How to Get General Liability Insurance for Handymen

At Insurance Brokers of Arizona®, we understand the unique challenges handymen face in their line of work.

General liability insurance for handymen is a critical safeguard against potential financial risks.

This comprehensive guide will walk you through the process of obtaining the right coverage for your handyman business, ensuring you’re protected while you focus on your craft.

What Is General Liability Insurance for Handymen?

The Essence of General Liability Coverage

General liability insurance provides essential protection for handymen against financial losses from accidents, property damage, or legal claims. This coverage typically includes bodily injury, property damage, and personal injury claims. For instance, if you accidentally break a client’s expensive vase, your policy will cover the replacement cost. If a client trips over your toolbox and sustains an injury, your insurance will pay for their medical expenses.

Unique Risks in the Handyman Profession

Handymen face specific risks daily. You work in other people’s homes and businesses, often using tools and equipment that could cause damage or injury if misused. Without proper insurance, a single accident could potentially bankrupt your business. Here are some common scenarios:

- Property damage: You might accidentally drill through a water pipe, causing extensive water damage to a client’s home.

- Bodily injury: A client could slip on a wet floor you’ve just mopped, resulting in a serious injury.

- Personal injury: You might face accusations of slander if you inadvertently make a negative comment about a competitor to a client.

The Cost of Protection

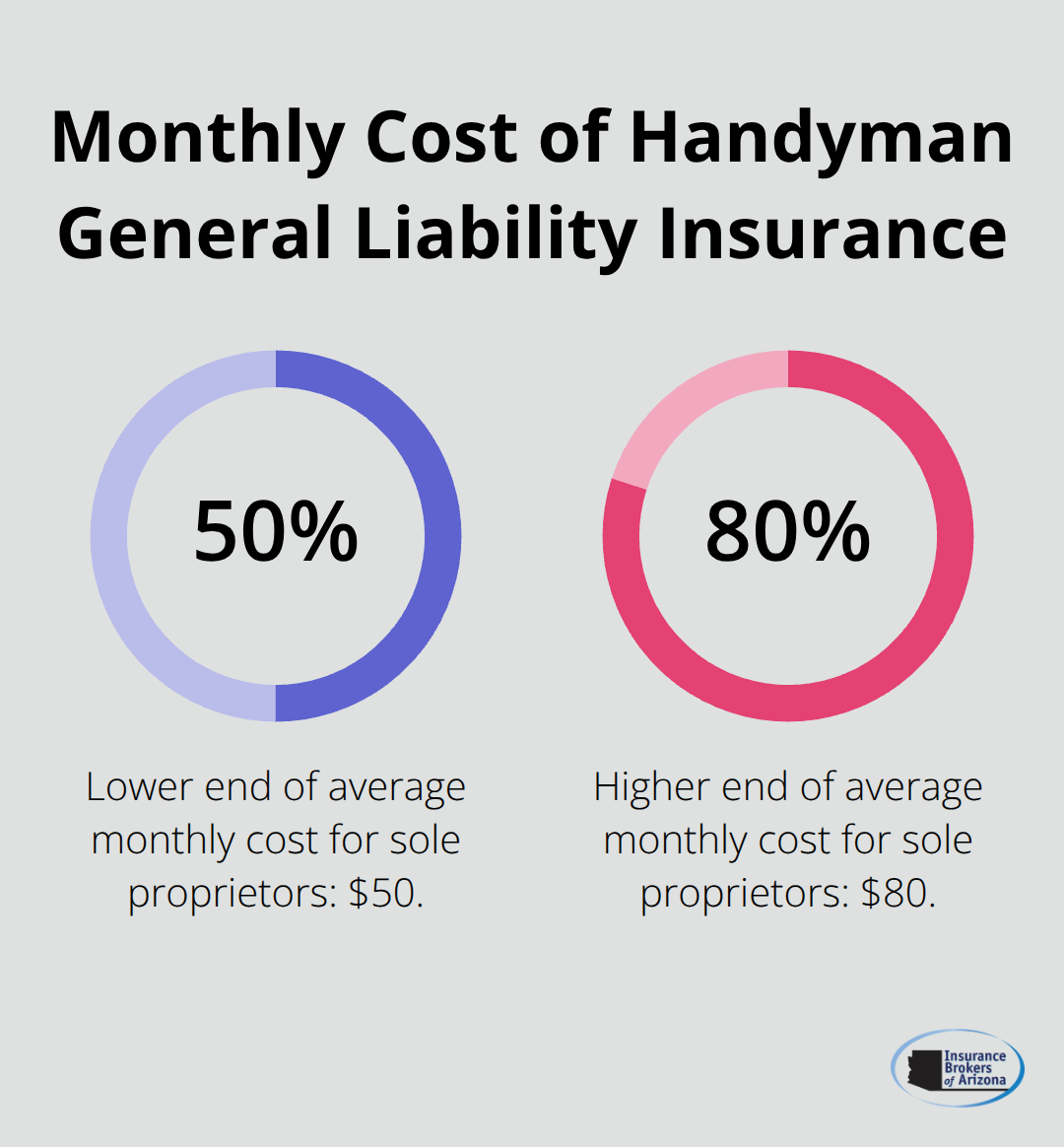

Industry data shows that the average cost for handyman general liability insurance ranges from $50 to $80 per month for sole proprietors. This amount represents a small investment for the peace of mind and financial protection it provides (considering the potential costs of lawsuits or damage claims).

Business Benefits of Insurance Coverage

Many clients now require proof of insurance before hiring handymen. Having general liability insurance not only protects you financially but also demonstrates professionalism and readiness to potential clients. It can become a key factor in winning contracts and growing your business.

Handymen with proper insurance coverage often have an advantage over their uninsured competitors. Clients view them as more reliable and responsible, which can lead to more referrals and repeat business. This professional edge (combined with the financial protection) makes general liability insurance an invaluable asset for any handyman business.

As we move forward, let’s examine the key components that make up a comprehensive general liability policy for handymen.

What Does a Handyman’s General Liability Policy Cover?

Property Damage Protection

A handyman’s work involves daily interaction with clients’ property. Accidents can occur, and property damage coverage provides essential protection. If you accidentally cause harm to a client’s belongings or premises, this coverage steps in. For instance, if a ceiling fan you’re installing falls and damages an expensive hardwood floor, your insurance will cover the repair costs. This protection extends to various scenarios (from minor mishaps to major accidents), ensuring you don’t pay out of pocket for costly repairs or replacements.

Bodily Injury Safeguard

Safety is a top priority in any handyman job, but injuries can still occur despite precautions. Bodily injury protection covers medical expenses and potential legal costs if a client or third party suffers an injury due to your work. Consider a scenario where a client trips over your extension cord and breaks their arm. Your policy would cover their medical bills and any legal fees if they decide to sue. This coverage is essential, as medical costs can quickly escalate (potentially bankrupting an uninsured handyman).

Personal and Advertising Injury Coverage

In the digital age, your online presence and reputation matter as much as your physical work. Personal and advertising injury coverage protects you from claims related to libel, slander, copyright infringement, and invasion of privacy. For example, if you unknowingly use a copyrighted image in your advertising materials or make a statement about a competitor that they consider defamatory, this coverage will help defend you against legal action. It’s a vital component in an era where a single social media post can lead to significant legal troubles.

Products-Completed Operations Protection

Your liability doesn’t end when you finish a job. Products-completed operations coverage protects you from claims arising from work you’ve already completed. Imagine you install a water heater, and months later, it malfunctions, causing water damage to the client’s home. This coverage would protect you from the resulting claim. It’s particularly important for handymen who often work on projects that can have long-term implications if something goes wrong.

Understanding these components is essential when selecting your policy. Insurance Brokers of Arizona® works closely with handymen to ensure their policies are tailored to their specific needs, providing comprehensive protection without unnecessary extras. Now that we’ve explored what a general liability policy covers, let’s move on to the steps you need to take to obtain this vital insurance for your handyman business.

How to Secure General Liability Insurance for Your Handyman Business

Evaluate Your Business Risks

Take a close look at your handyman operations. Consider the types of jobs you perform, whether you work in residential or commercial settings, and if you have employees. Understanding your specific risks will help determine the right coverage limits. For example, if you frequently work with expensive home fixtures, you might need higher property damage limits.

Gather Essential Information

Before you apply for insurance, collect key details about your business:

- Your business name and structure (sole proprietorship, LLC, etc.)

- Years in business

- Annual revenue

- Number of employees (if any)

- Types of services offered

- Any past claims or incidents

Having this information ready will speed up the application process and ensure accurate quotes.

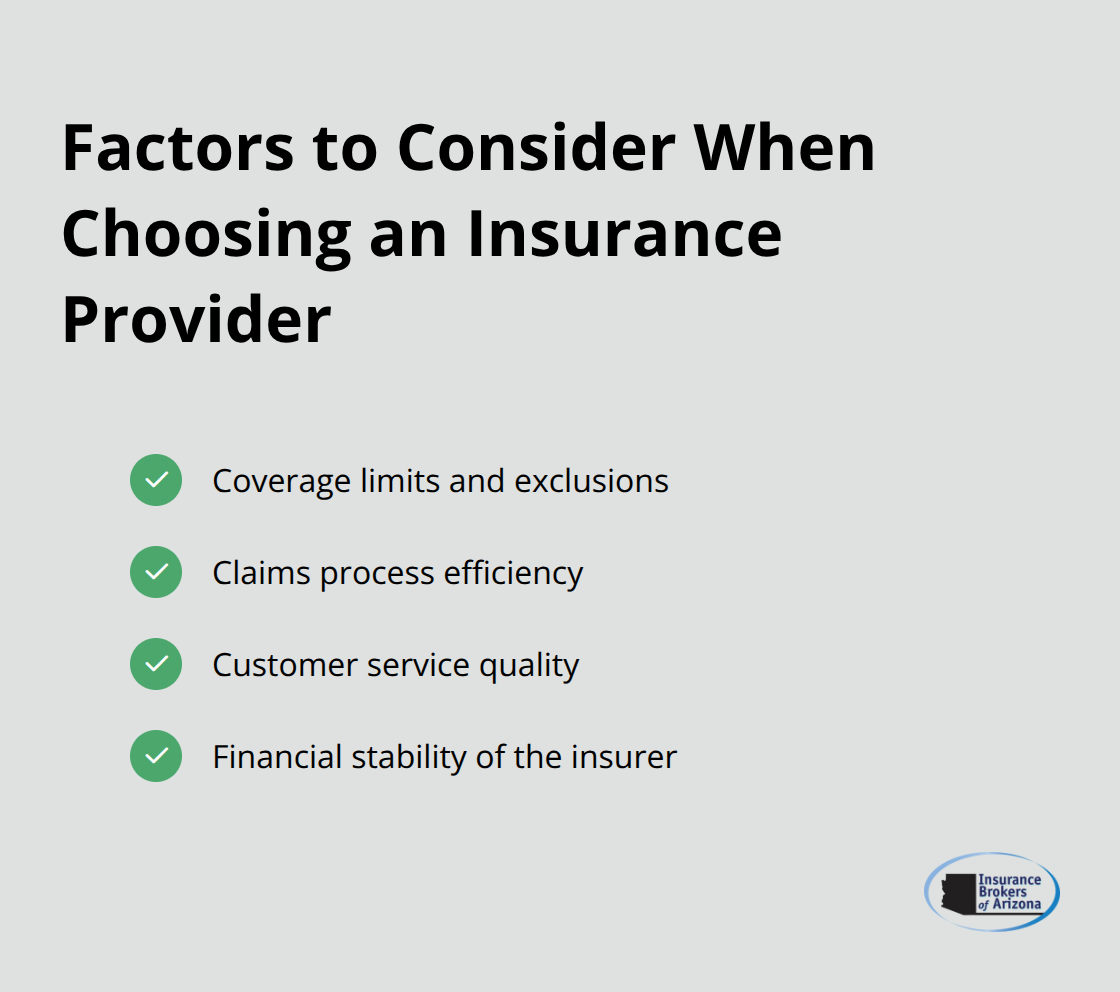

Choose the Right Insurance Provider

Many insurance companies offer general liability coverage, but not all specialize in handyman insurance. Look for providers with experience in your industry. When comparing providers, consider factors beyond price:

- Coverage limits and exclusions

- Claims process efficiency

- Customer service quality

- Financial stability of the insurer

The cheapest option isn’t always the best. You want an insurer that will be there when you need them most.

Apply and Review Your Policy

Once you’ve chosen a provider, complete the application process. This usually involves filling out an online form or speaking with an agent. Be honest and thorough in your responses to ensure you get the right coverage.

After submitting your application, you’ll receive a quote. Take time to review it carefully. Pay attention to:

- Coverage limits

- Deductibles

- Exclusions

- Additional coverages included or available

If anything is unclear, ask questions. A reputable insurer will explain your policy in detail.

Finalize and Maintain Your Coverage

Once you’re satisfied with the policy terms, finalize your coverage. You’ll typically need to make a down payment or pay the full premium to activate your policy.

After securing your coverage, keep your policy up to date. Inform your insurer of any changes in your business (such as new services offered or increased revenue). This ensures your coverage remains adequate as your business grows.

Final Thoughts

General liability insurance for handymen provides essential protection against financial risks from accidents, property damage, and legal claims. This coverage enhances credibility with clients and often gives an edge over uninsured competitors. Many clients now require proof of insurance before hiring, making it a necessity for securing contracts.

The process to obtain general liability insurance requires careful consideration of specific needs and reputable providers. We at Insurance Brokers of Arizona® specialize in tailoring coverage to meet the unique needs of handymen in Arizona (ensuring comprehensive protection at competitive rates). Our team guides handymen through every step of securing the right insurance for their business.

Insurance Brokers of Arizona® offers extensive expertise in handyman insurance. We work with a network of carriers to provide personalized service and find the best general liability insurance for handyman businesses. Take action to protect your business with appropriate insurance coverage and set yourself up for long-term success.