Handyman Insurance Arizona: Coverage That Keeps You Building

Running a handyman business in Arizona means managing real risks every single day. One accident on a job site or a client injury can wipe out your savings and shut down your operation.

That’s why handyman insurance in Arizona isn’t optional-it’s the foundation of a sustainable business. We at Insurance Brokers of Arizona® help handymen like you find the right coverage so you can focus on what you do best.

Why Handymen Need Insurance in Arizona

One client injury on your job site can trigger a lawsuit that costs $50,000 to $500,000 in legal fees and settlements alone, even if you believe the accident wasn’t your fault. Arizona courts don’t care about your intentions-they care about whether you had insurance to cover the damage. Without general liability coverage, a single incident drains your business bank account and forces you to shut down operations. The Arizona Registrar of Contractors requires general liability insurance with minimum coverage of $1 million per occurrence and $2 million aggregate before you can apply for most contractor licenses. This isn’t bureaucratic overkill; it’s a financial safety net that separates surviving handymen from those who lose everything to one bad day.

Your Tools Are Your Livelihood

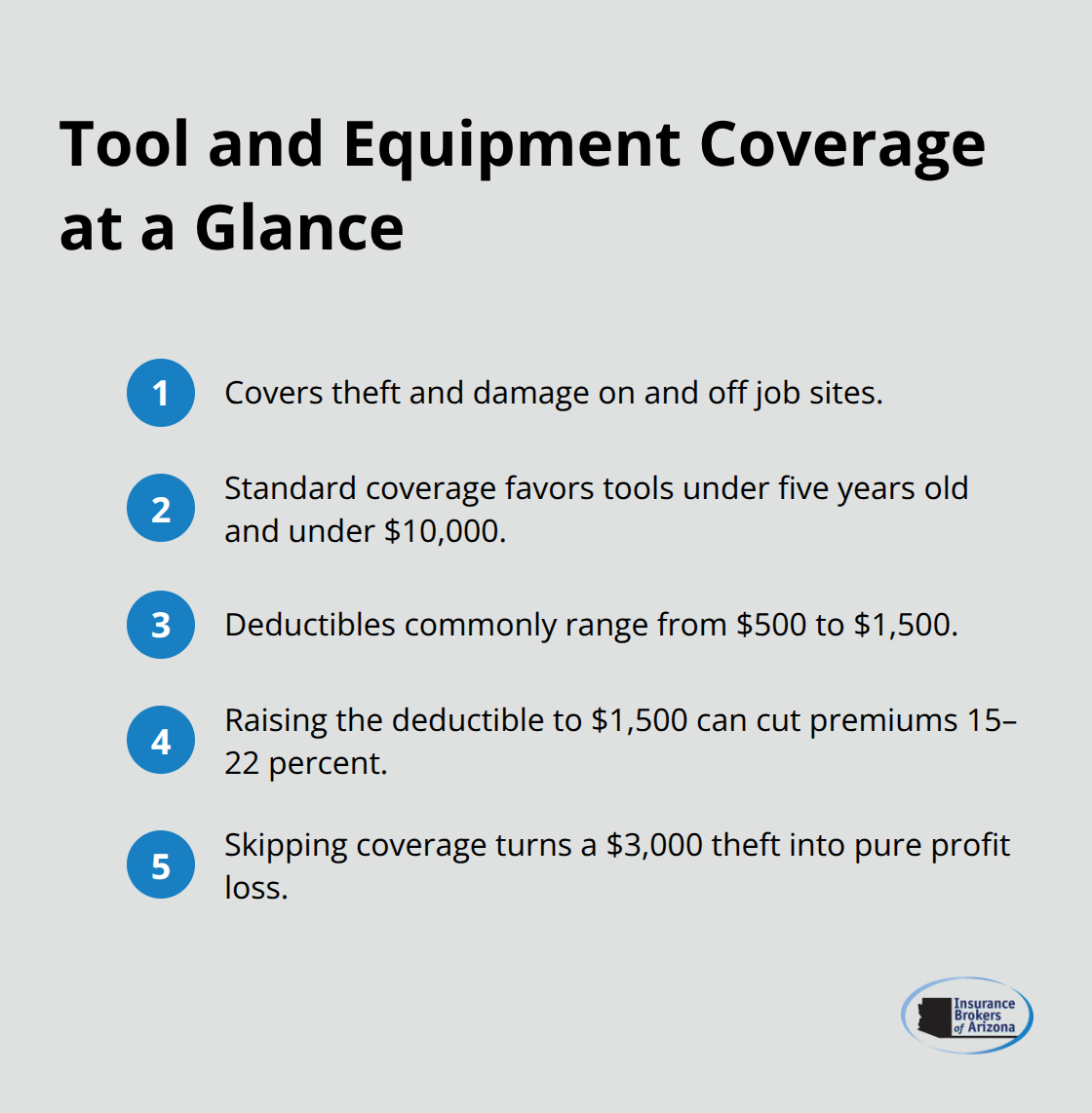

Handymen in Arizona lose thousands of dollars annually to theft and damage at job sites. Tools and equipment insurance covers repair or replacement costs when your drill, saw, or compressor disappears from a residential renovation or gets damaged during transport. Standard coverage focuses on tools under five years old valued under $10,000, with deductibles ranging from $500 to $1,500. Increasing your deductible to $1,500 cuts your premium by 15 to 22 percent, so if you maintain strong jobsite security, this strategy works well. Most handymen skip this coverage and absorb losses personally, which means a stolen $3,000 tool kit becomes pure profit loss that directly reduces your year-end income.

Arizona’s Licensing Reality Demands Coverage

Projects exceeding $1,000 in Arizona require a contractor license from the Registrar of Contractors, and unlicensed contracting in Phoenix carries penalties up to six months in jail, $1,000 minimum fine, and a one-year license ban for first offenses. Obtaining a license means providing proof of general liability insurance to the ROC and maintaining active coverage throughout your license period. The licensing process takes roughly 60 days, with about 20 days for administrative review and 40 days for substantive evaluation of your qualifications. You’ll need to pass the Arizona Statutes and Rules exam plus a trade-specific exam, obtain a contractor bond as low as $5 per month (depending on your credit), and budget $720 to $1,050 in licensing fees depending on your classification. Many handymen think licensing is optional for small jobs, but one client complaint to the city triggers an investigation, and operating without proper licensing when required destroys your reputation and exposes you to serious penalties.

What Happens When You Skip Coverage

One accident without insurance doesn’t just cost money-it ends your business. A client who slips on your ladder, a homeowner whose wall you damage, or a neighbor injured by falling debris can all file claims that exceed $100,000. Your personal assets become fair game in court, and creditors can pursue your home, vehicles, and savings. Arizona handymen who operate without coverage often find themselves unable to bid on jobs over $1,000, unable to satisfy client requirements (many clients demand at least $1 million in liability coverage before hiring), and unable to recover from a single mistake. The next chapter covers the specific types of coverage that protect you from these scenarios and fit your actual business operations.

Types of Handyman Insurance Coverage Available

General Liability Insurance Protects Your Core Business

General liability insurance protects your business when a client or third party sues you for bodily injury or property damage caused by your work. Arizona courts award settlements ranging from $50,000 to $500,000 or higher, and general liability covers your legal defense costs plus judgment amounts up to your policy limit. Most Arizona handymen operate with $1 million per occurrence and $2 million aggregate coverage, which matches the Registrar of Contractors requirement for contractor licensing. This coverage costs about $72 per month in Arizona according to current market data, making it the most affordable protection you can buy.

The real value emerges when a client slips on your ladder or you accidentally damage a homeowner’s wall-your insurer handles the lawsuit instead of your personal bank account. If you operate on leased job sites or bid on projects over $5,000, clients routinely demand proof of $1 million coverage before signing contracts, so this policy becomes non-negotiable for landing larger jobs.

Workers’ Compensation Covers Your Team

Workers’ compensation insurance in Arizona is required if you have employees on payroll, and it pays medical costs plus lost wages when an employee gets injured on the job. This coverage averages $54 per month in Arizona and protects you from lawsuits filed by injured workers, since workers’ comp replaces the employee’s right to sue. The requirement exists because Arizona law mandates coverage for any business with employees, and operating without it exposes you to significant penalties and personal liability.

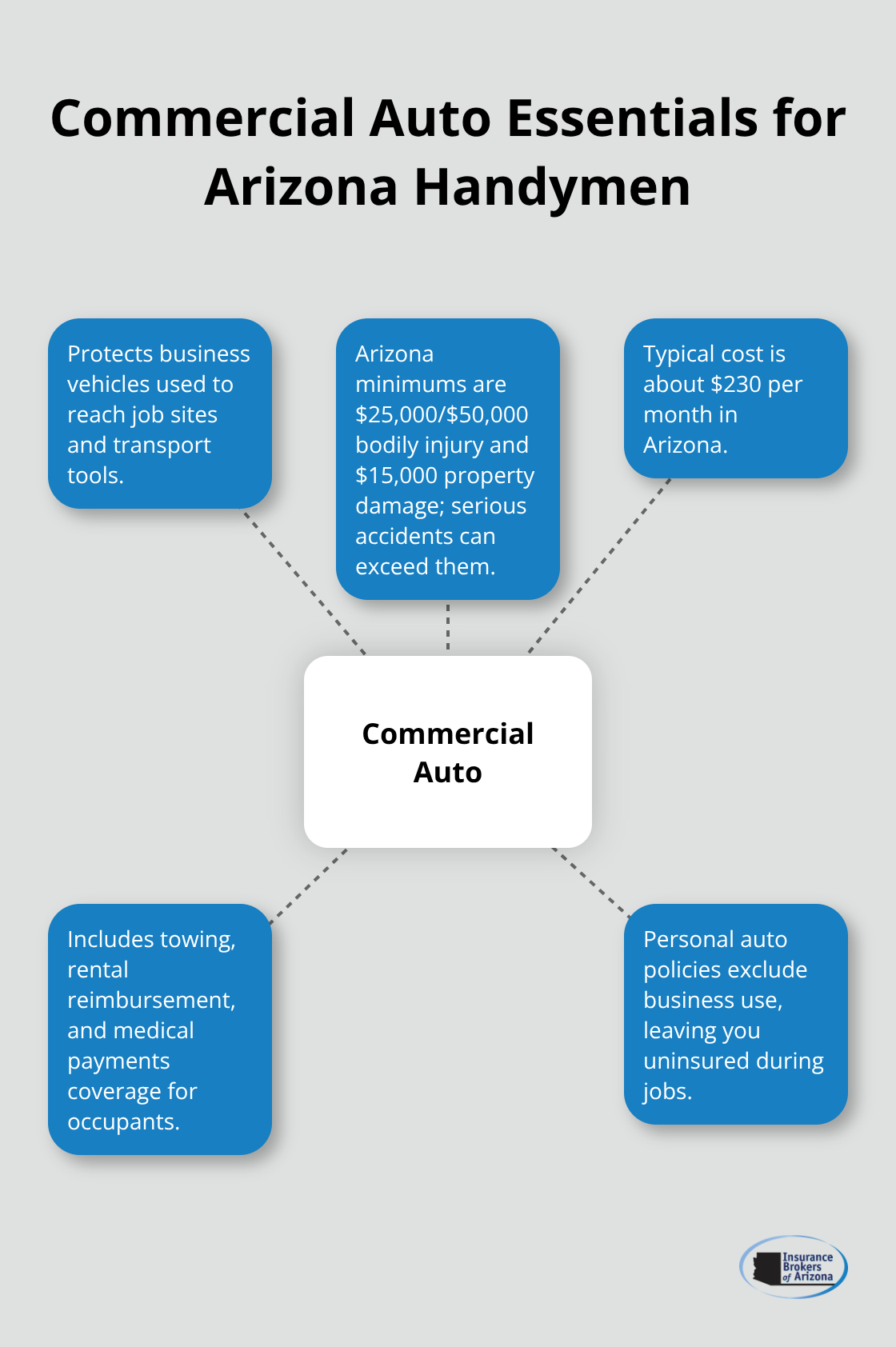

Commercial Auto Insurance Protects Your Work Vehicles

Commercial auto insurance covers your pickup truck or box truck used to transport tools and reach job sites, protecting you against third-party injury claims and property damage when you cause an accident. Arizona’s minimum liability requirements are $25,000 per person and $50,000 per accident for bodily injury, plus $15,000 for property damage, but this floor-level coverage leaves you dangerously exposed-a single serious accident easily exceeds these limits. Commercial auto costs roughly $230 per month in Arizona and covers towing, rental reimbursement, and medical expenses for occupants in your vehicle.

Many handymen assume their personal auto policy covers business use, but standard personal policies explicitly exclude business vehicle use, leaving you uninsured if an accident occurs during a job. This gap in coverage can destroy your finances faster than almost any other liability scenario.

Bundling Policies Saves Money and Simplifies Management

Combining general liability with commercial property coverage into a Business Owner’s Policy (BOP) reduces your monthly costs to roughly $363 nationwide, saving you money compared to purchasing policies separately. The combination of general liability, workers’ compensation if you have employees, and commercial auto insurance creates a foundation that satisfies licensing requirements, meets client demands, and protects your assets from the most common lawsuit scenarios handymen face in Arizona. Understanding which coverage types match your specific services-whether you handle minor repairs, electrical work, plumbing, or structural projects-determines how much protection you actually need and what you’ll pay for it.

How to Choose the Right Handyman Insurance Policy

Assess Your Specific Business Needs

Start with a complete list of every service you actually perform, not services you might offer someday. A handyman who handles minor drywall repair, cabinet installation, and painting faces different risk exposure than one who does electrical work or structural modifications. Each service tier demands different coverage limits and specialty endorsements. If you advertise tile installation but skip professional liability coverage, you’re gambling that no client will sue you for a cracked backsplash or uneven grout lines. Electrical and plumbing work command higher premiums because mistakes cause serious injuries or property damage. Minor repairs like furniture assembly or shelving installation cost far less to insure.

Write down your revenue estimate for the next 12 months, your current employee count, and whether you plan to hire workers. This information directly determines your workers’ compensation cost and your general liability premium. A solo operator with $80,000 annual revenue pays less than a crew leader managing three employees with $400,000 revenue.

Identify What Your Clients Actually Demand

Many residential clients require $1 million in general liability coverage before they’ll sign a contract, while commercial property managers often demand $2 million per occurrence with completed operations coverage extending two years after project completion. If you’re bidding on jobs over $50,000, expect clients to require proof of insurance before work starts and to list them as additional insured on your policy. This requirement costs nothing to add but refusing it costs you the job.

Compare Quotes from Multiple Carriers

Shopping quotes from at least three carriers reveals massive premium differences for identical coverage. One carrier might quote $72 monthly for general liability while another charges $95 for the same $1 million per occurrence limit, purely because of how they assess risk in Arizona. Insureon and NEXT Insurance both operate in Arizona and offer online quotes within minutes, though local brokers who work with 40-plus carriers often uncover better rates than online quote engines.

When comparing quotes, ensure each one includes the same coverage limits, deductibles, and endorsements so you’re comparing apples to apples. A $72 monthly premium for general liability looks attractive until you realize it comes with a $2,500 deductible while another quote at $85 includes a $500 deductible.

Review Coverage Limits and Deductibles

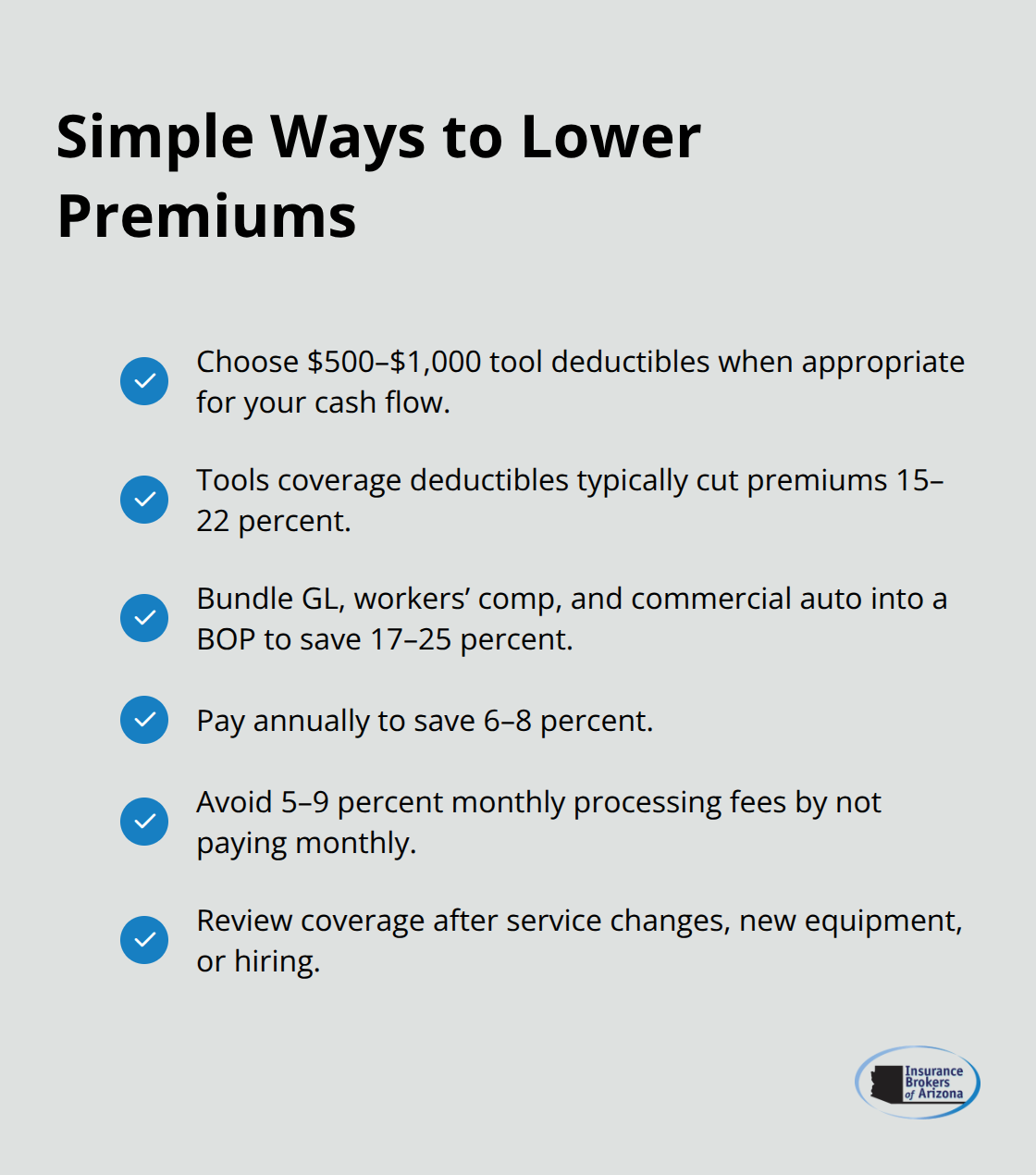

Higher deductibles absolutely reduce premiums, but only increase them if you maintain strong jobsite security and can afford to cover the deductible from operating cash. Most handymen benefit from $500 to $1,000 deductibles on tools and equipment coverage, which typically cuts premiums 15 to 22 percent.

Bundling general liability, workers’ compensation, and commercial auto into a Business Owner’s Policy saves 17 to 25 percent compared to purchasing policies separately. Annual payment rather than monthly installments typically saves 6 to 8 percent while avoiding 5 to 9 percent monthly processing fees. Review your coverage annually or whenever you add new services, invest in expensive equipment, or expand your employee count, since outdated policies leave gaps in protection.

Final Thoughts

Handyman insurance in Arizona protects your business from the financial devastation that follows a single accident or client injury. General liability coverage satisfies licensing requirements, meets client demands, and shields your personal assets when lawsuits arrive. Workers’ compensation protects your employees and keeps your license active, while commercial auto insurance covers your work vehicles and the tools you transport between jobs. Together, these policies cost roughly $356 per month and represent the difference between a sustainable business and financial ruin.

The real protection emerges when you stop treating insurance as an expense and start viewing it as the foundation that allows you to bid on larger projects, satisfy client requirements, and recover from mistakes without losing everything. A $1 million general liability policy costs about $72 monthly but saves you from a $100,000 lawsuit that would otherwise drain your business bank account. Bundling policies into a Business Owner’s Policy saves 17 to 25 percent compared to buying coverage separately, and paying annually rather than monthly secures 6 to 8 percent discounts while avoiding processing fees.

Gather your business details-the specific services you offer, your projected annual revenue, your current employee count, and any equipment or vehicles you own-then shop quotes from at least three carriers to reveal premium differences that often exceed $50 monthly for identical coverage. Insurance Brokers of Arizona® works with over 40 carriers to find handyman insurance Arizona that fits your budget and protects your operation. Contact us today for a personalized quote.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.