New drivers face some of the highest auto insurance premiums on the road. Insurance companies view inexperience as a major risk factor, which means your rates will likely be significantly higher than seasoned drivers pay.

The good news? Low cost auto insurance for new drivers is absolutely achievable with the right strategy. We at Insurance Brokers of Arizona® have helped countless young drivers cut their premiums by hundreds of dollars annually through smart choices and comparison shopping.

Why New Drivers Pay So Much for Auto Insurance

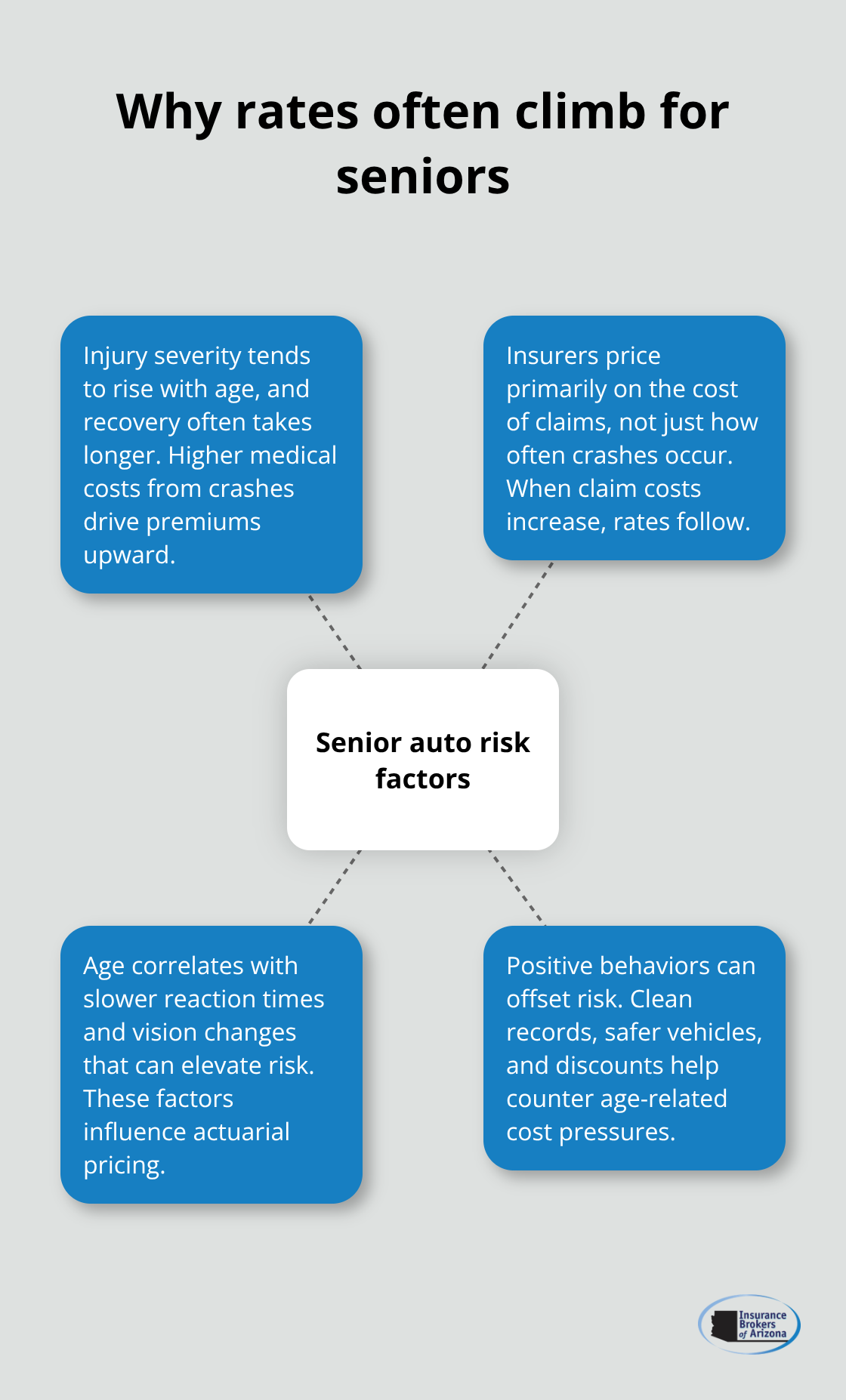

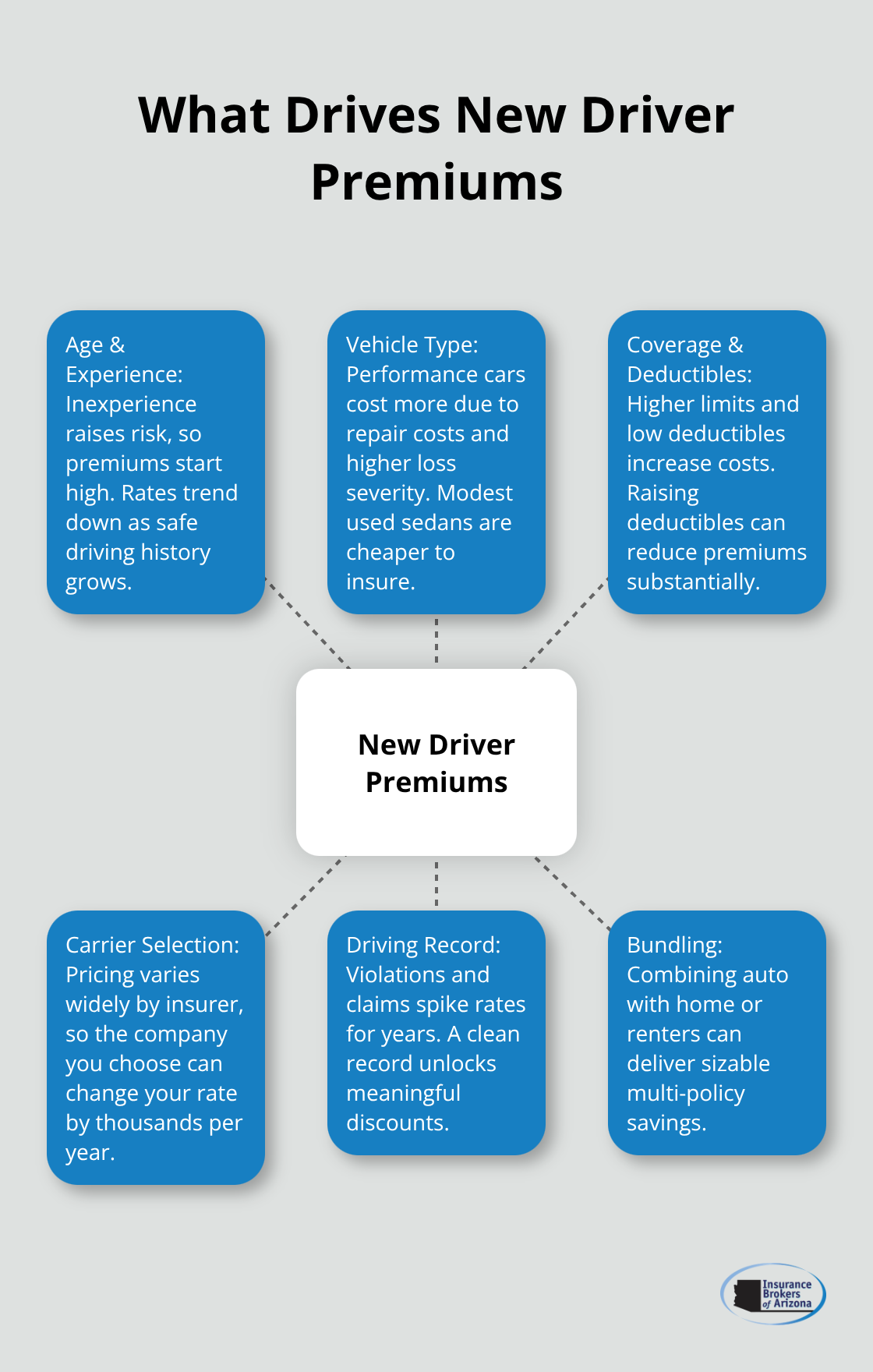

Insurance companies charge new drivers substantially more because inexperience correlates directly with accident risk. According to the Insurance Institute for Highway Safety and Highway Loss Data Institute, teen drivers are about three times more likely to be involved in a fatal crash than drivers aged 20 and over. This data comes from decades of claims history, not speculation. When you have zero or minimal driving history, insurers lack a track record to assess your actual risk level, so they apply higher premiums across the board. The national average cost to add a 16-year-old to a parent’s policy sits around $6,874 per year, though this varies significantly by carrier and location.

How Carriers Price Teen Drivers Differently

Some companies like Auto-Owners charge roughly $3,266 annually to add a teen, while others exceed $5,500. This 60 percent spread reveals that your choice of carrier matters as much as your driving habits. Auto-Owners and Erie are roughly 50 percent cheaper than the national average for adding a teen, making them strong options for cost-conscious families. Age plays a major role too: a 16-year-old typically costs more than a 20-year-old on the same policy because crash risk remains elevated through the late teens.

The Timeline for Rate Decreases

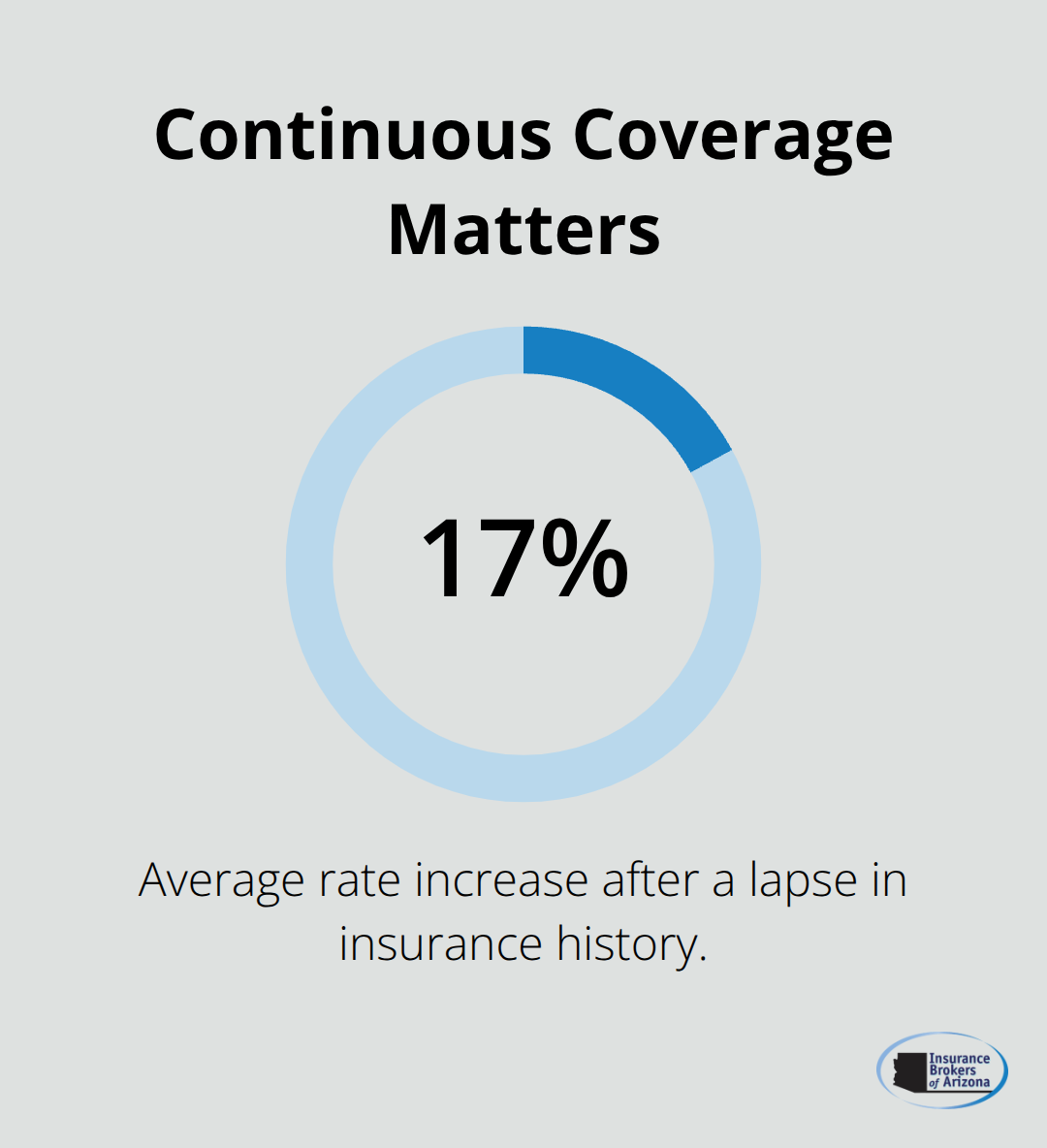

Your age and years holding a license directly impact your premium. A newly licensed adult in their twenties faces rates nearly as high as a teenager because insurers treat anyone without established driving history as a higher risk. Rates drop consistently as you age and maintain a clean record-most insurers see significant decreases by age 25, though some companies like Progressive offer drops as early as 19 for safe drivers. A lapse in coverage or insurance history can raise your rates by about 17 percent on average, so maintaining continuous coverage matters more than you might think.

Vehicle Choice and Premium Impact

The vehicle itself amplifies costs for new drivers. A high-performance car like a Dodge Challenger can push monthly premiums toward $1,200 or higher for a teen, while a used sedan keeps costs manageable. Shopping around reveals massive differences in pricing philosophy across the industry. Your next step involves understanding which discounts and coverage adjustments can offset these high baseline rates.

How to Cut Your Premiums as a New Driver

Compare Quotes Across Multiple Carriers

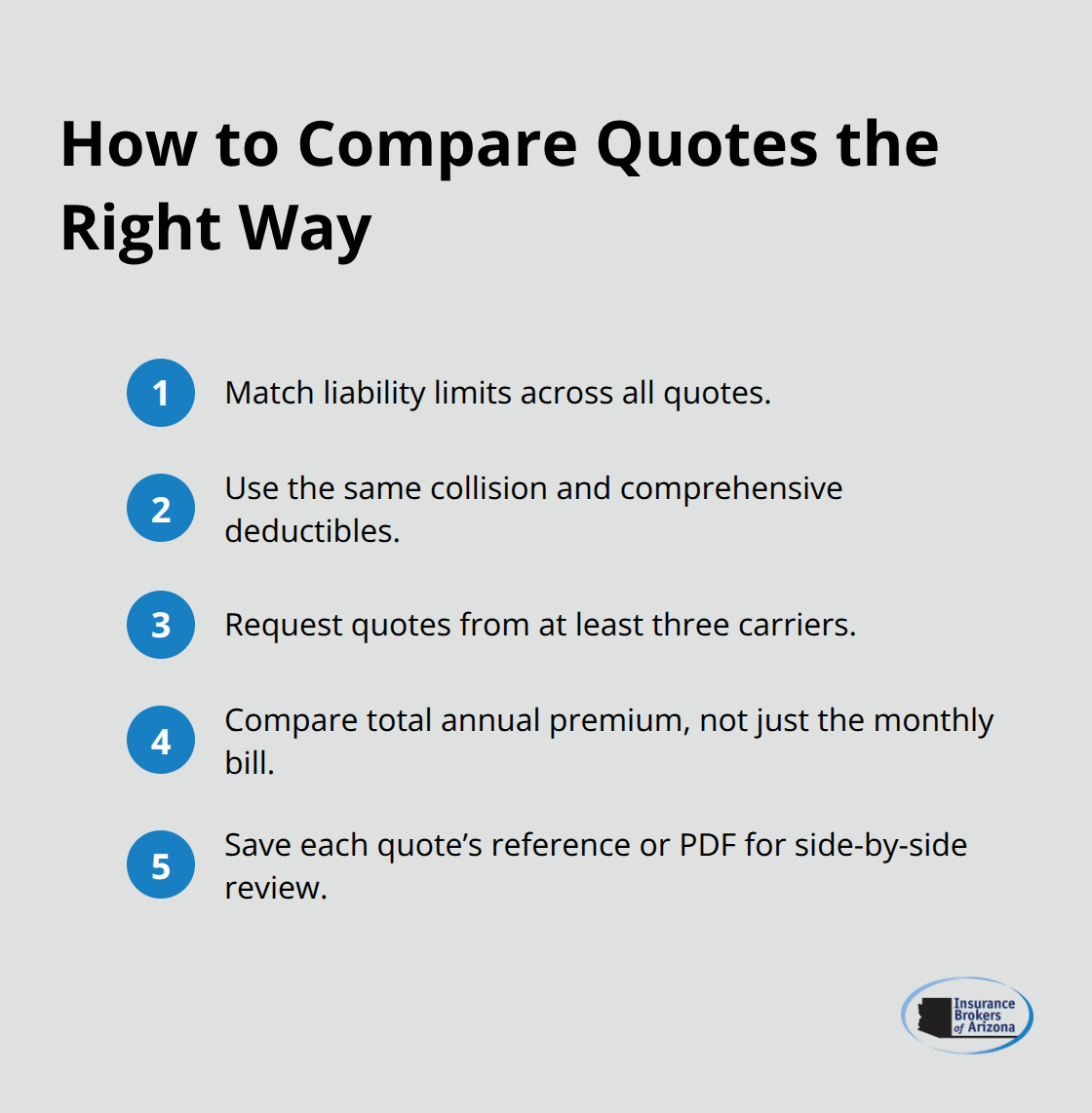

Comparing quotes from multiple insurers is non-negotiable if you want low costs. Auto-Owners, Erie, Geico, and State Farm price teen drivers differently based on their underwriting models, and the gaps are substantial. Adding a 16-year-old to Auto-Owners costs around $3,266 annually, while the same coverage at Geico runs about $5,507-a difference of $2,241 per year. You need to request quotes with identical coverage limits and deductibles to see apples-to-apples pricing instead of guessing which company offers the best deal. Most insurers offer free online quotes that take under five minutes, so you have no reason to settle with the first rate you receive.

When you request quotes, specify the exact same liability limits, collision deductible, and comprehensive deductible across all companies so the numbers actually mean something.

Stack Discounts to Reduce Your Base Rate

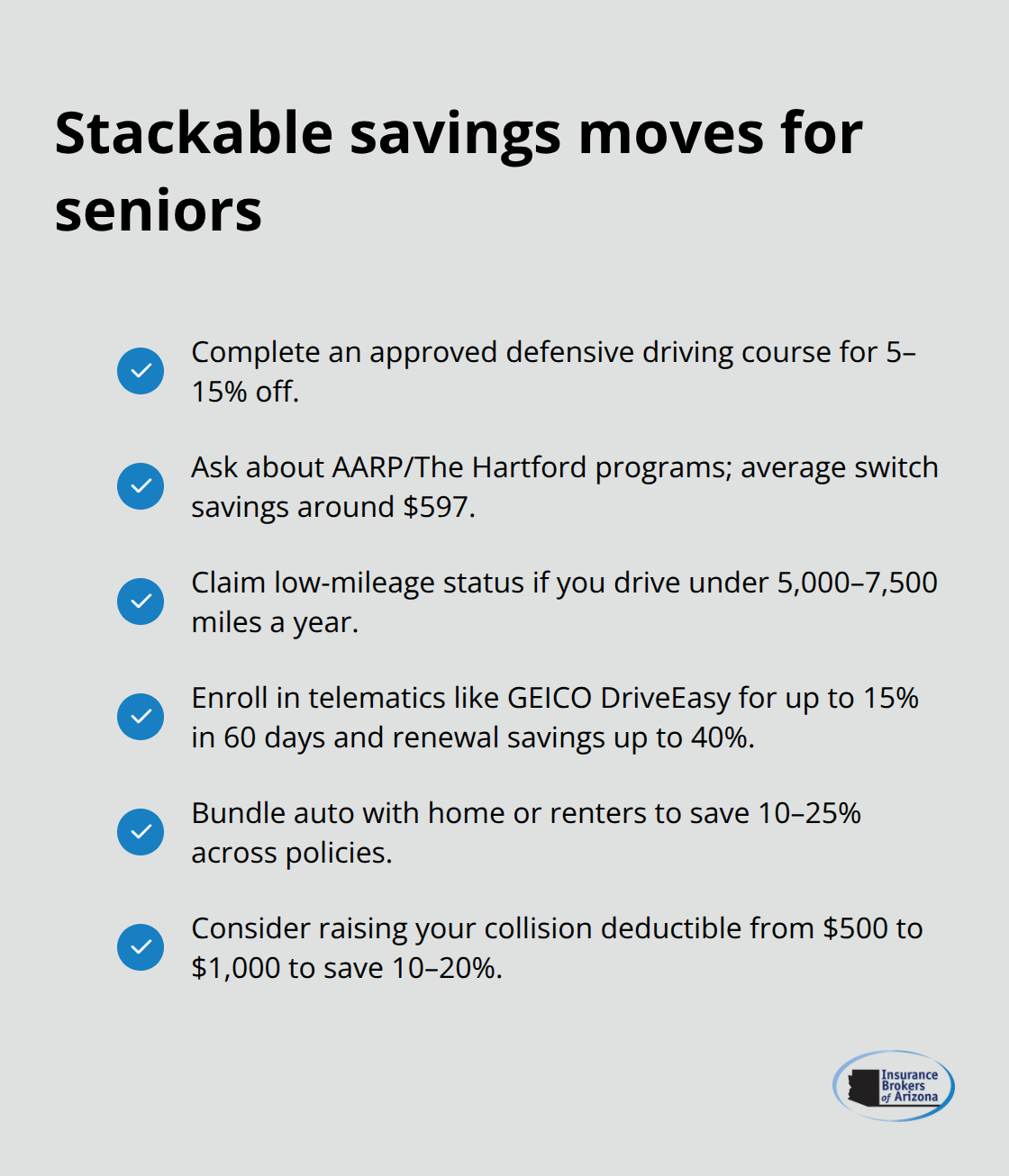

Discounts stack on top of your base rate, and new drivers qualify for several that others don’t. Good Student Discounts reward full-time students maintaining at least a B average and can cut premiums by around 15 percent according to industry data, though amounts vary by insurer and state. Completing a defensive driving course through an approved program often yields another 5 to 10 percent savings. Some insurers like State Farm offer Steer Clear, which combines driver training certification with ongoing discounts, while Auto-Owners provides teen monitoring through a mobile app that tracks driving habits. You should ask your insurer about all available discounts since eligibility can change by state or carrier.

Adjust Deductibles and Choose the Right Vehicle

Increasing your collision and comprehensive deductible from $250 to $1,000 typically saves roughly $440 per year on average, a direct reduction that requires no behavioral changes. The vehicle you drive matters far more than most new drivers realize: a used sedan costs significantly less to insure than a sports car or high-performance model because repair costs and theft risk are lower. You should obtain a quote before purchasing a vehicle to prevent the shock of discovering your dream car is unaffordable to insure. This step alone can save you thousands of dollars over the life of your ownership and helps you make an informed decision about which vehicle fits your budget.

How to Keep Your Rates Low as You Drive

Build a Clean Driving Record

A clean driving record is your most powerful rate-reduction tool over time. Traffic violations, accidents, and insurance claims all trigger rate increases that can persist for three to five years on your record. A single at-fault accident can raise your premiums by 25 to 40 percent depending on your insurer, while a speeding ticket typically adds 10 to 15 percent. The inverse is equally true: maintaining zero violations for three consecutive years often qualifies you for accident forgiveness programs or safe driver discounts that offset your new-driver penalty. Some insurers apply these discounts automatically once you hit the milestone, while others require you to request them. Every month without an incident moves you closer to substantially lower rates. Most insurers see measurable decreases by age 25, but your actual rate drop depends more on your driving history than your age alone. A 25-year-old with two accidents pays more than a 22-year-old with a spotless record, so your actions behind the wheel matter immediately.

Bundle Your Policies for Maximum Savings

Bundling home and auto insurance with the same carrier typically saves over $950 annually according to industry data, a discount that compounds your new-driver savings. Many insurers offer additional bundling discounts when you add renters, RV, or boat policies to the mix. Bundling simplifies policy management and gives you leverage to negotiate better rates during annual reviews. When your renewal notice arrives, contact your insurer and mention that you are considering switching to a competitor for bundled coverage. This statement alone often triggers a retention discount that reduces your quoted renewal rate by 5 to 15 percent.

Shop Annually and Switch When Necessary

Your rates should decrease as you age and gain experience, so shop competing quotes annually during your renewal window. If another carrier offers significantly lower pricing, switch without hesitation. Loyalty discounts rarely compensate for rate increases that accumulate when you stay put. Insurance Brokers of Arizona® can help you evaluate multiple carriers and bundling options simultaneously, ensuring you capture every available discount without the hassle of managing separate quote requests.

Final Thoughts

Finding low cost auto insurance for new drivers requires action, not hope. Start with quotes from at least three carriers using identical coverage limits and deductibles-the $2,000+ annual differences between Auto-Owners and Geico prove your choice of insurer directly impacts your wallet. Stack every discount you qualify for, increase your deductible to $1,000 if feasible (saving roughly $440 annually on average), and select a vehicle you can actually afford to insure before you purchase it.

Build your clean driving record from day one, since every month without a violation moves you closer to substantially lower rates. Bundle your auto policy with home or renters insurance to capture savings exceeding $950 per year, then shop annually during your renewal window to prevent overpaying for coverage. Most insurers apply significant discounts to drivers with spotless histories once they reach age 25, but your actual rate drop depends more on your driving history than your age alone.

We at Insurance Brokers of Arizona® work with over 40 reputable carriers, which means we compare pricing and discounts across the entire market without you spending hours on individual quote requests. Contact Insurance Brokers of Arizona® today to start your search for affordable coverage and let our team handle the comparison shopping so you get accurate, competitive quotes in minutes.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.