Homeowners insurance rates vary wildly depending on where you live, how old your home is, and your personal history. Most homeowners overpay because they don’t understand what actually moves the needle on their premiums.

At Insurance Brokers of Arizona®, we’ve helped hundreds of homeowners cut their costs by making smart choices about coverage and discounts. This guide walks you through the exact factors that determine your rates and the strategies that work.

What Actually Moves Your Homeowners Insurance Premiums

Home Age and Construction Materials

Your home’s age is one of the most predictable cost drivers. A home built in 2025 costs roughly $1,425 per year to insure compared to a 1984-built home at about $2,490 per year under identical policy terms, according to NerdWallet data. Older homes carry higher premiums because aging electrical systems, plumbing, and roofing increase claim risk. Construction materials matter just as much. A brick home costs less to insure than wood frame because brick resists fire and weather damage better. If you’re buying or renovating, upgrading to impact-resistant roofing or modern electrical systems directly reduces what you’ll pay.

Fire Station Proximity and Infrastructure

The closer you live to a fire station, the lower your premium. Distance to water sources and fire suppression infrastructure, measured by ISO’s Fire Suppression Rating Schedule, determines your fire risk category. These factors aren’t negotiable, but they’re worth evaluating before you buy a property.

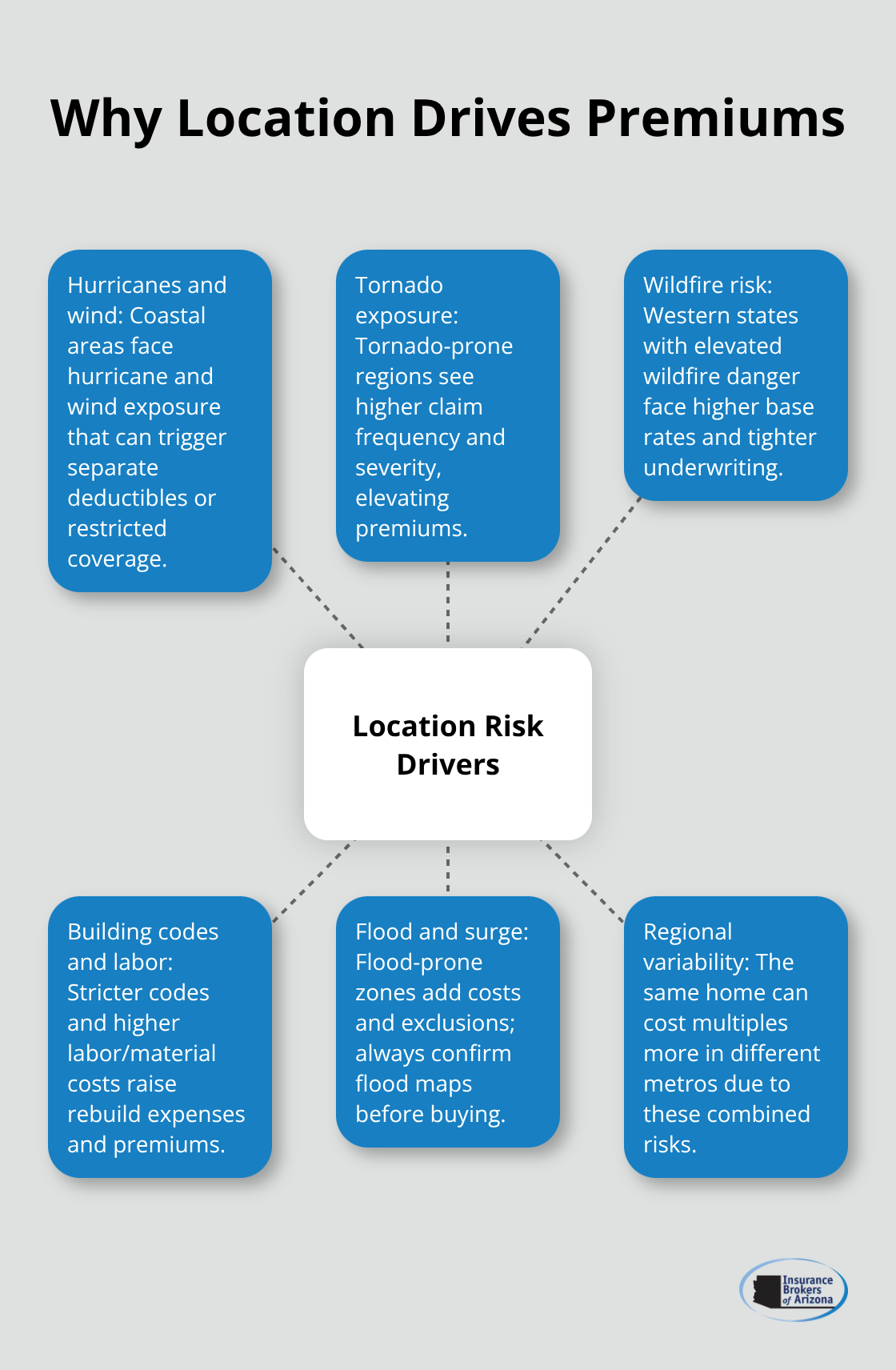

Location Creates Wild Price Swings

Oklahoma City homeowners pay roughly $9,770 per year while San Jose, California residents pay about $1,475 annually for comparable coverage. This sevenfold difference reflects regional disaster risk, building code standards, and labor costs. Coastal areas face hurricane and wind risk that trigger separate deductibles or coverage restrictions.

Tornado-prone regions see higher premiums. Wildfire risk in western states pushes costs up significantly. Before purchasing a home, use tools like First Street or Climate Check to assess flood, tornado, and wildfire exposure in your area. These hazards directly translate to premium increases.

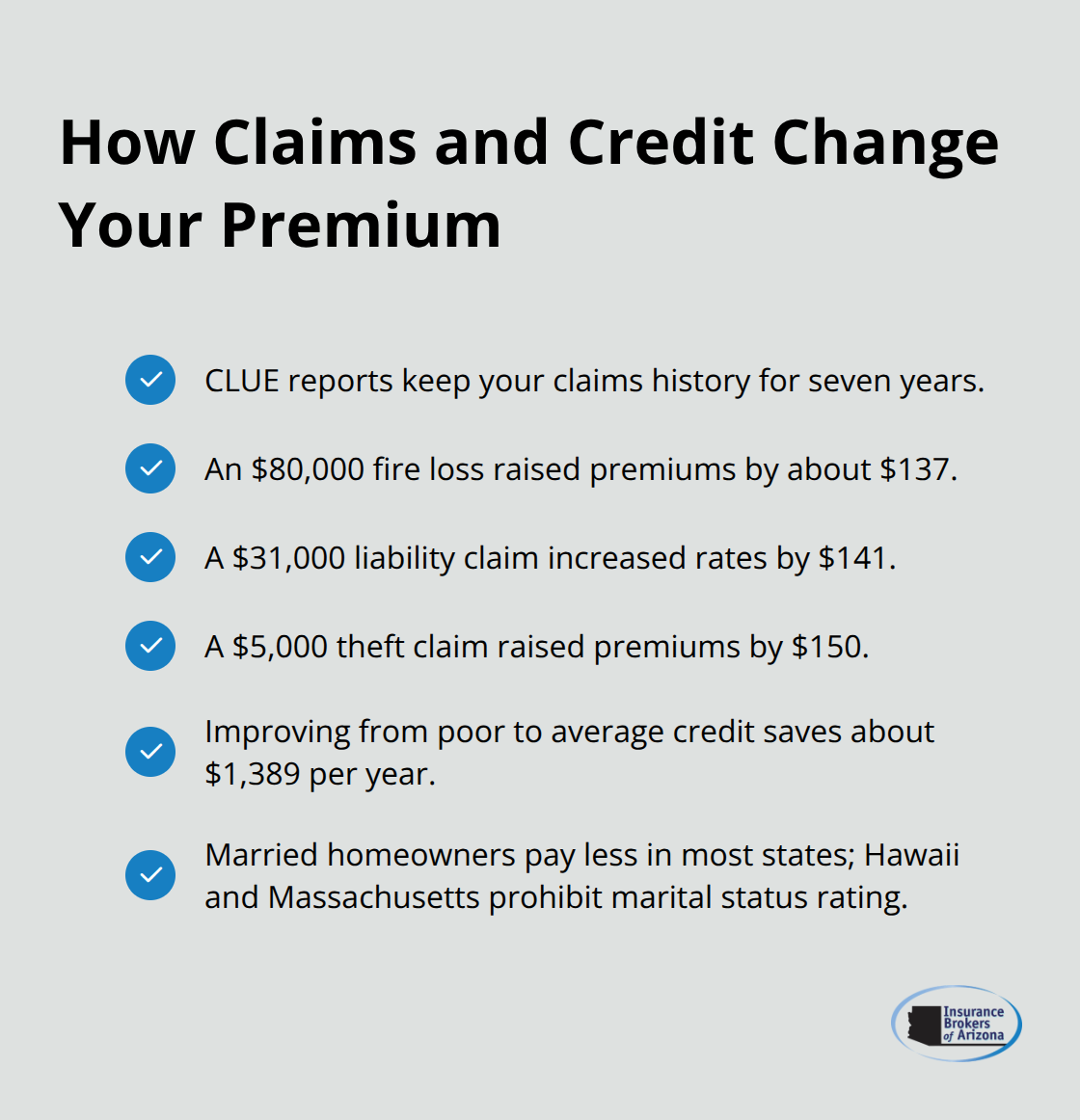

Claims History and Credit Impact

Your claims history stays on your CLUE report for seven years and follows you to new properties. A single fire loss of $80,000 raised premiums by about $137, while a $31,000 liability claim increased rates by $141, per Bankrate data. Smaller claims also count-a $5,000 theft claim raised premiums by $150.

This means filing minor claims costs more than just the deductible. Credit history matters significantly too. Improving from poor to average credit saves about $1,389 per year on average. In most states, marital status affects rates, with married homeowners paying less than single ones (Hawaii and Massachusetts prohibit using marital status as a rating factor).

These personal factors compound with home characteristics to determine your final rate, which is why understanding what insurers measure matters before you shop for coverage.

How to Cut Your Premiums Without Sacrificing Coverage

Bundle Policies to Unlock Immediate Savings

Bundling your homeowners and auto policies with the same insurer cuts what you pay faster than any other single move. Most carriers offer 10–25% discounts when you combine policies, though the actual savings depend on the insurer and your location. The catch is that bundling discounts don’t always stack the way you’d hope. Some insurers apply the discount to your homeowners policy only, while others reduce both. Before you commit to bundling, get quotes for both policies separately and together so you see the real number. If the bundle saves you $300 annually but costs you $400 more on auto, the math doesn’t work.

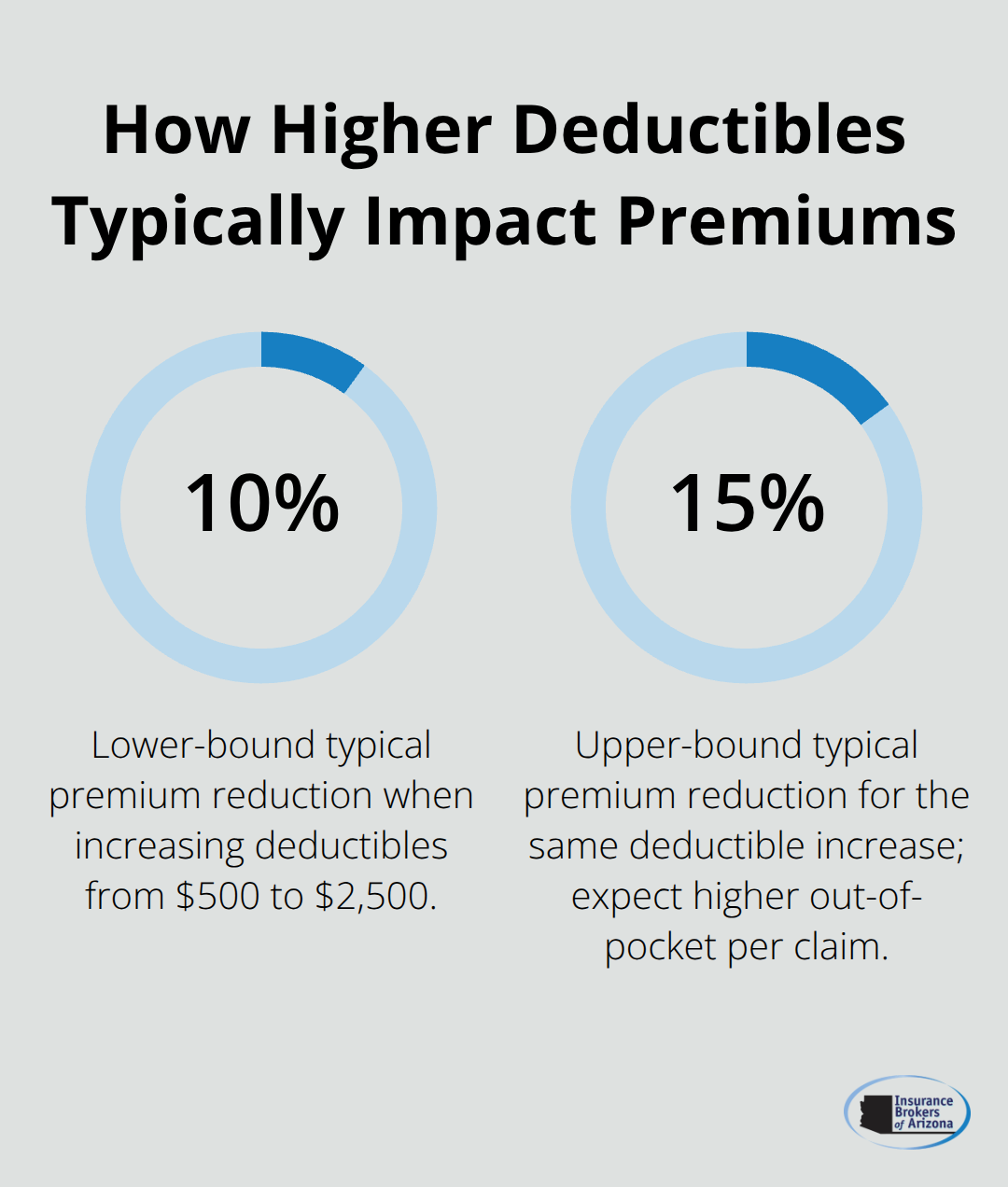

Raise Your Deductible to Lower Monthly Costs

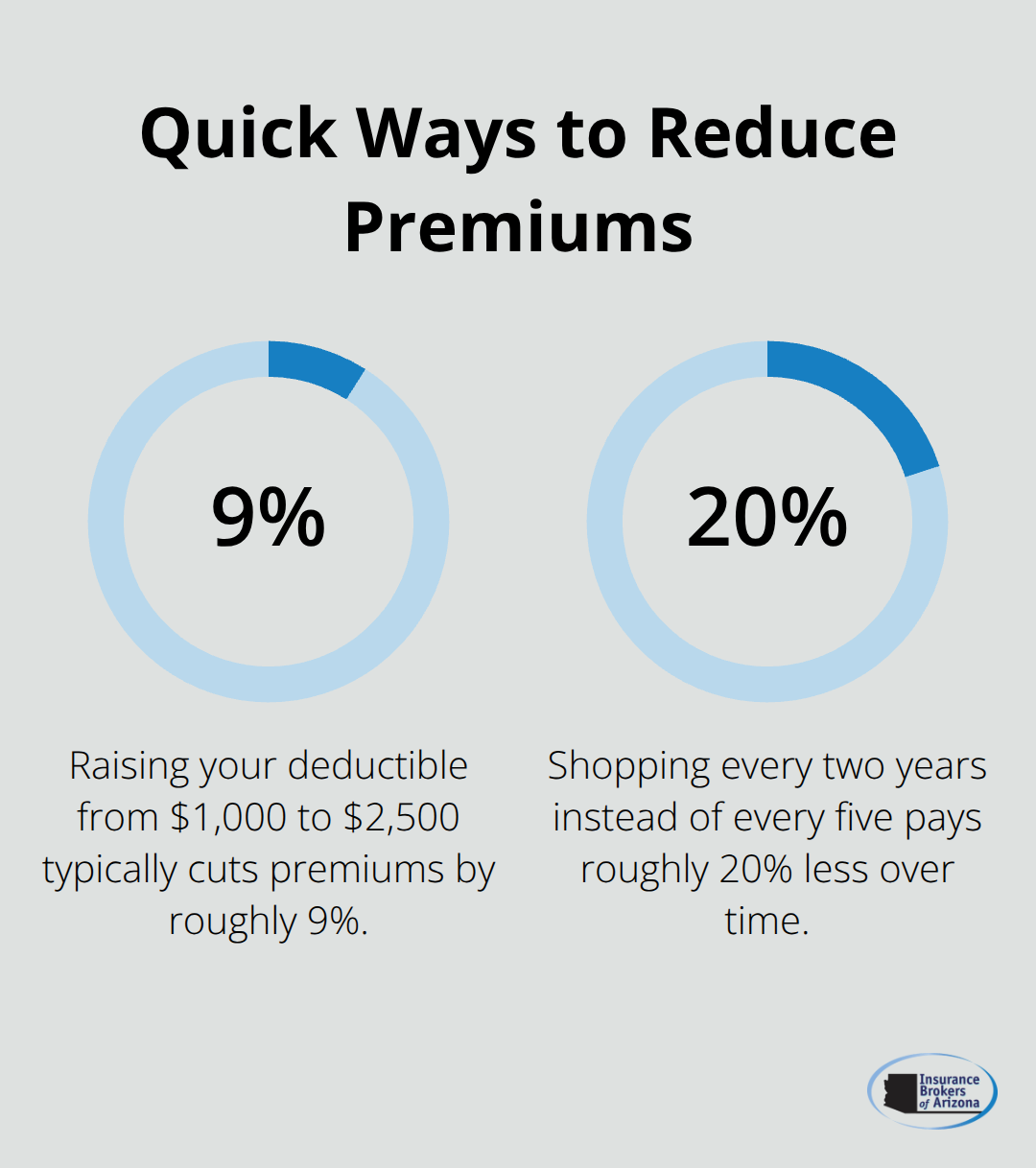

Your deductible is the single most controllable lever on your premium. Raising your deductible from $1,000 to $2,500 typically cuts premiums by roughly 9%, according to NerdWallet analysis, which translates to savings around $225 per year on a $2,490 benchmark policy. Going higher to $5,000 can push savings to 15–20%, but only if you can actually afford to pay that amount out of pocket when a claim happens. The mistake homeowners make is choosing a deductible they cannot cover. If a hail storm damages your roof and you owe $5,000 before insurance kicks in, you need cash on hand to pay it.

Install Safety Features That Reduce Risk and Premiums

Home security and safety upgrades deliver measurable premium reductions without increasing your out-of-pocket risk. Monitored alarm systems, smoke detectors, and sprinkler systems can yield 15–20% savings on some policies. Storm shutters and impact-resistant roofing qualify you for additional discounts in coastal and tornado-prone areas. These improvements cost money upfront, but they lower your annual premium permanently and increase your home’s resilience to actual disasters. The investment pays for itself through premium reductions over time, and you gain the added benefit of stronger protection when severe weather strikes.

Your home’s specific characteristics and your personal choices determine whether you overpay or find real value. The next section covers the mistakes that trap homeowners into paying more than they should.

Common Mistakes Homeowners Make When Shopping for Insurance

Choosing Coverage Limits That Are Too Low

Underinsuring your home is the costliest mistake homeowners make, yet it happens constantly. Many people lower their dwelling coverage to reduce premiums without understanding the consequences. A home with a $300,000 rebuild cost insured for only $150,000 leaves a $150,000 gap that you’ll pay out of pocket after a major loss. Bankrate data shows dwelling coverage at $150,000 costs about $1,459 annually, while $300,000 coverage runs roughly $2,424. The $965 annual difference feels significant until you face a house fire.

Your dwelling limit should reflect your home’s rebuild cost, not its market value or purchase price. Rebuild cost includes materials and current labor rates in your area, which vary dramatically by region. Oklahoma homeowners might rebuild for less than California homeowners in the same square footage. Before you set your coverage limit, get a rebuild cost estimate from a contractor or use your insurer’s cost calculator.

Many policies also tie liability and personal property coverage to your dwelling limit as a percentage, so cutting dwelling coverage reduces protection across your entire policy. This compounds the problem because you’re not just underinsuring the structure-you’re also cutting liability protection when a visitor gets injured on your property.

Ignoring Premium Increases at Renewal

Your insurer will raise rates whether your home changes or not, so treating renewal as automatic is expensive. The average homeowner saw premium increases over the past year according to Harris Poll data, driven largely by climate disasters and inflation in labor costs. Set a calendar reminder 30 days before your renewal date and get fresh quotes from at least three carriers with identical coverage limits and deductibles.

This comparison reveals whether you’re paying more than the market rate or whether your insurer has simply raised prices across the board. Some insurers offer loyalty discounts of 5–10% after several years, but these disappear if you don’t actively shop. The Zebra and other quote aggregators let you compare rates from 100+ insurers in minutes, making it practical to check your options annually.

Taking Action on Rate Comparisons

Getting three quotes takes less than 15 minutes and often saves $500 to $1,500 per year. Homeowners who shop for insurance every two years instead of every five years pay roughly 20% less over time because they catch rate increases early and switch before the damage compounds. Each quote you obtain provides leverage to negotiate with your current insurer or justification to move your policy to a carrier that values your business more fairly.

Final Thoughts

Finding the best value in homeowners insurance rates requires you to take three concrete actions. First, understand that your home’s age, location, and claims history determine most of what you pay, but your choices about deductibles, bundling, and safety features control the rest. Second, stop treating your renewal notice as final-getting quotes from multiple carriers every year catches rate increases before they compound and gives you leverage to negotiate better terms. Third, base your coverage on actual rebuild costs, not guesses, and resist the temptation to underinsure just to lower your premium.

The difference between overpaying and finding real value often comes down to having someone in your corner who understands how insurers price policies and which carriers offer the best rates for your specific situation. We at Insurance Brokers of Arizona® work with over 40 carriers to find coverage that matches your needs without wasting money on unnecessary protection or leaving gaps that could cost you thousands. Our team handles the comparison work so you don’t spend hours getting quotes yourself.

Review your current policy and note your dwelling coverage limit, deductible, and annual premium. Then contact Insurance Brokers of Arizona® to get fresh quotes with identical coverage terms. You’ll see immediately whether you’re paying market rate or whether switching carriers could save you hundreds annually.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.