What Does Commercial Auto Insurance Cover?

Commercial auto insurance coverage is a vital shield for businesses that rely on vehicles. At Insurance Brokers of Arizona®, we understand the complexities of protecting your company’s mobile assets.

This guide will break down the key components of commercial auto insurance, helping you navigate the various coverage options available. We’ll explore the factors that influence your policy and highlight additional protections to consider for comprehensive coverage.

What Does Commercial Auto Insurance Cover?

Commercial auto insurance provides essential protection for businesses that rely on vehicles. Let’s explore the key components of a robust commercial auto policy.

Liability Coverage: Your First Line of Defense

Liability coverage forms the foundation of any commercial auto policy. It protects your business if an employee causes an accident while driving a company vehicle. This coverage typically includes:

- Bodily injury liability: This pays for medical expenses if someone suffers injuries in an accident your driver caused.

- Property damage liability: This covers repair costs for damage to other vehicles or property.

In Arizona, the minimum liability limits often fall short for businesses. Higher limits (typically $1 million or more) are recommended, depending on your specific risks.

Physical Damage: Safeguarding Your Fleet

Physical damage coverage ensures your vehicles receive repairs or replacement after an accident. It splits into two main types:

- Collision: This covers damage from accidents with other vehicles or objects.

- Comprehensive: This protects against theft, vandalism, fire, and natural disasters.

For businesses with newer vehicles or a large fleet, this coverage proves invaluable. The National Automobile Dealers Association reported that in 2024, the average cost to replace a commercial vehicle stood at $45,000.

Medical Payments: Supporting Your Team

Medical payments coverage handles medical expenses for your employees if they sustain injuries in a work-related auto accident (regardless of fault). This coverage can bridge gaps in workers’ compensation and reduce potential lawsuits.

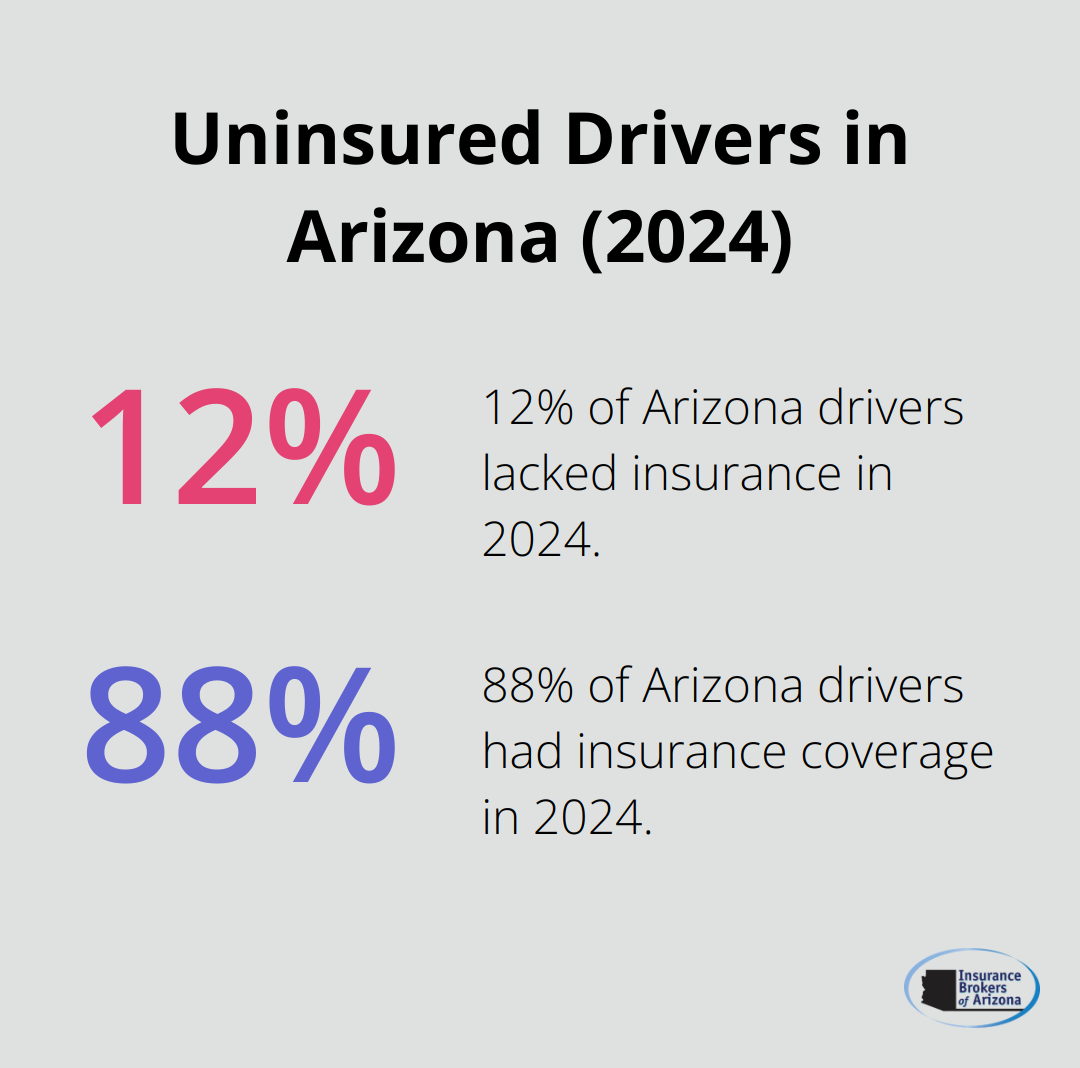

Uninsured/Underinsured Motorist: Closing the Gap

Despite laws requiring auto insurance, about 12% of Arizona drivers lacked insurance in 2024 (as reported by the Insurance Information Institute). Uninsured/underinsured motorist coverage protects your business if an employee experiences an accident with a driver who lacks adequate insurance.

This coverage has saved businesses from significant out-of-pocket expenses. It forms an essential part of a comprehensive commercial auto policy, especially given the high rate of uninsured drivers on the road.

The factors that affect your commercial auto insurance coverage extend beyond these basic components. Let’s examine how your business type, vehicle usage, and other elements influence your policy.

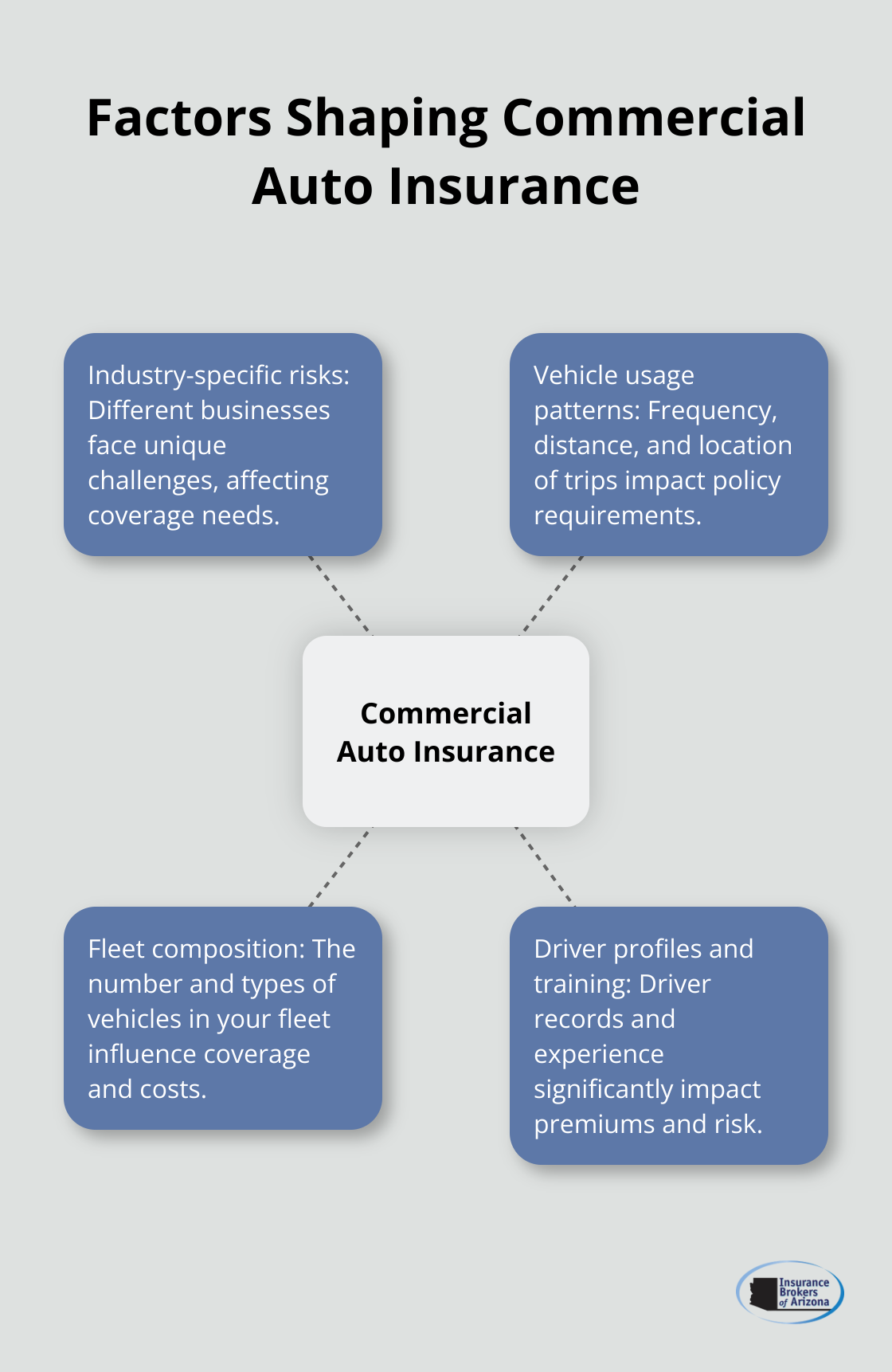

What Shapes Your Commercial Auto Insurance?

Industry-Specific Risks

Your business type significantly impacts your insurance needs. A construction company with heavy equipment faces different risks than a florist making local deliveries. In 2024, the trucking industry experienced a 15% increase in premiums due to rising accident rates and cargo values (according to the American Transportation Research Institute).

Insurance professionals analyze your specific industry risks to tailor coverage. A landscaping business might need higher liability limits due to frequent stops in residential areas, while a long-haul trucking company requires robust cargo coverage.

Vehicle Usage Patterns

Vehicle usage patterns directly affect your policy. Do your vehicles make frequent short trips or long-distance hauls? Are they used primarily in urban areas or on highways? A study by the Federal Motor Carrier Safety Administration found that vehicles driven over 50,000 miles annually were 50% more likely to be involved in accidents compared to those driven less.

Tracking your fleet’s mileage and routes provides valuable data. This information helps negotiate better rates and ensures you’re not over or under-insured.

Fleet Composition Matters

The number and types of vehicles in your fleet play a crucial role. In 2024, the average cost to insure a commercial truck was $7,000 annually, while a standard business car averaged $1,500 (according to the National Association of Insurance Commissioners).

Larger fleets often benefit from economies of scale, but also face increased exposure. Businesses should balance coverage needs with cost-effective solutions, such as fleet policies that cover multiple vehicles under one plan.

Driver Profiles and Training

Your drivers’ records and experience level significantly impact premiums. A study by the Insurance Institute for Highway Safety showed that drivers with clean records were involved in 70% fewer accidents than those with multiple violations.

Ongoing driver training programs reduce accident risks, and many insurers offer discounts for businesses with robust safety initiatives. Some businesses have seen premium reductions of up to 20% after implementing comprehensive driver safety programs.

Understanding these factors allows for the creation of a commercial auto policy that provides comprehensive protection without unnecessary costs. As businesses evolve, so should their insurance strategy. The next section explores additional coverage options that can further enhance your commercial auto insurance protection.

Enhancing Your Commercial Auto Coverage

At Insurance Brokers of Arizona®, we often see businesses that benefit from additional coverage options beyond the standard commercial auto policy. These add-ons provide crucial protection for specific business needs and scenarios.

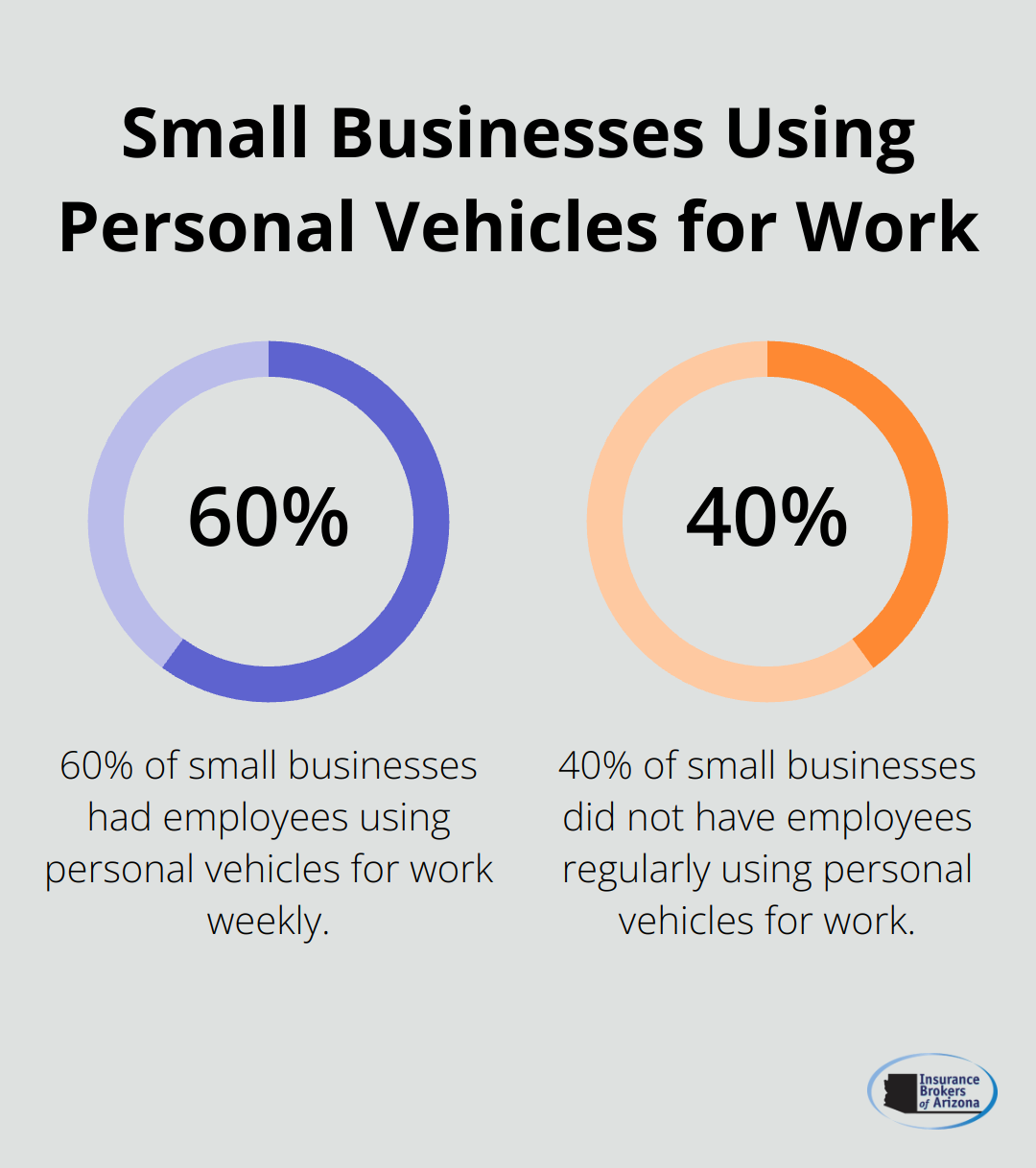

Hired and Non-Owned Auto Coverage

Many businesses overlook the risks associated with employees using personal or rented vehicles for work purposes. Hired and non-owned auto coverage fills this gap. A 2024 study by the National Association of Insurance Commissioners found that 60% of small businesses had employees who used personal vehicles for work at least once a week.

This coverage protects your business if an employee has an accident while driving their own car or a rental for work-related tasks. It’s particularly valuable for companies with salespeople, delivery drivers, or employees who attend off-site meetings.

Cargo Coverage: Protecting Your Goods in Transit

For businesses that transport goods, cargo coverage is essential. The American Trucking Associations reported that cargo theft resulted in $35 billion in losses in 2024. Standard commercial auto policies typically don’t cover the goods you transport.

Cargo coverage protects against theft, damage, or loss of items during transit. The level of coverage needed depends on the value and type of goods you transport. High-value or perishable items often require specialized coverage.

Rental Reimbursement: Keeping Your Business Moving

When a commercial vehicle is out of commission due to an accident or mechanical failure, rental reimbursement coverage can save your business. This add-on covers the cost of renting a replacement vehicle, ensuring your business operations continue smoothly.

A 2024 survey by Fleet Management Weekly found that businesses without rental reimbursement coverage lost an average of $1,500 per day when a key vehicle was out of service. This coverage is particularly valuable for businesses with specialized vehicles or those operating with a lean fleet.

Roadside Assistance: Minimizing Downtime

Roadside assistance coverage can significantly reduce downtime and associated costs. The Commercial Vehicle Safety Alliance reported that mechanical breakdowns were responsible for 25% of all roadside inspections in 2024.

This coverage typically includes services like towing, battery jumps, tire changes, and fuel delivery. For businesses operating in remote areas (or with vehicles that carry time-sensitive cargo), roadside assistance can be particularly beneficial.

We analyze your specific business operations to recommend the most appropriate additional coverages. These add-ons, when tailored to your needs, provide a robust safety net for your commercial auto risks.

Final Thoughts

Commercial auto insurance coverage protects businesses that rely on vehicles. It shields against financial losses from accidents, injuries, and property damage. The core components work together to provide comprehensive protection for various scenarios.

Your business needs will determine the ideal policy. Industry type, vehicle usage, fleet composition, and driver profiles all influence coverage requirements. We recommend you tailor your policy to align with your specific risk exposure.

At Insurance Brokers of Arizona®, we help you find the right commercial auto insurance coverage at competitive rates. Our team of professionals has access to over 40 reputable carriers (allowing us to customize policies for unique needs). You can focus on growing your business while we ensure your vehicles receive proper protection.