Liability-only auto insurance is the bare minimum required by law in every state, yet many drivers don’t understand what it actually covers or whether it’s right for them.

At Insurance Brokers of Arizona®, we’ve helped countless customers navigate this decision. This guide breaks down liability coverage limits, state requirements, and when this basic protection makes financial sense for your situation.

What Liability-Only Coverage Actually Pays For

The Three-Part Limit Structure

Liability-only auto insurance covers injuries and property damage you cause to other people in an accident. If you’re at fault and hit another vehicle, liability pays their medical bills, vehicle repairs, lost wages, and rental car costs while theirs is being fixed. It also covers legal expenses if the other driver sues you.

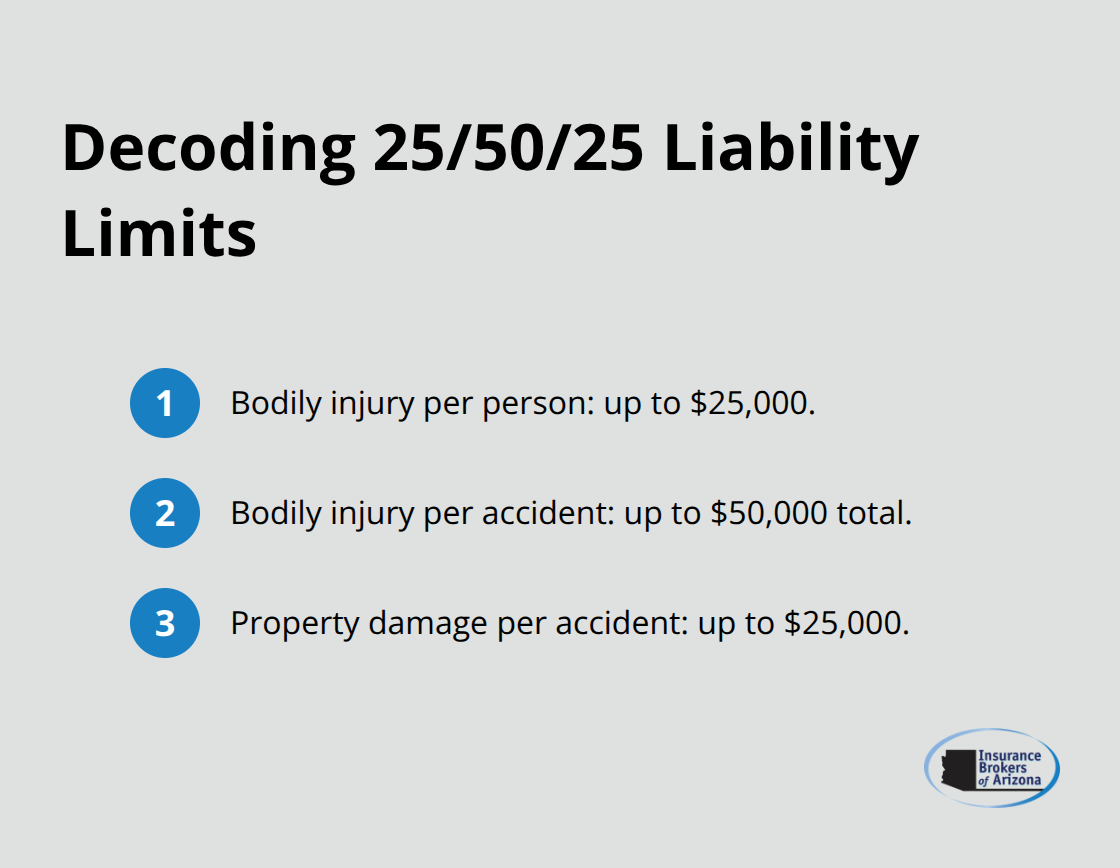

The coverage has three limits shown as numbers like 25/50/25, which represent bodily injury per person, bodily injury per accident, and property damage per accident in thousands of dollars. So 25/50/25 means the policy pays up to $25,000 per injured person, $50,000 total for all injuries in one accident, and $25,000 for property damage. These limits matter because if damages exceed them, you pay the difference from your own pocket.

Why Arizona’s Minimum Falls Short

Most states set minimum liability requirements, and Arizona’s state minimum is 15/30/10-a level many drivers consider dangerously low. Financial experts recommend liability limits of at least $100,000 per person and $300,000 per accident to protect against these scenarios, making the state minimum significantly inadequate for most drivers.

What Liability-Only Does Not Protect

Liability coverage only pays for damage you cause to others, never your own vehicle or medical bills. If you cause an accident and your car needs $8,000 in repairs, liability won’t pay a cent-you cover that yourself. Your own injuries, lost wages, and pain and suffering aren’t covered either. This is the critical trade-off: lower premiums in exchange for zero protection of your own assets.

Liability also does not apply if you hit an uninsured driver or someone with insufficient coverage, which is why uninsured motorist coverage exists in roughly half the states and why some drivers view it as essential, not optional.

When Liability-Only Makes Financial Sense

If you’re financing or leasing a vehicle, your lender will require full coverage including collision and comprehensive, so liability-only isn’t an option regardless of cost. For older, paid-off cars worth $3,000 to $5,000, liability-only becomes a legitimate financial strategy if you have an emergency fund to cover repairs.

The math is straightforward: if your car’s value is close to the annual premium difference between liability-only and full coverage, you self-insure small losses and it makes sense. But if you depend on that vehicle daily and can’t afford a $4,000 repair bill, liability-only creates real financial risk that no monthly savings can justify. Your personal circumstances-not just the price tag-determine whether this bare-bones coverage works for you.

State Requirements and Legal Minimums for Liability Coverage

What Your State Actually Requires

Every state mandates liability coverage, but the minimums vary dramatically and most fall dangerously short of real-world protection. Arizona’s state minimum of 25/50/15 ranks among the lowest in the nation, yet drivers who carry only these limits expose themselves to massive out-of-pocket liability if they cause a serious accident. A single accident involving multiple injuries can easily exceed $50,000 in damages, leaving you personally responsible for anything beyond your policy limits.

New Hampshire stands alone as the only state without a mandatory insurance requirement, though drivers must still prove financial responsibility or face license suspension. Florida operates under no-fault rules requiring Personal Injury Protection but only 10/20/10 in property damage liability, creating a different compliance landscape than at-fault states like Arizona. The key takeaway: meeting your state’s minimum means you’re legally compliant while remaining financially vulnerable.

Penalties for Driving Without Liability Insurance

Penalties for driving without liability insurance range from license suspension to substantial fines, but the real consequence is financial ruin if you cause an accident. Most states suspend your driver’s license immediately after an uninsured accident, and you’ll typically face fines between $500 and $2,000 depending on your state and whether it’s your first offense. Some states require you to file an SR-22 form, which certifies you carry insurance and costs an additional $15 to $25 annually. If you cause injury or property damage without insurance, the other party can sue you directly for damages, medical bills, lost wages, and legal fees-potentially garnishing your wages or placing a lien on your home for years.

How to Verify Your State’s Requirements

To verify your state’s specific requirements, visit your state’s Department of Motor Vehicles website or contact your state insurance commissioner’s office, where you’ll find exact liability limits, any required uninsured motorist coverage, and penalties for non-compliance. Arizona drivers should confirm whether their current policy meets state obligations and whether additional coverage (such as uninsured motorist protection) makes sense for their situation. Understanding these requirements takes minutes and prevents costly compliance mistakes that could affect your driving privileges and finances for years.

Who Should Choose Liability-Only Coverage

Liability-only coverage makes financial sense only in specific situations, and the wrong decision here costs you thousands. Drivers often make this choice for the wrong reasons, typically because they fixate on monthly premiums instead of total financial risk. The reality is stark: liability-only works for a narrow group of drivers, and if you’re not in that group, this bare-minimum coverage will devastate your finances after an accident.

The Math Behind Older Cars

For vehicles worth $3,000 to $5,000, the numbers can justify liability-only coverage, but only under specific conditions. Consider a real example: a 2007 Honda Pilot with 175,000 miles valued at roughly $3,500 in Massachusetts. The annual premium for liability-only was $2,900, while full coverage (collision and comprehensive) cost $3,900-a $1,000 annual difference. If your car’s replacement value is close to or lower than the annual premium gap, self-insuring makes mathematical sense because you’ll break even within a few years. However, this calculation only works if you have genuine financial reserves. The driver in that example had $25,000 in savings, which meant absorbing a $3,500 repair bill wouldn’t create financial hardship. Without that cushion, liability-only transforms from a cost-saving strategy into a gamble you can’t afford to lose.

When Budget Constraints Override Everything Else

Drivers with genuinely limited budgets face a harder choice, and no easy answer exists. If you earn $35,000 annually and can barely afford $150 monthly for insurance, liability-only becomes your only option-not because it’s ideal, but because full coverage at $250 monthly simply isn’t possible. In this situation, focus on maximizing what liability covers by choosing higher limits than your state minimum. Arizona’s 15/30/10 minimum is dangerously low; try 50/100/50 if you can manage it because that extra protection costs far less than the alternative of facing a lawsuit. Additionally, consider whether uninsured motorist coverage is available in your state-it protects you when someone else causes an accident, and it typically adds only $15 to $30 monthly to your premium.

Shop across multiple carriers because cheap auto liability insurance shows significant variation across states during 2024-2025. Three quotes take 20 minutes and could save $400 annually.

Your Job Status and Daily Dependence Matter More Than You Think

If you depend on your vehicle for work, liability-only coverage is a terrible decision regardless of cost. A rideshare driver, delivery worker, or salesperson whose car is essential to earning income faces catastrophic risk. If your vehicle gets totaled in an accident you caused, you’re without transportation, without income, and facing repair costs you can’t afford-all simultaneously. That’s not risk management; that’s financial self-sabotage. Similarly, if you have a long commute and no backup transportation option, liability-only exposes you to weeks without a vehicle while you scramble to pay repairs out of pocket. The monthly savings vanishes instantly when you’re paying $200 daily for a rental car while yours sits in the shop.

Final Thoughts

Liability-only auto insurance solves one problem while creating another. It keeps your monthly payments low and satisfies state legal requirements, but it leaves your own vehicle and finances completely unprotected when an accident happens. The decision to carry only liability coverage should never focus on finding the cheapest option-it should focus on whether you can genuinely afford the consequences if something goes wrong.

Auto insurance liability only makes sense for a small group of drivers who meet specific conditions. You need a paid-off vehicle worth less than the annual premium difference between liability and full coverage, a substantial emergency fund to cover repairs or replacement costs, and a clean driving record with low annual mileage. Most importantly, you cannot depend on that vehicle for work or daily transportation. If any of these conditions don’t apply to you, liability-only coverage will cost you far more than you save.

At Insurance Brokers of Arizona®, we work with drivers across Arizona to find coverage that protects both their finances and their driving privileges. With partnerships with over 40 carriers, we can show you real quotes for liability-only and full coverage options so you can compare actual costs instead of guessing. Contact Insurance Brokers of Arizona® today to get personalized quotes and stop overpaying for coverage you don’t need or underpaying for protection you can’t afford to lose.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.