Artisan contractors face unique risks that standard business insurance simply doesn’t cover. Your specialized skills, high-value projects, and custom techniques require artisan contractor insurance coverage designed specifically for your trade.

At Insurance Brokers of Arizona®, we’ve seen too many skilled craftspeople operate without adequate protection. This guide walks you through the coverage gaps, the policies that actually work, and how to build protection that matches your business.

The Three Core Coverages Every Artisan Contractor Needs

General Liability: Your First Line of Defense

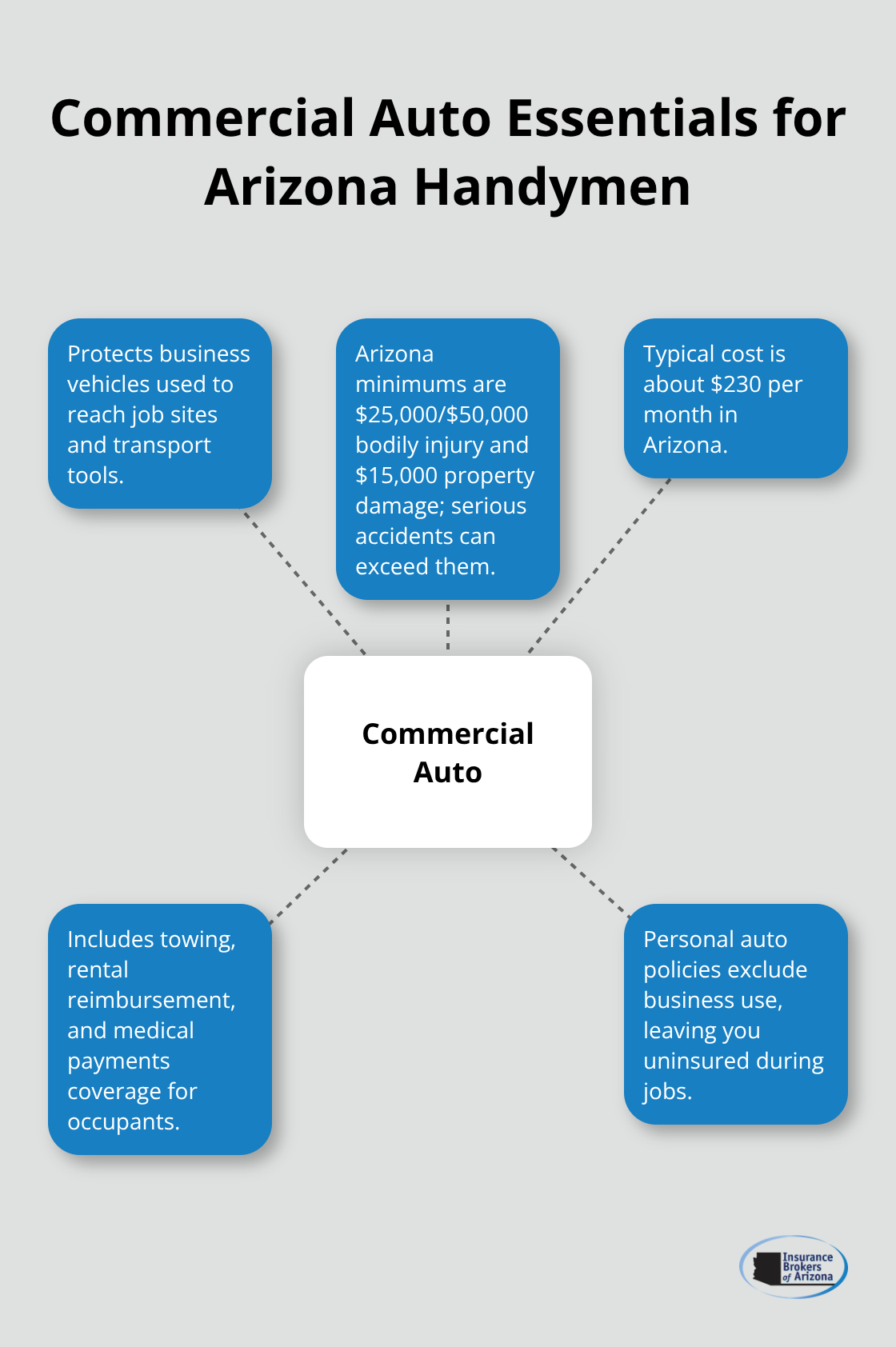

General liability forms the foundation of artisan contractor insurance and covers third-party bodily injury and property damage caused by your work. If you damage a client’s kitchen while installing custom cabinetry or a customer trips on your equipment and breaks an arm, general liability pays for medical expenses and legal costs. However, general liability has a significant blind spot: it does not protect your own tools and equipment. A $15,000 theft of power tools from your truck bed leaves you with zero recovery under a standard GL policy.

Inland Marine: Protecting Tools That Move

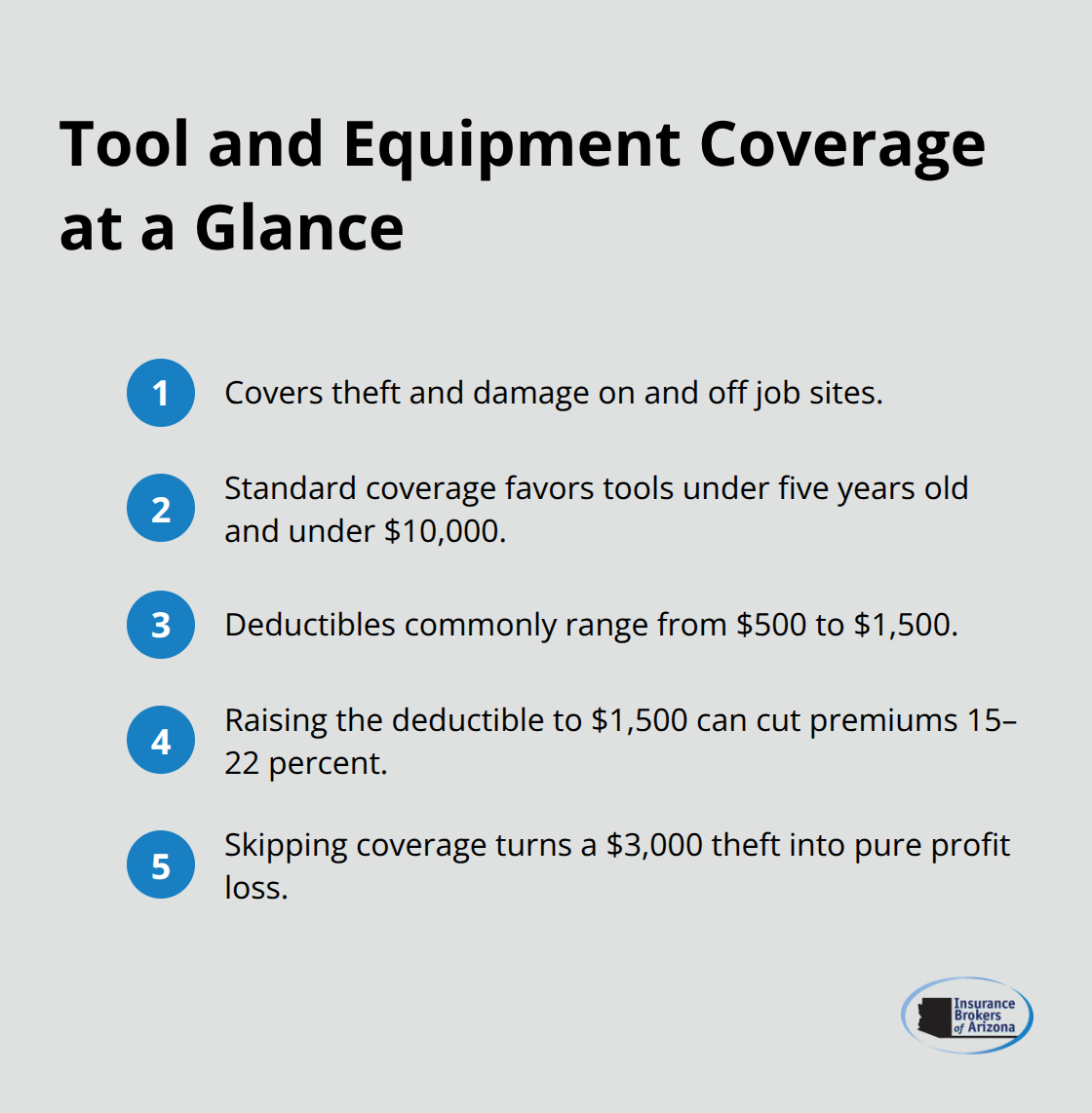

This coverage gap explains why inland marine insurance exists as a separate, non-negotiable layer. Inland marine covers mobile tools, equipment, and machinery in transit and at job sites, addressing tool theft which the Insurance Information Institute notes is a leading cause of costly project delays. For electricians, plumbers, roofers, and carpenters who move between customer locations constantly, inland marine is not optional.

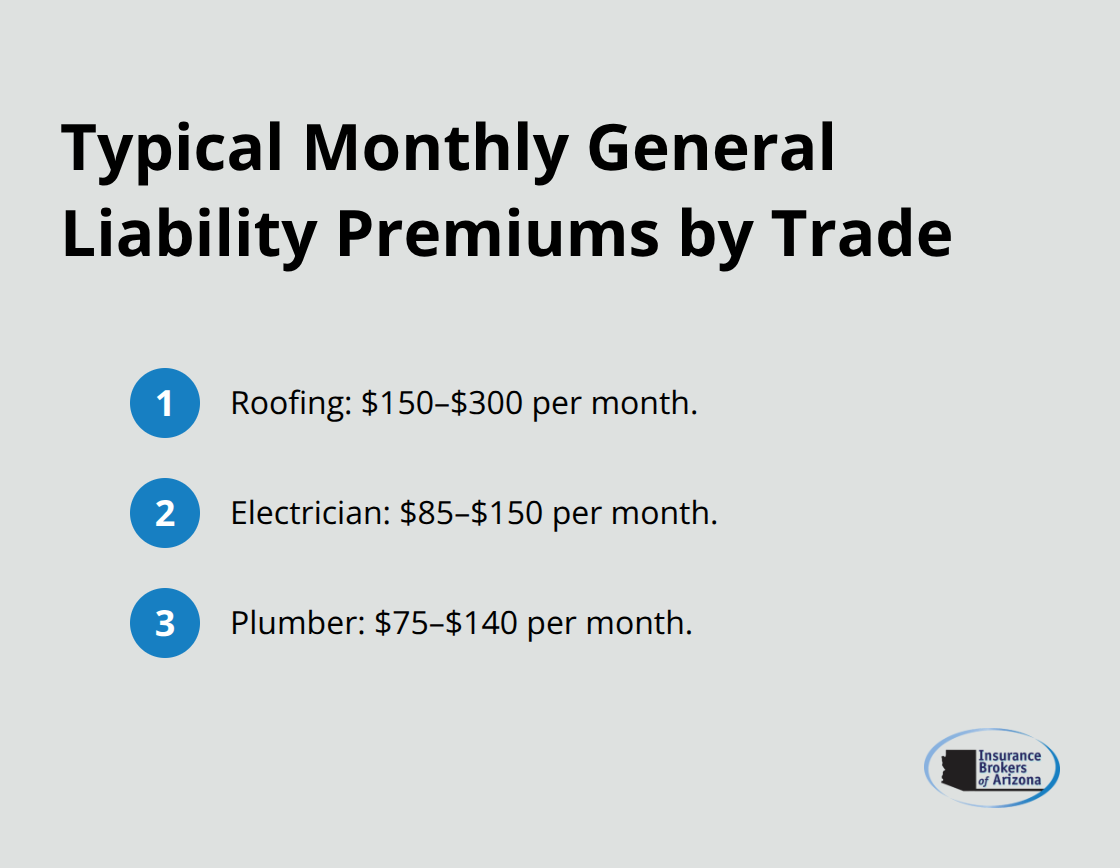

Premium costs vary significantly by trade. Roofing general liability runs $150–$300 per month, electrician GL averages $85–$150 per month, and plumber GL ranges $75–$140 per month with higher costs in flood-prone areas. These figures reflect the real risk profiles that carriers assess for each craft.

Workers Compensation: A Legal Requirement with Real Benefits

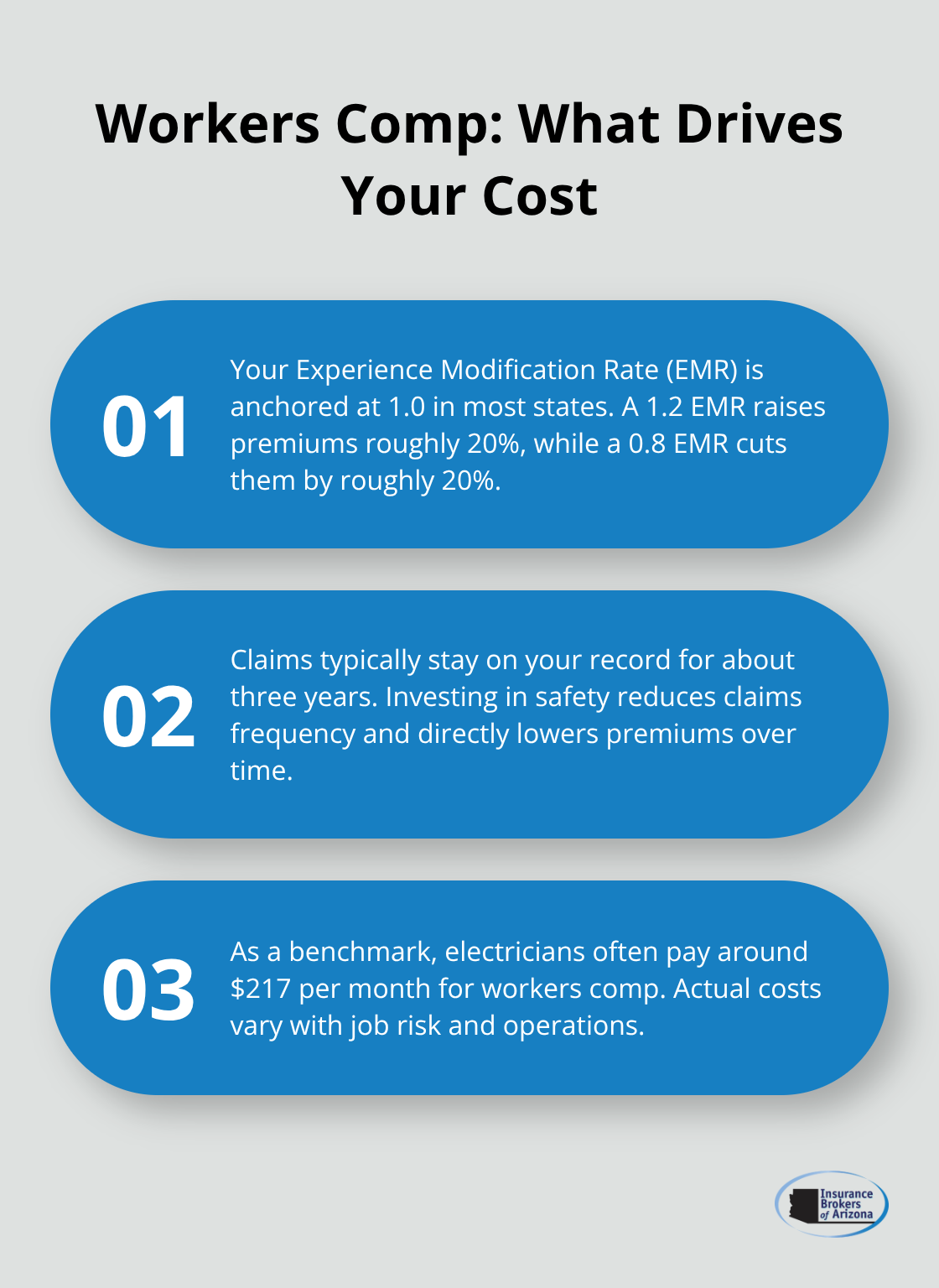

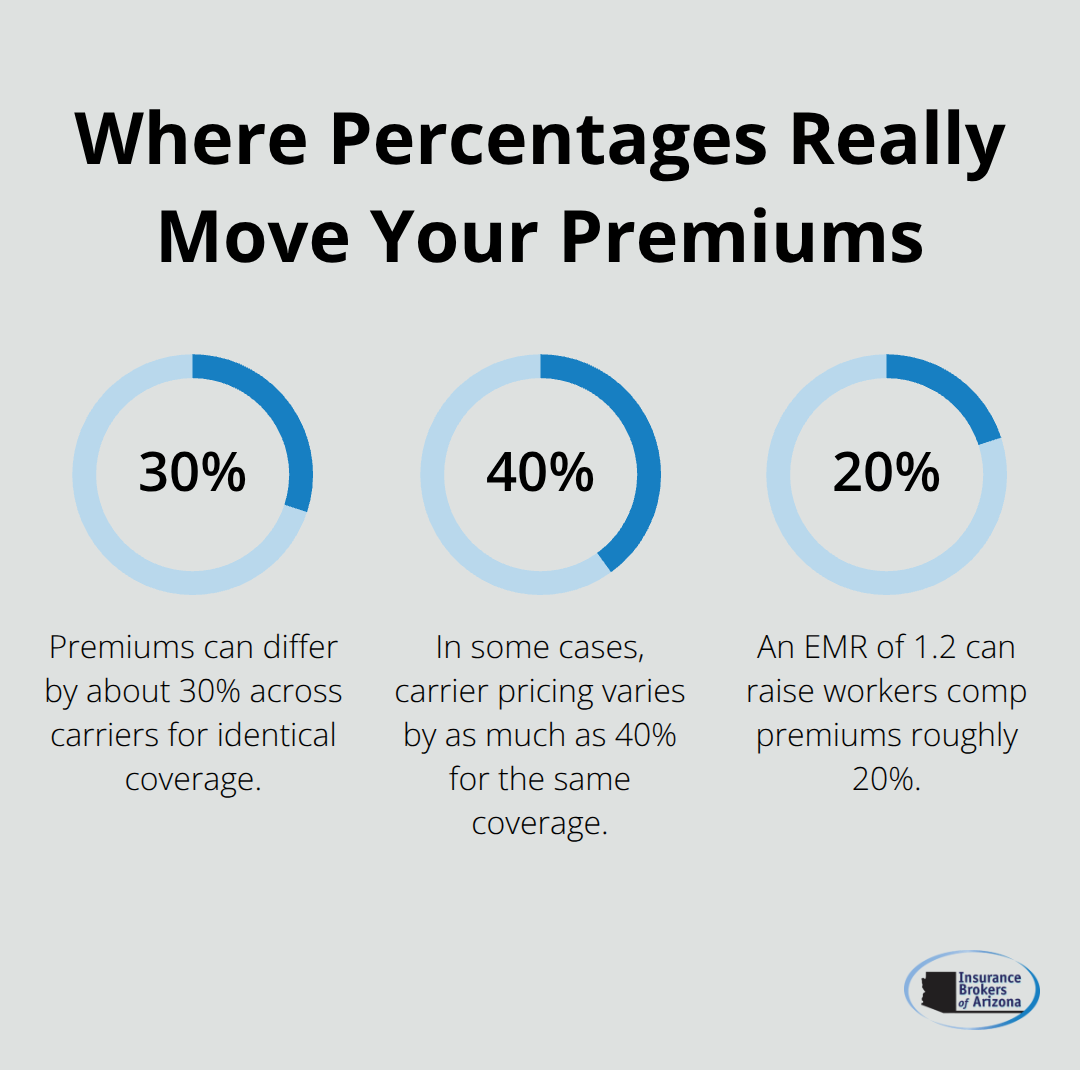

Workers compensation becomes legally required the moment you hire employees and covers medical expenses, lost wages, rehabilitation, and survivors’ benefits. Many artisan contractors delay hiring staff specifically to avoid workers comp costs, but this false economy backfires fast. Your Experience Modification Rate (EMR) directly controls your workers comp premiums; in most states, 1.0 is the baseline, a 1.2 rating increases premiums roughly 20%, and an 0.8 rating cuts them by roughly 20%. Claims remain on your record for approximately three years, making safety investments genuinely profitable. Electricians pay around $217 monthly for workers comp depending on risk factors.

Building Your Coverage Strategy

Obtain itemized quotes showing each coverage type with explicit limits and deductibles, and verify that certificates of insurance match your actual policies. Work with a broker who understands your specific trade, since generic brokers miss trade-specific exposures like electrical design versus installation work or welding performed by plumbers (which often require endorsements beyond template quotes). The right broker identifies gaps that standard packages overlook and positions you to move forward with confidence into the coverage gaps that threaten most artisan operations.

Common Coverage Gaps Artisan Contractors Face

The three core coverages we covered earlier form a solid foundation, but they leave dangerous gaps for artisan contractors working on high-value projects or managing complex job structures. A $15,000 general liability limit sounds reasonable until you face $50,000 in damage to a client’s custom home during a renovation. Standard policies also assume you work alone or with employees you directly control, which doesn’t reflect how most skilled trades operate in Arizona. Subcontractors, specialized techniques, and project complexity create exposures that generic policies simply ignore, and policy denials mid-project or after a claim costs far more than proper coverage upfront.

Limits That Don’t Match Project Value

Many artisan contractors purchase whatever coverage their equipment supplier recommends or their accountant suggests without analyzing their actual exposure. A roofing contractor with $250,000 annual revenue might carry $300,000 in general liability limits because that’s what a template policy includes, yet a single roof collapse claim can exceed $500,000 in damages and legal costs. The Insurance Information Institute emphasizes that liability limits should reflect your largest potential loss, not your comfort level with premium costs. Request itemized quotes that show limit options for $500,000, $1,000,000, and $2,000,000 in general liability, then honestly assess your biggest single project. If you install high-end electrical systems in commercial buildings or perform structural carpentry, $300,000 limits are dangerously low. Umbrella liability becomes more important as project size and risk grow, especially with rising verdicts in construction disputes, but you must pair it with strong primary coverage first.

Subcontractor Liability and Who Really Pays

When you hire subcontractors, your general liability policy does not automatically cover their negligent acts. If your subcontractor electrician causes a fire that damages the client’s property, your GL policy often excludes that claim because the subcontractor caused it. Owners and Contractors Protective liability coverage addresses this gap by protecting you against liability from subcontractors’ negligent acts, typically with the property owner or general contractor as the named insured. Many artisan contractors skip this coverage because they believe their subs carry their own insurance, yet client contracts often require that you, the primary contractor, hold coverage for all work performed on site. Verify that your liability coverage extends to subcontractors’ negligent acts and that any required coverage aligns with your client’s insurance requirements before you sign the job.

Custom Work Requires Custom Coverage

Specialized techniques like welding, electrical design, or custom fabrication introduce risks that standard policies don’t address. A plumber who performs welding work on a job site likely needs a welding endorsement on their general liability policy because the base policy excludes fire risk from welding operations. Electrical contractors who design custom systems rather than just install them may need professional liability coverage to protect against design errors that cause equipment failures or safety hazards. Read your policy language carefully to identify hidden exclusions for your specific work, and confirm that endorsements address multi-trade overlaps or specialized techniques you regularly perform. The difference between a claim denial and a covered loss often comes down to whether you purchased the right endorsement months before the incident occurred.

These coverage gaps expose you to financial risk that extends far beyond what standard policies address. The next section shows you how to evaluate your specific trade and select policies that actually protect your business and your craft.

How to Choose the Right Artisan Contractor Insurance Policy

Document Your Exact Work Activities

Start by writing down exactly what you do on job sites. Most artisan contractors skip this step and end up with generic policies that exclude their most common work. If you’re an electrician, distinguish between installation work and design consultation-design work requires professional liability coverage that standard GL policies don’t provide. If you’re a plumber who occasionally welds copper lines, that welding activity needs a specific endorsement or your claim gets denied when something goes wrong. If you work at heights regularly, fall protection and height-work endorsements matter.

Write down your three largest projects from the past year, the dollar values involved, the types of work performed, and any subcontractors you hired. This document becomes your briefing sheet when you request quotes from carriers.

Shop Multiple Carriers and Request Itemized Quotes

Premium differences across carriers for identical coverage can range from 30 to 40 percent due to broker relationships and trade specialization. Shopping around isn’t optional-it’s how you avoid overpaying by thousands annually.

Request itemized quotes from at least three carriers, and require that each quote breaks down general liability, workers compensation, inland marine, and any specialty endorsements with explicit limits and deductibles shown separately.

A quote that shows only a total premium hides whether you’re getting $500,000 or $1,000,000 in liability limits, and that difference could determine whether a claim gets paid. Ask each carrier detailed questions about your exact work, and listen for whether they push back or ask clarifying questions about your operations. A broker who understands construction trades will ask about the height of your work, whether you use subcontractors regularly, what your largest single project value is, and what tools you carry. A generic broker will quote you based on a template and move on.

Optimize Deductibles Across Your Coverage Package

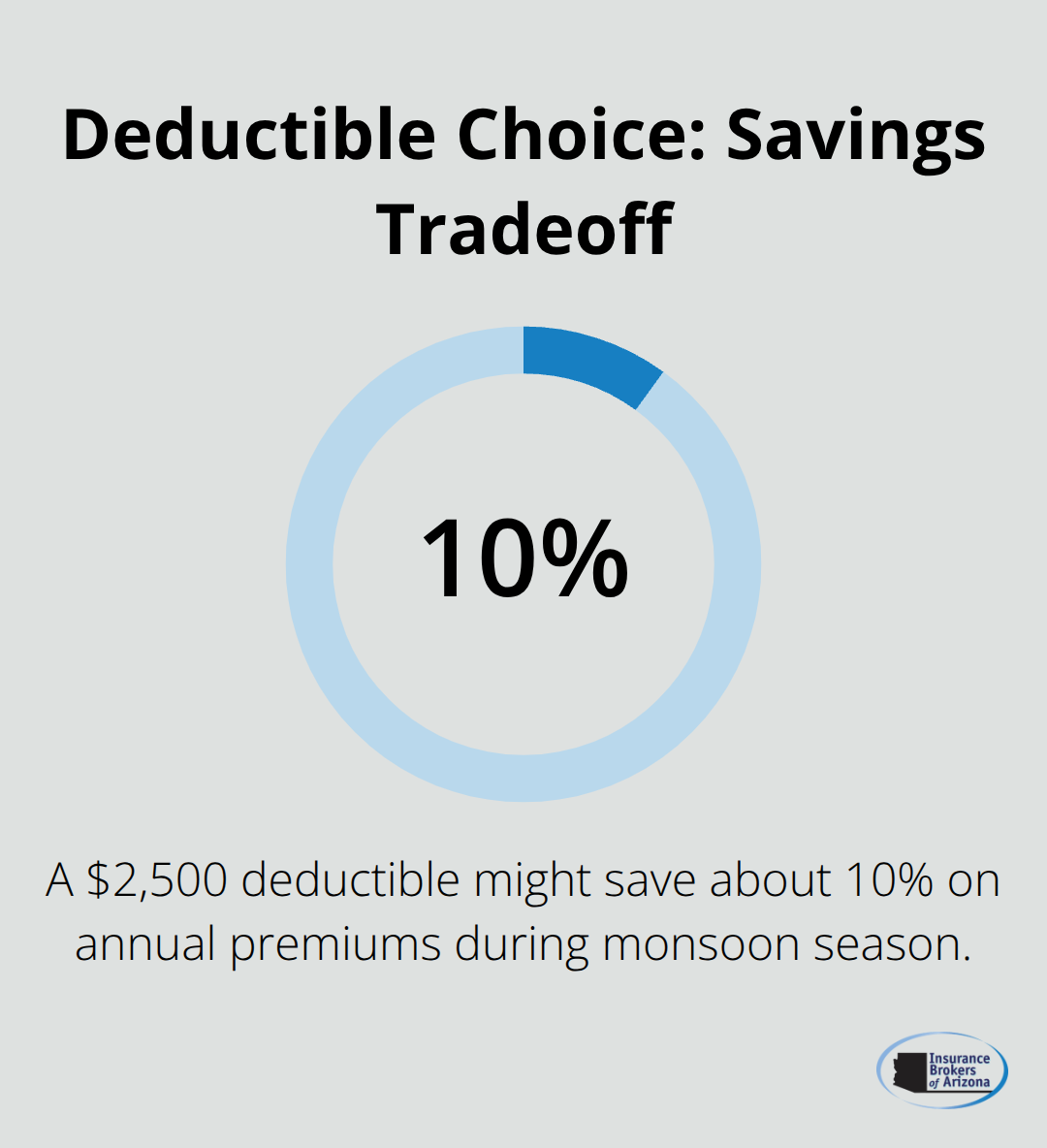

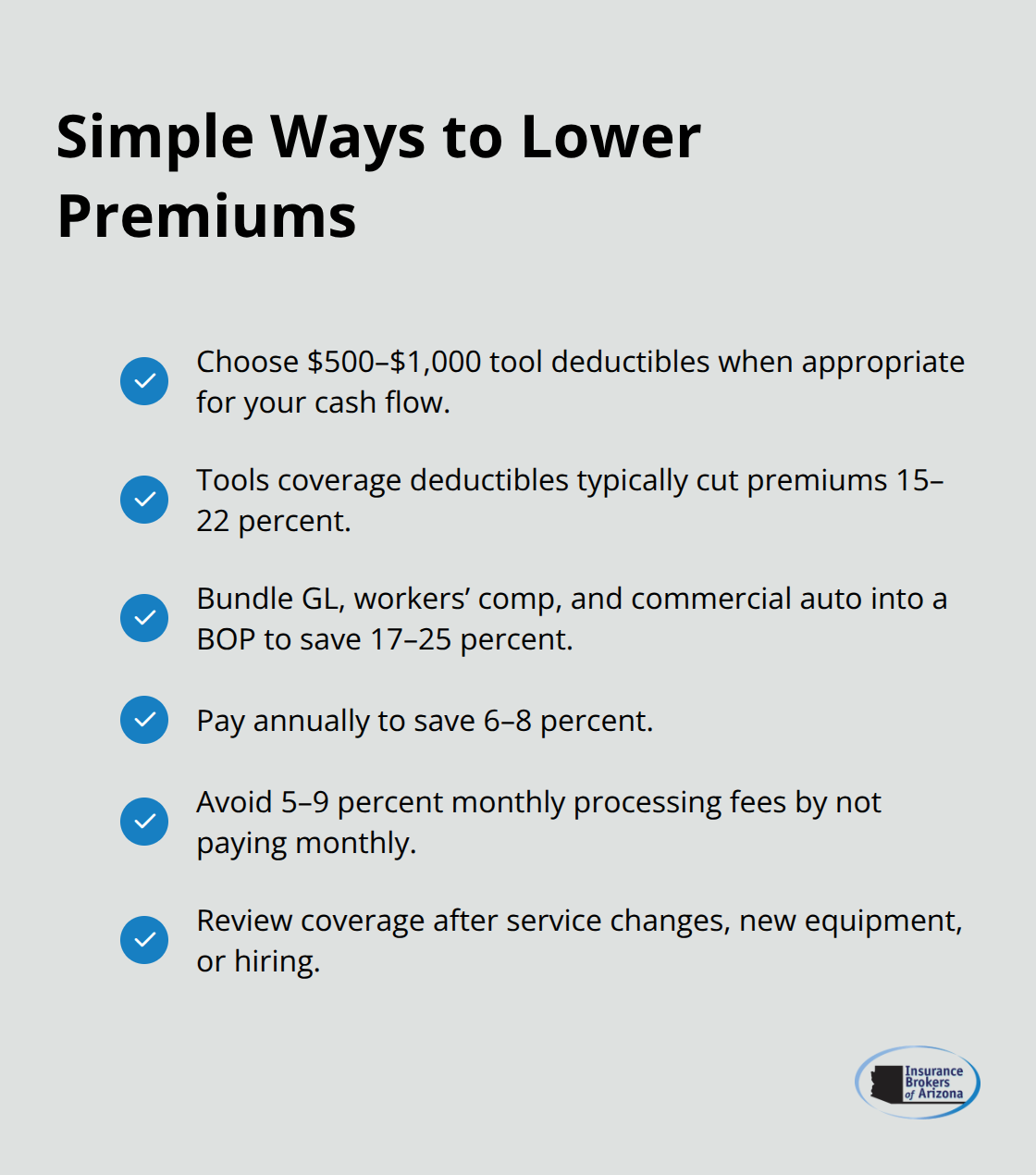

Raising deductibles cuts premiums, but the wrong deductible choices leave you exposed when claims happen. A $2,500 deductible on general liability saves maybe $300 annually compared to a $1,000 deductible, but when a customer’s property damage claim lands at $8,000, you absorb that $2,500 out of pocket before insurance kicks in.

The smarter approach involves deductible optimization across your entire package: raise the deductible on coverage you rarely claim (like commercial property damage if you work mostly in client spaces) while keeping lower deductibles on coverages where claims are more likely (general liability and workers comp). This strategy reduces total cost without sacrificing protection where it matters most. Align your deductibles across policies too-mismatched deductibles create confusion at claim time and sometimes result in coverage gaps.

Verify Coverage Territory and Read Policy Language Carefully

Arizona contractors working across state lines or in specific regions need policies that cover their actual service territory. Read the policy language section on coverage territory, because some policies limit coverage to Arizona only while others extend to neighboring states. If you travel to California for projects, a policy that excludes California leaves you uninsured on those jobs.

Check whether your policy covers work on residential properties, commercial buildings, or both, since some carriers restrict one or the other. Hidden exclusions bury themselves in the fine print, so search specifically for exclusions related to your trade. Electrical contractors should confirm their policy doesn’t exclude design work, welding, or work on certain building types. Once you select a carrier, request a certificate of insurance and verify it matches your actual coverage limits and policy dates before you start work.

Final Thoughts

Proper artisan contractor insurance coverage protects both your craft and your business from the financial devastation that follows a single claim. Without the right policies in place, a tool theft, a customer injury, or a subcontractor’s mistake can wipe out years of profit and force you to shut down operations. The three core coverages-general liability, inland marine, and workers compensation-form the foundation, but your specific trade demands additional layers like professional liability endorsements, umbrella coverage, or specialized equipment protection.

Getting comprehensive coverage starts with honest documentation of your work. Write down what you actually do on job sites, your largest projects, and the risks unique to your trade, then request itemized quotes from multiple carriers that break down each coverage type with explicit limits and deductibles. Premium differences of 30 to 40 percent between carriers mean shopping around saves thousands annually, and a broker who understands construction trades will ask the right questions about your operations instead of quoting you from a template.

We at Insurance Brokers of Arizona® work with artisan contractors across Arizona to build insurance packages that match your specific trade and project complexity. Contact us today to schedule a comprehensive review of your current coverage and identify the gaps that could cost you thousands.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.