Best Practices for Artisan Contractor Insurance: Protect Your Business

Artisan contractors face unique risks that standard business insurance simply doesn’t cover. A single lawsuit or equipment damage can wipe out years of profit, which is why best practices for artisan contractor insurance matter so much.

We at Insurance Brokers of Arizona® have helped hundreds of contractors build protection strategies tailored to their specific trades. This guide walks you through the coverage gaps, risk management steps, and policy choices that actually protect your business.

What Coverage Do Artisan Contractors Actually Need

The Foundation: General Liability and Beyond

General Liability Insurance covers third-party bodily injury and property damage claims, but it leaves your tools, equipment, and vehicles exposed. Contractors often assume their GL policy protects everything on the jobsite, then lose $15,000 in power tools from a truck bed and find the policy doesn’t cover it. This gap appears repeatedly because standard GL policies focus on liability, not asset protection. Your GL policy simply won’t replace those losses, which is why additional coverage layers matter.

Protecting Tools and Equipment in Transit

Inland Marine Insurance specifically protects mobile tools and equipment in transit and at worksites, which is where most tool theft happens. Industry data shows tool theft ranks among the most financially damaging claims in construction because tools move between sites and sit in trucks or trailers overnight. A single theft can halt your project timeline and drain cash reserves. This coverage applies regardless of who drives the vehicle, protecting your assets during transport and at job locations.

Workers’ Compensation and Vehicle Coverage

Workers’ Compensation becomes legally required once you hire employees in most states, and it covers medical expenses, lost wages, and rehabilitation costs for injured workers. Many solo contractors skip this thinking they don’t need it, but the moment you bring on a crew member, you face significant liability without it. Commercial Auto Insurance is non-negotiable if you use company vehicles for work. Personal auto policies explicitly exclude business use, so a crash during a jobsite visit leaves you personally liable and uninsured.

Trade-Specific Premium Realities

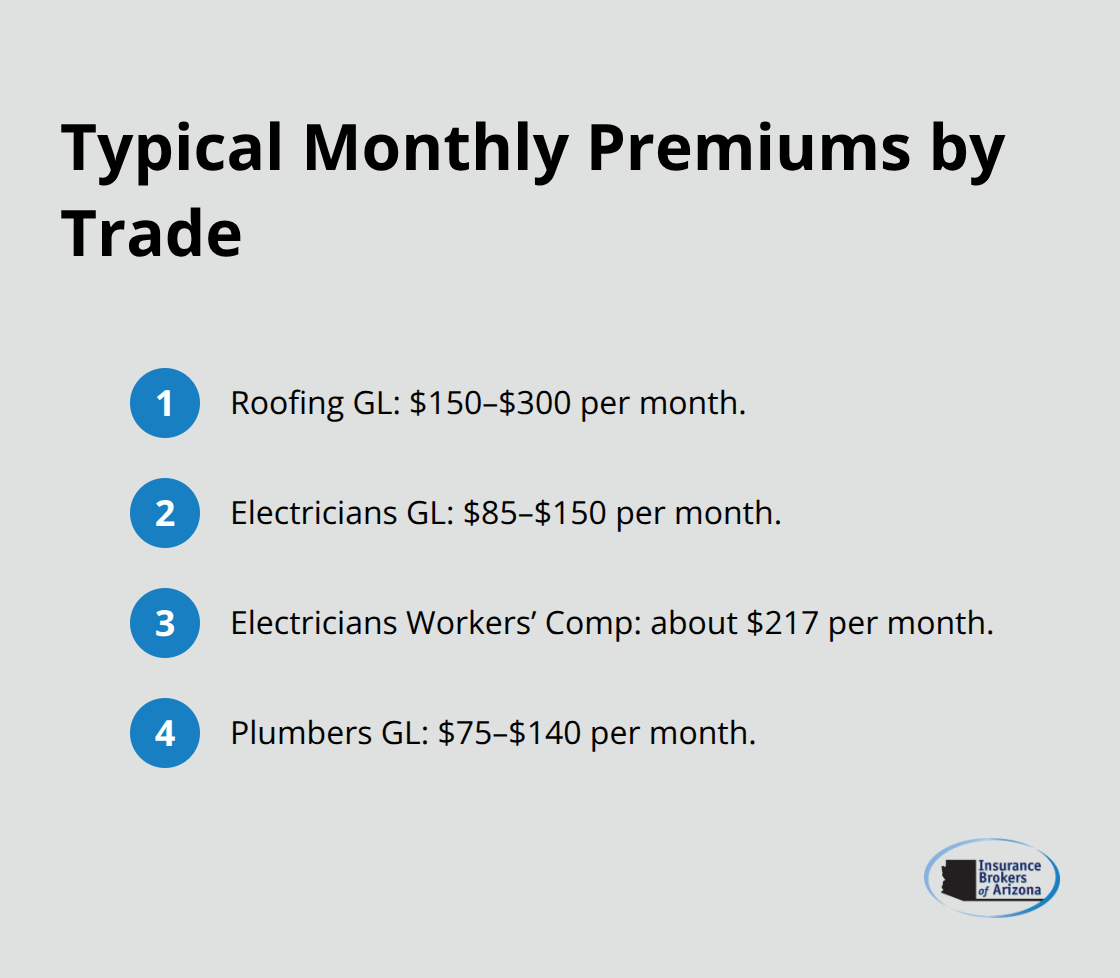

Roofing contractors pay the highest premiums among trades, typically $150–$300 monthly for GL, because height-related fall hazards create substantial risk. Electricians average $85–$150 monthly for GL and roughly $217 monthly for Workers’ Comp, reflecting electrical shock and ladder fall exposures. Plumbers generally pay $75–$140 monthly for GL, though costs rise in flood-prone areas where water damage claims spike.

These ranges reflect the actual exposure levels your trade carries, not arbitrary pricing.

Addressing Coverage Exclusions and Overlaps

A Business Owner’s Policy bundles property and liability coverage at a lower cost than buying separately, but it still doesn’t address trade-specific exposures. Electrical contractors who perform design work need Professional Liability coverage, which costs roughly $50–$100 monthly and covers errors or omissions in plans. Plumbers who weld face coverage exclusions under standard plumbing policies because welding creates a separate fire and burn exposure that requires specific endorsement. Multi-trade contractors working alongside other trades create overlapping risk exposures that standard policies never account for. The solution isn’t buying maximum limits everywhere; it’s tailoring coverage to your actual work.

Managing Claims History and Future Protection

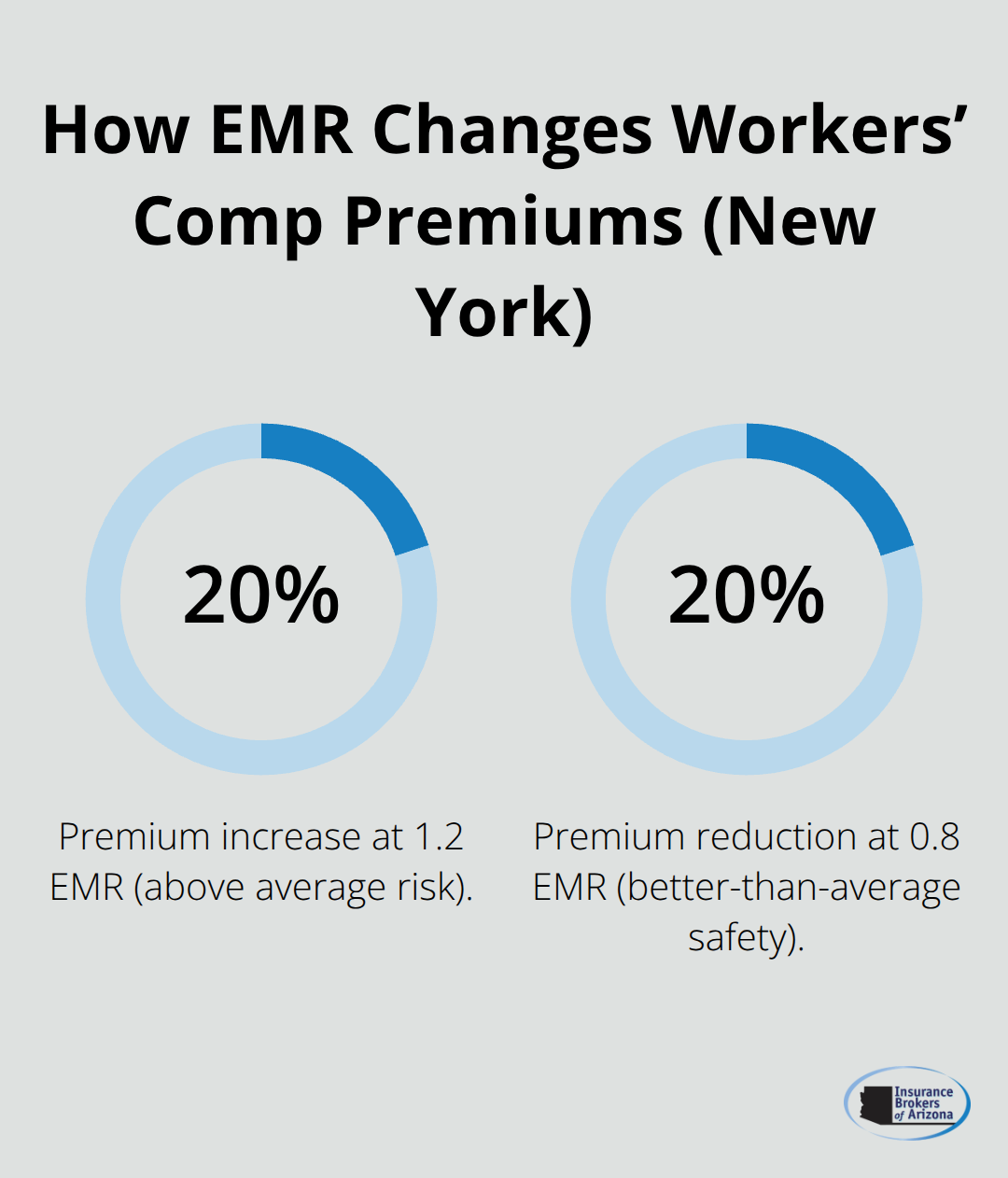

Experience Modification Rate heavily influences Workers’ Comp premiums. In New York, a 1.0 EMR is average, a 1.2 EMR raises premiums by about 20%, and a 0.8 EMR reduces them by about 20%, with claims staying on record for three years.

Proactive safety programs and documented training directly lower EMR and premiums. Umbrella Liability Insurance provides extra protection above your underlying policies and becomes increasingly important as projects grow in size and risk. The market for umbrella limits is tightening due to rising verdicts, so preparing now with strong primary coverage and documented risk controls positions you better than waiting until a major claim forces the issue. These layers of protection work together to address the real exposures your business faces, which is why selecting the right provider and understanding policy terms becomes your next critical step.

How to Lower Claims and Keep Your Business Running

Trade-Specific Safety Protocols Cut Claims and Premiums

Roofing contractors who implement formal safety training cut their Workers’ Comp claims by measurable amounts, directly lowering their Experience Modification Rate and future premiums. The data is clear: a 1.0 EMR in New York represents average risk, but contractors with documented safety programs regularly achieve 0.8 EMR or better, cutting premiums by approximately 20% over three years. A contractor with five employees paying $500 monthly in Workers’ Comp at a 1.0 EMR drops to roughly $400 monthly at 0.8 EMR, saving $600 annually just from one rate improvement.

Your trade-specific hazards demand targeted action. Electricians face electrical shock and ladder falls as their primary claim drivers; lockout-tagout procedures and harnesses on any work above six feet directly address these exposures. Plumbers encounter water damage liability and flood exposure; inspecting water lines before work starts and documenting site conditions prevent claims before they happen. Roofers working at height need fall protection systems that meet OSHA standards and documented proof that crews trained on those systems. The key is matching your safety protocols directly to your trade’s actual hazards, not adopting generic safety checklists that don’t apply to your work.

Documentation Transforms Safety Efforts Into Lower Premiums

Keep incident logs for every near-miss, every minor injury, and every safety observation on the jobsite. Carriers reviewing your renewal specifically look at these records to assess whether you actively manage risk or simply hope claims don’t occur. A contractor who reports three near-misses and implements corrective actions demonstrates stronger risk management than one who reports zero incidents, because zero often signals poor tracking rather than perfect safety.

Maintain tool inventories with serial numbers and photographs; when theft occurs, you’ll have proof for your Inland Marine claim rather than guessing at replacement costs. Store equipment in locked, secure locations and photograph storage setups to document your loss prevention efforts. Carriers offer premium discounts for documented safety features and controls, so comprehensive records directly reduce your costs. Your EMR, claims history, and safety documentation follow you across renewals and carriers, so investing in prevention now compounds into lower costs for years. A single major claim can spike your EMR for three years; preventing that claim through documented safety work costs far less than managing the aftermath.

Working With Advisors Who Understand Your Trade

Review your policies annually with a construction-focused advisor who understands your specific trade and project mix. A broker who serves electricians differently than roofers catches coverage gaps that generic advisors miss. Specialized programs exist precisely because artisan contractors need tailored solutions, not one-size-fits-all policies. Your advisor should ask about your specific work activities, the sites where you operate, and the equipment you use-not just offer standard templates. This level of attention reveals whether your current coverage actually protects your business or leaves dangerous gaps. When your broker understands roofing exposures, electrical work, or plumbing risks at a detailed level, they spot exclusions and overlaps that matter. The right partnership means your insurance adapts as your projects grow in size and complexity, keeping your protection aligned with your actual operations rather than falling behind market changes.

Finding the Right Broker for Your Trade

Premium Differences Demand Specialized Expertise

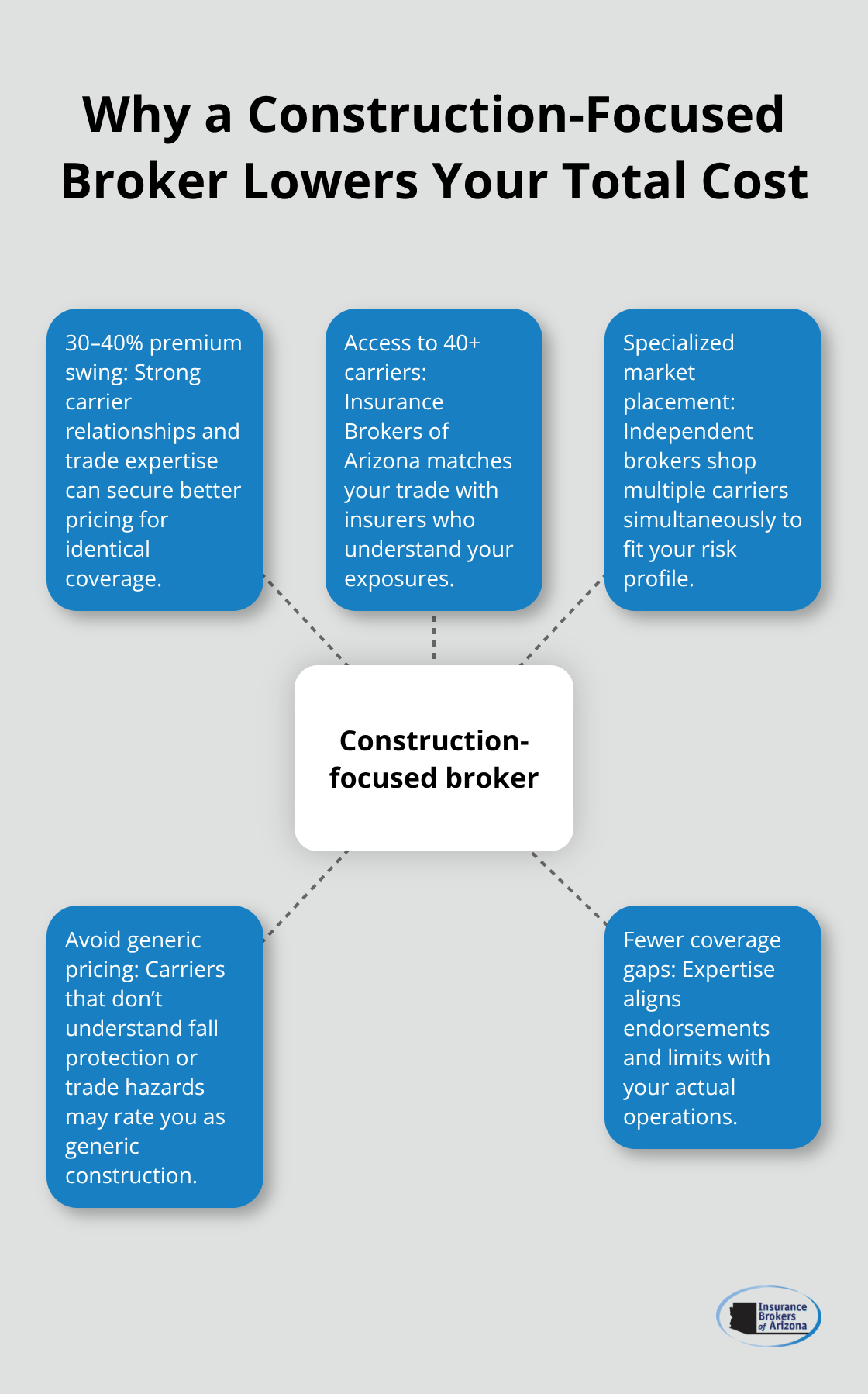

Comparing policies across carriers reveals a hard truth: premium differences for identical coverage swing 30–40% depending on the broker’s relationships and your trade specialization. A roofing contractor shopping solo might receive quotes from carriers that don’t understand fall protection work, pricing you as generic construction rather than specialized roofing. An independent broker with construction focus shops multiple carriers simultaneously, placing you with insurers who actively write roofing business and price accordingly.

Insurance Brokers of Arizona® partners with over 40 carriers, which means we can match your specific trade to insurers who understand your exposures rather than forcing you into standard templates. The difference between a generic business insurance agent and a construction-focused broker isn’t small talk-it’s thousands of dollars in annual premiums and coverage gaps that won’t appear until you file a claim.

Questions That Separate Real Brokers From Template Pushers

Your broker should ask detailed questions about your specific work before quoting anything. Do you perform electrical design work, or only installation? Do your plumbers handle any welding? Are your crews working at heights exceeding six feet? These details determine which endorsements you actually need and which ones waste money. A broker who quotes you without understanding whether you’re a solo electrician or a roofing company with ten employees is simply pulling templates. Request quotes that itemize each coverage type with limits and deductibles clearly stated, allowing you to compare actual protection rather than total premium figures. Avoid brokers who push umbrella coverage without reviewing your primary policies first-umbrella insurance only works when your underlying general liability, workers’ compensation, and commercial auto policies have strong limits and documented risk controls. Ask about Experience Modification Rate discounts and whether the carrier offers premium credits for documented safety training, because these reductions compound significantly over three years.

Reading Policy Language Catches Hidden Exclusions

Red flags appear quickly when you read policy language carefully. Exclusions for specific trades hide in endorsement sections, not in marketing materials. A plumbing policy excluding welding work means any claim involving heat or flame gets denied, even if welding was incidental to the main work. Request the actual policy documents before purchase, not summaries or brochures, and have your broker explain what each exclusion means for your specific projects. If a carrier’s policy excludes multi-trade overlaps or subcontractor work, that exclusion will haunt you the moment a claim involves another trade on the jobsite. Vague language around coverage territory matters too-if your policy covers work within Arizona only, you’re uninsured the moment you cross state lines.

Matching Certificates of Insurance to Actual Coverage

General contractors often require subcontractors to maintain specific policy limits and endorsements; your broker must confirm your actual policy matches what you promised on certificates of insurance, because mismatches create claim denials when you need protection most. Deductibles deserve equal scrutiny-a $2,500 deductible sounds reasonable until you file a claim and realize you’re paying that amount out of pocket repeatedly. Compare deductible levels across your entire package, because bundling policies often allows you to adjust deductibles strategically, reducing your highest-risk coverage to $1,000 while increasing lower-risk coverage to $2,500, lowering total premiums without sacrificing critical protection.

Final Thoughts

Best practices for artisan contractor insurance come down to matching your coverage to your actual work, not to generic templates that miss your trade’s specific exposures. You’ve learned that general liability alone leaves your tools unprotected, that workers’ compensation becomes legally required the moment you hire employees, and that trade-specific exclusions hide in policy language until a claim forces them into the open. The contractors who avoid catastrophic losses understand their exposures, document their safety efforts, and work with advisors who actually know their trade.

Contact a construction-focused broker who can review your current policies against your actual work activities and bring your project details, equipment inventory, and crew size to that conversation. Ask whether your coverage addresses tool theft, whether your workers’ compensation reflects your current payroll, and whether your commercial auto policy covers all vehicles you use for business. Request itemized quotes that show each coverage type with limits and deductibles clearly separated, not bundled totals that hide what you’re actually buying.

Contractors who implement documented safety programs lower their Experience Modification Rate and cut workers’ compensation premiums by 20% or more over three years, with those savings compounding annually. Contact Insurance Brokers of Arizona® today to review your coverage and identify the gaps that could derail your business, since we work with over 40 carriers to match your specific trade to insurers who understand your exposures rather than forcing you into standard templates.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.