Family auto insurance costs add up fast. Between multiple drivers, vehicle coverage, and monthly premiums, many households struggle to find affordable auto insurance for families without sacrificing protection.

We at Insurance Brokers of Arizona® know the frustration. That’s why we’ve put together practical strategies to lower your rates, compare quotes effectively, and keep your family covered without overspending.

What Actually Drives Your Auto Insurance Rates

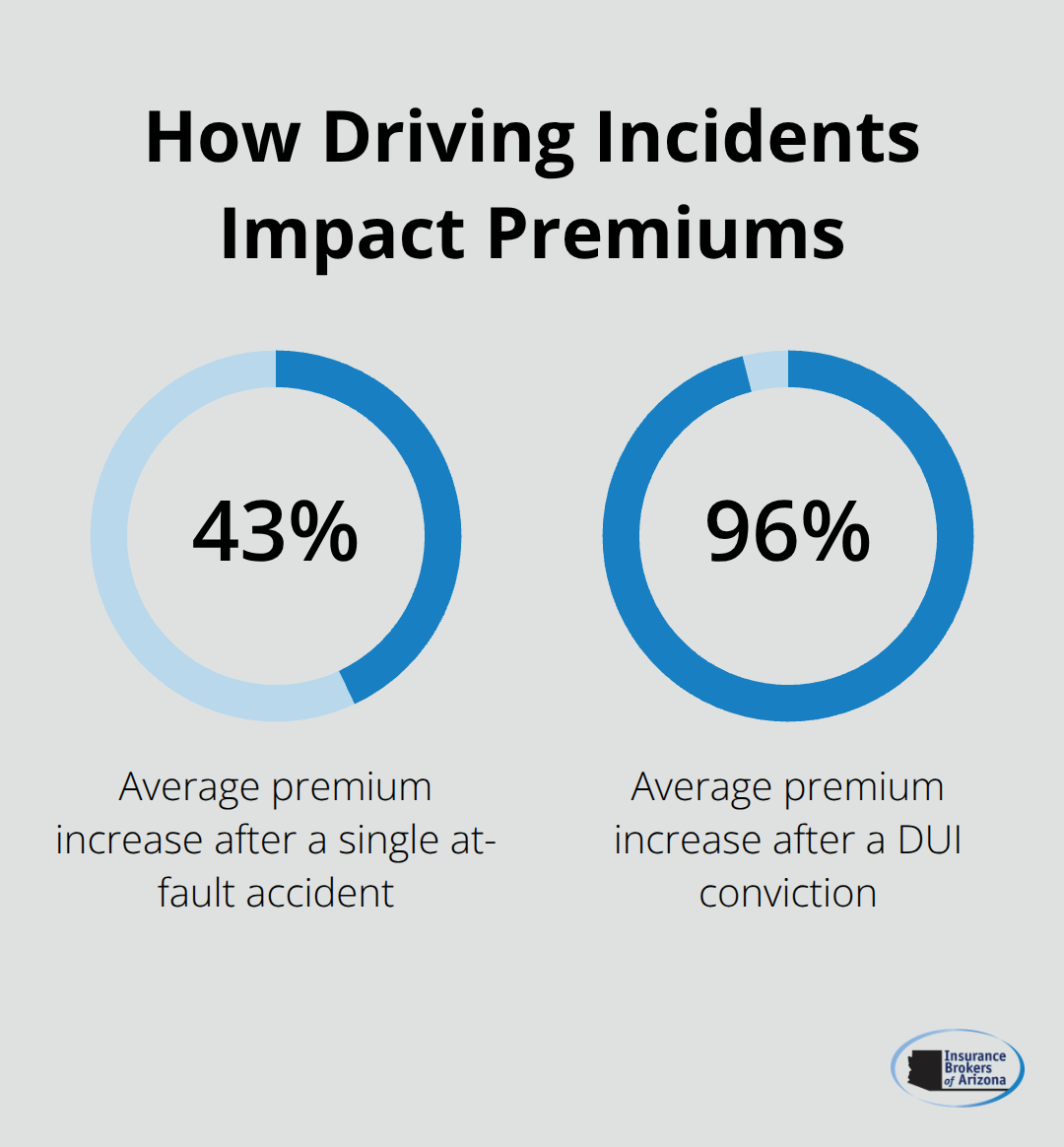

Your driving record is the single biggest lever you control. A clean record costs money-lots of it. According to Bankrate data via Quadrant Information Services, a single at-fault accident raises your premiums by roughly 43%, and a DUI conviction pushes costs up about 96% compared with a clean record. Insurers won’t negotiate this. Even one mistake stays on your record for years, so defensive driving isn’t optional if you want affordable rates.

If you’ve had incidents, focus on staying claim-free moving forward. That good-driver discount kicks in after you prove you won’t file claims, and it stacks with other discounts.

How Your Vehicle Choices Impact What You Pay

The car itself matters more than most families realize. A Tesla Model 3 costs about $285 per month for full coverage, while a Toyota Prius runs $231 and a Ford F-150 costs $219, according to Bankrate’s 2025 analysis. The difference comes down to repair costs and parts availability. High-end vehicles, sports cars, and newer EVs all cost significantly more to insure because parts are expensive and specialized repair shops charge premium labor rates. An older sedan costs less to insure than a brand-new truck, period. For families with teen drivers, this matters even more. Choosing a used sedan instead of a new vehicle can meaningfully lower your teen’s premiums. Vehicle age also factors in-older cars cost less to insure, so purchasing a clunker for a teen driver makes financial sense.

Location and How Far You Drive Changes Everything

Where you live and how much you drive determine a massive portion of your rate. The cheapest states for full coverage in 2025 are Idaho, Vermont, Hawaii, Maine, and New Hampshire, where premiums run roughly 38% to 45% below the national average of $2,697 annually. Louisiana, New York, Florida, Nevada, and New Jersey are the most expensive, with premiums up to 53% above average. You can’t move to save money on insurance, but you can reduce your annual mileage. A low-mileage discount applies when you drive under roughly 7,500 miles per year. If you work from home or your commute is short, you qualify for this discount. Commute distance directly affects accident risk and claim frequency, so insurers reward shorter drives with lower rates.

What Comes Next: Taking Action on These Factors

Understanding what drives your rates is half the battle. The other half involves taking concrete steps to lower what you actually pay each month. Your driving record, vehicle choice, and location set the foundation, but your next move determines whether you’ll pay full price or unlock real savings through smart strategy choices.

How to Cut Your Family’s Auto Insurance Bill in Half

Stack Discounts by Bundling Policies

Bundling your home and auto policies with the same insurer cuts what you pay each month faster than any other single move. Homeowners who bundle with auto typically save about 10% on average across policies, according to The Zebra’s analysis. On a $2,697 annual full-coverage premium, a 10% bundling discount saves you roughly $270 per year. Some families see even larger reductions-Bankrate reports that bundling auto with homeowners or renters insurance can reduce premiums by up to 35% compared with holding separate policies from different carriers.

One insurer covering multiple lines of business has lower acquisition costs and retention risk, so they pass savings to you. If you currently have home or renters coverage elsewhere, call your agent and ask for a bundling quote. You’ll almost always come out ahead.

Leverage Good Grades and Safe Driving Records

Safe driving and good grades unlock real money for families with teen drivers. A good student discount applies to teens maintaining a 3.0 GPA or higher and saves about $283 per year on average, according to data from The Zebra. For a 16-year-old whose annual premium averages $5,744, that $283 discount is meaningful. Defensive driving courses also reduce premiums when you complete an insurer-approved safe driving program, though the exact savings varies by company. More importantly, staying claim-free triggers a good-driver discount that compounds over time. A single claim can cost you dearly-a 43% premium increase for an at-fault accident-so avoiding claims matters far more than chasing small discounts.

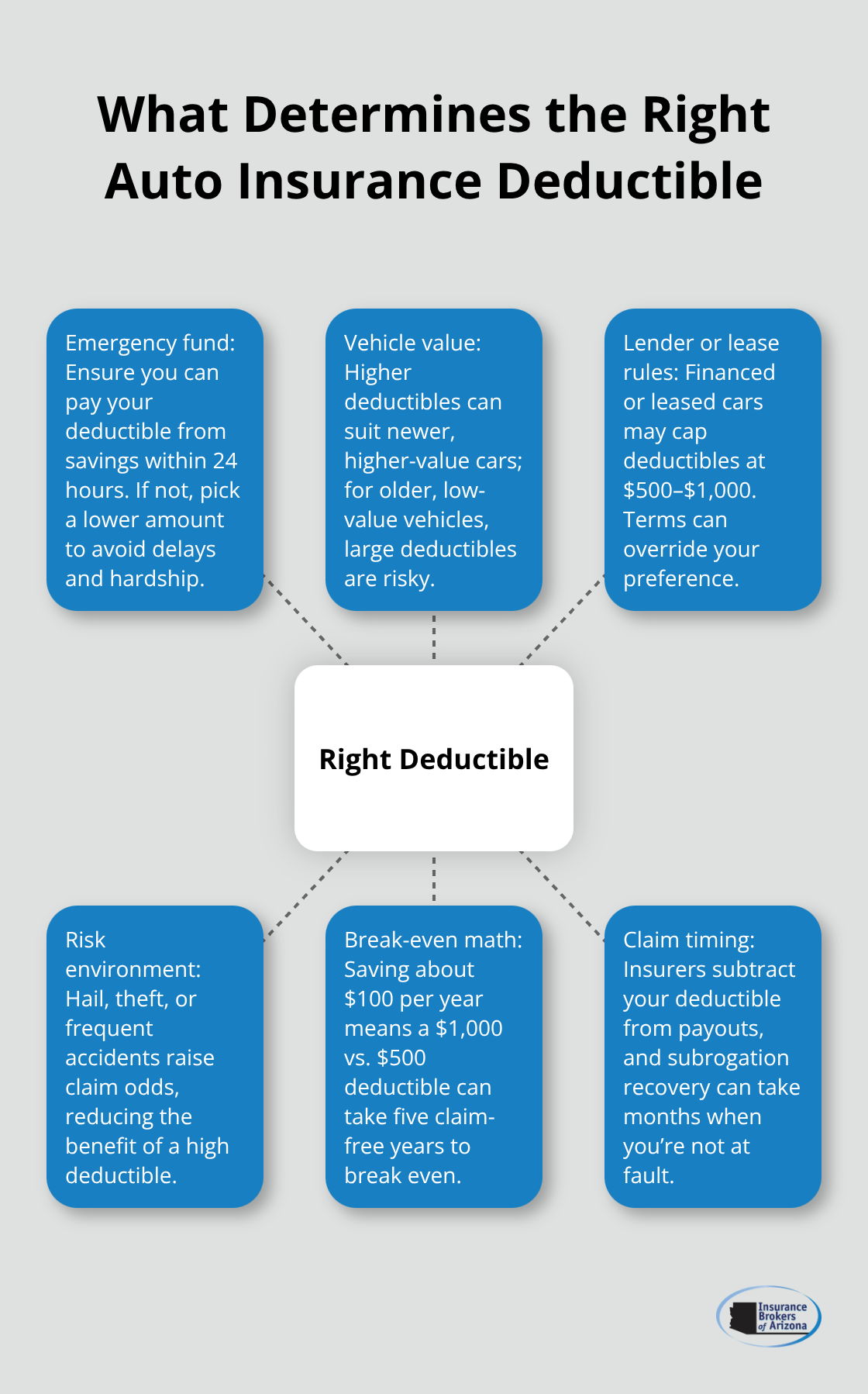

Raise Your Deductible to Lower Monthly Costs

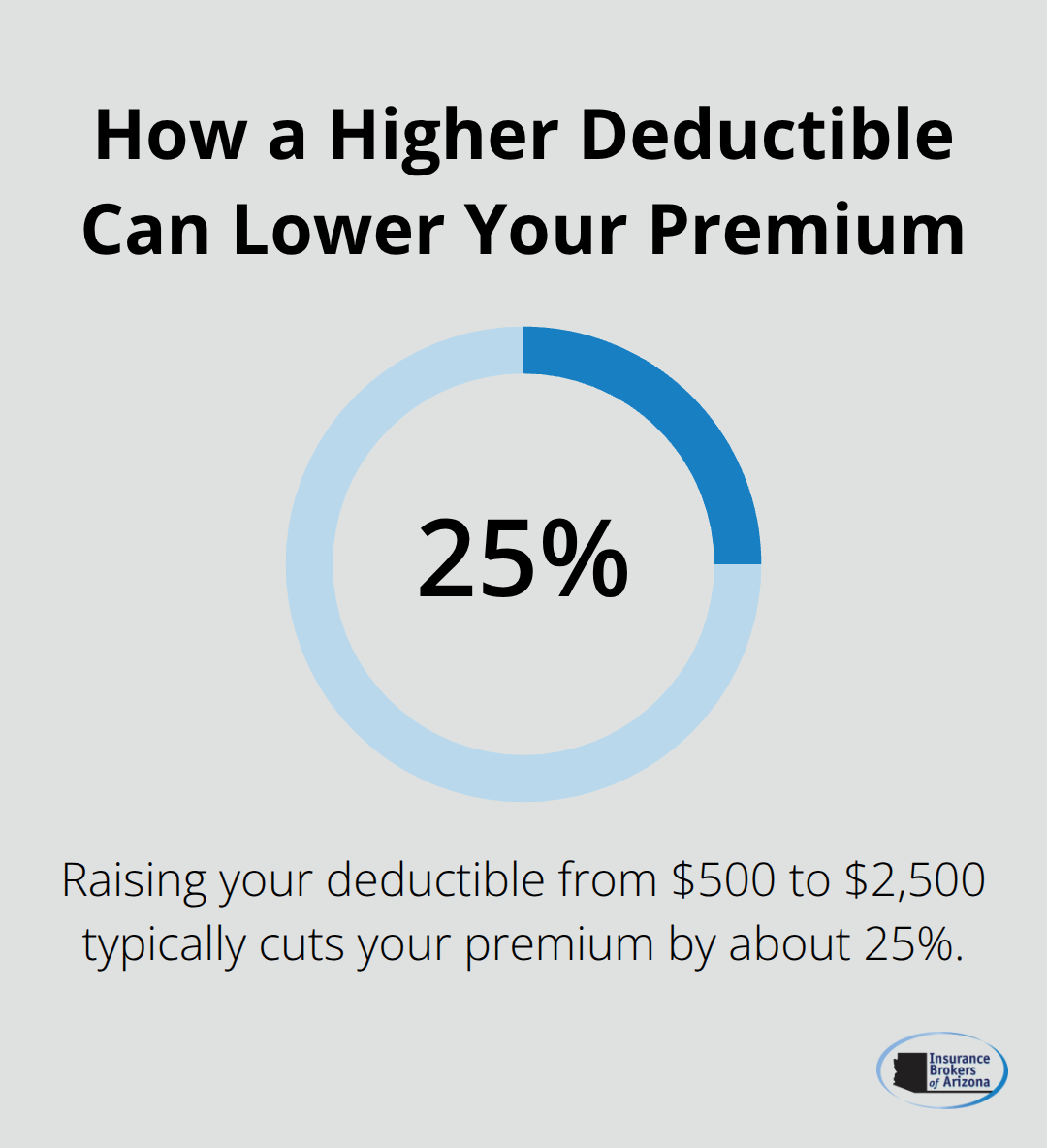

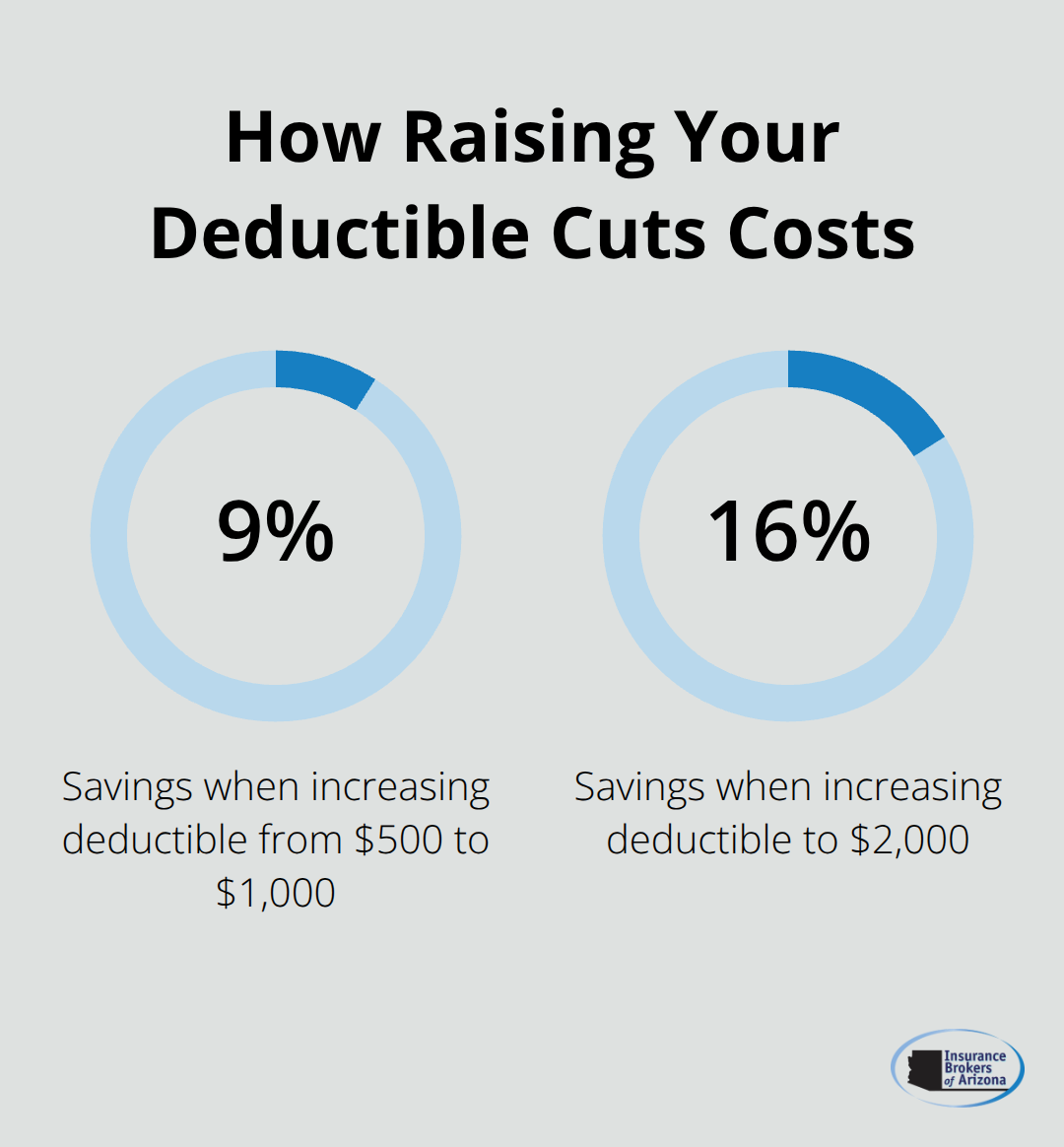

Increasing your deductible from $500 to $1,000 cuts costs by roughly 9%, and jumping to a $2,000 deductible saves about 16%, according to Bankrate’s 2025 analysis. For a 16-year-old, that $2,000 deductible could mean $919 in annual savings. The trade-off is straightforward: you pay more out of pocket if you file a claim, but you pay significantly less in monthly premiums.

If your family has an emergency fund and can cover a $2,000 deductible without hardship, this move makes sense. Your deductible should match your ability to pay, not some arbitrary rule. The bundling discount you secured stacks with this deductible strategy, meaning your savings compound when you combine multiple approaches.

Combine Multiple Strategies for Maximum Savings

The real power emerges when you layer these tactics together. A family that bundles policies, qualifies for a good student discount, and raises their deductible from $500 to $2,000 captures savings across three separate levers simultaneously. Each discount stacks independently, so your total savings multiply rather than stay flat. The next step involves comparing what different insurers actually charge for your specific situation, since rates vary dramatically by carrier and location.

Comparing Quotes and Choosing the Right Coverage

Getting multiple quotes is non-negotiable if you want competitive rates, but most families approach this wrong. They request one or two quotes, see a number, and assume that’s the market price. Rates vary wildly by carrier and location. According to The Zebra’s analysis of over 83 million insurance rates nationwide, the same driver in the same ZIP code can see premiums that differ by hundreds of dollars depending on which insurer quotes them. GEICO, Nationwide, and Erie are often among the cheapest carriers on average, but individual results depend entirely on your specific situation-your driving history, vehicle, age, and claims background.

Request Quotes from Multiple Carriers

When you shop for insurance, collect quotes from at least three to five major carriers, not one or two. Most insurers offer free quotes online in under five minutes, so there’s no reason to skip this step. Compare the exact same coverage limits across all quotes so you’re actually comparing apples to apples. If one quote includes a $1,000 deductible and another uses $500, you’re not seeing the real price difference. Request the same liability limits, collision coverage, and comprehensive coverage from each carrier, then line up the monthly costs side by side. You’ll spot which insurers price your profile favorably and which ones don’t.

Understand What Each Coverage Type Protects

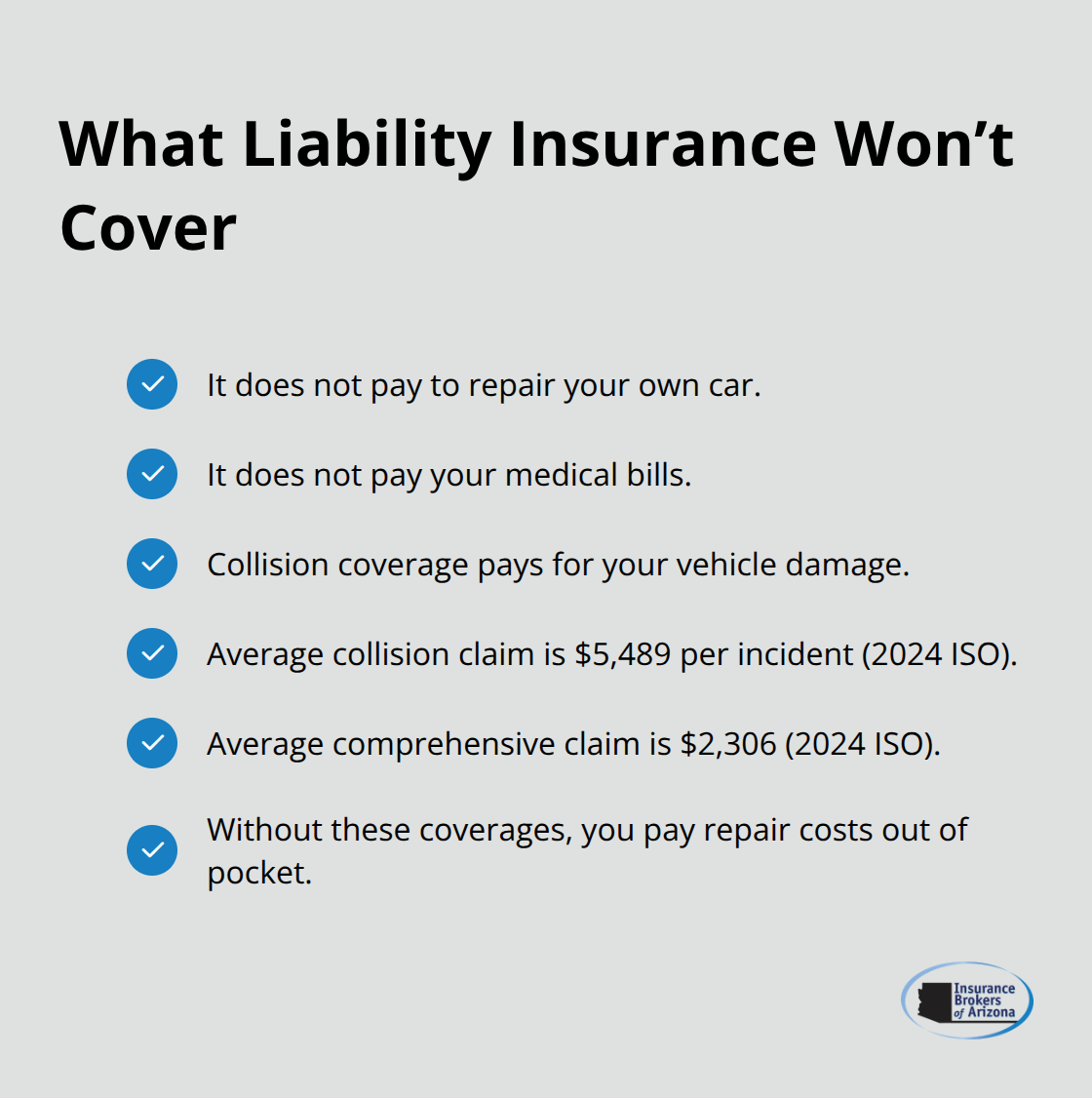

Full coverage means collision and comprehensive protection on top of liability, and it costs roughly $2,697 per year on average nationally according to Bankrate’s 2025 data, compared to minimum liability-only coverage at about $820 per year. If you finance or lease your vehicle, your lender requires full coverage, so you don’t have a choice. If you own your car outright, the decision hinges on your vehicle’s value and your financial cushion. An older car worth $3,000 doesn’t justify $200 monthly premiums for collision and comprehensive coverage. A newer vehicle worth $25,000 absolutely does.

The real mistake families make is keeping coverage they don’t need or dropping coverage they should keep. Collision pays for accidents you cause, comprehensive covers theft and weather damage, and liability covers damage you cause to others. Your deductible applies to collision and comprehensive only, not liability. When you raise your deductible to $2,000 as discussed earlier, that savings only applies to these two coverages.

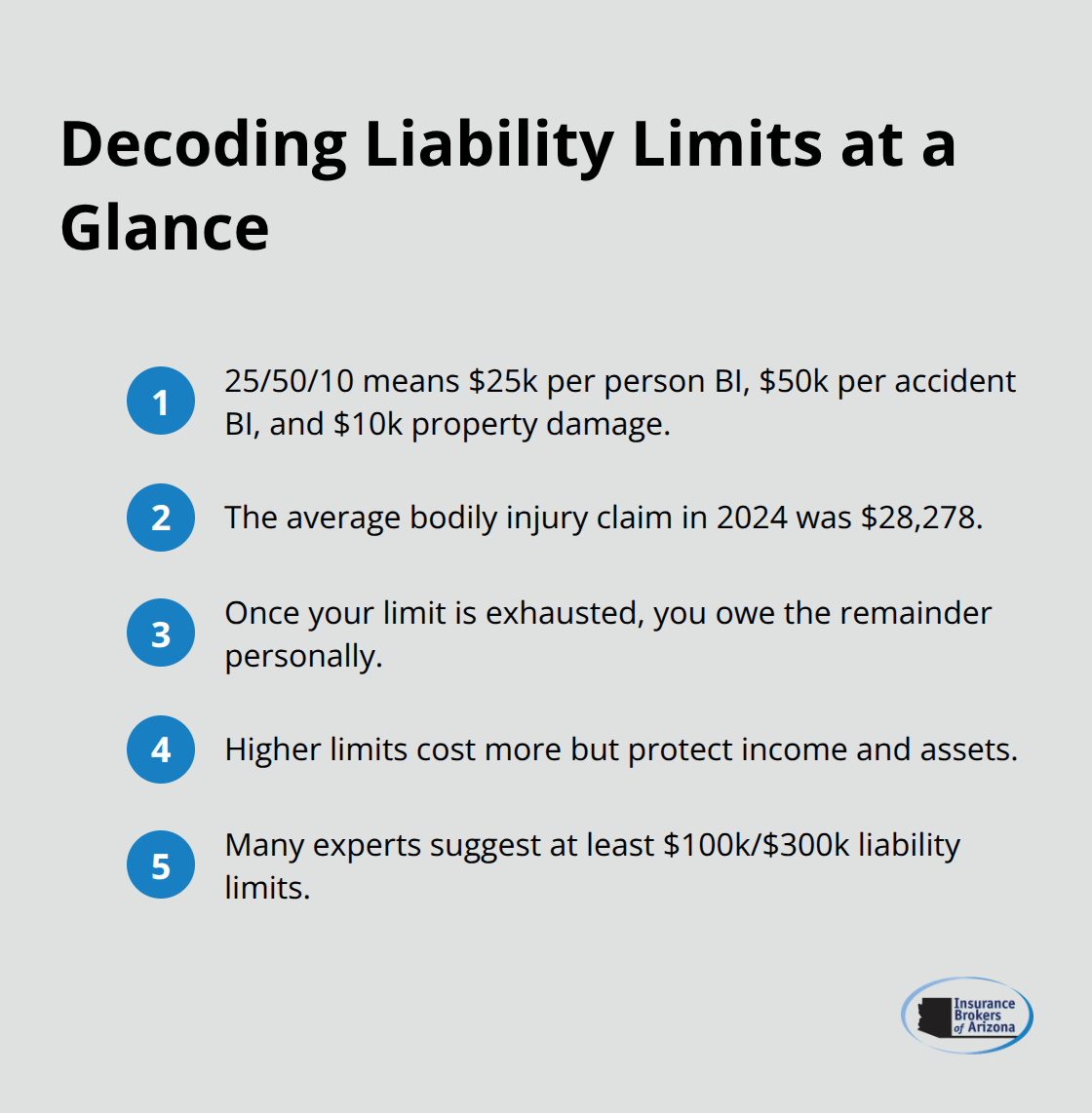

Set Liability Limits That Match Your Assets

Liability limits should match your assets and risk exposure. If you own a home, carry at least $100,000 in bodily injury liability per person and $300,000 per accident, or you risk losing everything in a lawsuit. These limits protect your financial future when you cause serious injury or property damage to someone else. Most families underestimate their exposure and carry inadequate limits to save a few dollars monthly. That decision can cost you hundreds of thousands in a major accident.

Review Your Policy Annually for Missed Savings

Annual policy reviews catch coverage gaps and identify savings you’ve missed since last renewal. Your situation changes-your car ages, your driving record improves, or you move to a safer neighborhood. These changes can lower your rates, but your insurer won’t automatically adjust your premium downward. You must request new quotes and compare them to what you currently pay. Many families stay with the same carrier for years without realizing they could save $50 to $100 monthly by switching or negotiating a better rate.

Final Thoughts

Finding affordable auto insurance for families requires action, not just reading. You now understand what drives your rates, how to stack discounts, and why comparing quotes matters. The strategies in this guide work because they address the real factors insurers use to price your coverage, and a clean driving record, smart vehicle choices, bundling policies, and raising your deductible create compounding savings that add up to hundreds of dollars annually.

Don’t settle for one or two quotes when you shop for coverage. Request quotes from at least three to five carriers using identical coverage limits, then compare the actual monthly costs side by side. Your situation is unique, and rates vary dramatically by insurer and location-a carrier that charges $150 monthly for one family might quote $220 for another in the same ZIP code.

We at Insurance Brokers of Arizona® work with over 40 reputable carriers, which means we can access competitive options you might not find on your own. Contact Insurance Brokers of Arizona® to start comparing quotes today, and our agents will walk you through coverage options, explain what each type protects, and show you exactly where you can cut costs without sacrificing protection for your family.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.