Home Insurance Coverage Arizona: Getting the Right Protection

Your home is likely your biggest investment, and protecting it properly matters more than most homeowners realize. Arizona’s unique climate brings specific risks that standard policies often miss, from intense heat to monsoon damage and wildfire threats.

At Insurance Brokers of Arizona®, we help homeowners navigate home insurance coverage Arizona options tailored to local conditions. This guide walks you through coverage types, Arizona-specific considerations, and how to find the right policy for your situation.

Understanding Your Home Insurance Coverage

Dwelling coverage protects the structure of your home itself-the walls, roof, foundation, and permanently attached systems like electrical wiring and plumbing. In Arizona, where construction costs rose about 6% from 2022 to 2023 according to Verisk data, this coverage must reflect actual rebuild expenses rather than your home’s market value. A home worth $400,000 might cost $550,000 to rebuild from scratch due to labor, materials, and current desert construction standards.

Most Arizona homeowners should carry replacement-cost coverage for dwelling, not actual cash value. Replacement cost covers the full expense to rebuild with materials of similar kind and quality, while actual cash value subtracts depreciation and leaves you thousands of dollars short when you file a claim. Your mortgage lender requires dwelling coverage at least equal to the loan amount because the home serves as collateral, but that minimum often falls short of true rebuild costs, so you may need to increase it yourself.

Personal Property Coverage Pays for Your Belongings

Personal property coverage reimburses you for furniture, electronics, clothing, and other contents if damage or theft occurs. This coverage also uses either replacement cost or actual cash value, and replacement-cost endorsements prove far more valuable because they pay to replace items with new equivalents rather than depreciated value. A television purchased five years ago might be worth $200 in actual cash value but cost $800 to replace with a comparable new model.

Most standard policies cap certain high-value items like jewelry, art, or collectibles at $1,500 to $2,500 per item. If you own items worth more than those limits, you’ll need separate scheduled personal property coverage or a valuable items endorsement. Document your belongings now with photos, videos, or a written inventory stored outside your home-this proof becomes critical when you file a claim.

Liability Coverage Protects Your Financial Security

Liability coverage pays for injuries or property damage you’re legally responsible for at your home. If a guest slips on your patio and breaks a leg, or your child accidentally damages a neighbor’s car, liability coverage handles medical expenses and legal costs up to your policy limit. Standard Arizona policies typically include $100,000 to $300,000 in personal liability protection, but that amount often proves insufficient for serious injuries.

Medical inflation and litigation costs mean a significant injury claim can easily exceed $300,000, so try higher liability limits-$500,000 or $1,000,000-especially if you have substantial assets. The cost increase is minimal; jumping from $300,000 to $1,000,000 in liability coverage adds only about $50 to $100 annually. Medical payments to others coverage, a separate component, covers medical bills for guests injured at your home regardless of fault (typically capping at $1,000 to $5,000 per person), and this coverage is inexpensive enough to maximize on every Arizona homeowners policy.

Why Arizona’s Specific Risks Demand Tailored Coverage

Arizona’s desert climate and seasonal weather patterns create coverage gaps that standard policies often miss. Monsoon season brings flash flooding, hail, and wind damage that many homeowners underestimate, while wildfire exposure affects pricing and availability in northern and rural areas. Water damage from rain or snow inside your home may not be covered unless caused by wind or roof damage, so endorsements can add protection for some water-related losses that standard policies exclude.

Understanding these coverage types forms the foundation for selecting adequate protection, but Arizona’s unique environmental threats require additional considerations that go beyond basic dwelling and liability limits.

Arizona’s Hidden Weather Risks and Coverage Gaps

Monsoon Season Flooding and Water Damage

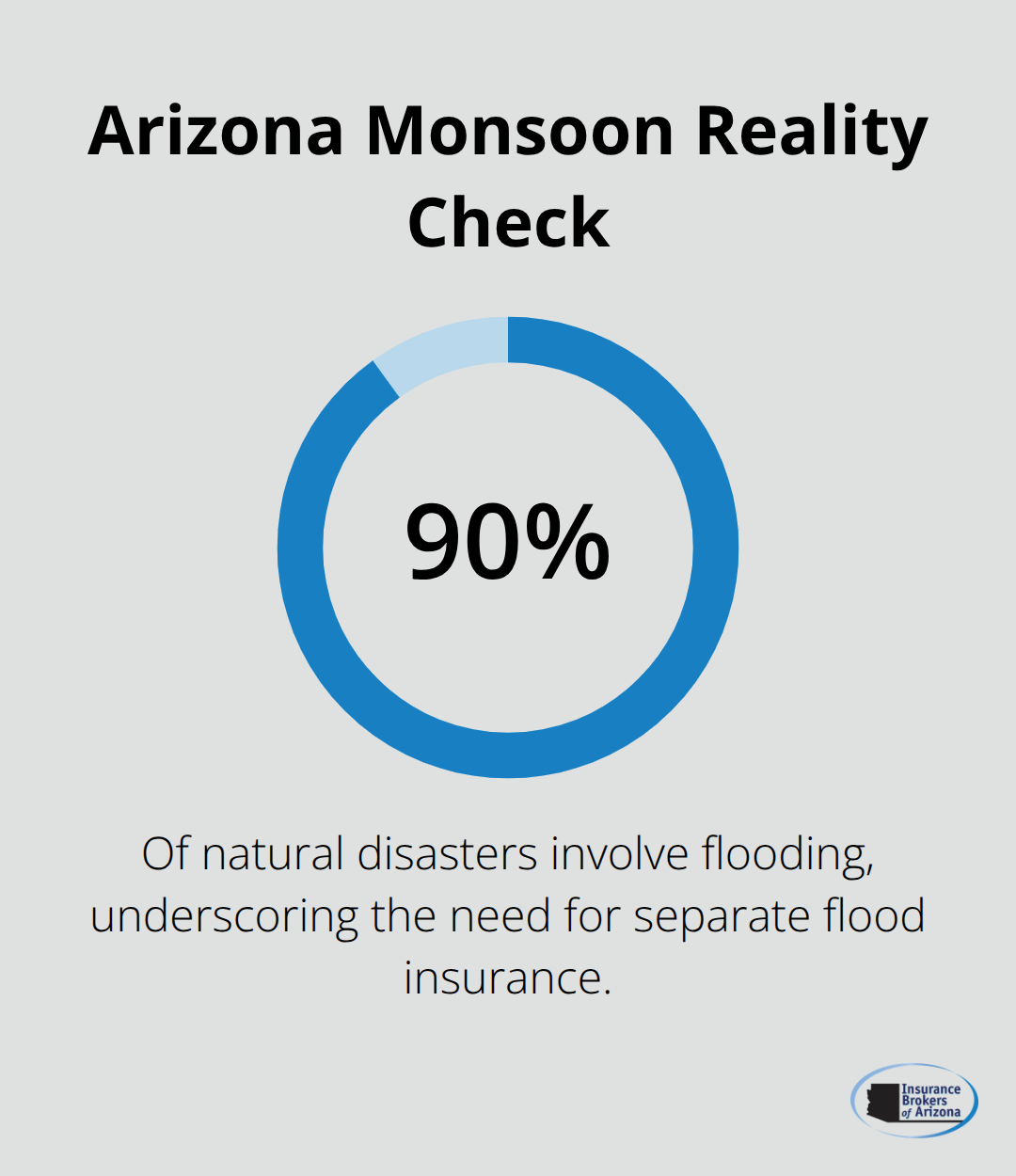

Arizona’s monsoon season, which typically runs from June through September, brings flash flooding, hail, and violent wind gusts that catch many homeowners unprepared. Standard homeowners policies exclude flood damage entirely, yet about 90 percent of natural disasters involve flooding according to the Insurance Information Institute. Monsoon storms can dump inches of rain in minutes, overwhelming drainage systems and forcing water into homes through doors, windows, and foundation cracks. If flooding damages your home during monsoon season, you cannot file a claim under your standard policy-you absorb the entire cost yourself unless you purchased a separate flood insurance policy through the National Flood Insurance Program or a private insurer.

Water damage from rain or snow inside your home also falls outside standard coverage unless the damage results from wind or roof damage. Endorsements become necessary to close this gap. Water backup coverage and service line protection add essential protection because these endorsements cover sewer backup and water line damage that monsoon season can trigger. The cost for these add-ons typically ranges from $50 to $150 annually, a small price against potential losses of thousands of dollars.

Wildfire Risk and Defensible Space

Wildfire exposure presents an even more urgent threat, particularly for homes in northern Arizona or near wildland-urban interface areas. Arizona reconstruction costs rose approximately 6 percent from 2022 to 2023 according to Verisk data, but wildfire risk has pushed insurers to tighten underwriting in forested and rural ZIP codes dramatically. The Arizona Department of Insurance reports that 38 communities across Arizona face ISO Public Protection Classifications of 8B or worse, meaning fire risk is severe enough to affect premium pricing and coverage availability.

If your home sits in a higher-risk wildfire zone, insurers may impose wildfire-specific deductibles (separate from your standard deductible) or decline to renew your policy altogether. The most effective response involves implementing defensible space around your property by clearing brush within 30 feet of your home, removing dead trees, and trimming branches away from the roof. These actions signal to insurers that you take risk seriously and may result in premium reductions.

Fire-Resistant Materials and Premium Discounts

Upgrading to fire-resistant roofing materials like tile or impact-resistant shingles yields discounts of 10 to 20 percent on your annual premium according to MoneyGeek analysis, making the upfront investment recoverable within a few years. Participation in community programs like Firewise USA strengthens your position with insurers and demonstrates commitment to risk mitigation.

Your dwelling replacement cost coverage must reflect current rebuild expenses in your area because wildfire damage often triggers total-loss claims. Policy language differences create coverage gaps that cheap quotes often hide, leaving you personally responsible for the gap between your coverage limit and actual rebuild costs. This financial exposure grows as construction costs climb. Understanding these Arizona-specific weather threats and the coverage gaps they create positions you to make informed decisions about which endorsements and additional protections your policy actually needs.

Finding the Right Coverage Limits for Your Home

Calculate Your True Replacement Cost

Calculating actual replacement cost separates homeowners who recover fully after a loss from those left thousands of dollars short. Construction costs in Arizona rose approximately 6 percent from 2022 to 2023 according to Verisk data, meaning a home’s market value often falls significantly below what it costs to rebuild. Contact local contractors and request quotes to rebuild your home from the foundation up, accounting for current labor rates and material prices in your area. This number becomes your dwelling coverage target, not your home’s appraised value.

Personal property coverage should reflect the actual cost to replace your belongings with new items, not depreciated versions. Walk through your home and photograph high-value items, document electronics with purchase dates, and maintain an inventory stored outside your home. For items exceeding standard policy limits of $1,500 to $2,500 per item, scheduled personal property endorsements cost only $50 to $150 annually but protect jewelry, art, or collectibles at their full replacement value.

Boost Your Liability Protection

Liability coverage deserves serious attention because Arizona’s litigation environment and medical inflation mean injury claims escalate quickly. Try higher liability limits-$500,000 or $1,000,000-especially if you have substantial assets. Jumping from $300,000 to $1,000,000 in liability coverage costs only about $50 to $100 per year, making this upgrade nearly cost-free compared to the financial exposure you eliminate.

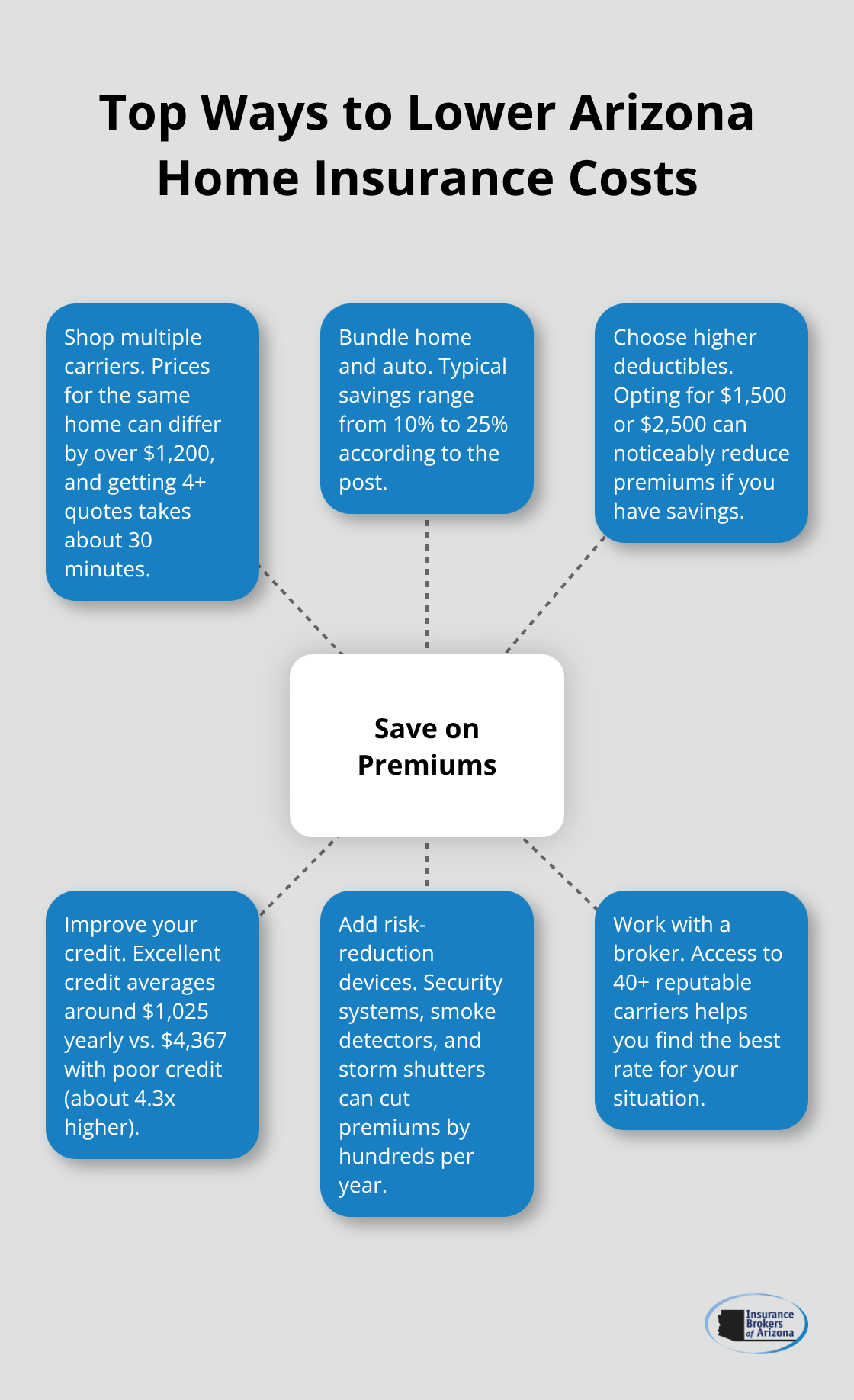

Shop Multiple Carriers for Better Rates

Price variation between carriers in Arizona runs dramatically wider than most homeowners expect. Six major carriers pricing for the same Arizona home can differ by over $1,200 annually, with State Farm averaging around $1,334 per year while other carriers quote substantially higher, according to MoneyGeek analysis. Obtain quotes from at least four different insurers-this takes roughly 30 minutes online and reveals whether you’re overpaying by hundreds of dollars annually.

Credit score influences pricing more than most factors. Excellent credit scores yield premiums around $1,025 yearly while poor credit scores push costs to $4,367 yearly for identical coverage, a 4.3 times difference according to MoneyGeek data. Bundle home and auto insurance to typically save 10 to 25 percent on total costs, making this strategy worth evaluating even if it means switching carriers.

Optimize Deductibles and Discounts

Try higher deductibles ($1,500 or $2,500 instead of $500) to reduce premiums noticeably, but only choose this approach if you maintain savings to cover the deductible when a loss occurs. Risk-reduction credits for security systems, smoke detectors, or storm shutters can cut premiums by hundreds of dollars annually, so ask carriers specifically about these discounts rather than assuming they apply automatically. Insurance Brokers of Arizona® partners with over 40 reputable carriers, allowing you to compare multiple quotes efficiently and identify which insurers offer the best rates for your specific situation.

Final Thoughts

Protecting your Arizona home requires more than a standard policy and hoping for the best. The coverage gaps we’ve outlined-from monsoon flooding to wildfire exposure to water damage exclusions-represent real financial risks that affect thousands of Arizona homeowners annually. Your dwelling coverage must reflect actual rebuild expenses, your liability limits must exceed $300,000, and your personal property coverage must use replacement cost rather than actual cash value.

The most effective strategy involves calculating your true replacement cost, obtaining quotes from multiple carriers, and reviewing your policy annually as construction costs and your home’s condition change. Arizona homeowners who shop around save hundreds or even thousands annually because price variation between insurers runs dramatically wider than most people expect. Higher deductibles, bundled policies, and risk-reduction credits compound these savings further.

We at Insurance Brokers of Arizona® understand Arizona’s unique insurance landscape and the coverage decisions that matter most. With partnerships across over 40 reputable carriers, we help homeowners compare options efficiently and identify which insurers offer the best rates for their specific situation. Contact us today to review your current coverage, identify gaps, and secure home insurance coverage Arizona that actually matches your home’s value and Arizona’s environmental risks.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.