Running an electrical business in Arizona means managing serious risks every single day. One mistake on a job site-a worker injury, damaged equipment, or property damage claim-can threaten your entire operation.

At Insurance Brokers of Arizona®, we’ve seen electricians lose thousands because they didn’t have the right coverage in place. This guide walks you through the insurance for electricians Arizona needs to protect their business and their team.

What Coverage Do Electricians Actually Need in Arizona

General Liability Protects Your Contracts and Your Wallet

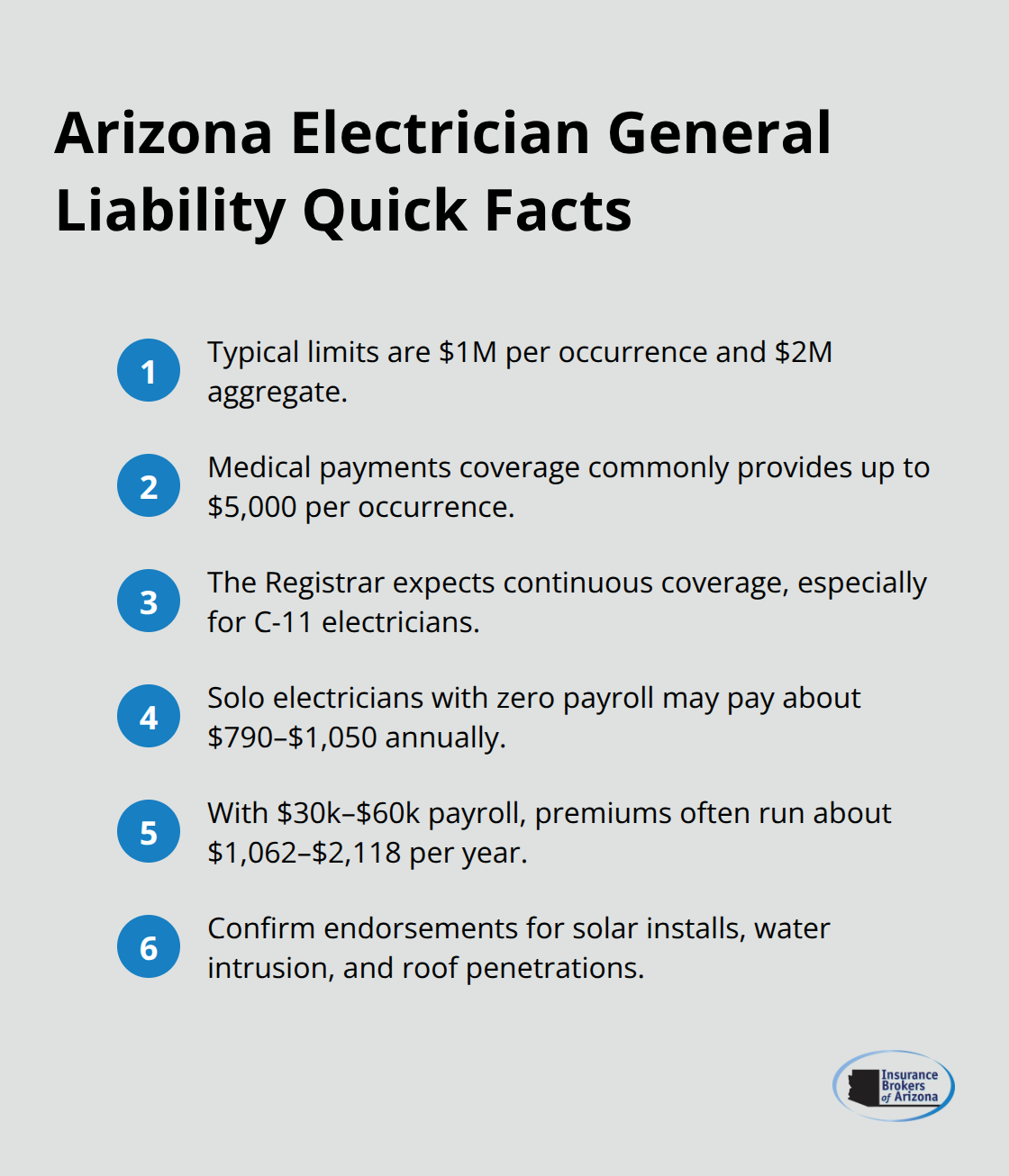

General liability insurance is non-negotiable if you want to win contracts in Arizona. Most clients require proof before awarding work, even though it’s not legally mandated for a contractor license. Standard coverage runs $1 million per occurrence and $2 million aggregate, which matches what municipalities, general contractors, and homeowners typically demand. Medical payments coverage up to $5,000 per occurrence is usually included, covering immediate treatment costs when someone gets hurt on your job site.

The Arizona Registrar of Contractors expects continuous general liability as part of your licensing requirements, especially for C-11 commercial electricians. Premium costs vary significantly based on payroll, trade classification, and location. A solo electrician with zero payroll might pay $790 to $1,050 annually, while someone with $30,000 to $60,000 in payroll typically pays $1,062 to $2,118 per year. If you install solar systems or handle high-voltage DC work, verify your policy covers solar installations and check for water intrusion and roof-penetration liability, since these exclusions appear frequently in standard policies.

Workers Compensation Covers Your Team and Satisfies State Law

Arizona requires workers compensation for any business with employees under A.R.S. §23-901, and the Arizona Registrar of Contractors enforces this requirement continuously. Your premium depends heavily on accurate payroll classification by job type, so misclassifying employees into higher-risk codes inflates costs unnecessarily. Run renewal audits to verify classifications match actual work performed.

Tools and Equipment Coverage Protects Your Most Valuable Assets

Tools and equipment coverage, sometimes called inland marine insurance, protects your meters, diagnostic gear, and power tools from theft or damage whether they’re stored in trucks or at job sites. Set your coverage limits based on total inventory value, since a single theft of specialized equipment can cripple operations for weeks. Arizona electricians face specific climate risks including monsoon season damage, extreme heat stress, and wildfire exposure in foothill communities, so confirm your policy includes these endorsements.

Completed Operations Coverage Extends Protection Years After Project Completion

Completed operations coverage matters critically because Arizona’s eight-year construction defect statute of repose, found in A.R.S. §12-552, means claims can surface years after project completion. Without extended reporting periods on your completed operations coverage, you lose protection once a policy renews. For electrical work on high-value projects like data centers, owners commonly require $2 million to $5 million in liability limits and specialized endorsements for computer equipment, so discuss project types with your carrier before bidding to avoid coverage gaps that could derail contracts.

These foundational policies form your baseline protection, but selecting the right insurance provider separates electricians who stay protected from those who face unexpected claim denials and coverage disputes.

What Claims Actually Drain Electrician Budgets in Arizona

Heat Injuries and OSHA Compliance Create Preventable Losses

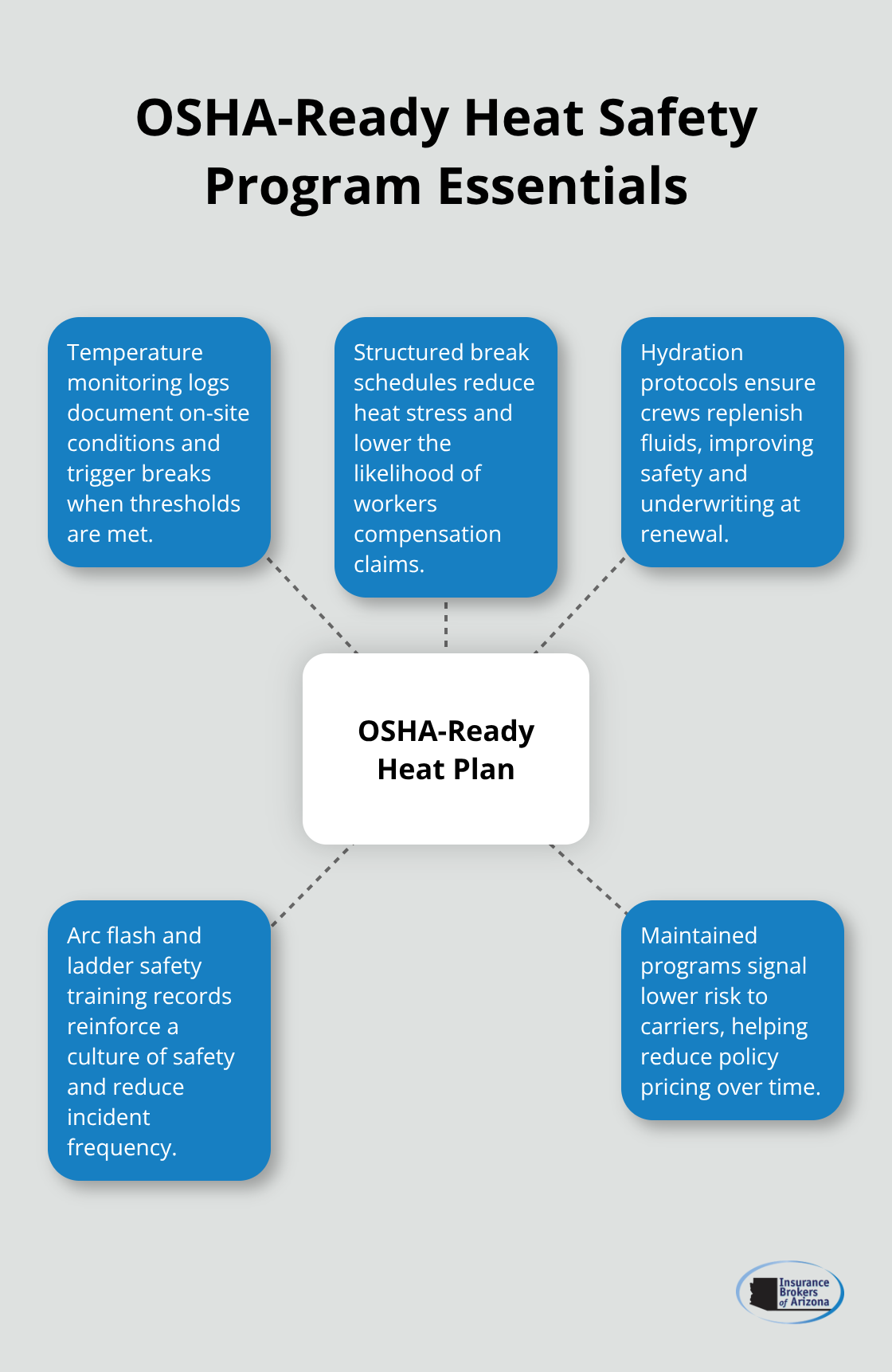

Electrical work in Arizona exposes your team to serious heat-related injuries during summer months. When an employee collapses from heat exhaustion on a 115-degree job site, workers compensation covers medical costs, but only if you’ve implemented a documented heat safety program meeting OSHA standards. Temperature monitoring logs, break schedules, and hydration protocols reduce claims frequency and improve your underwriting rates at renewal. Arc flash hazard assessments and ladder safety training records accomplish the same result. Carriers price policies lower when you maintain these programs in place.

Electrocution and Property Damage Claims Hit Hard in Arizona

Electrocution claims run higher in Arizona than national averages due to monsoon season moisture and dust storms creating conductive conditions. A single electrocution claim can exceed $500,000 in medical, legal, and settlement costs. Your workers compensation policy covers employee injuries, but third-party electrocution claims fall to general liability, which is why that $1 million per occurrence limit matters. Property damage from faulty wiring installations represents your second major exposure. When a customer’s home experiences an electrical fire traced back to your installation work, completed operations coverage becomes your financial lifeline. Without extended reporting periods on that coverage, you lose protection the moment your policy renews. Arizona’s eight-year construction defect statute means claims can surface seven years after you finish a job. Data center and semiconductor facility work amplifies this risk dramatically-owners require $2 million to $5 million in liability limits with specialized computer equipment endorsements. Missing these endorsements before bidding means either declining lucrative contracts or accepting uninsured exposure.

Subcontractors and Temporary Workers Create Hidden Gaps

Subcontractor and temporary worker gaps create the biggest coverage surprises. Many electricians assume their general liability covers subcontractor work, but most carriers require subcontractors to carry their own coverage and list you as additional insured on their policies. Without those certificates of insurance collected at the start of your policy year, your carrier may add subcontractor revenue to your audit, inflating your premium. Temporary workers and day laborers create similar problems. Incorrect classification in your workers compensation records triggers premium audits that can add thousands in back charges. Copper theft at job sites drains budgets constantly, and standard property coverage often excludes materials not yet installed. Your inland marine or tools and equipment policy must specifically cover raw materials stored on site. Electricians lose $15,000 to $40,000 in copper theft because their policies cover finished tools but not inventory waiting installation.

Vehicle and Equipment Storage Expose You to Uninsured Losses

Commercial vehicles storing equipment present another gap. If you use a personal truck for work and store diagnostic equipment or tools in it, your personal auto policy likely excludes business use. Adding a business-use endorsement costs far less than replacing stolen meters or paying for accident repairs from your operating account. Hired and non-owned auto liability fills the gap when you rent trucks or use employee-owned vehicles for jobs. Most electricians skip this coverage, thinking their general liability handles it-it doesn’t. One accident in a rented bucket truck with no hired auto coverage creates a coverage dispute that can cost $50,000 to $150,000 to resolve.

These gaps expose your business to financial losses that proper coverage selection eliminates. The next step involves finding an insurance provider who understands electrical contracting well enough to identify and close these gaps before they cost you money.

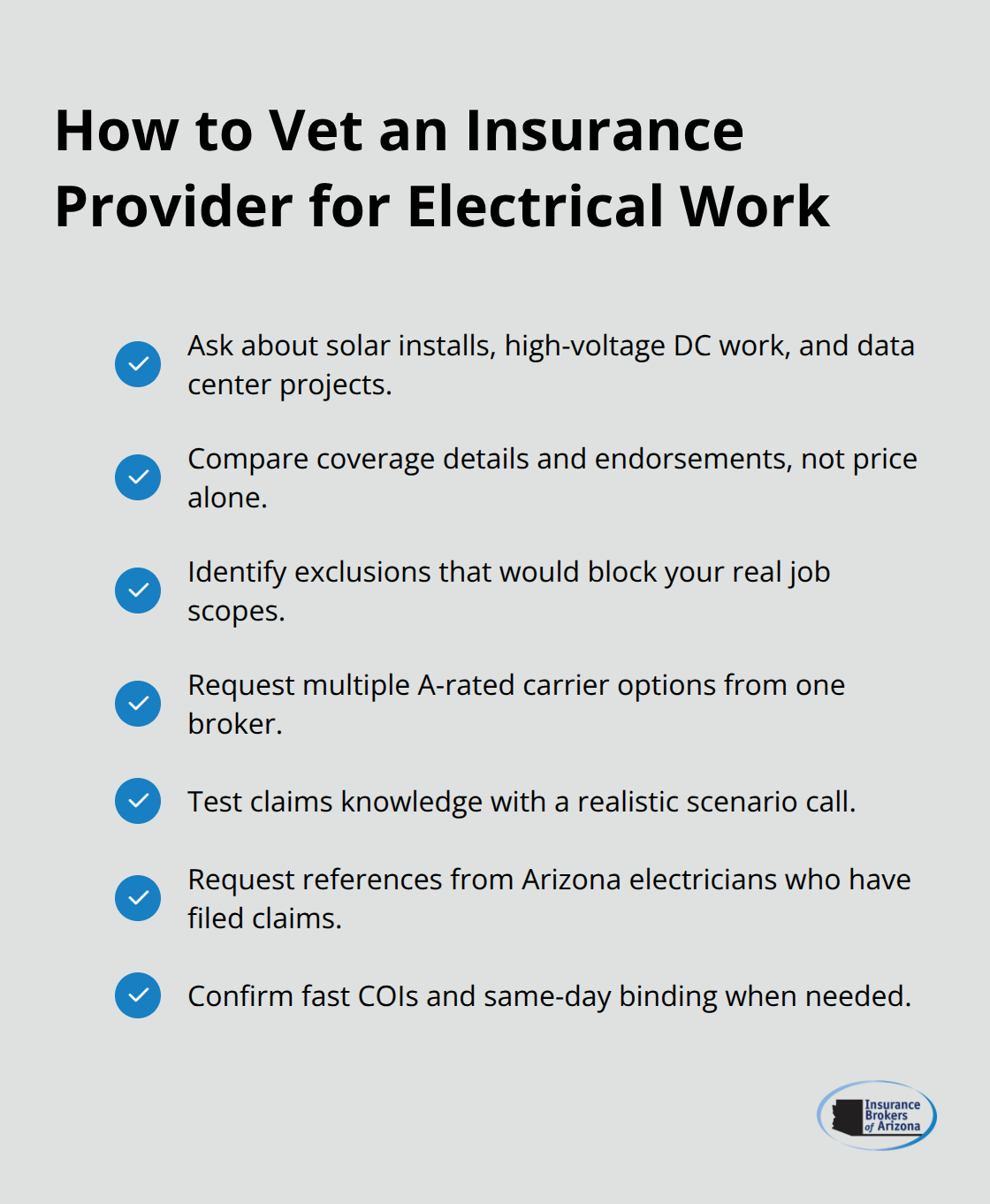

Picking an Insurance Provider Who Actually Understands Electrical Work

Finding the right insurance provider separates electricians who stay protected from those who face coverage gaps when claims hit. Most electricians shop by price alone, then encounter denied claims because their provider didn’t understand electrical-specific risks. The difference between a cheap policy and the right policy often comes down to whether your provider asks detailed questions about your work before quoting.

Ask the Right Questions Before You Accept a Quote

Does your potential provider ask whether you install solar systems, handle high-voltage DC work, or bid data center projects? If not, you’re receiving a generic quote that will exclude your actual work. Request quotes from multiple carriers, but don’t compare them side-by-side on price alone. Instead, compare what each quote actually covers.

One carrier might quote $2,100 annually for general liability with completed operations and solar endorsements included, while another quotes $1,850 but excludes solar work entirely. The cheaper option becomes expensive the moment you bid a solar installation and face a coverage denial.

Insurance Brokers of Arizona® maintains partnerships with over 40 reputable carriers, which means they can show you side-by-side options from multiple A-rated insurers in a single conversation rather than forcing you to call five different brokers independently.

Verify Genuine Electrical Contractor Experience

Verify that your provider has genuine experience with electrical contractors, not just construction in general. Ask your potential broker how many electrician clients they serve and what claims they’ve handled. A broker who works with roofers, plumbers, and electricians equally will miss electrical-specific exposures like arc flash hazard documentation or monsoon-season equipment damage. Electricians in Arizona face unique risks from extreme heat, dust storms, and wildfire exposure in foothill communities, so your provider needs to know which endorsements address these specific threats.

Evaluate Customer Service and Claims Response

When evaluating customer service, call your potential provider with a hypothetical claim scenario and observe how they respond. Ask what happens if a subcontractor gets injured on your job site and their family sues your company. Does your provider know whether your general liability covers that claim or whether it falls to workers compensation? A knowledgeable broker answers confidently. Request references from other Arizona electricians they’ve served, particularly those who’ve filed claims. Claims handling matters more than anything else because a fast, professional response when you’re stressed about a claim determines whether you stay in business or face financial disaster.

Prioritize Speed and Accessibility

The provider who returns calls within hours, coordinates with your carrier, and explains coverage clearly is worth paying slightly more for. Speed matters tremendously too. Coverage can often be secured the same day, and once active, your broker should issue certificates of insurance immediately rather than within business days, because job site delays cost you contracts. Your provider’s responsiveness during the application process predicts how they’ll handle claims when pressure is highest.

Final Thoughts

Protecting your electrical business in Arizona requires more than hoping nothing goes wrong. General liability, workers compensation, tools and equipment coverage, and completed operations protection form the foundation that keeps your operation running when claims hit. Without these policies in place, a single job site injury, equipment theft, or property damage claim can drain your savings and force you to turn down future contracts.

The coverage gaps we discussed throughout this guide represent real financial threats that electricians face constantly. Subcontractors without proper certificates of insurance, temporary workers misclassified in your payroll records, copper theft from job sites, and vehicle storage exposures drain thousands annually from electricians who thought they were protected. Arizona’s eight-year construction defect statute means claims surface years after you finish work, making completed operations coverage non-negotiable for your long-term survival.

Getting properly insured starts with finding a provider who understands electrical contracting specifically, not construction in general. Your broker needs to ask detailed questions about solar installations, high-voltage DC work, monsoon season exposures, and project types before quoting. Insurance Brokers of Arizona® partners with over 40 reputable carriers and can show you side-by-side options from multiple insurers in a single conversation, helping you build the insurance for electricians Arizona needs to protect your business and your team.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.