferior coverage choices. A carrier charging $95 monthly might require a $1,000 deductible while another charges $110 monthly with a $500 deductible. After one accident, the $500 deductible saves you $500 out-of-pocket. You should calculate the total annual cost for each quote, then factor in deductible implications for your situation. If you drive safely and rarely file claims, a $1,000 deductible lowers your premium meaningfully. If you park on the street in a high-theft neighborhood, a $500 deductible provides better value despite higher premiums. Check which discounts each carrier offers and whether you qualify. Good-driver discounts, bundling home and auto policies, paying in full upfront, and multi-car discounts all reduce costs. One carrier might offer a 15 percent bundling discount while another offers 10 percent. GEICO offers good-student discounts in Arizona, as does Progressive. Some carriers discount for safety features or anti-theft devices. You must verify the discount applies to your vehicle and situation before you decide. The cheapest quote means nothing if you don’t qualify for the discounts factoring into that price.

Spot Hidden Fees and Policy Conditions

Beyond the premium itself, insurers charge fees that inflate your actual cost. Some carriers impose policy fees ($50 to $100 annually), payment plan fees, or cancellation fees. A quote that looks cheap might include a $75 annual policy fee that another carrier doesn’t charge. Read the fine print on each quote to identify these hidden costs. You should also check cancellation policies-some carriers penalize you for switching mid-term, while others allow free cancellation. Accident forgiveness programs vary significantly across carriers. Some forgive your first accident, while others require you to maintain a clean record for three to five years before they apply forgiveness. If you have a recent accident, this difference matters enormously. You should also verify how each carrier handles rate increases. Some carriers lock rates for a year, while others adjust them quarterly. In Arizona, where premiums rose $232 from 2023 to 2024 according to The Zebra, rate stability provides real value.

Now that you’ve collected quotes and understand the true cost of each option, the next step involves selecting the coverage levels and limits that actually protect your financial situation.

Money-Saving Strategies for Arizona Auto Insurance

Bundle Home and Auto Policies for Maximum Savings

Consolidating your home and auto policies with a single carrier cuts your annual costs substantially. Drivers who bundle typically save 15 to 25 percent on their combined premiums. GEICO offers bundling discounts in Arizona, as do Progressive, Travelers, and most major carriers. Insurers reduce their acquisition costs when they retain multiple policies from one customer, and they pass those savings to you.

If you currently split home and auto coverage between two carriers, consolidating saves real money. Request quotes for bundled home and auto coverage from at least three carriers, then compare the total annual cost against your current separate policies. Many drivers discover they save $300 to $500 annually just through consolidation, even if the auto premium alone appears slightly higher than a competitor’s standalone rate.

Claim Discounts That Stack and Compound

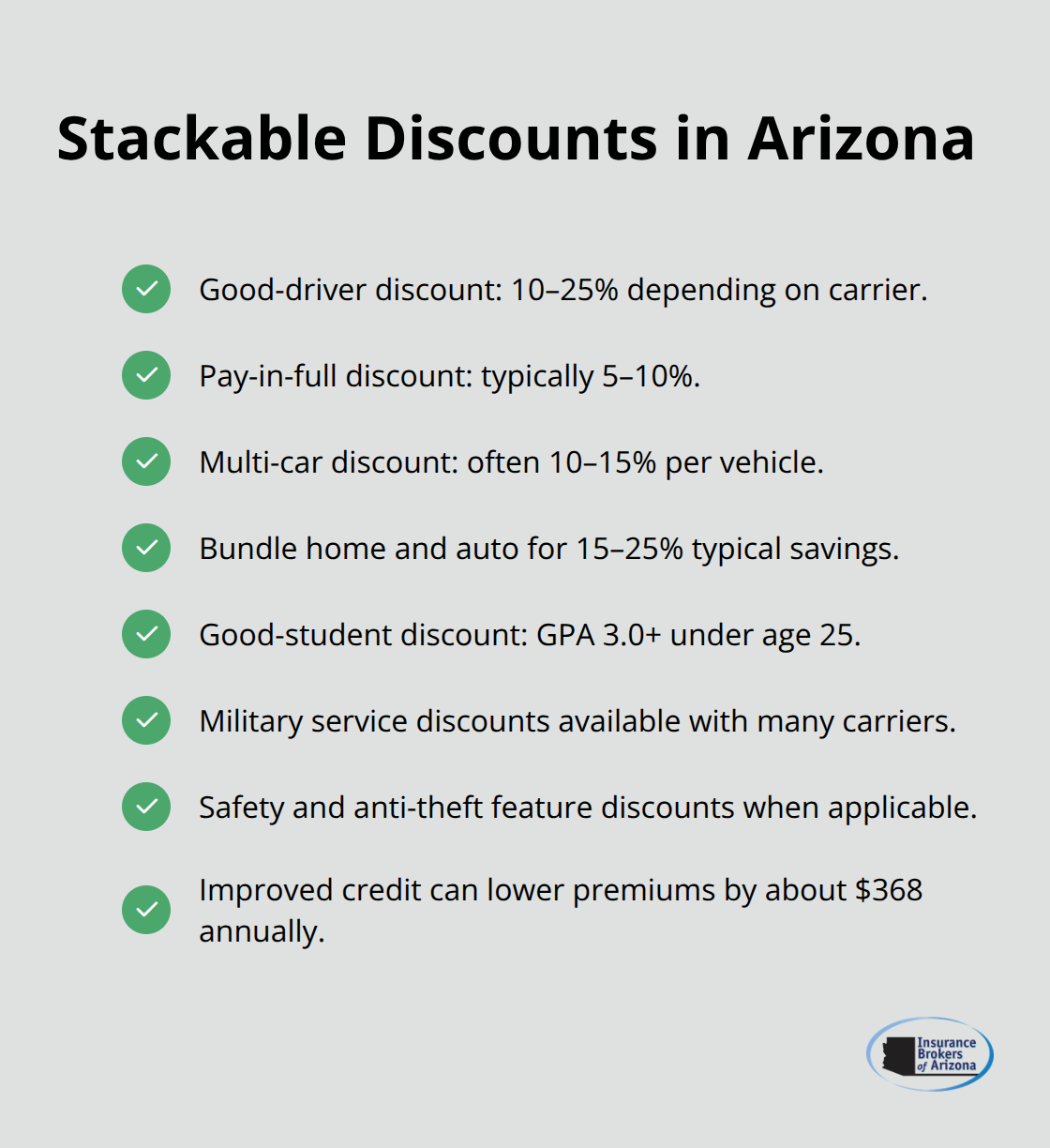

Safe driving records and good credit scores unlock discounts that stack on top of your base premium. Drivers with clean records qualify for good-driver discounts ranging from 10 to 25 percent depending on the carrier. GEICO, Progressive, and Travelers all offer these discounts in Arizona. Credit scores matter equally-The Zebra’s data shows drivers with poor credit pay roughly $368 more annually than those with good credit. Improving your credit score before requesting quotes directly reduces your premiums.

Paying your premium in full upfront rather than monthly installments typically saves 5 to 10 percent. Multi-car discounts apply when you insure two or more vehicles with the same carrier, often delivering 10 to 15 percent savings per vehicle. Good-student discounts apply to drivers under 25 with a GPA of 3.0 or higher. Military service qualifies you for discounts with most carriers.

These discounts compound-a driver with multiple qualifications can reduce their premium by 40 to 50 percent through stacking discounts alone.

Adjust Deductibles to Match Your Financial Reality

Raising your collision and comprehensive deductibles from $500 to $1,000 typically cuts your premium by 15 to 30 percent. If you have $5,000 in emergency savings and drive safely in low-crime areas, the higher deductible makes financial sense. After an accident, you’ll pay $1,000 out-of-pocket instead of $500, but you’ll have paid significantly less in premiums over multiple years. The math only works if you can genuinely afford that deductible without financial hardship. Drivers without emergency savings should maintain $500 deductibles despite higher premiums.

Select Liability Limits That Protect Your Assets

Lowering your liability limits below Arizona’s minimum of 25/50/15 is financially reckless and illegal, but selecting liability limits above the minimum requires careful thought. Arizona’s 25/50/15 minimum leaves you dangerously underinsured-a serious accident with medical costs exceeding $50,000 forces you to pay the difference personally. Most drivers with assets to protect should try 100/300/100 limits instead. The premium difference between 25/50/15 and 100/300/100 typically runs $15 to $30 monthly, yet the protection difference is enormous.

Comprehensive and collision deductibles affect your actual out-of-pocket cost after a claim far more than they affect your monthly premium. Prioritize affordability over premium minimization when selecting deductibles, since you’ll actually pay that deductible if an accident occurs.

Final Thoughts

Finding the cheapest Arizona auto insurance requires three concrete steps: understanding what insurers charge for, collecting quotes from multiple carriers using identical coverage levels, and strategically adjusting deductibles and limits to match your financial situation. Your driving record, vehicle type, age, and credit score shape your baseline costs, while bundling policies, stacking discounts, and selecting appropriate deductibles control what you actually pay. The difference between shopping aggressively and accepting the first quote you receive typically exceeds $300 annually.

Your coverage needs change over time, especially after major life changes like marriage, purchasing a home, or significant income increases. Arizona’s minimum liability of 25/50/15 provides legal compliance but inadequate protection for most drivers, so you should review your policy annually. If you’ve maintained a clean driving record for three years, ask your carrier about accident forgiveness programs, and if you’ve improved your credit score, request a new quote since your premium should decrease.

At Insurance Brokers of Arizona®, we work with over 40 carriers to find coverage that fits your specific situation and budget. Rather than spending hours collecting quotes yourself, our team handles the comparison work and secures the best rates available for the cheapest Arizona auto insurance. Contact us today to discover how much you can save.