How to Find Cheap General Liability Insurance for Handymen

At Insurance Brokers of Arizona®, we understand that handymen need affordable protection for their businesses. Finding cheap general liability insurance for handymen can be challenging, but it’s essential for safeguarding your livelihood.

This guide will walk you through the process of securing cost-effective coverage without compromising on quality. We’ll explore key factors that influence insurance costs and provide practical strategies to help you find the best rates for your handyman business.

What Is General Liability Insurance for Handymen?

Definition and Core Coverage

General liability insurance serves as a fundamental safeguard for handymen, protecting against common risks associated with their daily operations. This type of insurance covers bodily injury, property damage, and personal injury claims that may arise from your work.

Specific Risks Covered

As a handyman, you face unique risks in your line of work. General liability insurance typically covers scenarios such as:

- A client tripping over your tools and sustaining injuries

- Accidental damage to a customer’s property during work

- Unintentional water damage caused during a plumbing repair

These situations can result in costly lawsuits or medical bills (which underscores the importance of proper coverage).

Legal Requirements and Client Expectations

While general liability insurance isn’t always legally mandated for handymen, many states require it for licensed contractors. Even if it’s not a legal requirement in your area, clients often expect or demand proof of insurance before hiring you.

A survey by The Hartford reveals that over 40% of small businesses (including handymen) are likely to experience a liability claim within a decade. This statistic highlights the need for adequate preparation.

Cost Considerations

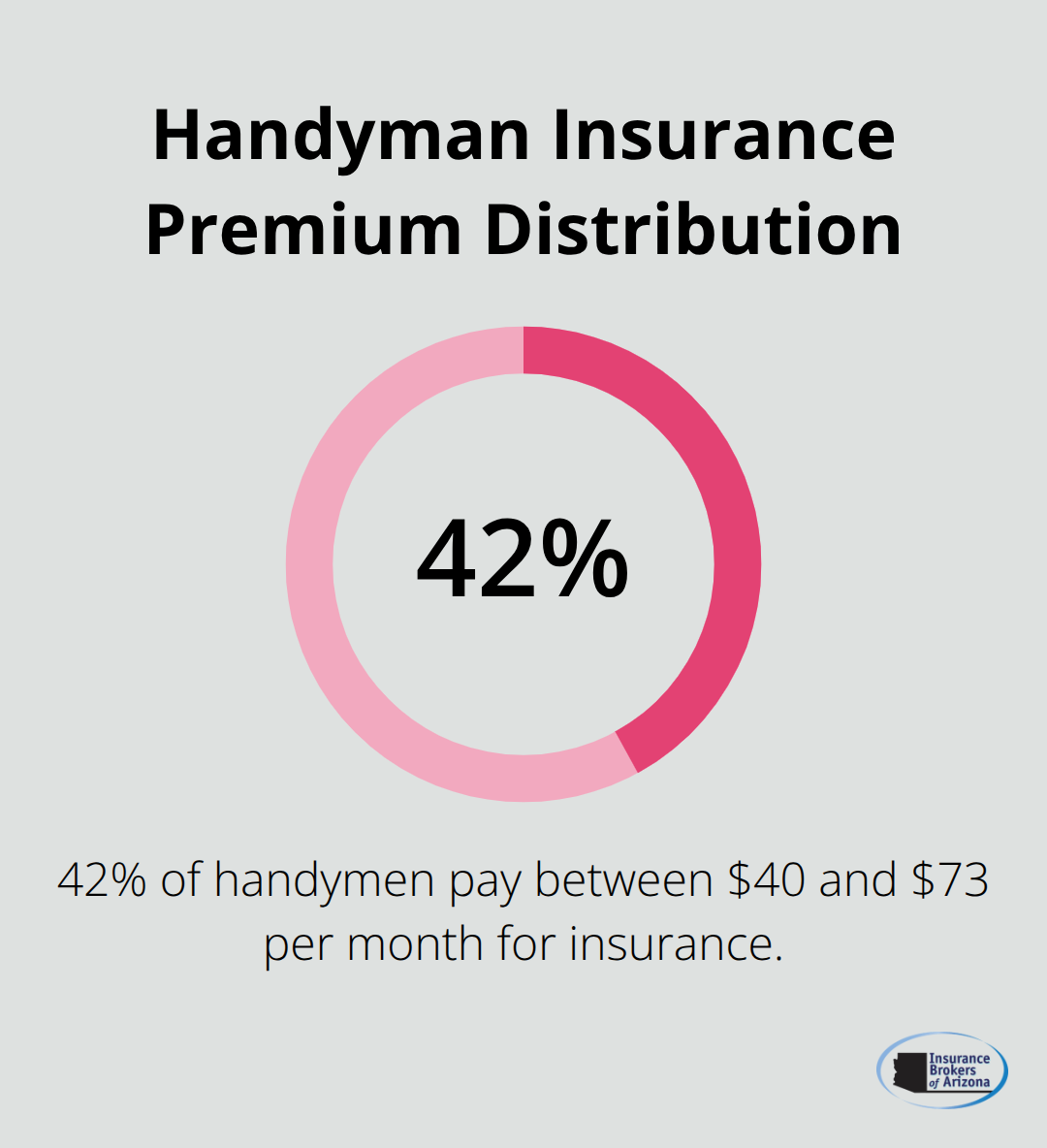

The cost of general liability insurance for handymen can vary widely. Data from Next Insurance shows that the average monthly premium is around $72. However, about 42% of their customers pay between $40 and $73 per month. These figures provide a ballpark estimate of what to expect, but your actual costs may differ based on various factors.

Handymen who take proactive steps to mitigate risks often secure more favorable rates. This can include maintaining a clean claims history, implementing safety protocols, and choosing appropriate coverage limits.

While finding affordable general liability insurance is important, it’s equally essential to ensure you have adequate coverage. The next section will explore the factors that affect your insurance costs and how you can use this knowledge to your advantage when seeking the best rates for your handyman business.

What Impacts Handyman Insurance Costs?

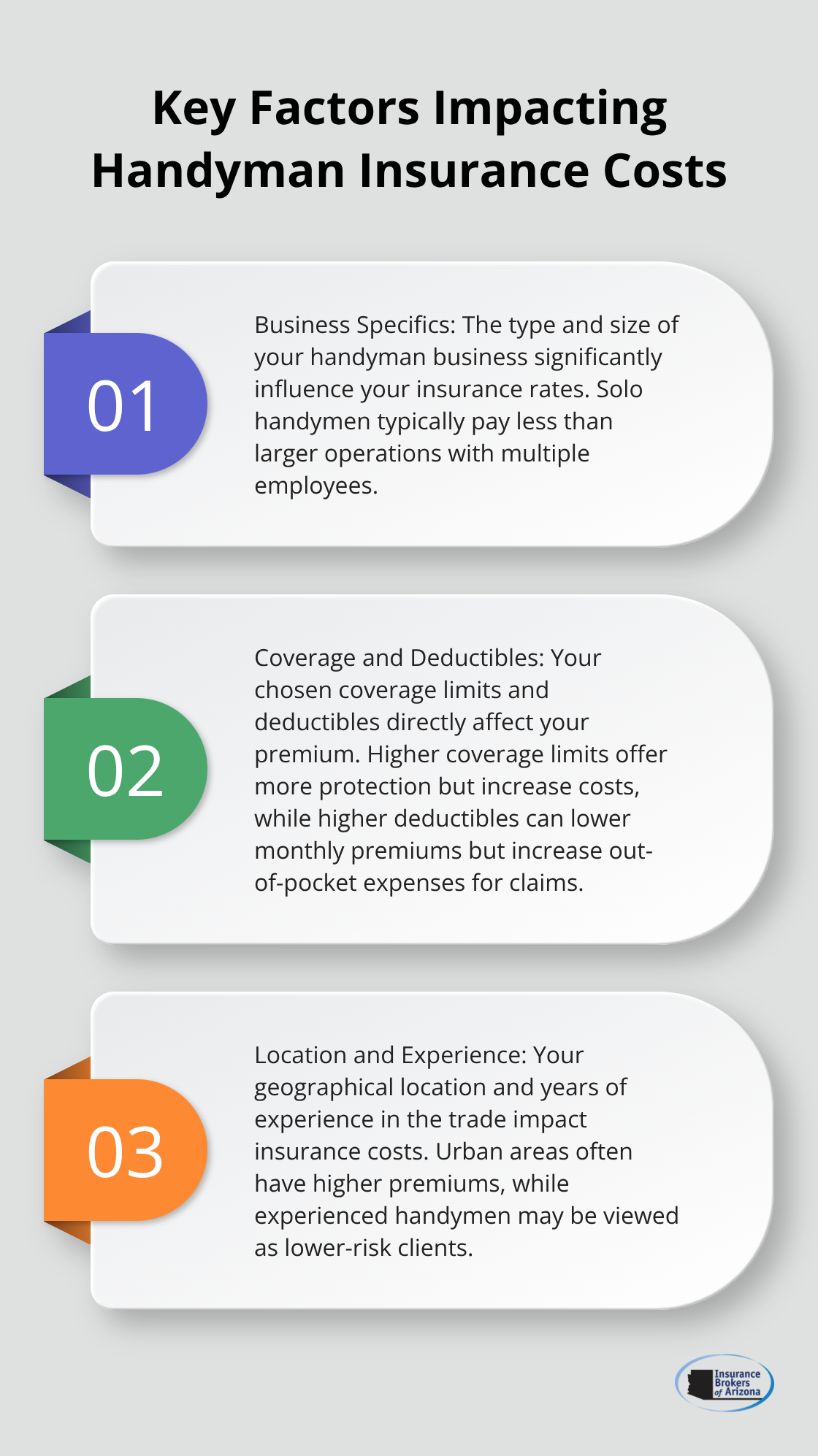

Business Specifics Matter

The type and size of your handyman business significantly influence your insurance rates. A solo handyman who works on small home repairs will likely pay less than a larger operation with multiple employees that tackles more complex projects. Data shows that the average cost for handyman general liability insurance ranges from $50 to $80 per month for sole proprietors. However, these figures can vary based on your specific business model.

Coverage and Deductibles: Finding the Right Balance

Your chosen coverage limits and deductibles directly affect your premium. Higher coverage limits offer more protection but increase costs. Conversely, a higher deductible can lower your monthly premium, but you’ll pay more out-of-pocket if you file a claim. Try to find a balance that provides adequate protection without straining your finances.

Location and Experience: Key Factors

Your geographical location plays a significant role in insurance costs. Handymen who operate in urban areas with higher living costs and more frequent claims typically face higher premiums than those in rural regions. Additionally, your years of experience in the trade can impact your rates. Insurance providers often view experienced handymen as lower-risk clients, potentially offering more favorable premiums.

Claims History and Safety Measures

Your claims history is a critical factor in determining your insurance costs. A clean record demonstrates to insurers that you’re a low-risk client, potentially leading to lower premiums. Implementation of robust safety measures and maintenance of a strong safety record can also work in your favor.

For example, regular safety training for yourself (and employees, if applicable) and use of proper protective equipment can showcase your commitment to risk mitigation.

Industry-Specific Risks

The specific services you offer as a handyman also impact your insurance costs. Some tasks (such as electrical work or roofing) carry higher risks and may result in higher premiums. Insurance providers assess these risks when calculating your rates. It’s important to accurately disclose all the services you provide to ensure proper coverage and avoid potential claim denials.

Now that we’ve explored the factors that influence handyman insurance costs, let’s examine strategies to find affordable general liability insurance without compromising on coverage quality.

How Can Handymen Secure Affordable General Liability Insurance?

At Insurance Brokers of Arizona®, we help handymen find affordable general liability insurance. Here are some proven strategies to help you secure cost-effective coverage without sacrificing protection.

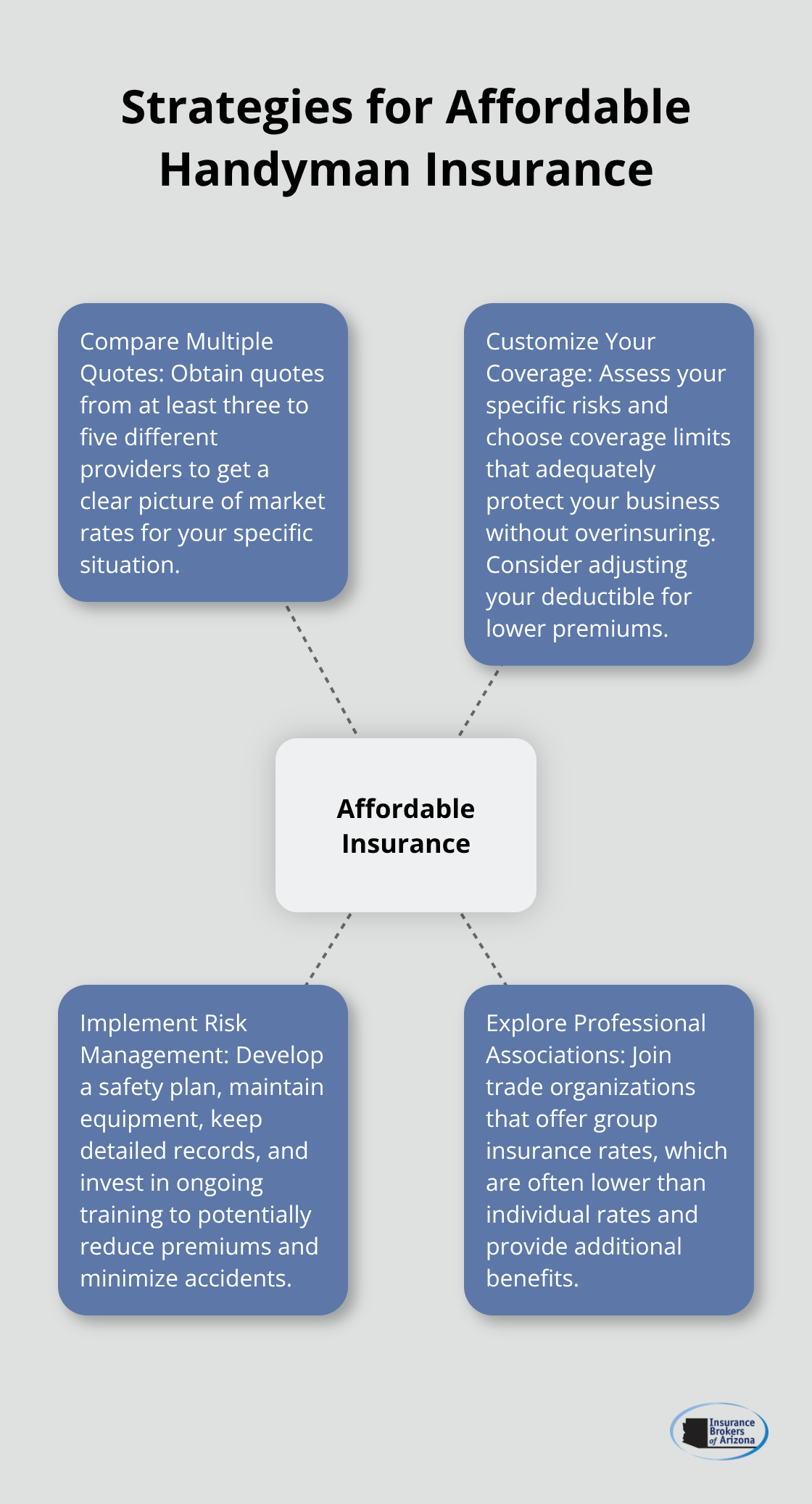

Compare Multiple Quotes

One of the most effective ways to find cheap general liability insurance is to compare quotes from multiple insurers. Each insurance company uses different criteria to calculate premiums, so prices can vary significantly. We recommend you obtain quotes from at least three to five different providers to get a clear picture of the market rates for your specific situation.

Online comparison tools can simplify this process, but working with an independent insurance broker often produces better results. Brokers have access to a wider range of insurers and can provide personalized advice based on your unique needs.

Customize Your Coverage

While it’s tempting to opt for the highest coverage limits, this isn’t always necessary or cost-effective. Assess your specific risks and choose coverage limits that adequately protect your business without overinsuring. For example, a handyman who primarily does small home repairs might not need the same level of coverage as one who works on large commercial projects.

Consider adjusting your deductible as well. A higher deductible typically results in lower premiums, but make sure you can comfortably afford the out-of-pocket expense if you need to file a claim.

Implement Risk Management Strategies

Insurance companies often offer discounts to businesses that demonstrate a commitment to safety and risk management. Here are some steps you can take:

- Develop and follow a comprehensive safety plan

- Regularly maintain and inspect your tools and equipment

- Keep detailed records of your work and any incidents

- Invest in ongoing training and certification

These measures not only help reduce your premiums but also minimize the likelihood of accidents and claims, which can lead to lower insurance costs in the long run. Implementing a robust risk management plan is one of the most impactful ways to lower your general liability insurance costs.

Explore Professional Associations

Many trade associations and professional organizations offer group insurance rates to their members. These rates are often lower than what you could secure on your own. For example, the National Association of Home Builders provides access to discounted insurance programs for its members.

Even if you don’t join for the insurance benefits, membership in professional organizations can provide valuable networking opportunities, educational resources, and industry insights that can help you grow your business and manage risks more effectively.

Final Thoughts

Finding cheap general liability insurance for handymen requires a strategic approach. You must compare quotes from multiple providers and customize your coverage to match your specific needs. Implementing robust safety measures and risk management strategies can lead to significant savings on your premiums while reducing the likelihood of accidents and claims.

Professional associations often offer group insurance rates, providing access to more affordable options. A clean claims history and experience in your trade can positively impact your insurance costs over time. Regular reviews of your insurance needs (especially as your business grows or changes) will help you maintain adequate protection without overspending.

We at Insurance Brokers of Arizona® offer personalized options tailored to handymen’s specific needs. With access to over 40 reputable carriers, we can help you find competitive rates for general liability insurance and other essential coverage types. Investing in the right insurance coverage is a fundamental step in securing the long-term success and stability of your handyman business.