Auto Liability Insurance Coverage Explained

Auto liability insurance covers the costs when you’re found responsible for injuring someone or damaging their property in a car accident. Yet many drivers misunderstand what this coverage actually protects-and what it doesn’t.

Here at Insurance Brokers of Arizona®, we’ve seen firsthand how confusion about liability limits leads to serious financial exposure. This guide breaks down exactly how auto liability insurance works, what your state requires, and how to avoid costly coverage gaps.

What Auto Liability Insurance Covers

Auto liability insurance splits into two distinct parts that work together to cover costs when you cause an accident. Bodily injury liability pays for medical expenses, lost wages, pain and suffering, and legal fees when someone gets hurt because of your at-fault accident. Property damage liability covers repairs to the other driver’s vehicle, damage to buildings, fences, or other property destroyed in the collision. Liability never pays for your own injuries or vehicle damage-only for what you owe to the other party. Every state requires both components, though the minimum amounts vary significantly. Florida drivers must carry at least $10,000 in bodily injury per person coverage, while California requires only $15,000. Louisiana and New York sit at $15,000 and $25,000 respectively. Your state’s minimum represents the legal floor, not a recommendation for adequate protection.

Understanding Liability Limits in Practice

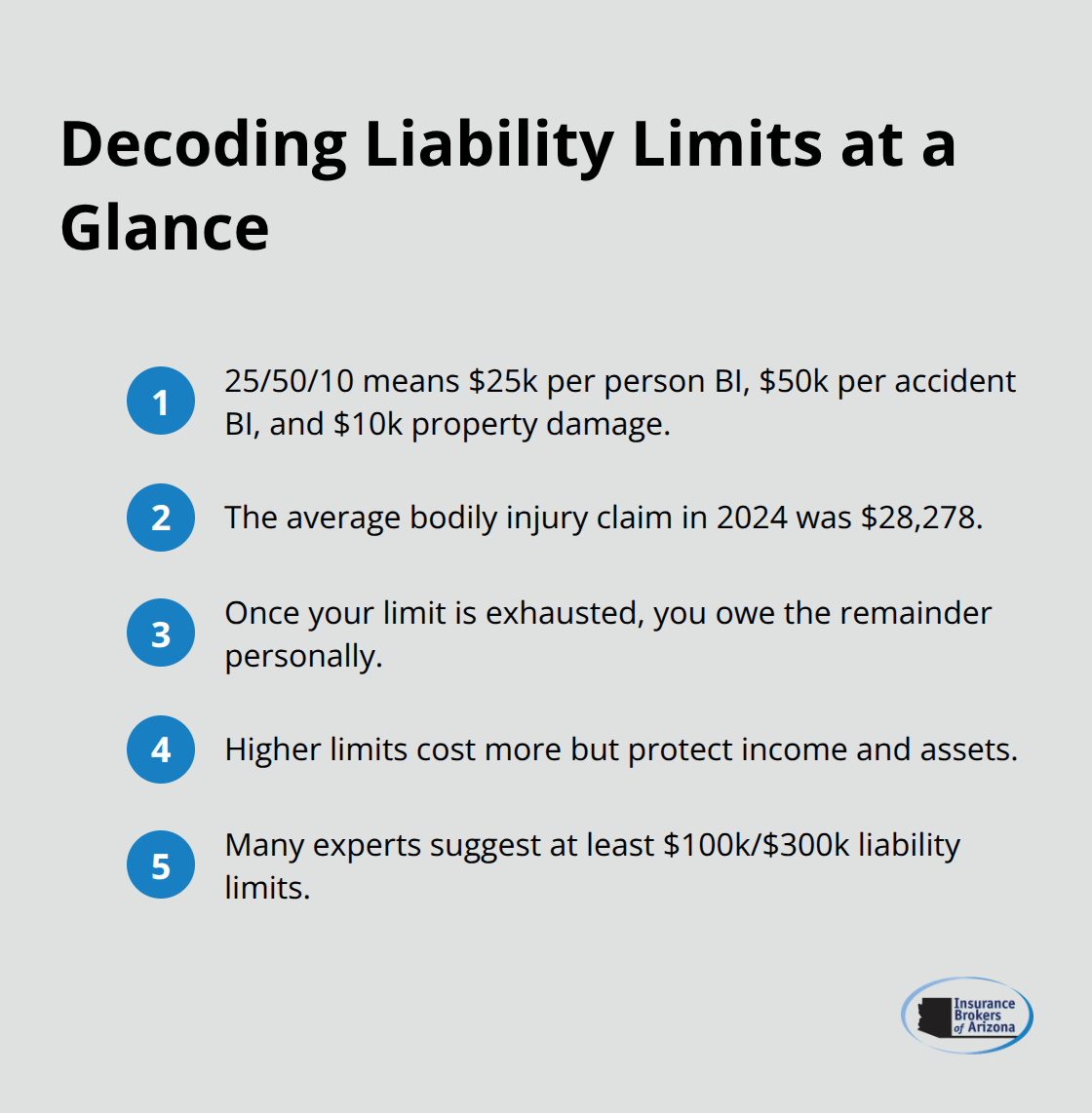

Most policies show liability limits as three numbers, such as 25/50/10, which means $25,000 per person for bodily injury, $50,000 total per accident for bodily injury, and $10,000 for property damage. According to ISO data from 2024, the average bodily injury claim costs $28,278-already exceeding many state minimums and standard limits. This matters because once your policy limit exhausts, you personally owe the remaining balance.

If someone accumulates $75,000 in medical bills and your policy covers only $50,000, you’re liable for the $25,000 difference from your own assets. Higher limits cost more upfront but protect your paycheck and savings when serious injuries occur. Financial experts recommend liability limits of at least $100,000 per person and $300,000 per accident to protect against these scenarios.

How Limits Interact With Real Accident Costs

State minimums exist primarily to meet legal requirements, not to protect your assets. A practical guideline suggests selecting limits that match or exceed your net worth, ensuring your house, savings, and retirement accounts stay protected if someone sues. If your net worth is $300,000, carrying only $25,000 in bodily injury coverage leaves you exposed to massive personal liability. The 2024 average collision payment reached approximately $10,000 per claim according to Highway Loss Data Institute data, and serious multi-person accidents routinely exceed $100,000 in total costs. An umbrella policy extends protection beyond your auto liability limits for roughly $150 to $300 annually per million dollars of coverage, offering affordable additional security.

Why Adequate Coverage Protects Your Financial Future

Underinsured drivers face devastating consequences when accidents exceed their policy limits. A single serious injury claim can wipe out years of savings and trigger wage garnishment or asset seizure. Your liability coverage directly determines how much financial exposure you carry personally. The difference between state minimums and adequate limits often amounts to just a few dollars per month in premium increases. Discussing your specific financial situation with a licensed agent helps you select limits that actually protect what you’ve built, rather than defaulting to state minimums that leave gaps. This conversation becomes even more important as you consider what happens when your coverage limits prove insufficient for the actual damages involved.

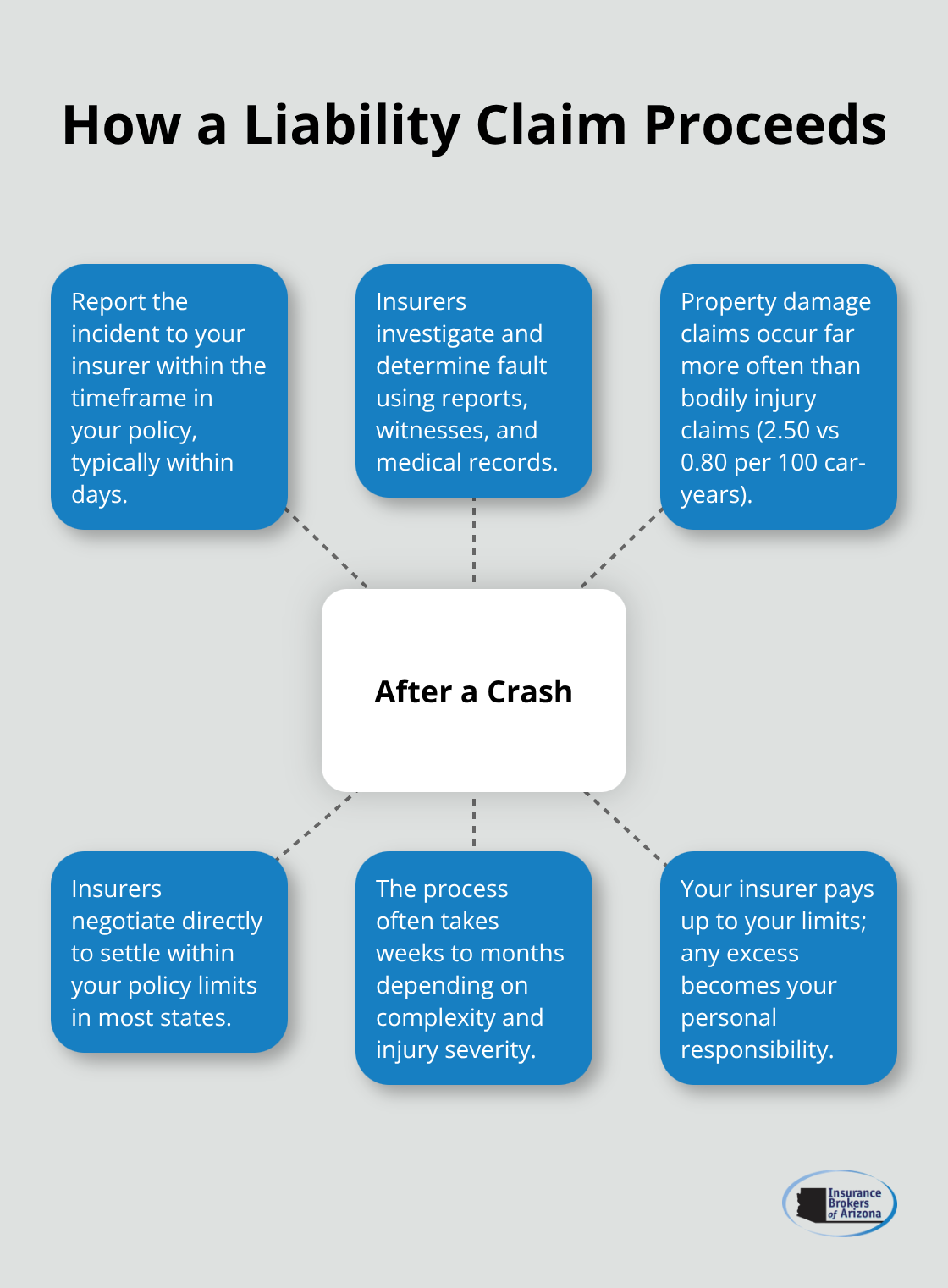

How Your Liability Coverage Works After an Accident

The moment you cause an accident, your liability coverage activates and follows a specific sequence. You report the incident to your insurer within the timeframe specified in your policy, typically within days of the accident. Your insurer then contacts the other driver’s insurer to begin the investigation and liability determination process. According to ISO data from 2024, property damage liability claims occur at a frequency of 2.50 per 100 earned car years, while bodily injury claims occur at 0.80 per 100 earned car years-meaning property damage claims are significantly more common. The other insurer gathers evidence, accident reports, witness statements, and medical records to establish fault. In most states, your insurer negotiates directly with the other party’s insurer to settle the claim within your policy limits.

This process typically takes weeks to months depending on claim complexity and injury severity. Once liability is determined and damages are quantified, your insurer pays the settlement up to your chosen limits. If damages exceed your limits, you become personally responsible for the overage. Your deductible only applies to your own vehicle damage under collision or comprehensive coverage, not to liability claims you owe others.

How Coverage Limits Function as a Hard Ceiling

Your policy limits establish a hard ceiling on what your insurer pays. If you carry 25/50/10 limits and someone racks up $75,000 in medical expenses, your policy pays only $25,000 per person, leaving you liable for the remaining $50,000. The average bodily injury claim reached $28,278 in 2024 according to ISO, and serious accidents routinely exceed $100,000 in total damages when multiple people are injured. Higher limits cost more monthly but eliminate this personal liability exposure. Selecting limits that match your net worth is the only strategy that actually protects your assets, because courts can garnish wages and seize property to satisfy judgments exceeding your policy limits.

The Real Cost of Underinsurance

An umbrella policy extends protection beyond your auto liability limits for roughly $150 to $300 annually per million dollars of additional coverage, making it an affordable safeguard for anyone with substantial assets. Claims processing itself moves faster when liability is clear-cut, averaging 30 to 60 days for straightforward property damage claims. However, complex injury cases involving multiple parties or permanent disabilities can stretch to 6 to 12 months or longer. The gap between what your liability coverage pays and what damages actually total determines your personal financial exposure. Understanding this gap matters far more than simply meeting your state’s minimum requirements.

What Your Liability Coverage Actually Won’t Pay For

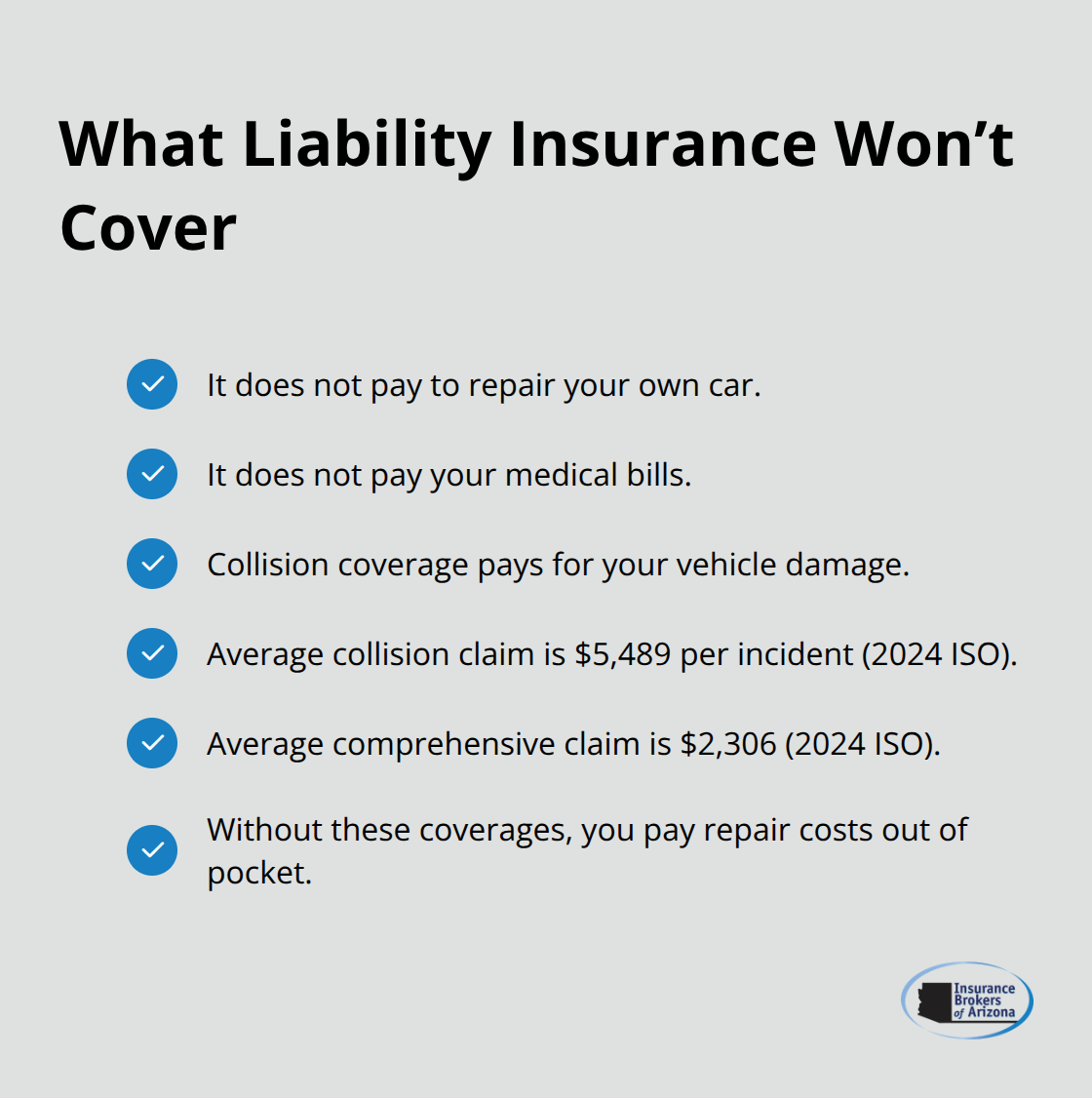

Most drivers believe their liability insurance protects their own vehicle when an accident happens. This misconception costs people thousands in unexpected out-of-pocket expenses every year. Your liability coverage exists solely to pay for injuries and property damage you cause to others, not to repair your own car or cover your medical bills.

If you hit another vehicle and your car sustains $8,000 in damage, your liability coverage pays nothing toward those repairs. You need collision coverage to handle your own vehicle damage, which is a completely separate policy component. This distinction matters enormously because many drivers discover this gap only after an accident occurs, when it’s far too late to add coverage. According to ISO data from 2024, collision claims average $5,489 per incident, and comprehensive claims average $2,306. Without these coverages, you absorb the full cost of fixing your vehicle from your personal funds.

Why State Minimums Leave You Dangerously Exposed

Many drivers assume that meeting their state’s minimum liability requirement provides adequate protection. This assumption is financially reckless. State minimums exist to meet legal requirements, not to protect your assets or match actual accident costs. In 2024, the average bodily injury claim reached $28,278 according to ISO data, yet numerous states allow minimum coverage of just $15,000 to $25,000 per person. This creates an immediate shortfall where your insurance pays only partial costs and you cover the remainder. Louisiana and Florida drivers face some of the nation’s highest insurance costs, with average annual premiums reaching $1,558 and $1,625 respectively according to NAIC data, yet many still carry minimum limits that leave them financially vulnerable. The real problem is that state minimums reflect political compromise, not financial reality. A single serious injury accident involving multiple people can easily exceed $100,000 in medical expenses, lost wages, and pain and suffering damages. Financial experts recommend liability limits of at least $100,000 per person and $300,000 per accident to protect against these scenarios. Carrying only $25,000 in bodily injury coverage means you personally owe $75,000 or more after your insurance limit exhausts. The monthly premium difference between minimum and adequate coverage typically amounts to $15 to $40, making the upgrade inexpensive compared to the protection it provides.

How Judgment Creditors Access Your Assets

Drivers often believe their personal assets remain protected as long as they carry some liability insurance. Courts and creditors view this differently. If a judgment against you exceeds your policy limits, creditors can garnish your wages, seize your bank accounts, and place liens against your home to satisfy the debt. A single serious accident can generate judgments of $250,000, $500,000, or higher when permanent disability or death occurs. Your $25,000 policy limit covers only a fraction of this exposure, leaving you personally responsible for the remaining balance. Financial experts recommend selecting liability limits that match or exceed your total net worth, which creates a genuine protective barrier. If your net worth is $400,000, carrying $100,000 in bodily injury coverage leaves $300,000 of your assets exposed to judgment creditors.

Why Umbrella Policies Fill the Critical Gap

An umbrella policy extends protection beyond your auto liability limits and covers the gap where your standard policy ends. These policies cost remarkably little-typically $150 to $300 annually per million dollars of additional coverage. Without this additional layer, your house, retirement accounts, and future earnings remain at risk from a single catastrophic accident. An umbrella policy activates only after your auto liability limits exhaust, so it works in tandem with your underlying coverage to provide comprehensive protection. For drivers with substantial assets (homes, savings, investment accounts), an umbrella policy represents one of the most cost-effective insurance decisions available. The protection it offers far exceeds what you pay in premiums, especially when you consider the alternative: losing everything to a judgment creditor.

Final Thoughts

Auto liability insurance covers the costs when you cause an accident, but only for injuries and property damage to others. This distinction separates drivers who understand their coverage from those who face devastating financial surprises after an accident. The gap between state minimums and adequate protection determines whether an accident depletes your savings or leaves your assets intact.

Carrying only your state’s minimum liability limits exposes you to serious financial risk. A single serious accident generates medical bills, lost wages, and pain and suffering damages that far exceed $25,000 or $50,000 limits, with the 2024 average bodily injury claim reaching $28,278 according to ISO data. When your policy limit exhausts, creditors garnish your wages, seize bank accounts, and place liens against your home to satisfy the judgment. Financial experts recommend liability limits matching or exceeding your net worth because this strategy actually protects what you’ve built.

We at Insurance Brokers of Arizona® work with over 40 reputable carriers to find competitive options tailored to your specific financial situation and risk tolerance. A licensed agent reviews your assets, discusses potential accident scenarios, and recommends limits that actually protect your future-often for just a few dollars monthly more than minimum coverage. Contact us today to discuss your liability coverage and ensure your protection matches your financial reality.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.