How to Find the Cheapest Auto and Homeowners Insurance

Finding the cheapest auto and homeowners insurance requires more than just comparing prices. Smart shoppers understand the factors that drive premium costs and know how to leverage discounts effectively.

We at Insurance Brokers of Arizona® see clients save hundreds of dollars annually by avoiding common pricing mistakes. The right strategy can reduce your insurance costs by 20-30% without sacrificing coverage quality.

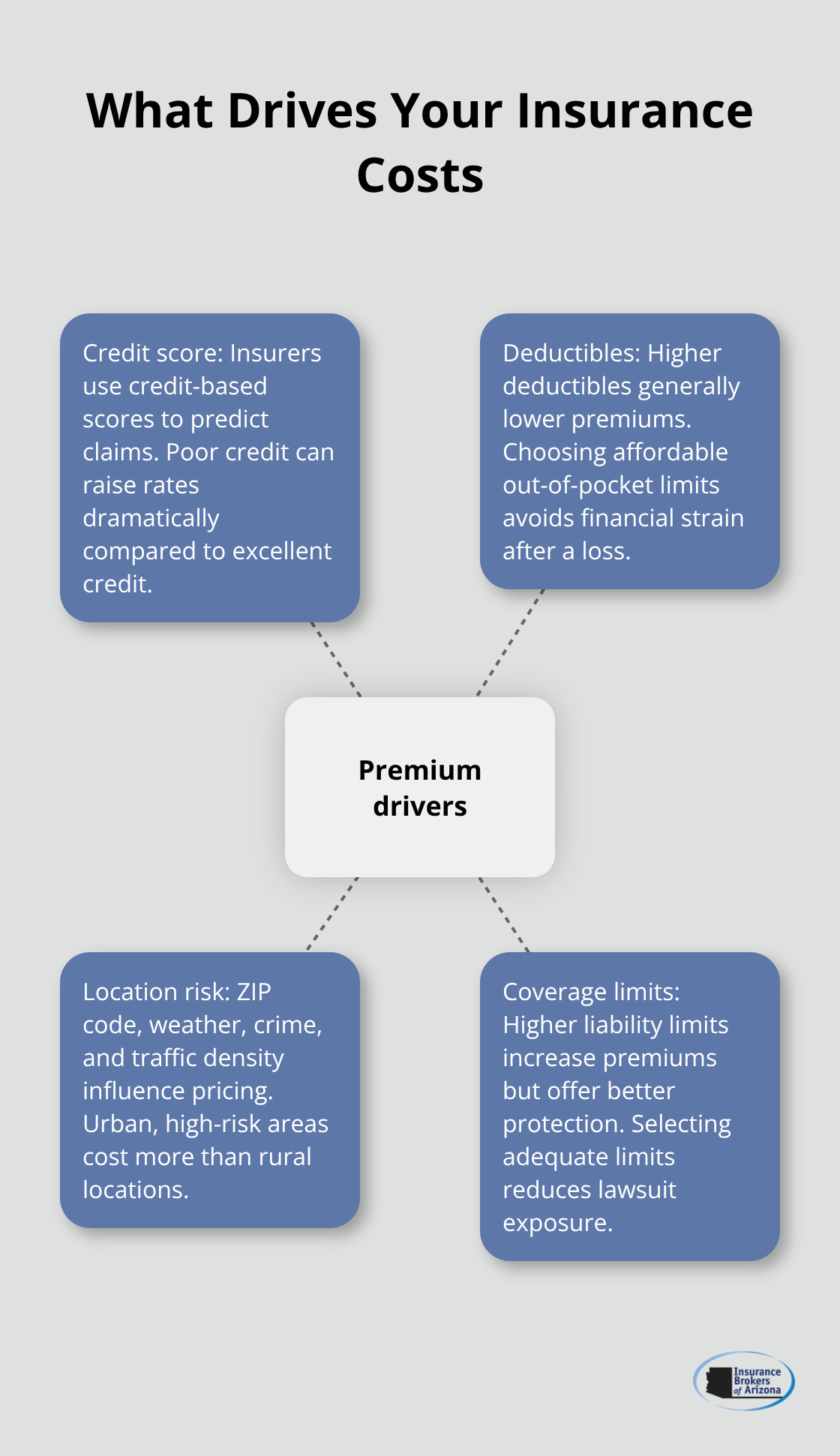

What Drives Your Insurance Costs

Credit Score Impact on Premium Rates

Your credit score affects your insurance premiums more than most people realize. Insurance companies use credit-based insurance scores to predict claim likelihood, with poor credit potentially raising your rates by 50-100% compared to excellent credit. Clients with credit scores below 600 often pay double what those with scores above 750 pay for identical coverage. Improving your credit score from fair to good can save you $400-800 annually on combined auto and home insurance.

Deductible Strategy Changes Everything

Higher deductibles reduce your premiums significantly, but most people choose the wrong amounts. Raising your auto deductible from $500 to $1,000 typically saves 10-15% on comprehensive and collision coverage, while increasing your homeowners deductible from $1,000 to $2,500 can cut premiums by 12-20%. The key lies in setting deductibles at amounts you can afford to pay out-of-pocket without financial strain.

Location Risk Factors You Cannot Control

Your ZIP code determines a substantial portion of your insurance costs through risk assessment algorithms. Urban areas with higher crime rates, severe weather patterns, and accident frequencies command premium increases of 30-60% over rural locations. Insurance companies analyze hyperlocal data including theft rates, natural disaster frequency, and traffic density within specific neighborhoods. Moving just five miles can sometimes reduce your premiums by hundreds of dollars annually (making location a critical factor when house hunting or relocating).

Coverage Limits Shape Your Rates

The coverage limits you select directly impact your premium costs. Higher liability limits increase your rates but provide better protection against lawsuits and major claims. Most drivers choose state minimum coverage without understanding the financial risks they face. Increasing your auto liability from state minimums to $100,000/$300,000 typically adds only $50-100 annually but provides substantially better protection.

These pricing factors work together to create your final premium, but smart shoppers know how to minimize costs through strategic choices and comparison techniques.

How Can You Cut Insurance Costs by Hundreds

Master the Art of Policy Bundling

Bundling auto and homeowners insurance with the same carrier saves you between 5% and 30% on total premiums according to industry data. Liberty Mutual reports their new customers save an average of $950 annually through bundled policies, while some carriers like Amica offer up to 30% discounts for combined coverage. The savings compound when you add additional vehicles under the multi-car discount, which can reduce each additional vehicle’s premium by 10-25%.

However, bundling only works when the combined discounted price beats separate policies from different carriers. We recommend you calculate both scenarios before you commit to any bundle arrangement. Some carriers excel at auto insurance while others provide better homeowners rates, making separate policies the smarter financial choice.

Compare Quotes From Multiple Carriers Strategically

Shopping at least five different insurance companies can reduce your costs by 20-40% for identical coverage levels. Rate variations between carriers for the same coverage profile often exceed $1,000 annually, which makes comparison shopping the single most effective cost-reduction strategy. Focus your comparisons on highly-rated carriers with strong financial stability ratings from A.M. Best Company.

Use online comparison tools like The Zebra, which compares quotes from over 100 companies in approximately 5 minutes, or work with independent agents who access multiple carrier networks. The key lies in comparing identical coverage limits and deductibles rather than just premium prices (since coverage differences can create misleading cost comparisons).

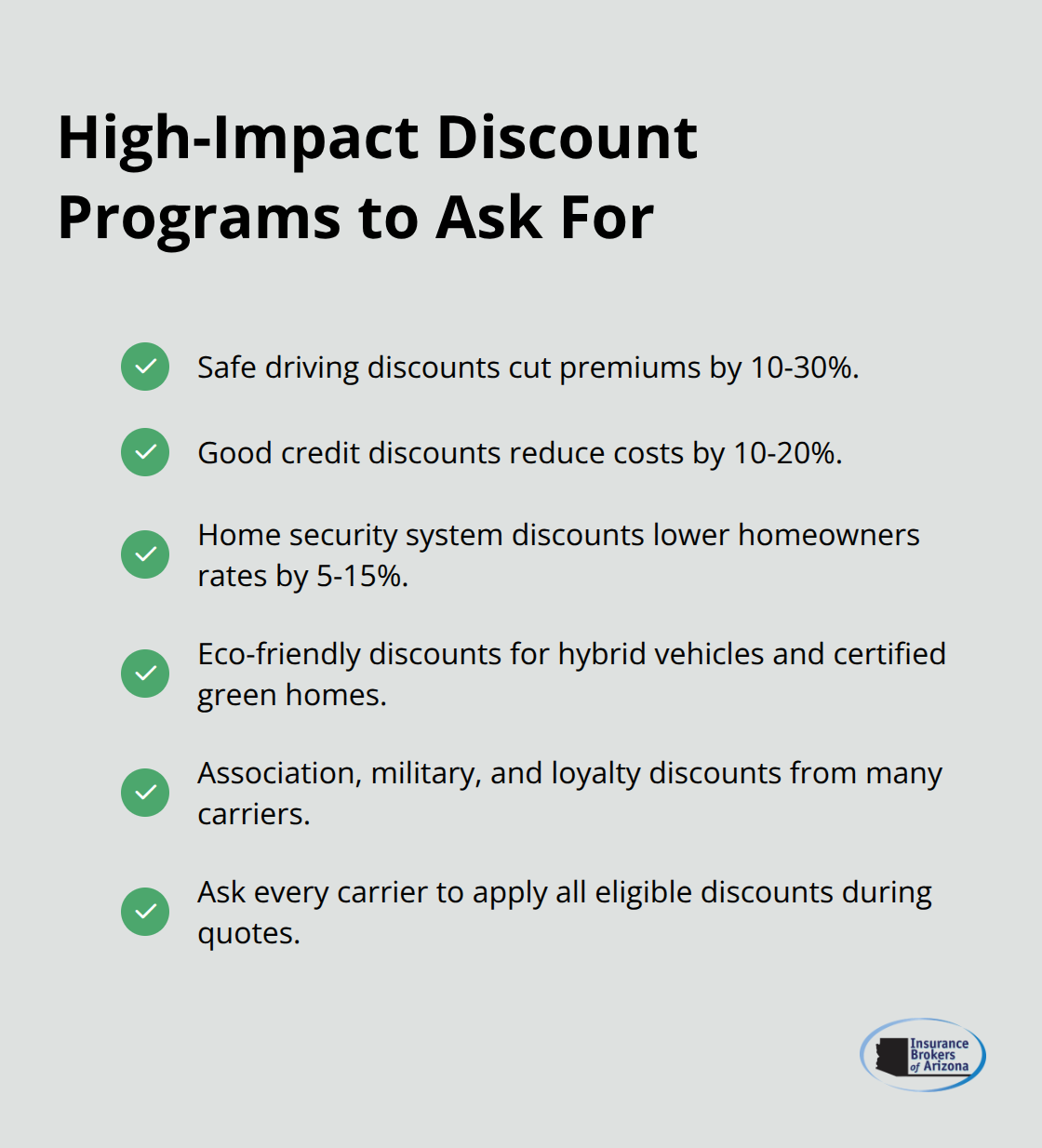

Maximize Available Discount Programs

Insurance carriers offer numerous discounts beyond bundling that most customers never request. Safe driving discounts reduce premiums by 10-30% for claim-free periods of three to five years. Good credit discounts can save another 10-20% on total premiums. Security system discounts for homes with monitored alarms provide 5-15% reductions on homeowners coverage.

Eco-friendly discounts from carriers like Travelers reward hybrid vehicle owners and certified green home owners with additional savings. Professional association memberships, military service, and loyalty programs offer further reductions. The critical step involves asking each carrier specifically about all available discounts during the quote process rather than assuming they will automatically apply them.

These cost-cutting strategies work best when you avoid common mistakes that unknowingly inflate your premiums.

What Insurance Mistakes Cost You Money

Minimum Coverage Creates Maximum Financial Risk

State minimum auto insurance coverage exposes you to catastrophic financial losses that far exceed any premium savings. Texas requires only $30,000 per person and $25,000 for property damage, but a single serious accident can generate medical bills that exceed $100,000 and property damage claims that reach $50,000 or more. Drivers with minimum coverage face personal bankruptcy when their $30,000 liability limit cannot cover a $200,000 injury claim, which forces them to pay hundreds of thousands from personal assets. The difference between minimum coverage and adequate $100,000/$300,000 limits costs only $50-100 annually but protects against million-dollar lawsuits that destroy financial stability.

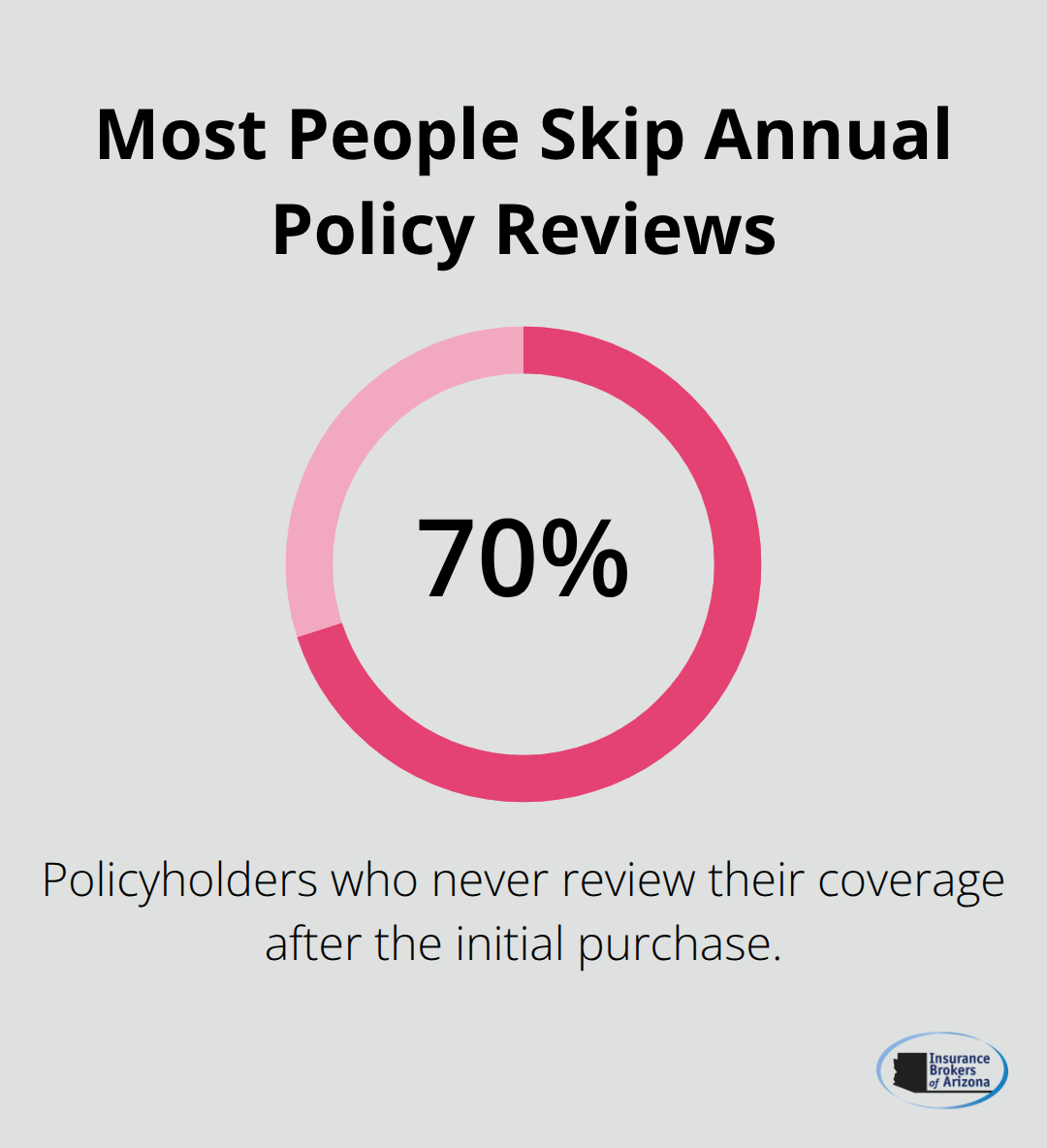

Annual Policy Reviews Prevent Rate Creep

Insurance companies raise rates annually through small increases that compound over time, yet 70% of policyholders never review their coverage after the initial purchase. Carriers count on customer inertia and gradually increase premiums by 3-8% yearly while competitors offer lower rates for identical coverage.

Clients who skip annual reviews pay 15-25% more after three years compared to active shoppers who switch carriers every two to three years. Life changes like marriage, new jobs, home improvements, or paid-off vehicles qualify you for additional discounts, but insurers will not automatically apply these savings unless you specifically request coverage updates and discount reviews.

Unreported Changes Leave Money on the Table

Policyholders lose hundreds of dollars in missed discounts when they fail to report changes that qualify for rate reductions. Security system installations, defensive course completions, or milestone birthdays trigger discount eligibility that requires active notification to your carrier. Remote work arrangements that reduce daily commutes can lower auto premiums by 10-20% through low-mileage discounts, but insurers maintain higher rates unless you report reduced patterns. Home improvements like new roofs, updated electrical systems, or security upgrades reduce risk profiles and qualify for premium reductions, yet most homeowners continue to pay higher rates for outdated risk assessments that no longer reflect their actual situation.

Final Thoughts

The cheapest auto and homeowners insurance comes to those who treat coverage selection as an active annual process rather than a set-and-forget decision. Smart buyers compare quotes from multiple carriers every 12-18 months, maintain excellent credit scores, and actively pursue all available discounts. These strategies consistently reduce insurance costs by 20-30% while maintaining comprehensive protection.

Independent agents provide valuable expertise when you own multiple properties, operate a business, or face complex coverage needs that require specialized knowledge. These professionals access multiple carrier networks and identify coverage gaps that online tools often miss. We at Insurance Brokers of Arizona® connect clients with personalized insurance solutions that match specific risk profiles and budget requirements.

Smart insurance shoppers save $800-1,500 annually while maintaining superior coverage protection compared to those who accept the first quote they receive. These savings compound over decades and create substantial wealth preservation that supports long-term financial goals (making strategic insurance decisions one of the most effective ways to protect both assets and budgets). The most successful approach adapts coverage decisions to changing life circumstances rather than maintaining static policies year after year.