How to Get Commercial Truck Insurance You Need

Running a commercial trucking operation means managing serious liability and asset protection. If you need commercial truck insurance, understanding your coverage options is the first step toward protecting your business.

At Insurance Brokers of Arizona®, we help fleet owners navigate the specific policies that match their operations. This guide walks you through the coverage types, rate factors, and selection process you need to make informed decisions.

What Coverage Types Do You Actually Need?

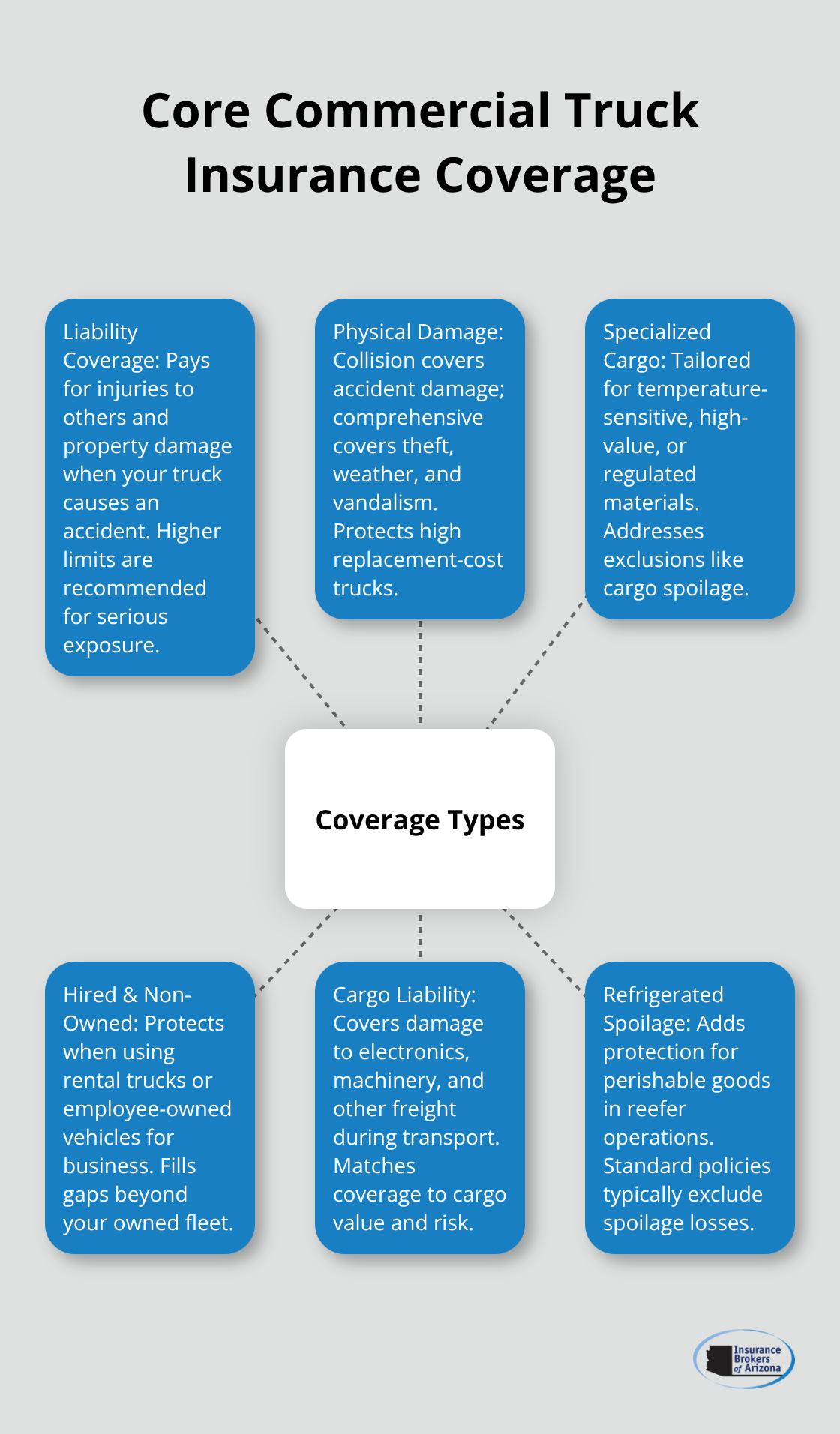

Liability Coverage Protects Against Serious Claims

Liability coverage is non-negotiable for commercial trucking operations. This coverage pays for injuries to other people and damage to their property if your truck causes an accident. In Arizona, the minimum liability requirement is $15,000 for bodily injury per person and $30,000 for property damage per accident, but these limits are dangerously low for trucking operations.

Most fleet operators carry $100,000 or higher per occurrence because a single serious accident can easily exceed state minimums. Medical costs for severe injuries regularly reach $500,000 or more, and property damage claims from multi-vehicle collisions add up quickly. We recommend liability limits of at least $250,000 per occurrence for most commercial trucking operations, with higher limits if you transport hazardous materials or operate on highways regularly.

Physical Damage Coverage Protects Your Fleet Assets

Physical damage coverage protects your actual trucks through collision and comprehensive policies. Collision coverage pays for damage from accidents, while comprehensive covers theft, weather, and vandalism. A typical commercial truck replacement cost ranges from $80,000 to $150,000 depending on size and equipment, making this coverage essential for protecting your fleet assets.

Without physical damage coverage, a single accident or theft can force you to absorb the full replacement cost out of pocket. This coverage becomes especially important if you financed your trucks through a lender, as most require it as a condition of the loan.

Specialized Coverage Matches Your Cargo Type

Specialized cargo coverage matters significantly if you haul temperature-sensitive goods, high-value freight, or regulated materials. Refrigerated truck operations need coverage specifically for cargo spoilage, which standard policies exclude entirely. If you transport electronics or machinery, cargo liability covers damage that occurs during transport.

Hired and non-owned vehicle coverage protects you when drivers use rental trucks or employee-owned vehicles for business purposes. This coverage is often overlooked but becomes critical when your operation needs flexibility beyond your owned fleet. Your specific cargo type determines which specialized options you actually need, so audit your shipment types before selecting policies.

Understanding these three coverage categories positions you to make smart decisions about your fleet protection. The next step involves recognizing what factors actually drive your insurance rates.

What Drives Your Commercial Truck Insurance Costs

Insurance carriers price commercial truck policies using hard data about your operation, not guesswork. The age and type of truck you operate matters tremendously because older vehicles cost more to insure than newer ones.

Vehicle Age and Type Impact Your Premium

A 2024 model truck with modern safety features typically costs 15-25% less to insure than a 2010 model, according to industry data from the American Trucking Associations. Carriers recognize that newer trucks have advanced braking systems, collision avoidance technology, and better structural integrity that reduce accident severity. If you operate a mix of ages in your fleet, prioritize getting the older units off the road or upgrading them with safety equipment. Specialized trucks like refrigerated units or tankers carry higher premiums because they require additional certifications and present unique operational risks compared to standard dry vans.

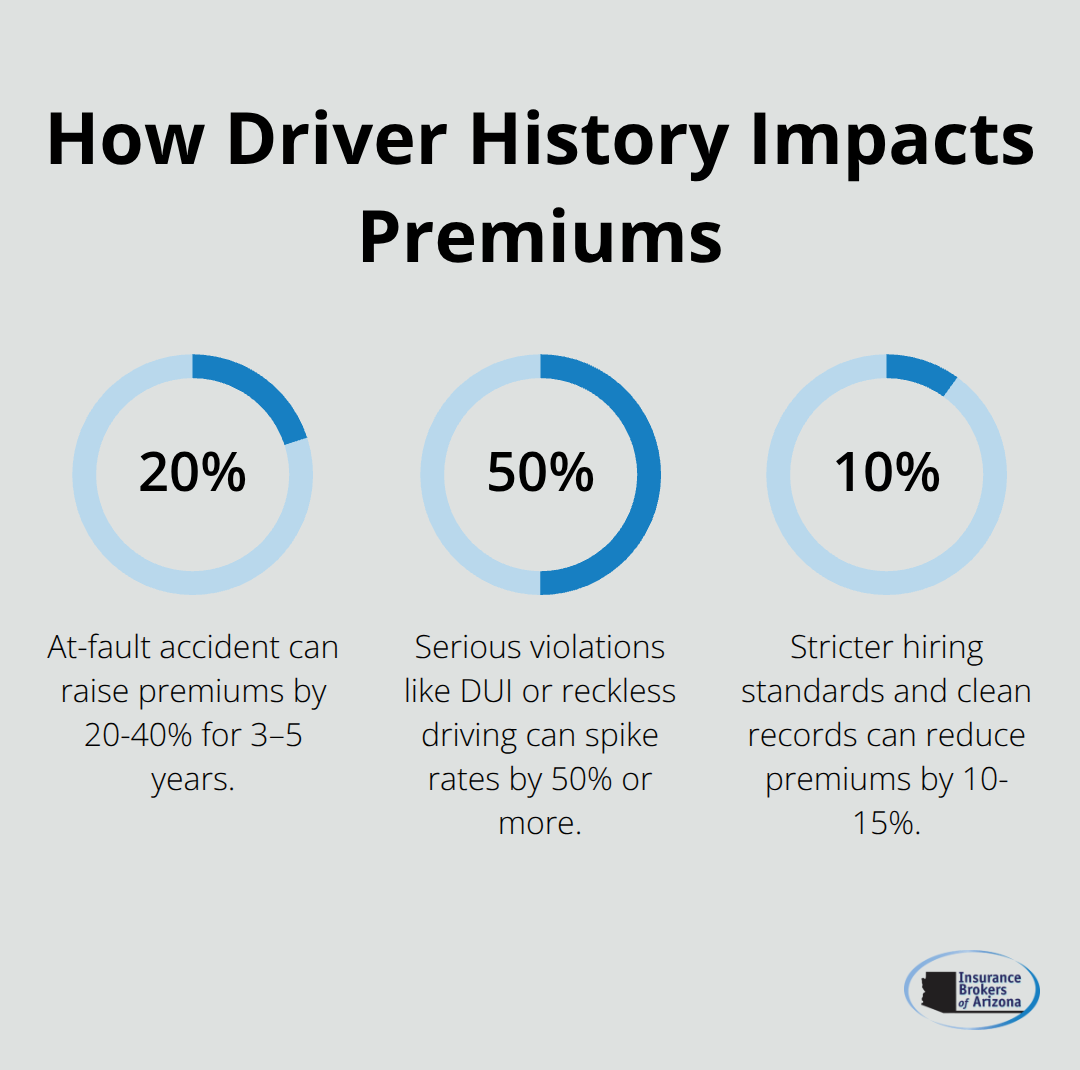

Driver History Shapes Your Rates Most Significantly

Your driver history determines more of your rate than almost any other factor. A single at-fault accident increases your commercial truck insurance premium by 20-40% for three to five years, while serious violations like DUI or reckless driving spike rates by 50% or more. Fleets reduce their premiums by 10-15% simply through implementing stricter hiring standards and requiring drivers with clean records. This direct connection between driver quality and cost makes your hiring process a financial decision, not just an operational one.

Mileage and Routes Affect Your Exposure Level

Annual mileage and the specific routes you operate shift your costs significantly. Carriers charge more for drivers who accumulate 100,000+ miles annually compared to those running 50,000 miles, because exposure increases accident probability. Long-haul operations across multiple states pay higher premiums than regional routes because interstate driving carries greater risk. If you concentrate routes in Arizona versus cross-country hauling, your premium reflects that reduced exposure. Urban delivery routes typically cost less than highway operations because speeds are lower and accident severity is reduced.

These three factors-vehicle specifications, driver quality, and operational exposure-form the foundation of how carriers calculate your rates. Understanding what moves your premium allows you to make strategic decisions about fleet composition and hiring practices. The next step involves comparing how different carriers apply these factors to your specific operation.

Steps to Choose the Right Commercial Truck Insurance Policy

Audit Your Operations Before Requesting Quotes

Start with your actual operations, not assumptions about what you might need. Pull your shipping records from the last 12 months and list every cargo type you transport, your annual mileage by route, and your current fleet composition. This exercise takes two hours but prevents expensive coverage gaps or overpaying for unnecessary add-ons.

If you haul refrigerated goods one month and standard freight the next, you need cargo spoilage coverage. If 80% of your routes stay within Arizona and 20% cross state lines, your exposure calculation changes significantly. Carriers ask detailed questions about these specifics anyway, so gathering this data upfront accelerates the quoting process and produces more accurate rate comparisons.

Request Quotes from Multiple Carriers

Once you have your operational profile documented, request quotes from at least three carriers. The National Association of Insurance Commissioners data shows that commercial truck insurance rates vary by 30-50% across carriers for identical coverage, making comparison essential. When you receive quotes, verify that each one covers the same liability limits, deductibles, and specialized options before comparing prices. A quote for $2,500 annually with a $1,000 deductible is not comparable to one at $2,200 with a $5,000 deductible. Carriers also apply different surcharges for driver violations or older fleet vehicles, so a $300 price difference might reflect different risk assessments rather than better pricing.

Compare Quotes with Transparency

Request quotes that break down the premium by coverage type so you see exactly what you’re paying for liability, physical damage, and specialized coverages separately. This transparency prevents surprises when your renewal comes around and shows you where rate increases actually occur. Insurance Brokers of Arizona® partners with over 40 carriers, which means you access quotes that most brokers cannot obtain, giving you genuinely competitive options that reflect your specific operation. Verify that each carrier applies the same driver surcharges and vehicle depreciation calculations (these vary significantly between insurers). The most affordable quote often comes from a carrier that recognizes your specific operational profile and risk level rather than one that applies generic pricing formulas.

Final Thoughts

Your commercial truck insurance strategy should prioritize liability coverage first because a single serious accident can bankrupt your operation without adequate protection. Physical damage coverage ranks second since replacing an $80,000 to $150,000 truck out of pocket destroys cash flow. Specialized cargo coverage comes third only if your specific shipment types require it, but don’t skip this step if you haul temperature-sensitive goods or high-value freight.

Working with a broker eliminates the guesswork from this process. When you need commercial truck insurance, brokers access quotes from multiple carriers simultaneously rather than forcing you to contact each one individually. We at Insurance Brokers of Arizona® partner with over 40 carriers, which means you receive genuinely competitive options that reflect your actual operational profile instead of generic pricing formulas.

Gather your shipping records, fleet composition, and driver information, then contact Insurance Brokers of Arizona® to discuss your specific operation. We’ll identify the coverage gaps in your current protection and show you how much you can save by switching to carriers that recognize your risk profile. Protecting your commercial fleet starts with understanding what you actually need, not what a generic policy offers.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.