One accident shouldn’t derail your finances for years. Auto insurance with accident forgiveness protects you from rate hikes when you’re at fault, letting you move forward without penalty.

At Insurance Brokers of Arizona®, we help drivers understand how this coverage works and whether it’s right for you. This guide breaks down the real benefits and shows you how to find the best policy for your situation.

What Accident Forgiveness Actually Covers

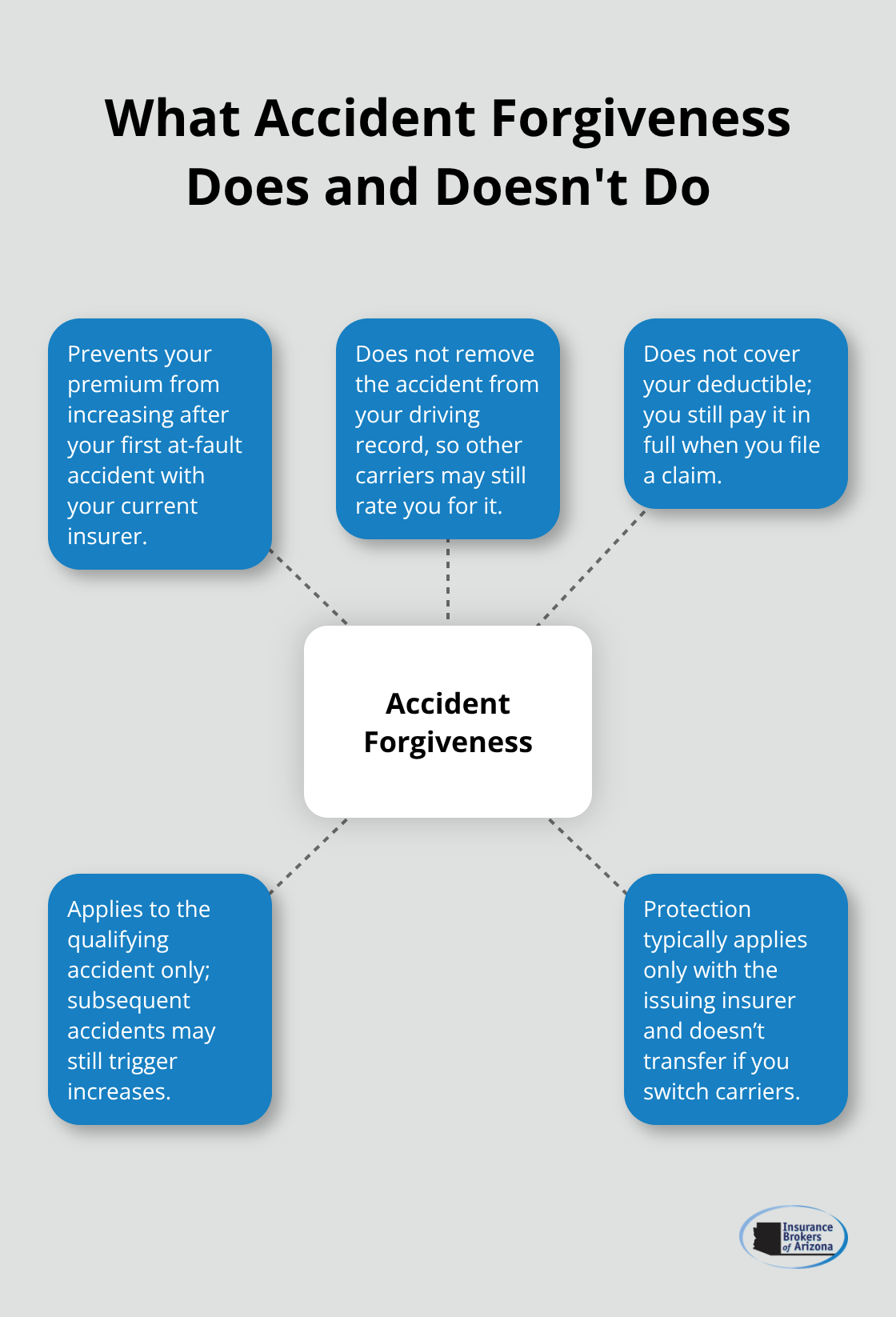

Accident forgiveness sounds straightforward, but most drivers misunderstand what it actually protects. It prevents your insurance rate from increasing after your first at-fault accident, but it does not erase the accident from your driving record or cover your deductible. When you file a claim, you still pay the full deductible out of pocket. What accident forgiveness does is stop your insurer from using that claim as a reason to raise your premium at renewal.

According to The Zebra’s analysis of Quadrant Information Services and S&P Global rate filings, the average rate increase after a first at-fault accident reaches about $845 per year. Over three years, that adds up to roughly $2,535 in extra premiums. Accident forgiveness blocks that increase, but only for that specific accident and only with that specific insurer. If you switch carriers later, the new company can still consider the accident when calculating your rates.

Eligibility Requirements Vary Widely by Insurer

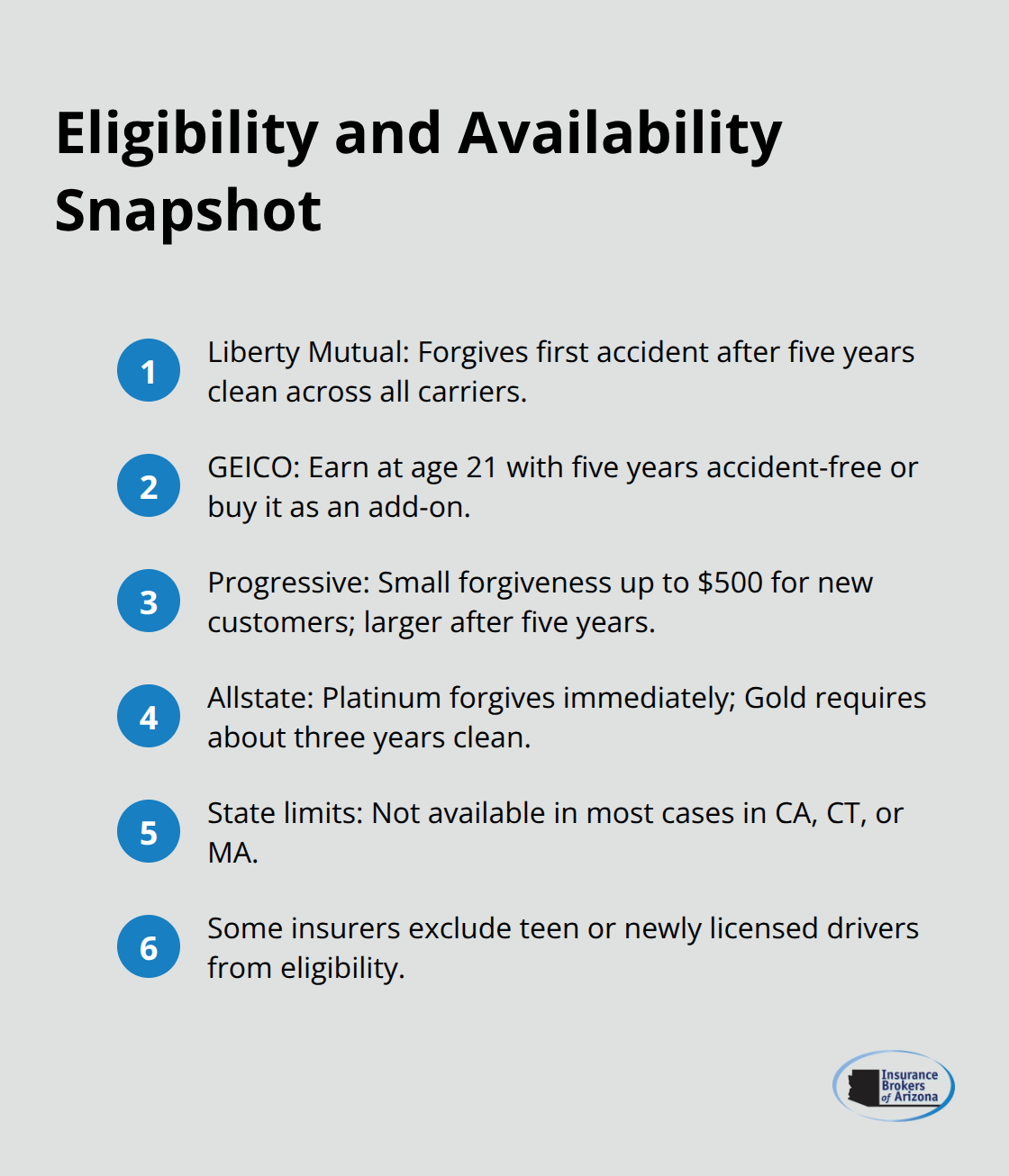

Most major carriers require five years of accident-free driving before you qualify, though some have different timelines. Liberty Mutual forgives the first accident after five years of clean driving across all carriers, not just with them. GEICO lets you earn accident forgiveness at age 21 with five years accident-free, or you can purchase it upfront. Progressive takes a tiered approach with new customers automatically receiving small accident forgiveness that covers claims up to $500, then offering larger forgiveness after five years with the company. Allstate’s approach depends on your plan level. The Platinum plan forgives immediately, while the Gold plan requires roughly three years accident-free. Importantly, accident forgiveness is not available in California, Connecticut, or Massachusetts in most cases, so your state matters significantly.

Some insurers also exclude teen drivers or newly licensed drivers from these programs entirely.

What Disqualifies You from Protection

A single speeding ticket or violation can eliminate your eligibility with some insurers, making this coverage harder to access than it appears. Drivers younger than 25 often face longer waiting periods. If you switch insurers, that forgiveness does not transfer, meaning your new company treats you as a new customer without the benefit. The forgiveness also applies per policy, not per driver in most cases, so a household with multiple drivers typically shares one forgiven accident across everyone on that policy.

Understanding these exact limitations matters before an accident happens. Your insurer’s specific rules determine whether accident forgiveness actually protects you when you need it most. The next section shows you how to compare coverage options across carriers and ask the right questions to confirm what your policy actually includes.

Why Accident Forgiveness Saves You Money Over Time

The math behind accident forgiveness is straightforward, and it heavily favors drivers who carry this coverage. According to The Zebra’s analysis of rate data from Quadrant Information Services and S&P Global, a single at-fault accident costs the average driver $845 more per year in premiums. That $845 annual increase doesn’t last just one year-it typically persists for three years, totaling approximately $2,535 in extra premiums for one mistake. Accident forgiveness eliminates that hit entirely. If your insurer charges $50 to $100 annually for accident forgiveness, you protect yourself against thousands in potential rate increases. The coverage pays for itself many times over if you ever file an at-fault claim.

Why Even Safe Drivers Need This Protection

You cannot control other drivers on the road, which is why even safe drivers benefit from accident forgiveness. A rear-end collision or an accident at an intersection isn’t always preventable, regardless of your skill behind the wheel. Without accident forgiveness, one incident creates a financial penalty that follows you through multiple renewal periods, even after you’ve paid your deductible and the claim closes. One accident shouldn’t trigger years of financial consequences.

The Real Cost of Switching Insurers After an Accident

Many drivers mistakenly believe they can escape rate increases by switching to a new insurance company after an accident. This strategy fails completely because your new insurer will see the accident on your driving record and factor it into your rates immediately. The accident doesn’t transfer with you as a forgiven claim-it transfers as a liability mark that the new company uses to calculate your premium. If your current insurer offers accident forgiveness and you already qualify, leaving them after an accident wastes that protection and exposes you to higher rates everywhere else.

Some insurers like Liberty Mutual extend forgiveness across all carriers, meaning five years of clean driving with any combination of companies qualifies you, but once you file a claim, only your current insurer’s forgiveness policy protects you at renewal. Switching carriers also means losing any loyalty discounts or bundled savings you’ve accumulated. The financial advantage of staying with an insurer that has already forgiven your accident far outweighs any perceived savings from shopping around immediately after a claim.

How Accident Forgiveness Reduces Your Stress

Beyond the dollars, accident forgiveness removes the anxiety that accompanies being at fault. After an accident, most drivers worry about their renewal notice and whether their rates will spike. With accident forgiveness in place, you file the claim, pay your deductible, and move forward knowing your rate stays stable. This peace of mind has real value-it means you can focus on repairs and recovery rather than financial dread.

Families with teenage drivers benefit especially because teen accidents are statistically more common. According to the National Highway Traffic Safety Administration, drivers aged 16 to 19 have crash rates three times higher than drivers aged 20 and older. If your teen causes an accident without forgiveness, your entire household’s premiums increase, affecting every driver on your policy.

Accident forgiveness applied at the household level protects everyone. For parents managing multiple drivers, this coverage transforms an accident from a financial catastrophe into a manageable incident. You still pay the deductible, but you avoid the compounding effect of higher premiums across multiple policies or drivers on the same policy (which can easily exceed $500 to $1,000 per year).

Finding the Right Coverage for Your Household

The protection accident forgiveness offers depends entirely on your insurer’s specific rules and your state’s regulations. Some carriers make this coverage automatic for new customers, while others require you to purchase it as an add-on. Your household’s driving profile-whether you have teen drivers, multiple vehicles, or a history of violations-determines how valuable this coverage actually is. The next section walks you through how to compare coverage options across carriers and ask the right questions to confirm what your policy actually includes.

Selecting the Right Accident Forgiveness Coverage for Your Needs

Shopping for accident forgiveness means comparing not just the cost of the add-on but how each insurer’s specific rules align with your driving situation. The differences in accident forgiveness programs across carriers are substantial enough to affect your long-term costs significantly. Progressive automatically includes small accident forgiveness for new customers in most states, covering claims up to $500 without a rate increase. Liberty Mutual requires five years of accident-free driving but applies that requirement across all carriers you’ve used, not just with them, which matters if you’ve switched companies in the past. GEICO charges extra for accident forgiveness unless you’ve already qualified through five years accident-free at age 21 or older. Allstate’s Platinum plan forgives immediately while Gold requires roughly three years clean, creating a pricing gap you need to evaluate against your household’s actual risk.

Availability and Cost Vary Across Arizona Carriers

Before comparing quotes, identify which carriers operate in Arizona and offer accident forgiveness without state restrictions. Arizona drivers have access to most major programs, unlike residents in California, Connecticut, and Massachusetts who face severe limitations. The cost varies dramatically-some insurers include it free for loyal customers, others charge $50 to $100 annually, and a few offer it only as a paid endorsement. Your deductible choice directly impacts whether accident forgiveness is worth purchasing. If you carry a $500 deductible and file a claim, you pay that out of pocket regardless of forgiveness coverage. Progressive’s small accident forgiveness only protects claims up to $500, meaning a $600 accident wouldn’t qualify, and you’d face both a deductible and a rate increase.

How Deductibles Affect Your Decision

Choosing a $1,000 deductible lowers your monthly premium but makes accident forgiveness more valuable because the financial hit from one accident grows larger. Conversely, a $250 deductible means your monthly costs are higher, but accident forgiveness becomes less critical financially since your immediate out-of-pocket expense is already lower. The relationship between deductible and forgiveness coverage determines your actual protection level. A high deductible paired with accident forgiveness shields you from rate increases on larger claims. A low deductible without forgiveness leaves you vulnerable to premium spikes that compound your financial exposure.

Three Questions to Ask Before You Commit

Ask your agent three specific questions before committing to any policy. First, does accident forgiveness apply per policy or per driver, and how does that affect your household if multiple people drive? Liberty Mutual forgives the first accident for the entire household, but most carriers apply forgiveness per policy, meaning one forgiven accident is shared across all drivers on that policy. Second, what specific violations or incidents disqualify you from eligibility-a single speeding ticket eliminates coverage with some insurers, while others only care about at-fault accidents. Third, confirm the exact waiting period before you qualify and whether that period resets if you switch companies. If you’re 24 years old, some carriers won’t let you access accident forgiveness until age 25 or until you’ve been with them for a specific duration.

Teen Drivers and Household-Level Coverage

The National Highway Traffic Safety Administration reports drivers aged 16 to 19 have crash rates three times higher than drivers aged 20 and older, so households with teen drivers should prioritize accident forgiveness availability and household-level coverage. These details determine whether you’re actually protected when an accident happens. A household with multiple drivers faces compounded risk, making accident forgiveness that applies to the entire policy far more valuable than per-driver coverage. Teen drivers especially benefit from household-level forgiveness because their higher accident rates mean the coverage protects not just them but every driver on your policy.

Final Thoughts

One at-fault accident costs the average Arizona driver $845 per year in premium increases, totaling roughly $2,535 over three years according to The Zebra’s analysis of rate data from Quadrant Information Services and S&P Global. Auto insurance with accident forgiveness eliminates that financial penalty entirely and protects your rate at renewal. Whether you manage multiple drivers, have a teen driver who faces statistically three times higher crash rates than older drivers, or simply want protection against unpredictable situations on the road, this coverage removes years of financial consequences from a single incident.

Your deductible still applies when you file a claim, but your rate stays stable at renewal with accident forgiveness in place. This protection matters most for Arizona households with higher accident risk and for safe drivers who understand they cannot control every situation on the road. The real value lies in the stability and peace of mind that comes from knowing one mistake won’t trigger years of inflated premiums.

Contact Insurance Brokers of Arizona® to compare accident forgiveness options across our partnerships with over 40 reputable carriers. We help Arizona families and individuals find coverage that matches their specific needs and budget, answering the exact questions that matter about per-policy versus per-driver forgiveness, disqualifying violations, and how your deductible choice affects this coverage’s value. A personalized quote takes minutes and reveals exactly what protection costs and what it covers for your household.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.