Homeowners Insurance Arizona Quotes: Getting the Best Rates

Finding the right homeowners insurance Arizona quotes takes strategy, not just luck. Arizona homeowners face unique risks-from monsoons to theft-that directly impact what you’ll pay.

We at Insurance Brokers of Arizona® know that most people overpay because they don’t understand what moves the needle on their rates. This guide walks you through exactly what insurers look at, how to compare quotes properly, and where the real savings hide.

What Actually Drives Your Arizona Homeowners Insurance Rate

Location Creates Massive Price Differences

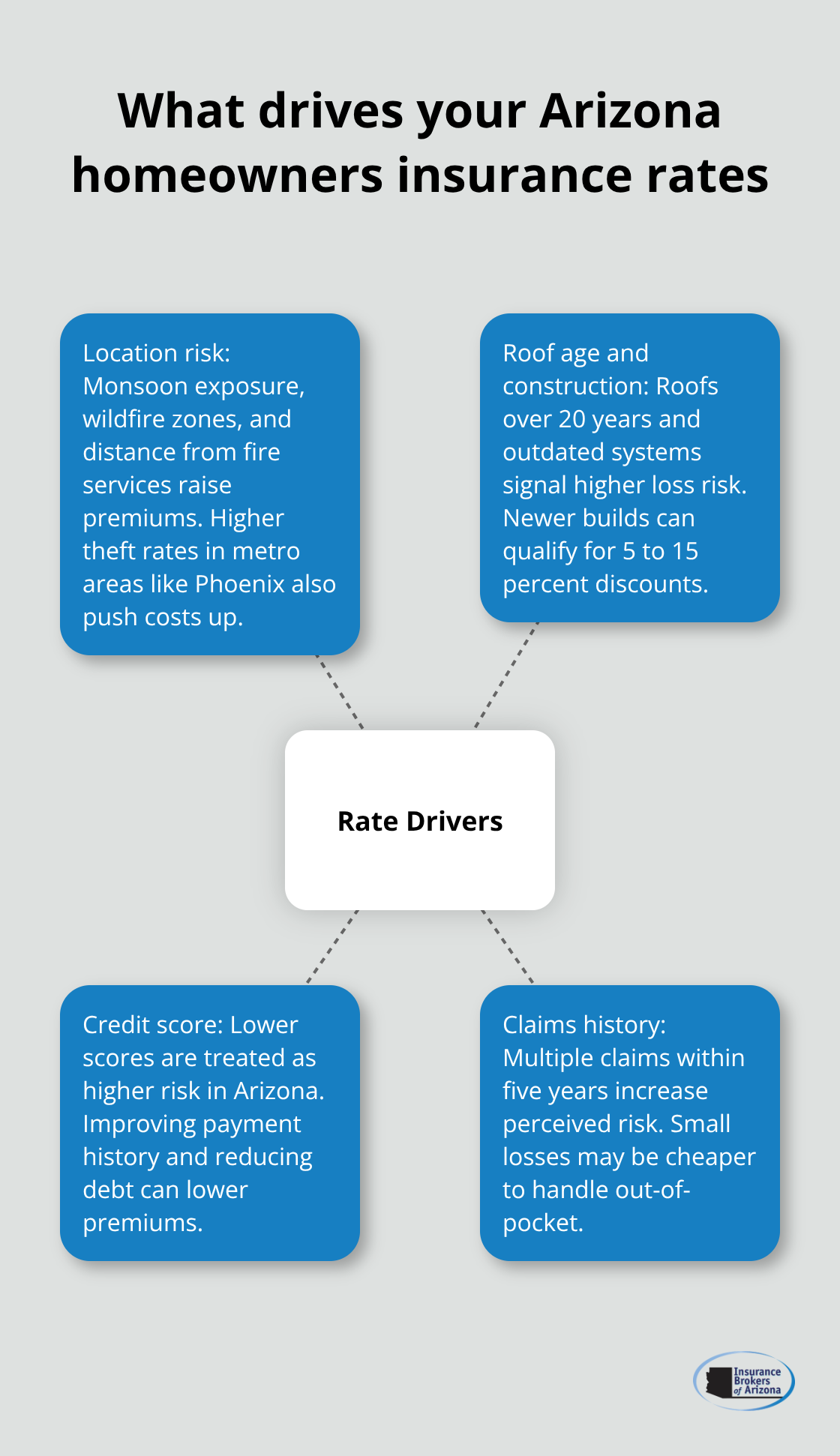

Your location in Arizona matters far more than most people realize. Phoenix residents pay roughly $2,811 annually for a $300,000 dwelling, while Gilbert homeowners in the same coverage bracket pay about $2,087-a difference of $724 per year for nearly identical homes in the same state. This gap exists because Phoenix sits in a higher-risk zone for theft and weather events.

If you live in a monsoon-prone area, your premiums climb because June through September brings flash floods that standard policies don’t cover. Wildfire risk pushes rates even higher; 38 Arizona communities carry ISO Public Protection Classifications of 8B or worse, which signals extreme fire danger to insurers. Distance from fire stations and water sources directly influences your premium, so a home in Prescott will cost more to insure than one in downtown Scottsdale.

Roof Age and Home Construction Type Impact Your Premium

Your roof age and construction type shape what you pay. Homes with roofs older than 20 years face steep rate increases because insurers view them as higher loss risks. If your home was built before 1980 with outdated electrical, plumbing, or HVAC systems, expect to pay significantly more. Conversely, homes built within the last 10 years qualify for newer home discounts that can reduce premiums by 5 to 15 percent depending on the carrier. Insurers assess these factors because older systems fail more often and cost more to repair after damage.

Credit Score Influences Your Premium More Than You Think

Your credit score influences your Arizona homeowners insurance premium more than many people expect. Insurers treat poor credit as a risk indicator, meaning someone with a 620 credit score pays substantially more than someone with a 750 score for identical coverage on identical homes. Arizona does not ban credit-based pricing like California or Massachusetts do, so this factor remains in play. The solution is straightforward: pay bills on time, dispute credit report errors, and reduce revolving debt to improve your score. Even modest improvements to your credit profile can lower your annual premium by hundreds of dollars.

Claims History Affects Your Renewal Rates

Your claims history matters equally. Filing multiple claims within five years signals to insurers that you represent higher risk, even if those claims were legitimate. A single water damage claim three years ago stays on your record and affects renewal rates. This is why small repairs sometimes make financial sense to handle out-of-pocket rather than file claims. Asking your insurer for an inquiry instead of filing an official claim can help preserve your rate status for future renewals. Understanding this dynamic helps you make smarter decisions about when to involve your insurer and when to absorb costs yourself.

Now that you understand what moves your rates, the next step involves comparing quotes from multiple carriers to spot where real savings hide.

How to Compare Quotes Without Wasting Time

Lock in Identical Coverage Across All Quotes

Comparing quotes properly means you request identical coverage levels from multiple carriers, then evaluate what each one actually covers. Most Arizona homeowners request quotes but fail at the comparison stage because they look at different coverage amounts across different insurers. A $300,000 dwelling limit with a $1,000 deductible from State Farm is not comparable to a $250,000 dwelling limit with a $1,500 deductible from USAA. You must lock in the same dwelling amount, deductible, and coverage types across all quotes before price comparisons mean anything.

Calculate Your True Replacement Cost

Start by deciding your actual replacement cost needs-not the home’s market value, but what it would cost to rebuild from scratch. Arizona’s average residential reconstruction costs rose about 6 percent from September 2022 to September 2023 according to Verisk data, so your estimate needs to account for current construction inflation. Request quotes for Coverage A (dwelling), Coverage C (personal property), Coverage D (loss of use), Coverage E (liability), and Coverage F (medical payments to others) at identical limits.

Ask specifically whether quotes include replacement cost value or actual cash value, since replacement cost coverage pays significantly more after damage and better protects you against inflation in repair costs.

Evaluate Claims Handling Before You Choose Price

Once you have apples-to-apples quotes, evaluate customer service quality before deciding on price alone. State Farm carries a complaint index slightly below average in Arizona according to NAIC data, while Allstate’s complaint index runs higher relative to its size. Check how each carrier handles claims by reading recent customer reviews on independent sites-not their own websites. Ask each insurer directly about their claims process: do they have local adjusters in Arizona, how long do they typically take to respond, and can you file claims online or through their mobile app?

A premium that costs $200 less annually becomes expensive if the carrier takes three months to process your wildfire damage claim. Ask about their wildfire mitigation discount structure and whether they offer endorsements like flash flood coverage that American Family provides. These details separate carriers that truly serve Arizona homeowners from those that simply operate here.

Move Forward with Confidence

You now understand what makes quotes comparable and what separates a good carrier from a mediocre one. The next step involves identifying which specific discounts apply to your situation and how to stack them for maximum savings.

How to Stack Discounts and Cut Your Premium

Bundling Delivers Your Largest Savings Opportunity

Consolidating your home and auto insurance with the same carrier produces the single most effective way to lower your Arizona premium. Most insurers offer multi-policy discounts ranging from 10 to 25 percent when you combine homeowners and auto coverage, which means a household paying $1,500 annually for homeowners insurance could save $150 to $375 just by moving auto coverage to the same carrier. State Farm’s average premium for a $400,000 dwelling in Arizona sits around $1,391 per year, and that figure typically includes bundling discounts already factored in. If you’re currently split between two carriers, consolidating immediately addresses your largest savings opportunity before touching deductibles or coverage levels. Progressive’s 2025 Arizona pricing data shows their average homeowners policy costs $122.98 per month, but bundled customers consistently report lower effective rates. The bundling discount alone justifies shopping around because even a moderate rate increase on auto coverage often costs less than the combined savings across both policies.

Raising Your Deductible Requires Honest Financial Assessment

Raising your deductible serves as your second-strongest lever, but it demands honest financial assessment rather than blind rate chasing. Jumping from a $500 deductible to a $1,500 deductible can reduce your annual premium by 15 to 30 percent depending on your carrier and location, which translates to $225 to $450 in annual savings on a $1,500 base premium. However, this only works if you can actually pay that deductible out-of-pocket without financial strain when a loss occurs. Arizona’s wildfire risk and monsoon season mean claims happen, and filing a claim with insufficient deductible funds forces you into worse financial decisions. The key is matching your deductible to your actual emergency savings, not to the discount percentage alone.

Home Improvements and Security Devices Stack Smaller Savings

Home improvements and security devices offer smaller but stackable savings that compound across your policy term. Installing a burglar alarm, smoke detectors, or water leak detection systems typically reduces premiums by 5 to 10 percent, while wildfire mitigation measures like creating defensible space and using fire-resistant materials can qualify you for additional discounts in high-risk zones like Prescott or areas near Flagstaff. Homes built within the last 10 years automatically qualify for newer home discounts of 5 to 15 percent. These improvements matter because they reduce the likelihood of claims, which insurers reward with lower rates.

Combine Multiple Discounts for Maximum Impact

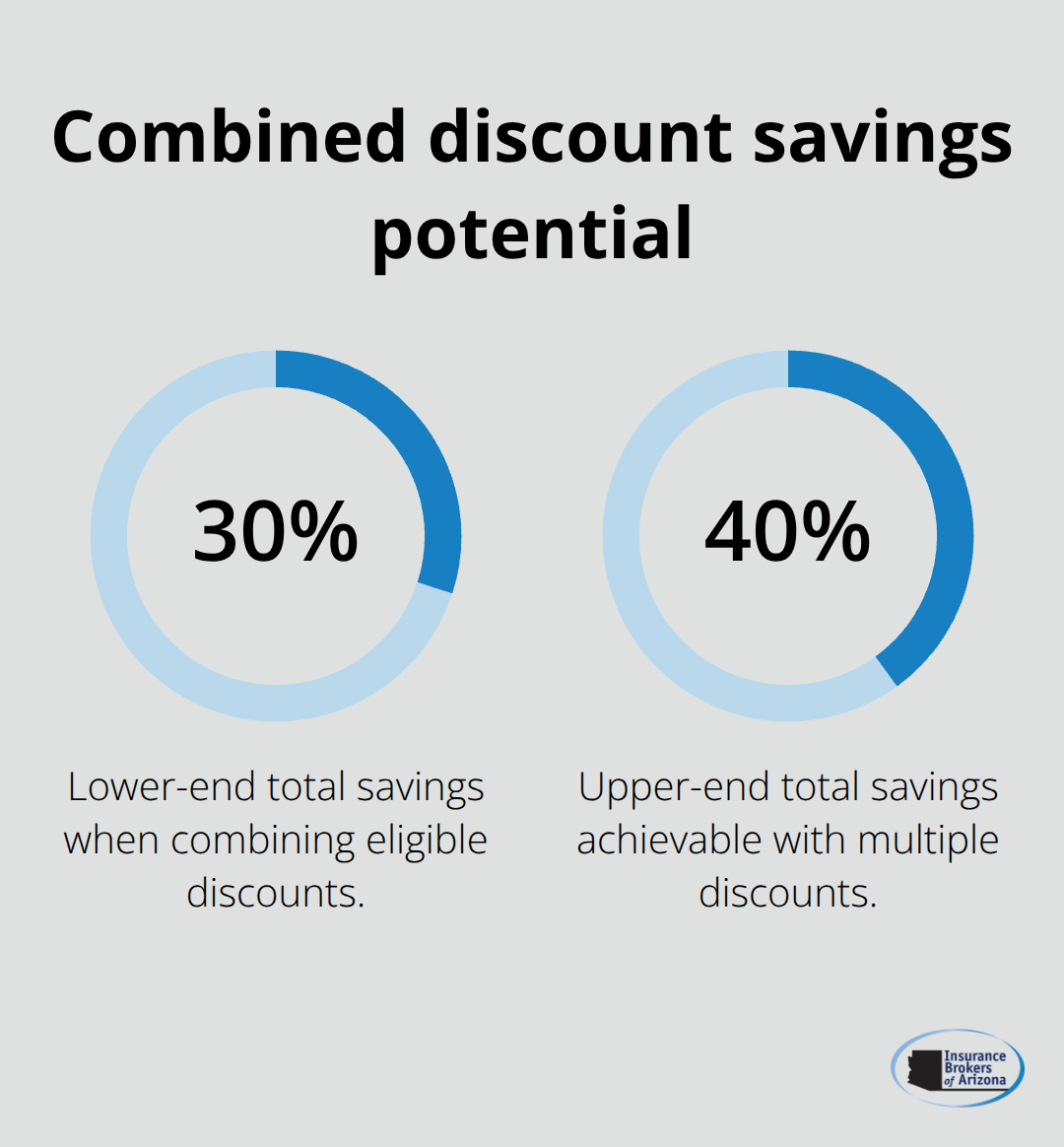

The Arizona Department of Insurance and Financial Institutions notes that combining these smaller discounts-bundling, alarm systems, newer construction, and a sensible deductible increase-often yields total savings of 30 to 40 percent compared to a baseline premium. On a $2,500 annual cost, this means $750 to $1,000 back in your pocket annually.

Each discount individually appears modest, but stacking them transforms your overall rate from expensive to competitive. Most Arizona homeowners leave money on the table because they apply only one or two discounts when four or five are available to them.

Final Thoughts

The real challenge isn’t understanding what drives your homeowners insurance Arizona quotes-it’s executing the comparison work while managing multiple carriers, coverage types, and discount combinations. We at Insurance Brokers of Arizona® partner with over 40 reputable carriers, which means we access rates and options you won’t find shopping alone online. Rather than spending hours requesting quotes from individual insurers and manually comparing coverage details, we handle that legwork and present you with genuinely comparable options tailored to your specific situation.

We listen to your needs, assess your actual replacement cost requirements, identify which discounts apply to you, and present quotes that reflect your real options in the Arizona market. We know the local risk factors that affect Phoenix versus Gilbert versus Tucson, and we understand which carriers handle wildfire claims efficiently. We catch coverage gaps that could leave you underinsured after a monsoon or dust storm.

Contact Insurance Brokers of Arizona® to request personalized homeowners insurance quotes. Bring your current policy if you have one, your home’s age and construction details, and your desired coverage levels. We’ll handle the comparison work and present you with options that balance cost, coverage, and carrier reliability.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.