Auto Insurance for New Drivers: Complete Guide

Getting your first car is exciting, but auto insurance for new drivers can feel overwhelming. You’re facing unfamiliar terms, coverage options, and decisions that directly impact your wallet and protection on the road.

At Insurance Brokers of Arizona®, we’ve helped countless young drivers navigate these choices and find policies that actually fit their needs and budgets. This guide breaks down everything you need to know in plain language.

What Coverage Do You Actually Need

Arizona’s Liability Requirements and Why Minimums Fall Short

Arizona requires liability insurance before you drive legally, and that’s the foundation every new driver must understand. Liability coverage pays for damage or injuries you cause to others, and Arizona’s minimum is 15/30/10-meaning $15,000 per person and $30,000 per accident for bodily injury, plus $10,000 for property damage. That’s the legal floor, but it’s dangerously low. A single accident can easily exceed these limits, leaving you personally responsible for thousands in damages.

We recommend 100/300/100 coverage as a realistic target that actually protects your assets without excessive cost. Most new drivers underestimate how quickly medical bills and vehicle repairs climb after an accident.

Collision and Comprehensive: When You Need Them

Beyond liability, you need to evaluate collision and comprehensive coverage based on your specific situation. If you financed or leased your vehicle, your lender requires both collision and comprehensive, so you don’t have a choice. If you own the car outright, the decision depends on its value and your ability to replace it.

Collision covers damage from accidents, while comprehensive handles theft, weather, vandalism, and other non-collision events. Your premium gets calculated using your age, driving record, vehicle type, location, and the coverage limits you choose.

Deductibles and Optional Coverage

A higher deductible reduces your monthly payment but increases what you’ll pay out-of-pocket if you file a claim. The math is straightforward: a $1,000 deductible costs less monthly than a $250 deductible, but you need funds available if something happens. New drivers should also consider optional coverages like roadside assistance and rental reimbursement, which add modest monthly costs but prevent major headaches when your car breaks down or gets damaged.

How Vehicle Type and Location Shape Your Costs

Your vehicle choice matters significantly. Insuring a used Mazda MX-5 Miata costs roughly $2,640 annually for a teen, while a Subaru Outback runs about $2,735, according to insurance data. Sports cars and luxury vehicles cost substantially more due to higher repair costs and theft risk.

Location shapes your baseline costs regardless of coverage choices. The least expensive states for young drivers include Iowa at around $1,613 annually and Alabama at $2,274. According to Forbes Advisor data, the typical cost to add a 16-year-old to a parent’s policy runs about $2,408 annually, but this varies dramatically by state and carrier. Louisiana averages around $5,468 for a teen, while North Carolina sits closer to $2,312.

Finding Your Coverage Sweet Spot

The coverage you select directly determines what you’ll pay each month and what protection you actually have when an accident happens. Your next step involves shopping for quotes from multiple carriers to see how different coverage combinations affect your premium. Each insurer prices risk differently, and the quotes you receive will reveal which carriers offer the best value for your specific situation.

How to Shop for Quotes and Lock in Real Savings

Request Quotes from Multiple Carriers

Getting multiple quotes stands as the single most effective way to find affordable coverage, yet most new drivers skip this step entirely. When you request quotes from different carriers, provide identical information across all applications so you’re comparing apples to apples. Your age, driving record, vehicle details, ZIP code, and coverage selections all influence the final price, so consistency matters.

According to Forbes Advisor data, the average cost to add a 16-year-old to a parent’s policy ranges from $2,993 with Nationwide to $4,885 with Travelers, but these figures shift dramatically based on your specific situation and state. A new driver in North Carolina might pay around $2,312 annually, while the same driver in Louisiana could face $5,468. This state-level variation means your location determines a baseline cost that no discount eliminates, but your carrier choice absolutely does.

Request quotes from at least three to five different insurers using the same deductible and coverage limits. Online quote tools work quickly, but speaking directly with a licensed representative often reveals discounts you’d miss on a website.

Stack Discounts to Reduce Your Premium

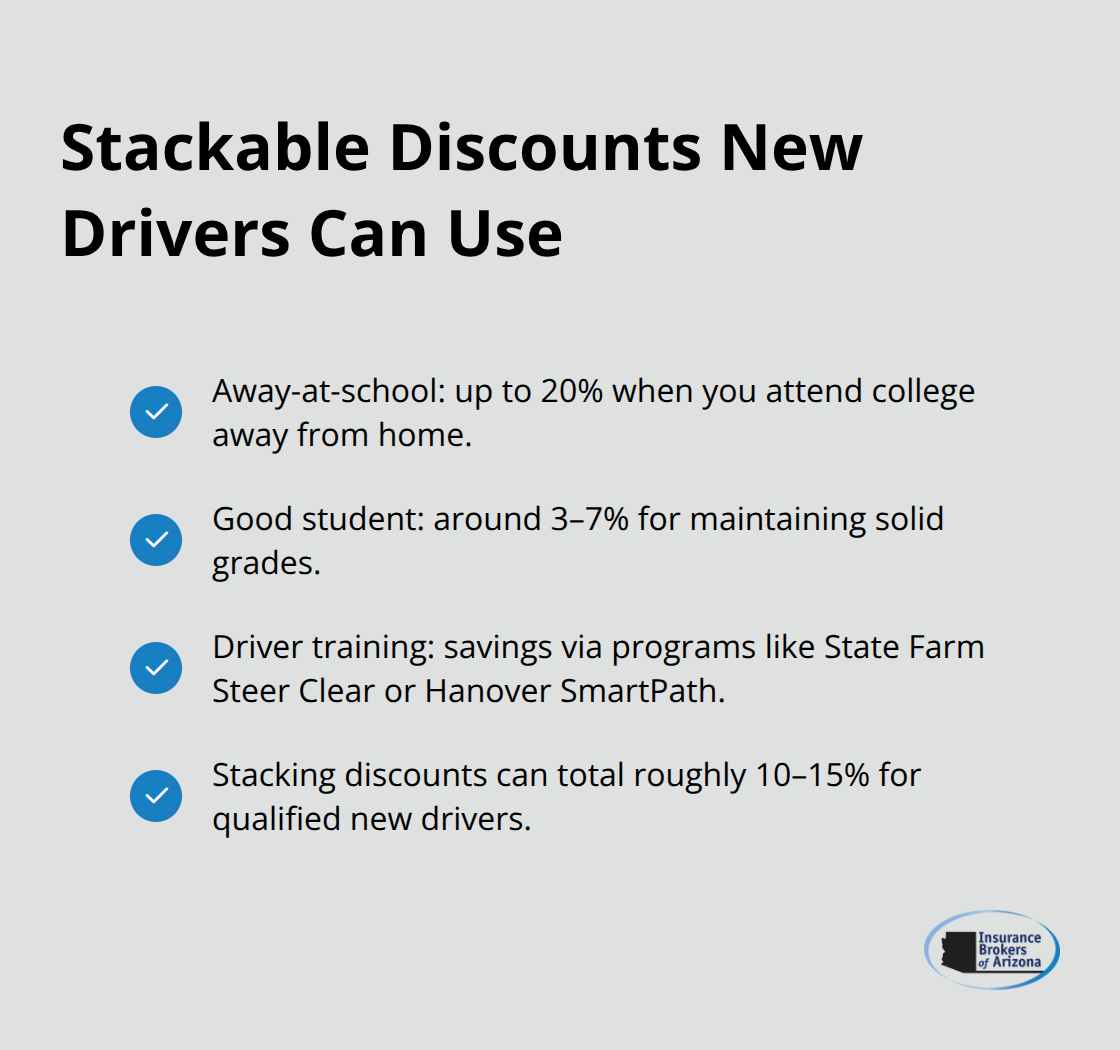

Many insurers offer away-at-school discounts up to 20 percent if you attend college away from home, good student discounts around 3 to 7 percent for maintaining solid grades, and driver training discounts through programs like State Farm Steer Clear or Hanover SmartPath. These discounts compound, so a new driver with good grades who completed a defensive driving course might reduce their annual premium by 10 to 15 percent simply through stacking available reductions.

Choose the Right Vehicle and Policy Structure

A used Mazda MX-5 Miata runs approximately $2,640 annually for a teen driver, while a Subaru Outback costs around $2,735, making older vehicles with strong safety ratings dramatically cheaper to insure than new sports cars. If your family has multiple vehicles, adding the teen driver to the parent’s policy on the least expensive car saves hundreds annually compared to insuring them on a newer or higher-value vehicle.

Bundling auto insurance with home or renters coverage typically yields multi-policy discounts ranging from 10 to 25 percent depending on the carrier. Usage-based insurance programs that monitor your driving habits through a mobile app can reward safe driving with lower premiums, though new drivers should verify upfront that the program offers a guaranteed discount rather than risking rate increases for normal teenage driving patterns.

Protect Yourself with Strategic Coverage Choices

Accident forgiveness coverage prevents your rate from jumping after your first at-fault accident, protecting you from the typical 20 to 40 percent premium increase that follows a claim. Higher deductibles directly lower monthly payments, but only choose a $1,000 or $500 deductible if you have that amount available in savings for an emergency claim.

Shopping around when adding a teen to an existing policy often reveals that switching carriers entirely saves more money than staying with your current insurer, even after accounting for loyalty discounts. Obtain fresh quotes every two to three years regardless of your current coverage, as carrier pricing shifts and new discounts emerge regularly. Once you’ve narrowed your options and selected a carrier, the next critical step involves understanding exactly what your policy covers and what it doesn’t before you sign the paperwork.

What New Drivers Get Wrong About Coverage

Selecting Insufficient Liability Limits

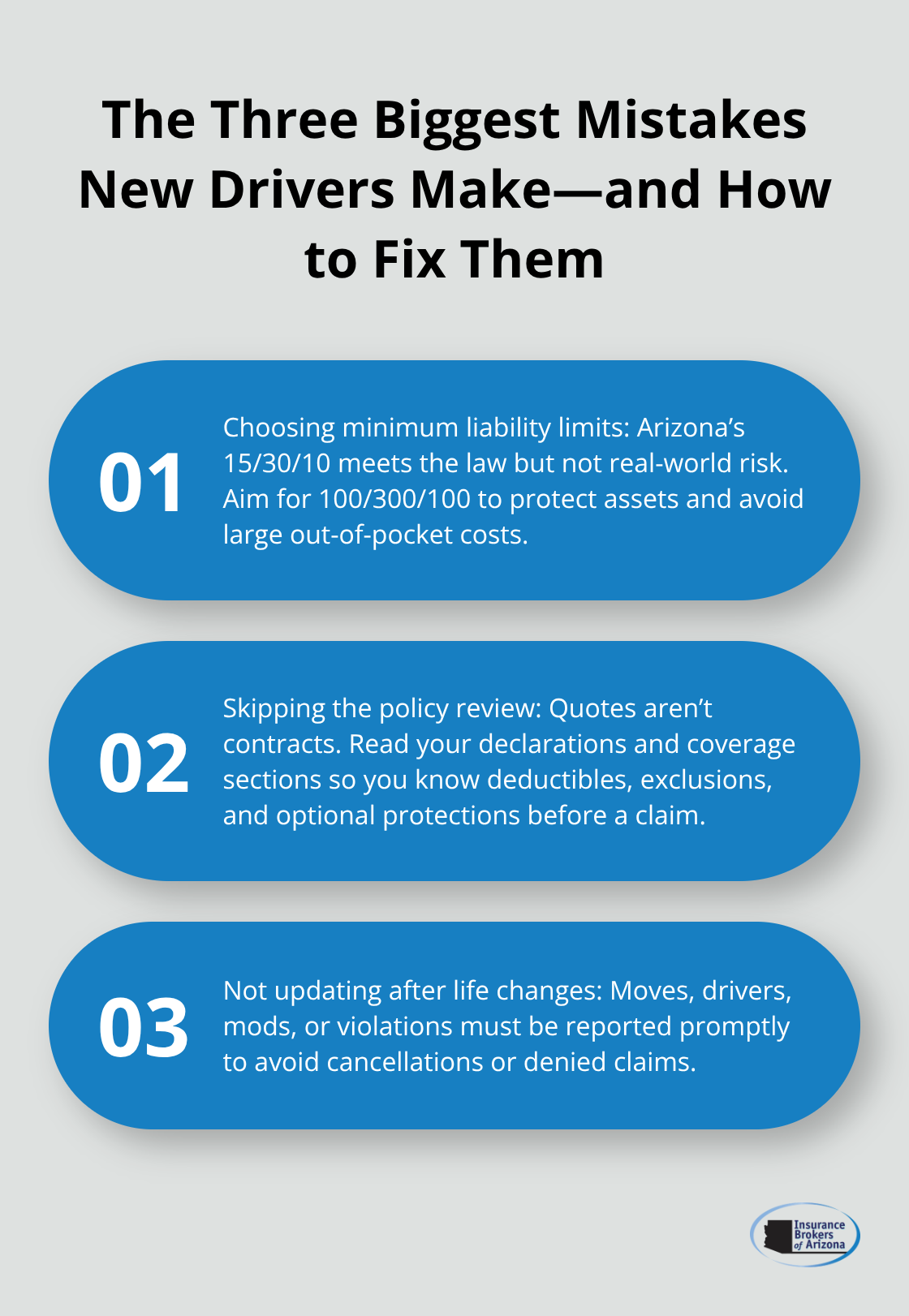

Most new drivers make their first critical mistake before they even start shopping: they assume Arizona’s minimum liability limits provide adequate protection. The 15/30/10 requirement satisfies the law, but it leaves you financially exposed. A single accident involving injuries can generate medical bills exceeding $30,000 in minutes, and you’ll owe the difference personally. Forbes Advisor data shows that recommended coverage sits at 100/300/100, yet many new drivers stick with minimums because they don’t understand the real-world cost of underinsurance. You might save $30 monthly with lower limits, but one accident costs you tens of thousands.

Skipping the Policy Document Review

The second mistake happens at the point of purchase: new drivers skip reading their actual policy documents entirely. They glance at a quote summary, see a price they can afford, and click purchase without understanding what their deductible actually means, which optional coverages they selected, or what exclusions apply. Your policy document contains the precise details that determine what happens when you file a claim-not the marketing materials or quote confirmation. Many insurers include coverages you didn’t request and exclude situations you thought were covered. Spend 20 minutes reading your declarations page and coverage section before finalizing anything.

Failing to Update Information After Purchase

The third mistake involves ignoring the need to update information after you purchase a policy. New drivers change addresses, add roommates, modify their vehicle, or pick up traffic violations, then fail to notify their insurer. Some assume they’re locked in at the quoted rate; others simply forget. When you eventually file a claim and the insurer discovers you misrepresented your situation-whether intentionally or through oversight-they can deny coverage entirely or cancel your policy. Arizona insurers take material misrepresentation seriously, and the consequences far exceed the premium you saved by not updating your information.

Taking Action on Life Changes

A move to a higher-crime ZIP code, adding a second driver to your household, or installing new safety features all affect your rate and coverage eligibility. Contact your insurer within 30 days of any significant life change, and request a new quote to see whether your rate should adjust. These three mistakes compound: insufficient coverage leaves you unprotected, skipping the policy review means you don’t realize what’s missing, and failing to update information creates gaps that emerge exactly when you need coverage most.

Final Thoughts

Auto insurance for new drivers requires three critical decisions: selecting adequate coverage limits, understanding your policy details, and maintaining accurate information with your insurer. You’ve now seen why Arizona’s minimum liability limits leave you financially exposed, how to shop effectively across multiple carriers, and which mistakes derail new drivers before they even start driving. The difference between a policy that protects you and one that leaves you vulnerable often comes down to spending time on these fundamentals rather than rushing through the process.

Gather your driver’s license, vehicle information, and driving history, then request quotes from at least three to five different insurers using identical coverage selections. Compare the quotes side by side, stack available discounts like good student or away-at-school reductions, and select a carrier that balances affordability with strong claims handling. Once you’ve chosen a policy, read your declarations page and coverage section before finalizing anything.

Professional guidance matters because insurance brokers understand how different carriers price risk and which discounts apply to your specific situation. Contact Insurance Brokers of Arizona® to have a licensed representative compare options for you and explain exactly what each policy covers. New drivers benefit enormously from having someone explain the real-world implications of coverage choices instead of making decisions based on price alone.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.