How to Choose the Right Auto Insurance Deductible

Picking the right auto insurance deductible is one of the most overlooked decisions Arizona drivers make. Most people either choose too low a deductible and overpay on premiums, or pick too high a deductible and risk financial hardship after an accident.

We at Insurance Brokers of Arizona® help clients find the sweet spot that matches their budget and risk tolerance. This guide walks you through the exact factors you need to consider.

What a Deductible Is and How It Works

A deductible is the amount you pay out of your own pocket when you file a claim, and your insurance company pays the rest. If you hit a parked car and cause $3,000 in damage with a $500 deductible, you pay $500 and your insurer covers the remaining $2,500. This applies to collision and comprehensive coverage, which protect your vehicle from accidents and weather events. The deductible amount you choose directly shapes your monthly premium, but the relationship works against what many Arizona drivers assume. Higher deductibles lower your monthly payments because you agree to absorb more risk yourself, while lower deductibles raise your premiums since the insurance company takes on more financial responsibility per claim. Progressive reports that $500 is the most common deductible choice nationwide, and for good reason-it strikes a reasonable balance for many drivers. Arizona residents should understand that deductibles are per claim, not annual, meaning you pay the deductible every time you file an approved claim, not just once per year.

How Deductibles Affect Your Monthly Premium

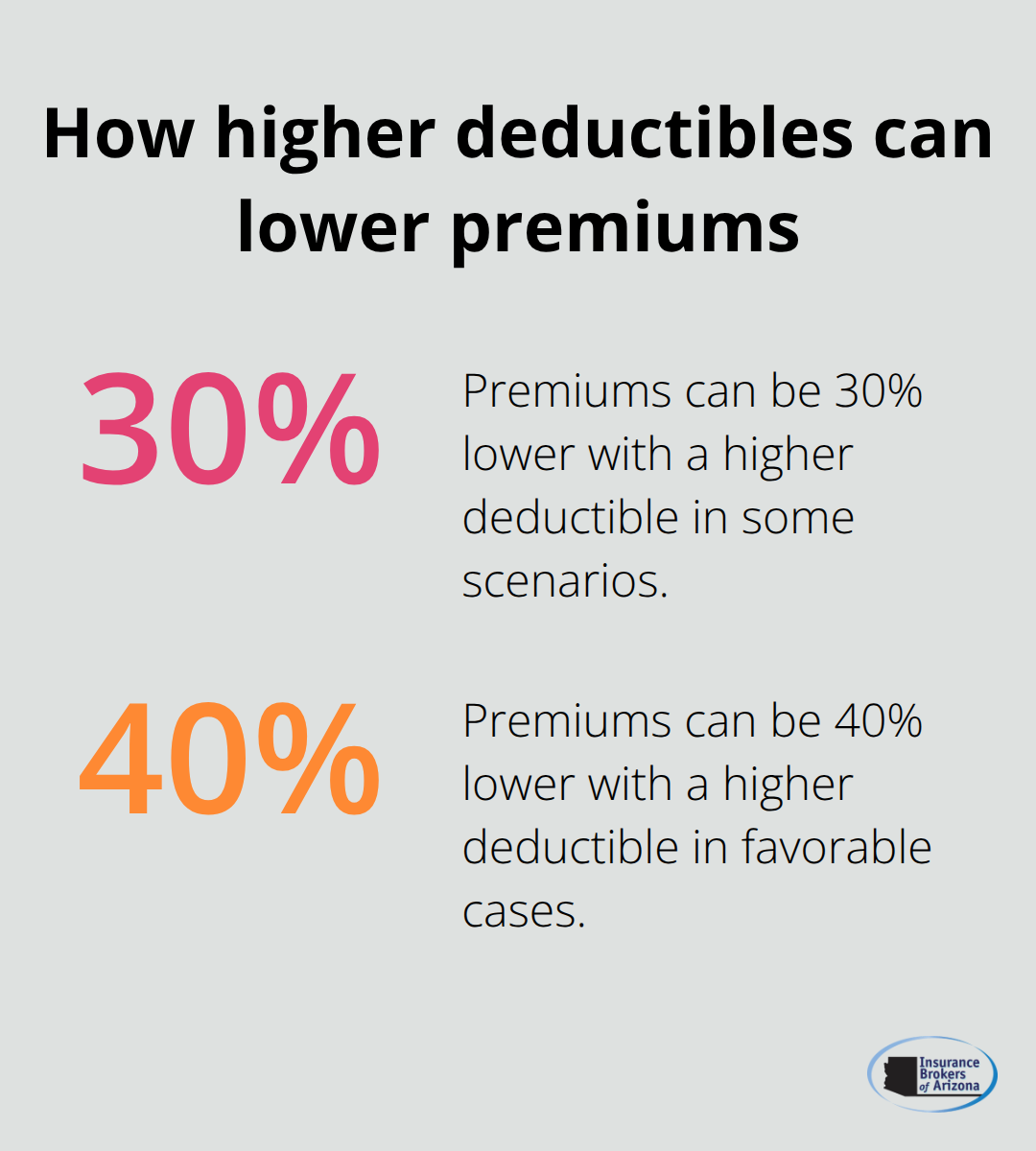

The premium difference between a $250 deductible and a $1,000 deductible can be substantial, sometimes 30 to 40 percent lower for the higher deductible. However, this savings only matters if you don’t file claims frequently.

A driver who files one collision claim every five years pays that deductible once during that period, so the monthly savings add up fast. But a driver involved in two accidents over five years pays the deductible twice, which can erase years of premium savings.

Assessing Your Claim Likelihood

Arizona drivers must honestly assess their claim likelihood based on their commute, traffic exposure, and parking situation. Someone driving peak hours on Phoenix’s I-10 faces different risk than someone working from home and driving occasionally. The math matters too-if your monthly premium drops by $40 with a higher deductible, you save $240 annually, but a single claim means you forfeit five years of those savings.

Getting Accurate Quotes for Your Situation

Run actual quotes from multiple carriers at different deductible levels to see the exact numbers for your situation, not relying on industry averages that may not reflect Arizona-specific rates or your driving profile. This comparison reveals whether the premium savings justify the higher out-of-pocket risk in your particular case. Your next step involves examining your personal financial situation and driving habits more closely to narrow down which deductible range makes sense for you.

Factors to Consider When Choosing Your Deductible

Your Emergency Fund Sets Your Deductible Ceiling

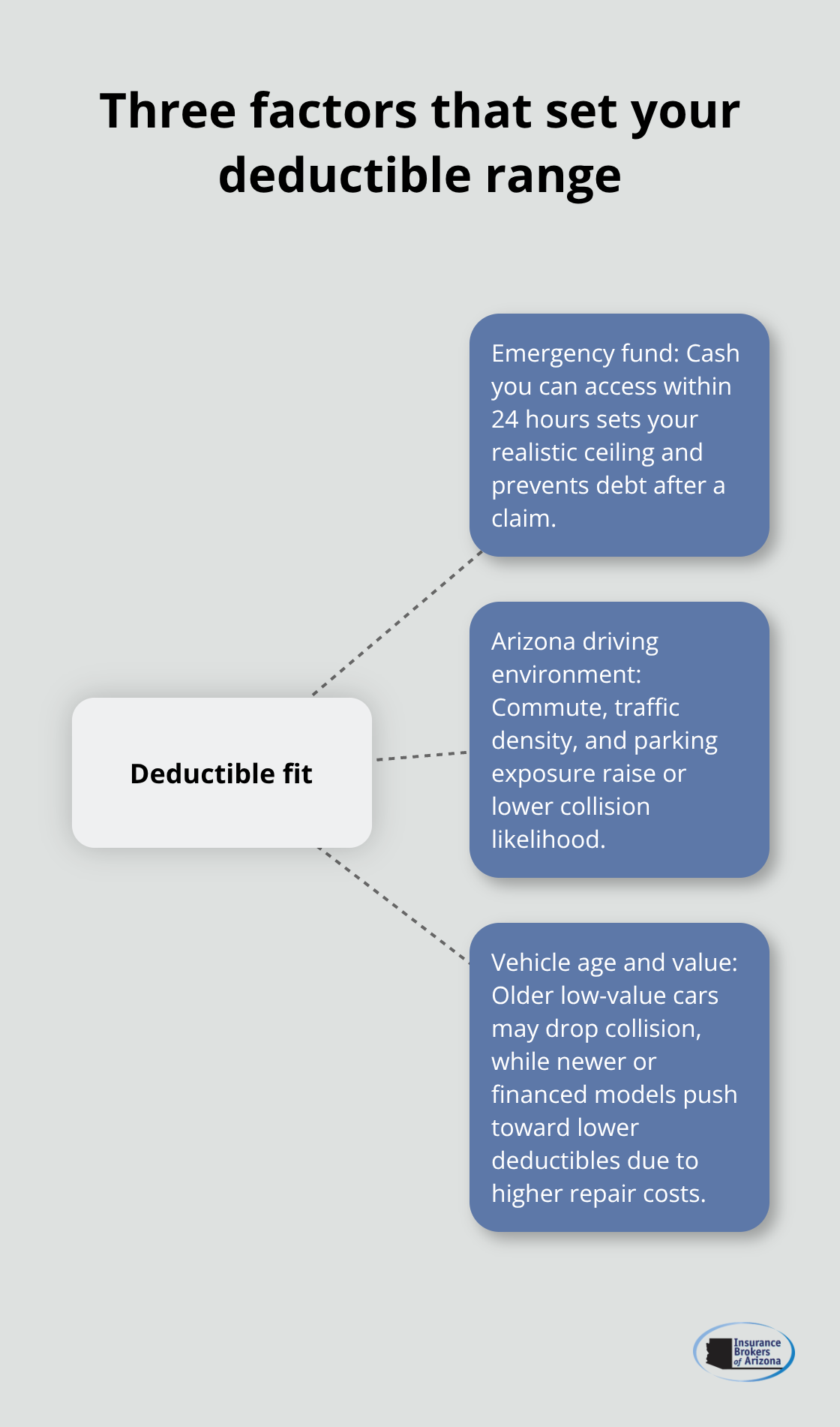

Your emergency fund is the first hard constraint on deductible selection, and ignoring it leads to financial disaster. If you have $800 saved and pick a $1,500 deductible, you cannot afford to file a claim without borrowing money or going into debt. Many Arizona drivers choose deductibles based solely on premium savings without checking their actual cash reserves. Count the money you can access within 24 hours without touching retirement accounts or selling assets. That number is your realistic deductible ceiling.

Three months of expenses saved means you can comfortably handle a $1,000 or $1,500 deductible. One month of savings suggests you stick with $500 or lower. The premium savings mean nothing if a single accident forces you to finance the deductible through a credit card at 20 percent interest, which erases years of monthly savings in weeks.

Your Arizona Driving Environment Shapes Your Risk Profile

Your driving environment in Arizona matters far more than national statistics. Someone commuting through downtown Phoenix during rush hour faces collision risk that someone working from home cannot match. If you drive peak hours in heavy traffic, park on busy streets, or navigate areas with high accident rates, a lower deductible reduces your financial vulnerability to statistically likely events.

Conversely, if you drive mostly surface streets in light traffic or work from home, the premium savings from a higher deductible compound faster than your actual claim likelihood. Your commute pattern directly influences whether you should absorb more risk through a higher deductible or protect yourself with lower out-of-pocket costs.

Your Vehicle’s Age and Value Determine Coverage Strategy

Your vehicle’s current value directly determines whether physical damage coverage even makes financial sense. A 2015 sedan worth $8,000 with a $1,000 deductible means an accident that totals the car leaves you paying $1,000 for a vehicle worth $8,000, which is wasteful. For older vehicles worth less than $5,000, dropping collision coverage entirely often costs less than paying premiums plus deductible.

For newer financed vehicles, your lender may require a lower deductible regardless of your preference, so check your loan documents first. Newer technology-heavy vehicles and electric vehicles cost substantially more to repair than older models, which shifts the math toward lower deductibles for newer cars since repair bills exceed deductibles more frequently. These three factors work together to narrow your realistic deductible range, and understanding how they interact reveals which option actually saves you money over time.

Strategies for Selecting the Right Deductible

Compare Actual Numbers Before You Decide

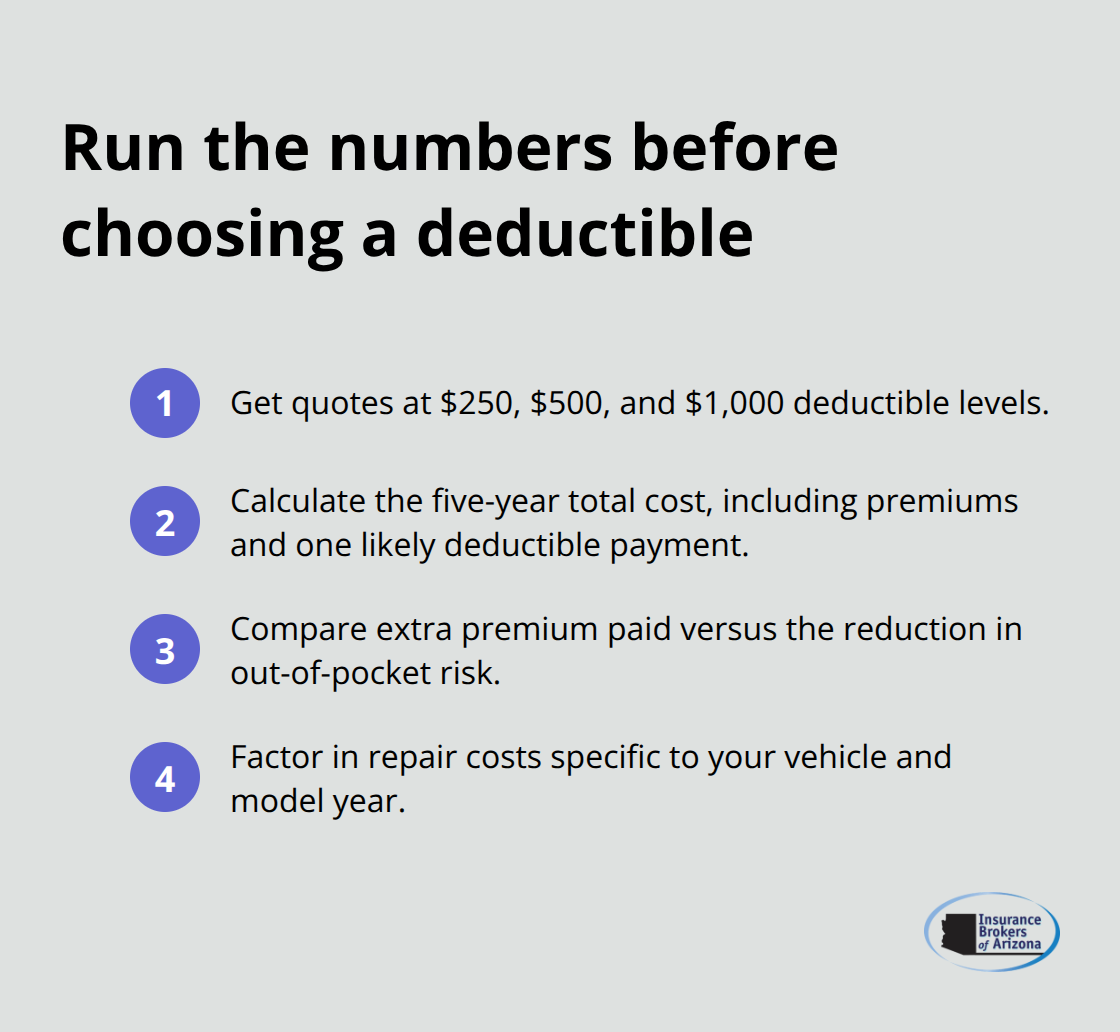

The real test of deductible selection happens when you compare actual numbers from your insurer rather than relying on industry benchmarks. Get quotes at three different deductible levels-typically $250, $500, and $1,000-and calculate the five-year cost for each option. If dropping from $500 to $250 costs an extra $25 monthly but saves only $250 in out-of-pocket risk, that’s $1,500 in additional premiums over five years to protect against a single claim you may never file. The math often reveals that the mid-range deductible saves more money than either extreme.

Arizona drivers commonly find that a $500 deductible delivers 70 to 80 percent of the premium savings compared to a $250 deductible while maintaining reasonable financial protection. However, this changes dramatically if you drive a newer vehicle with expensive repairs-a single collision on a 2024 model can cost $8,000 to $12,000 in repairs, making a $500 deductible feel dangerously high. Run the numbers specific to your vehicle’s repair costs and your actual premium quotes before you decide.

Optimize Deductibles Across Different Coverage Types

The most overlooked strategy involves using different deductibles across your coverage types rather than locking in one deductible for everything. Comprehensive coverage typically costs 40 to 50 percent less than collision coverage, which means lowering your comprehensive deductible from $500 to $250 might add only $3 to $5 monthly while dramatically reducing your out-of-pocket costs for theft, weather, or vandalism claims.

These events happen frequently in Arizona-vehicle theft rates in Phoenix rank among the highest nationally, and monsoon season creates predictable comprehensive claims. Conversely, keep collision at $1,000 to preserve premium savings since collision claims happen less frequently for most drivers. You can also optimize glass coverage separately; some insurers offer zero-deductible glass or waive the deductible if you use their preferred repair shop, which matters in Arizona where windshield damage from debris on highways is common.

Review Your Deductible Annually

Reassess your deductible annually rather than setting it once and forgetting it. Major life changes-a new job with a longer commute, purchasing a newer vehicle, or building additional emergency savings-all justify reconsidering your deductible. Your financial situation improves over time, which typically means you can comfortably absorb a higher deductible and recapture those monthly savings.

Job loss or reduced income shifts the math toward lower deductibles that protect your limited cash reserves. Each renewal cycle offers an opportunity to confirm your choice still aligns with your current circumstances rather than your situation from twelve months ago.

Final Thoughts

Choosing the right auto insurance deductible comes down to three core decisions: understanding what you can realistically afford to pay out of pocket, honestly assessing your driving risk in Arizona, and running actual numbers from your insurer rather than guessing based on industry averages. The deductible that works for someone commuting through Phoenix traffic differs completely from the deductible that makes sense for someone working from home. Your emergency fund sets the ceiling, your vehicle’s value shapes the strategy, and your claim likelihood determines whether premium savings actually materialize over time.

The most common mistake Arizona drivers make is selecting a deductible based solely on monthly premium savings without considering the total five-year cost or their actual financial cushion. A $1,000 deductible saves money only if you avoid filing claims, but a single accident erases years of those savings. Conversely, a $250 deductible provides peace of mind but costs substantially more in premiums if you never file a claim.

We at Insurance Brokers of Arizona® work with drivers every day to find that balance and can show you actual quotes at different deductible levels to help you understand which option truly saves money for your circumstances. Contact Insurance Brokers of Arizona® to schedule a consultation or request quotes online, and we’ll run the numbers specific to your situation and vehicle.