Arizona drivers overpay on auto insurance every single year. The average policyholder leaves hundreds of dollars on the table by missing discounts they actually qualify for.

We at Insurance Brokers of Arizona® know that auto insurance discounts in Arizona range from obvious ones like safe driver discounts to hidden gems most people never hear about. This guide shows you exactly where to find them.

Common Auto Insurance Discounts Available in Arizona

Safe Driver Discounts Cut Your Premium Significantly

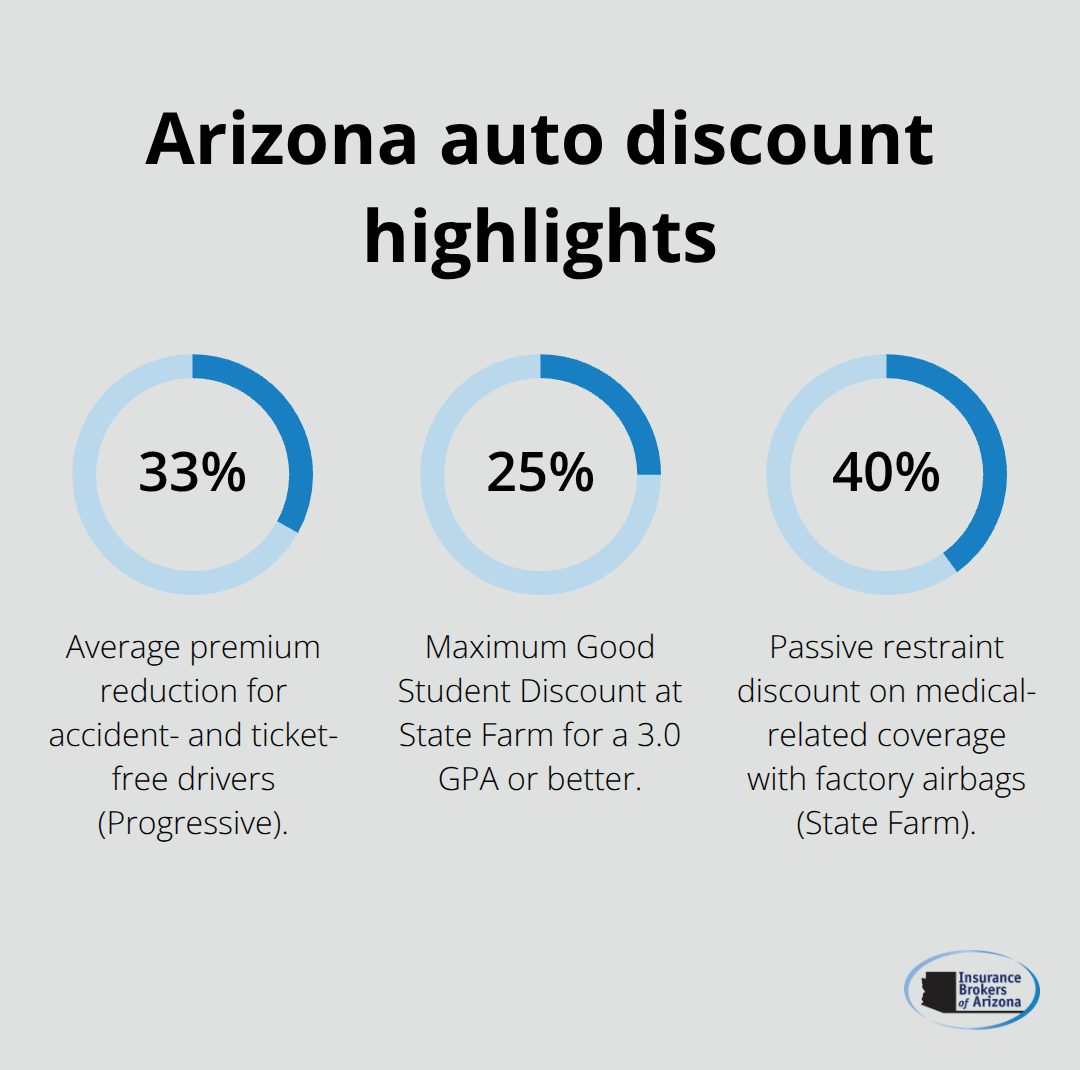

Safe driver discounts represent the most straightforward way to cut your premium, and the numbers prove it. Progressive data shows that drivers who stay accident- and ticket-free reduce their premiums by an average of 33 percent. That’s substantial.

GEICO rewards clean driving records directly on your policy, while State Farm’s Good Driver Discount becomes available after three or more years without moving violations or at-fault accidents. The key here is that this discount applies automatically once you qualify-you don’t need to ask for it, but you should verify it’s actually applied when your renewal hits.

If you’ve had a minor incident, some carriers like Progressive offer Small Accident Forgiveness, which means a claim under $500 won’t raise your rate at all. This matters because one mistake shouldn’t penalize you forever.

Multi-Policy Bundling Delivers Real Savings

Multi-policy bundling is where most Arizona drivers leave real money on the table. When you combine auto insurance with homeowners, renters, or condo coverage through the same carrier, bundling auto and homeowners insurance with the same carrier saves you between 5% and 30% on total premiums according to industry data. State Farm lets you bundle auto with homeowners, renters, condo, or life insurance to increase savings. GEICO offers similar multi-policy discounts that grow the longer you stay with them.

The bundling advantage extends beyond the initial discount-carriers reward loyalty, so staying bundled for years compounds your savings. This strategy transforms your insurance costs into a long-term advantage rather than a one-time savings opportunity.

Vehicle Safety Features Lower Your Rates

Vehicle safety features matter more than most people realize. Anti-theft devices, factory-installed airbags, and driver-assist technology qualify for discounts across most carriers. State Farm’s passive restraint discount can reach up to 40 percent on medical-related coverage if your vehicle has factory airbags. Newer cars with advanced safety systems typically qualify for better rates than older vehicles, which is one reason replacing an aging car sometimes lowers your premium despite the vehicle being worth more.

Understanding which safety features your vehicle has and reporting them to your carrier ensures you capture every available discount. The next section reveals discounts that most Arizona drivers completely overlook-opportunities that could save you hundreds more each year.

How to Actually Find Lower Rates on Your Auto Insurance

Shop Around and Compare Quotes from Multiple Carriers

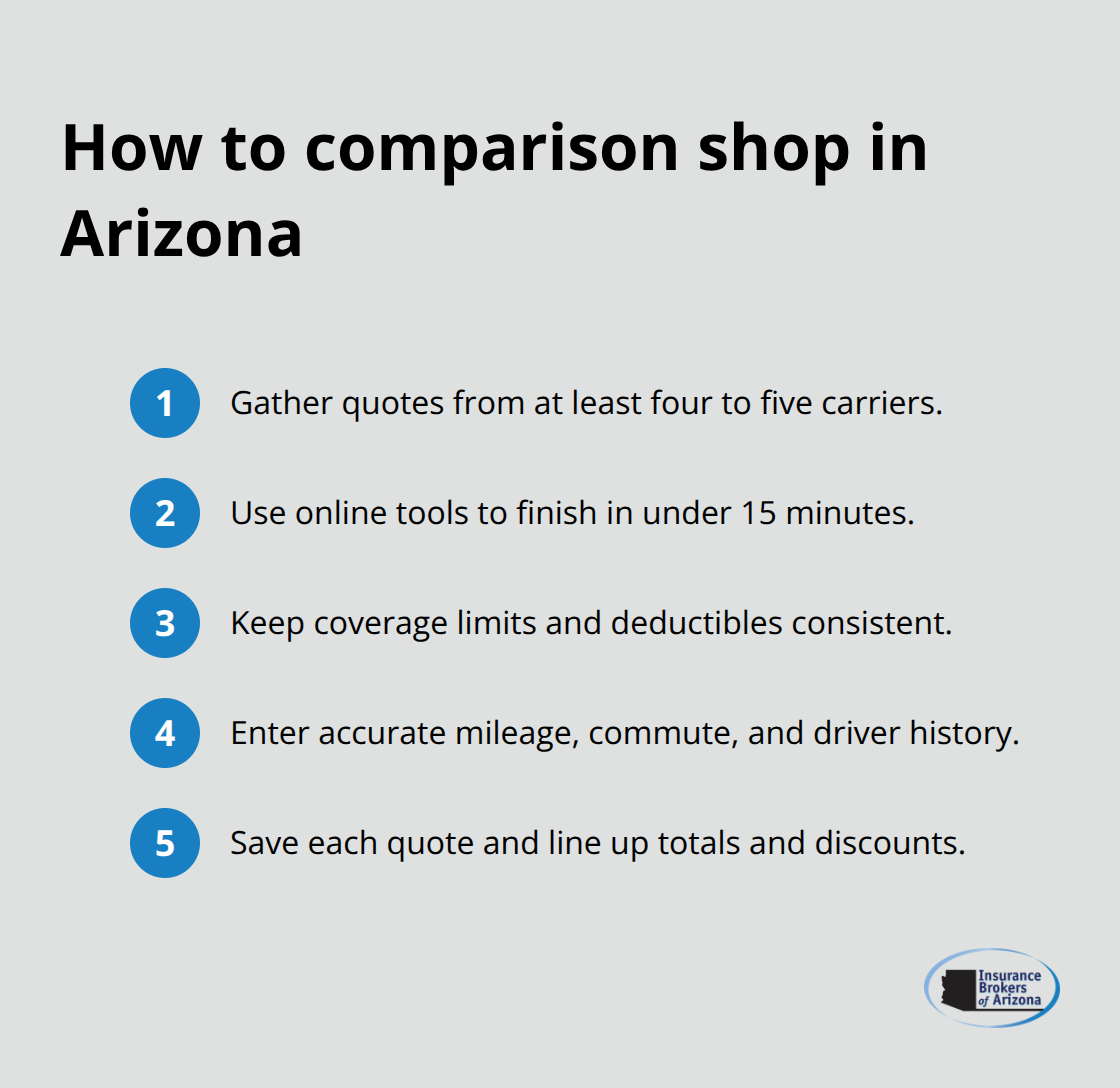

Shopping around remains the single most effective way to lower your premium, yet most Arizona drivers never do it. Price variation across insurers is substantial, and small changes in coverage or information yield meaningful savings. Progressive reports that 99 percent of their auto customers earn at least one discount, but this doesn’t mean Progressive offers the best rate for your situation. GEICO, State Farm, and regional carriers often price policies differently based on your driving record, vehicle type, and location.

Online quote tools make comparison effortless-you can gather quotes from five carriers in under 15 minutes without speaking to anyone. Pull quotes from at least four carriers before deciding, and provide honest answers about every detail: your commute distance, annual mileage, driving record, and current coverage limits all affect pricing. Inaccurate information inflates quotes and masks real savings opportunities.

Ask Carriers About Discounts You Don’t Know Exist

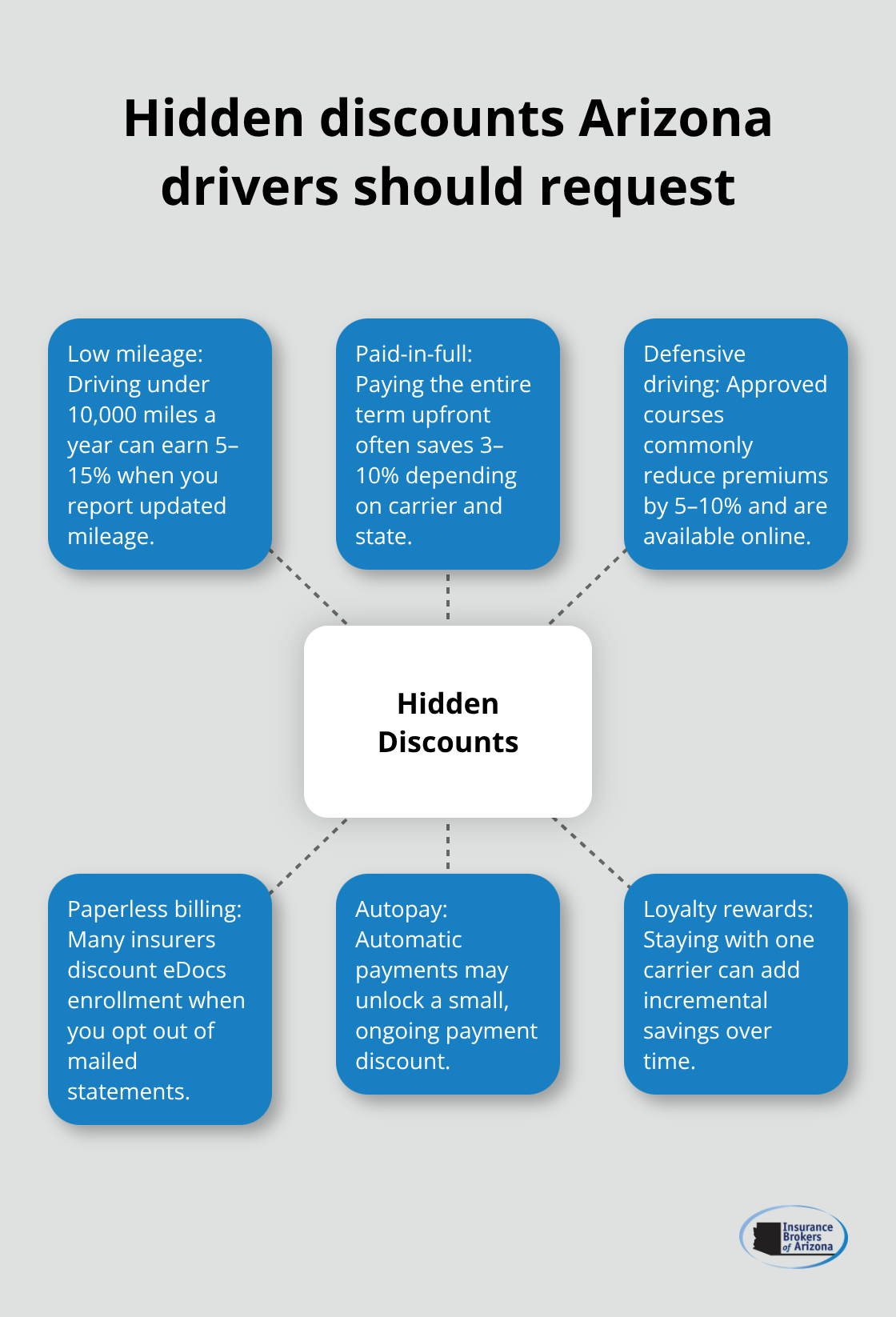

Once you’ve gathered quotes, the next step separates smart shoppers from average ones: asking carriers specifically about discounts you might not know exist. Call your current insurer and list every possible discount: good student status, defensive driving completion, low mileage, paid-in-full discounts, paperless billing, automatic payments, and loyalty rewards.

State Farm’s Good Student Discount reaches up to 25 percent for teen drivers with a 3.0 GPA or better, and this savings can last until age 25. GEICO offers defensive driver discounts for Arizona residents age 55 and older who complete an approved course. Many carriers provide paid-in-full discounts that rival autopay savings, yet few drivers ask about them. Most people assume they qualify for nothing-that assumption costs them hundreds annually.

Review Your Coverage Annually to Eliminate Waste

Your coverage deserves annual review because policies accumulate unnecessary add-ons or maintain limits higher than your situation requires. If you own an older vehicle worth less than $5,000, collision and comprehensive coverage may cost more annually than the vehicle’s value, making removal a smart financial move.

Major life changes trigger the need for immediate review: paying off a car loan, moving to a safer neighborhood, or reducing your annual mileage all warrant a policy adjustment. These shifts often qualify you for additional discounts or allow you to reduce coverage that no longer makes financial sense. The next section reveals discounts that most Arizona drivers completely overlook-opportunities that could save you hundreds more each year.

Hidden Discounts Most Arizona Drivers Miss

Low Mileage Discounts Reward Your Reduced Road Time

Low mileage represents one of the easiest discounts to qualify for, yet most Arizona drivers never mention it to their carriers. If you drive under 10,000 miles annually, you should receive a low mileage discount immediately-this isn’t optional or hidden, it’s standard across major carriers. Less time on the road means lower accident risk, so insurers reward you for it. Ask your current carrier what mileage threshold triggers the discount and confirm they’ve applied it. If you work from home, carpool, or use public transportation for your commute, this discount alone could save you 5 to 15 percent annually. Some drivers discover after five years of overpaying that they qualified all along.

The moment your mileage drops-whether from a job change or retirement-call your insurer and report the change immediately.

Paid-in-Full Discounts Offer Flexibility Most Drivers Ignore

Paid-in-full discounts operate differently than autopay discounts, and most carriers offer both, but drivers rarely ask about the paid-in-full option. Progressive, State Farm, and GEICO all provide discounts for paying your entire premium upfront rather than monthly installments. This discount typically ranges from 3 to 10 percent depending on the carrier and your state. The advantage here is flexibility: if you have cash available at renewal time, paying in full costs less than spreading payments across twelve months. Many people assume autopay is always the best option, but that’s not necessarily true for your situation. Compare both options when your renewal arrives and pick whichever saves more money. This decision changes annually as your circumstances shift, so revisit it every time your policy renews rather than assuming last year’s choice remains optimal.

Defensive Driving Courses Deliver Measurable Savings

Defensive driving course discounts apply to more age groups than most people realize. GEICO specifically offers this discount to Arizona drivers age 55 and older who complete an approved course, delivering measurable savings that justify the small time investment. Younger drivers also qualify with many carriers-State Farm recognizes driver training completion for drivers under 21, and completing an approved defensive driving course can reduce your premium by 5 to 10 percent. The courses themselves typically cost between 20 and 40 dollars and take three to four hours to complete, making the return on investment substantial if you save even 50 dollars annually. Online courses satisfy most carrier requirements, so you can complete the training on your schedule without attending a classroom. Some insurers require you to request the discount after completion, meaning the savings won’t apply automatically-you must proactively submit your course certificate to your agent or upload it through your online policy portal. This single step separates drivers who capture the discount from those who complete the course and receive no benefit.

Final Thoughts

Safe driver discounts deliver 33 percent savings for clean records, multi-policy bundling cuts 5 to 30 percent off your total premiums, and vehicle safety features, low mileage, paid-in-full options, and defensive driving courses each add measurable reductions that compound when stacked together. Most Arizona drivers qualify for multiple auto insurance discounts Arizona simultaneously but never claim them because they don’t ask. The gap between what you’re paying now and what you could pay represents real money that sits unclaimed in your policy.

Start this week by pulling quotes from at least four carriers, then call your current insurer and ask about every discount mentioned in this guide. Verify that safe driver discounts, bundling savings, and vehicle safety features actually appear on your policy. If you’ve reduced your mileage or completed a defensive driving course, report it immediately-these actions take two hours total and often save hundreds annually.

We at Insurance Brokers of Arizona® work with over 40 carriers, which means we see rate differences across companies that most drivers never discover on their own. Our team matches you with the carrier offering the best combination of price and coverage for your specific situation, and we identify every discount you qualify for without the hours you’d spend comparing quotes yourself. Contact Insurance Brokers of Arizona® today and let us show you what better rates look like.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.