Commercial Property Insurance 101: A Beginner’s Guide

Commercial property insurance is a vital safeguard for businesses of all sizes. At Insurance Brokers of Arizona®, we’ve seen firsthand how this coverage can protect companies from devastating financial losses.

In this Commercial Property Insurance 101 guide, we’ll break down the essentials of this crucial coverage. We’ll explore what it covers, who needs it, and how to choose the right policy for your business.

What Is Commercial Property Insurance?

Definition and Purpose

Commercial property insurance protects a company’s physical assets against various risks. This insurance covers buildings, equipment, inventory, and other physical property essential to business operations. It shields businesses from financial losses due to fire, theft, and natural disasters.

Who Needs This Coverage?

Almost every business that owns or leases physical space should consider commercial property insurance. This includes:

- Retail stores and restaurants

- Manufacturing facilities

- Office buildings

- Warehouses

- Hotels and motels

- Apartment complexes

Even home-based businesses often require separate commercial property coverage, as homeowners insurance typically doesn’t cover business-related losses.

Commercial vs. Residential Property Insurance

Commercial property insurance differs significantly from its residential counterpart. Key differences include:

- Coverage Limits: Commercial policies often have higher limits to account for the greater value of business assets.

- Complexity: They tend to be more complex, with options for specialized coverage (e.g., business interruption insurance).

- Claims Process: Commercial property claims often involve more extensive investigations and can take longer to resolve due to the complexity of business operations and the potential for larger financial losses.

Tailoring Coverage to Your Business

When you select a commercial property insurance policy, you must assess your specific risks. Factors like location, industry, and the value of your assets all play a role in determining the right coverage. For example, a beachfront hotel in Arizona might need additional protection against water damage, while a tech company might require higher limits for expensive computer equipment.

The Importance of Professional Guidance

Navigating the complexities of commercial property insurance can challenge business owners. Professional insurance brokers (like those at Insurance Brokers of Arizona®) can provide valuable insights and help you find a policy that addresses all potential risks and provides comprehensive protection.

As we move forward, let’s explore the various coverage options available in commercial property insurance policies.

What Does Commercial Property Insurance Cover?

Building Coverage: The Foundation of Protection

Building coverage forms the cornerstone of commercial property insurance. It protects the physical structure of your business premises, including permanent fixtures and fittings. The Insurance Information Institute reports that building coverage typically accounts for about 60% of a commercial property policy’s value.

This coverage extends beyond the main building. It often includes structures like storage sheds, garages, and fences. For businesses in Arizona, where extreme heat can cause structural damage, this coverage proves particularly important.

Business Personal Property: Safeguarding Your Assets

Business personal property coverage protects the items you use to run your business. This includes furniture, equipment, inventory, and even improvements you’ve made to a leased space. The Small Business Administration reports that 40% of small businesses never reopen after a disaster, often due to inadequate coverage for their business property.

When you assess your needs, consider the replacement cost of all your business assets. Many businesses underestimate this value, which leaves them vulnerable to significant out-of-pocket expenses in the event of a loss.

Business Interruption Insurance: Keeping You Afloat

Business interruption insurance is a critical component that many overlook. It covers lost income and ongoing expenses if your business must temporarily close due to a covered event. The Federal Emergency Management Agency (FEMA) states that 40% of businesses do not reopen after a disaster, and 25% fail within one year. Business interruption coverage can make the difference between recovery and closure.

This coverage typically activates after a short waiting period (usually 48 to 72 hours after the event). It can cover expenses like rent, loan payments, and employee wages, which helps you maintain operations and retain staff during the recovery period.

Additional Coverage Options: Tailoring Your Protection

Commercial property insurance isn’t one-size-fits-all. Additional coverage options can fill gaps and provide comprehensive protection. Equipment breakdown coverage, for instance, can be essential for businesses that rely on specialized machinery. The Hartford reports that equipment breakdown causes over $1 billion in losses annually.

Debris removal coverage is another important consideration, especially in areas prone to natural disasters. After a catastrophic event, cleanup costs can be substantial. This coverage helps manage those expenses, which allows you to focus on rebuilding.

Every business has unique needs. Insurance professionals can help you identify potential risks and recommend appropriate coverage options. Their goal is to ensure that when the unexpected happens, your business remains fully protected and ready to bounce back.

Now that we’ve covered the main components of commercial property insurance, let’s explore the factors that affect your premiums.

What Impacts Your Commercial Property Insurance Costs?

Location: A Key Factor

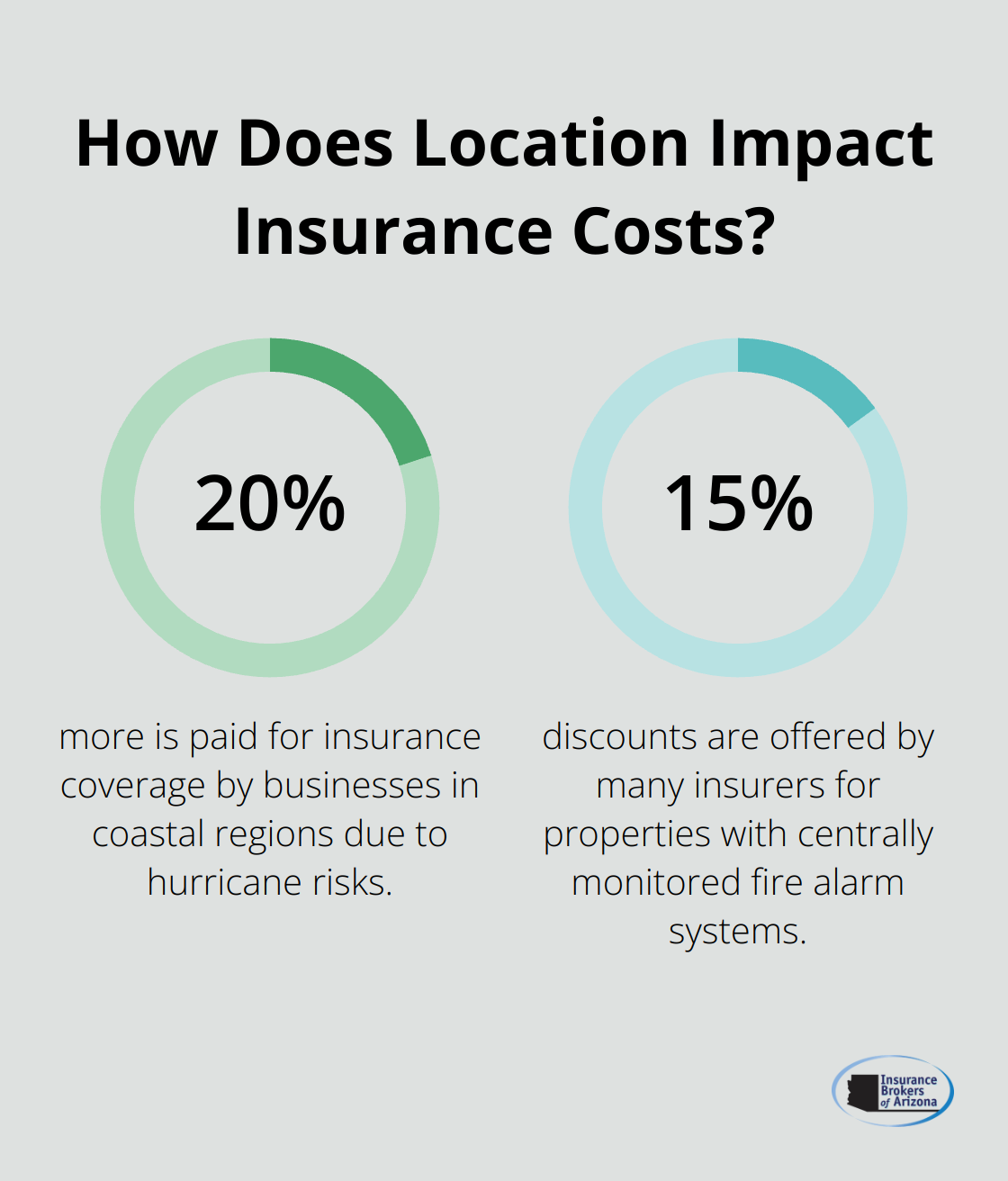

Your property’s location significantly affects insurance costs. Areas prone to natural disasters typically face higher premiums. The Insurance Information Institute reports that businesses in coastal regions might pay up to 20% more for coverage due to hurricane risks.

In Arizona, extreme heat and dust storms can increase rates. Urban areas with higher crime rates might also see increased premiums. Properties near fire stations or in areas with low crime rates often benefit from lower insurance costs.

Building Characteristics and Age

The type of building, its construction materials, and age impact insurance rates. Newer buildings constructed with fire-resistant materials often qualify for lower premiums. The Insurance Services Office (ISO) reports that buildings made of fire-resistive materials can see up to a 60% reduction in fire-related property insurance costs compared to wood-frame structures.

Older buildings might face higher premiums due to outdated electrical systems, plumbing, or roofing. Upgrading these systems can lead to substantial savings. For example, replacing an old roof can result in premium reductions of up to 20% with some insurers.

Safety Measures: Protection Systems and Security

Investments in fire protection and security systems can reduce your insurance costs. The National Fire Protection Association states that buildings with sprinkler systems experience 60% lower property damage on average during fires. Many insurers offer discounts of up to 15% for properties with centrally monitored fire alarm systems.

Security measures like surveillance cameras, alarm systems, and secure locks can also lead to premium reductions. Some insurance companies offer discounts of 5-20% for comprehensive security systems.

Claims History and Business Operations

Your claims history plays a significant role in determining your premiums. Businesses with a history of frequent claims might face higher rates. The type of business operations also affects costs. High-risk industries (e.g., manufacturing or chemical processing) typically pay more for coverage than low-risk businesses (e.g., office-based companies).

Coverage Limits and Deductibles

The amount of coverage you choose and your deductible level directly impact your premiums. Higher coverage limits result in higher premiums, while higher deductibles can lower your costs. It’s important to balance adequate protection with affordable premiums.

Insurance Brokers of Arizona® can help businesses find this balance, ensuring comprehensive coverage at competitive rates. We understand the unique risks faced by Arizona businesses and can tailor policies to meet specific needs.

Final Thoughts

Commercial property insurance 101 emphasizes the importance of protecting your business assets. This coverage safeguards physical property and financial stability, making it essential for informed decision-making. We recommend you assess your specific business needs, location risks, and potential financial impacts when selecting the right policy.

Insurance Brokers of Arizona® specializes in tailoring commercial property insurance to the unique needs of Arizona businesses. Our partnerships with over 40 reputable carriers allow us to offer competitive rates without compromising on coverage. We take pride in our exceptional customer service, ensuring that you understand your policy and have the protection you need.

Our team of experienced brokers can guide you through the complexities of commercial property insurance. We help you navigate coverage options, understand policy terms, and find the best fit for your business. Contact us today to secure optimal coverage that balances comprehensive protection with cost-effectiveness for your business.