Builder Liability Insurance Arizona: What You Need to Know

Construction projects in Arizona come with real financial risks. One accident or defect claim can cost tens of thousands of dollars-or more.

Builder liability insurance in Arizona protects your business from these costly situations. We at Insurance Brokers of Arizona® help contractors understand their coverage options and find policies that match their actual project needs.

What Builder Liability Insurance Actually Covers

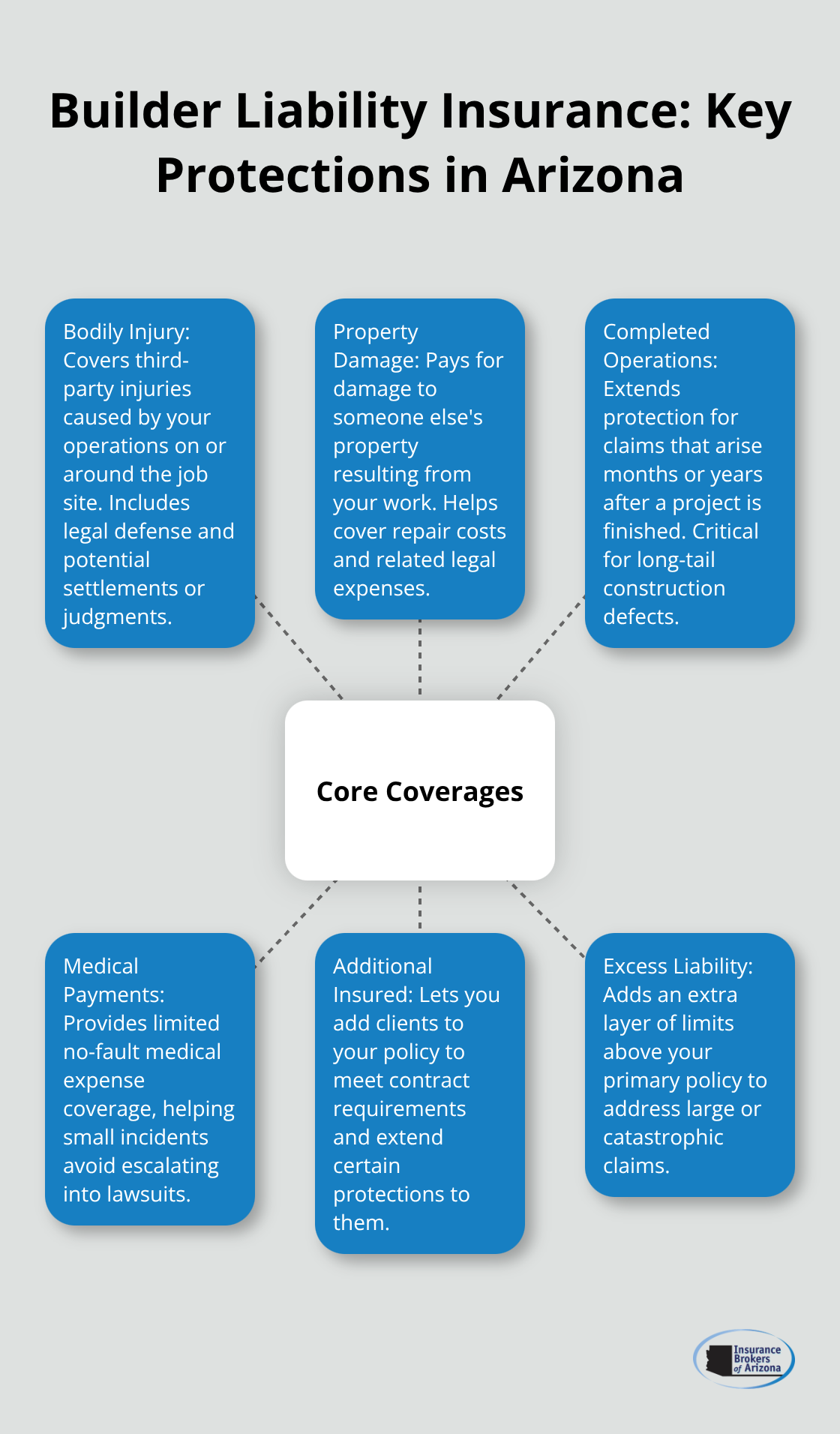

Builder liability insurance protects your business from third-party claims for bodily injury, property damage, and design defects that occur during or after your work. In Arizona, this coverage addresses the specific risks contractors face on job sites, from accidents involving workers and bystanders to claims about faulty workmanship that emerge months after project completion.

General liability policies typically include bodily injury coverage for injuries caused by your operations, property damage coverage for harm to someone else’s property, and completed operations coverage that extends protection for up to several years after you finish a project. Medical payments coverage on Arizona policies usually covers on-site medical expenses up to about $5,000, which can help prevent small injury claims from escalating into lawsuits. Arizona contractors commonly carry policy limits of $1 million per occurrence and $2 million aggregate, though larger commercial projects often demand $2 million per occurrence or higher. The state does not legally require general liability insurance to obtain a contractor’s license, but most clients will refuse to award you work without proof of coverage-this reality makes liability insurance non-negotiable if you want to win competitive bids.

Why Arizona’s Legal Framework Creates Liability Exposure

Arizona’s construction laws create specific liability exposure that standard business insurance won’t address. The Purchaser Dwelling Actions statute requires homeowners to notify contractors of defects and give them a chance to repair before filing a lawsuit, which means design and workmanship claims can surface years into the future and still fall within your liability window. Construction defect claims frequently involve issues like improper installation, material deficiencies, or design flaws that your completed operations coverage must handle. Payment disputes rank among the most common construction conflicts in Arizona, and the state’s Prompt Pay Act sets strict deadlines for payments between owners, contractors, and subcontractors-disputes over late payments can trigger counterclaims and liability exposure that your policy needs to address. Occurrence-based policies, which cover incidents during the policy period regardless of when claims are filed, are more common in Arizona than claims-made policies and offer better long-term protection for contractors. If you work on projects worth more than $1,000 or requiring a building permit, Arizona’s Registrar of Contractors requires a general contractor license, and most clients will ask for proof of liability insurance before work starts.

Matching Coverage Limits to Your Project Scope

Your liability limits should match your project scope and client expectations, not just match what competitors carry. A $500,000 limit might work for small residential repairs, but commercial clients and large residential projects typically demand $1 million or $2 million per occurrence. Premium audits after your policy period adjust your final premium based on actual payroll and expenses, so your initial estimate will shift once work concludes. Annual costs in Arizona vary significantly by trade, payroll, subcontractor costs, and location-a contractor with zero payroll pays roughly $790 to $1,050 annually, while one with payroll between $60,000 and $100,000 pays $1,338 to $2,934. If a standard policy’s limits aren’t enough for large claims, excess liability coverage adds an extra layer of protection beyond your base policy at flexible limits, which gives you protection without paying for higher limits on your primary policy. An additional insured endorsement lets you add clients to your coverage at no extra cost in most cases, and many clients require this before awarding contracts. You can receive an instant quote and start coverage the same day in Arizona, which means you won’t lose time between bidding and starting work.

What Comes Next in Your Coverage Strategy

Understanding what your policy covers and what limits you need sets the foundation for protecting your business. The next step involves identifying the specific claims that commonly arise on Arizona job sites and how your coverage responds to real-world scenarios that contractors face every day.

Common Claims That Hit Arizona Contractors

Property Damage Claims on Job Sites

Property damage claims strike Arizona contractors constantly. A dropped tool pierces a neighbor’s roof, scaffolding collapses into a parked car, or concrete spray damages adjacent structures. These incidents cost thousands in repairs and trigger third-party lawsuits that your liability policy must defend. The financial impact extends beyond the repair bill-legal defense costs, settlement negotiations, and potential judgments add up quickly. Your liability coverage protects you from paying these costs out of pocket, which means you stay operational while your insurer handles the claim.

Bodily Injury Claims From Accidents

Bodily injury claims follow property damage as a constant threat on Arizona job sites. A worker steps on an unsecured nail, a bystander gets hit by falling materials, or a subcontractor suffers injury due to unsafe conditions. These incidents create liability exposure that extends beyond workers’ compensation because third parties can sue your business directly. Medical expenses, lost wages, rehabilitation costs, and pain-and-suffering damages accumulate fast. Your liability policy covers these costs and provides legal defense, protecting your business from personal financial ruin when serious injuries occur.

Design Defects and Workmanship Claims

Design defects and workmanship claims represent the most insidious threat because they surface months or years after project completion. A roofing installation leaks after the first monsoon season, electrical work fails inspection, or framing cracks under load. These failures trigger claims years into the future, and your completed operations coverage must respond even if you’ve moved on to other projects. Arizona’s Purchaser Dwelling Actions statute amplifies this exposure-homeowners must notify you of defects and give you a reasonable opportunity to repair, but this window stretches years into the future. Claims filed within that window still fall under your liability exposure, making long-tail coverage essential for any contractor.

How Arizona’s Legal Framework Extends Your Liability Window

Real claims data shows that design and workmanship defects account for a substantial portion of construction liability payouts, particularly in residential work where material failures and installation errors create direct financial losses for owners. A $50,000 roofing repair, a $75,000 foundation correction, or a $100,000 electrical system overhaul can all trigger claims against your policy if the defect traces back to your work. Payment disputes compound this exposure significantly. When an owner withholds payment citing defects, counterclaims and disputes escalate quickly, and your liability coverage must defend you even if the dispute stems from legitimate quality disagreements. The Prompt Pay Act creates strict timelines that amplify tension between contractors and owners, and disputes over late payments frequently trigger cross-claims that involve your liability coverage.

Why Coverage Limits Matter More Than You Think

Contractors who carry only minimum coverage limits discover too late that a single major claim exhausts their protection, leaving them personally liable for amounts above their policy limits. A $1 million per occurrence limit works for mid-range residential and light commercial work, but larger commercial projects and high-value residential developments demand $2 million or higher per occurrence limits to match client requirements and protect against catastrophic losses. Your coverage limits must reflect your actual project scope and client expectations, not just what competitors carry. Understanding these three claim categories and how Arizona’s legal framework extends your liability window shapes the coverage strategy you need to protect your business. The next step involves assessing your specific project risks and selecting coverage limits that actually match your work.

How to Choose the Right Builder Liability Coverage for Your Arizona Business

Match Coverage Limits to Your Actual Client Requirements

Start by examining your actual contracts and client requirements rather than industry averages. Most Arizona commercial clients demand proof of $1 million per occurrence and $2 million aggregate coverage before awarding work, but high-value projects frequently require $2 million per occurrence or higher. Pull three recent contracts you’ve bid on and note the exact insurance requirements each client specified-this reveals whether your current limits create a competitive disadvantage. A contractor carrying $500,000 limits loses bids to competitors with $1 million coverage, even if the smaller limit technically covers the work scope.

Your deductible selection matters equally but receives less attention. A $1,000 deductible costs less upfront but means you absorb the first $1,000 of every claim, which adds up across multiple incidents. A $5,000 or $10,000 deductible reduces your annual premium by roughly 10 to 20 percent, depending on your trade and claims history, making it worthwhile if your cash flow handles occasional out-of-pocket costs. Arizona contractors with strong safety records and no prior claims often qualify for lower deductibles at competitive rates, so your claims history directly influences which deductible makes financial sense.

Evaluate Your Project Mix and Trade Classification

Evaluate your project mix realistically-residential remodeling work carries different risk profiles than commercial construction, and your coverage limits should reflect which type of work generates the majority of your revenue and exposure. Your trade classification affects both coverage availability and premium costs more dramatically than most contractors realize. Electricians, roofers, and HVAC contractors face different liability exposure than carpenters or concrete specialists, and carriers price policies accordingly based on injury frequency and claim severity data specific to each trade.

Request quotes from multiple carriers rather than accepting the first offer, as premium variations of 30 to 50 percent between carriers are common for identical coverage. Arizona’s market includes carriers willing to issue coverage the same day you apply, eliminating delays between contract award and project start.

Provide Accurate Information and Secure Endorsements

Provide accurate payroll figures and subcontractor costs during the quoting process, as underestimating these amounts triggers premium audits that increase your final bill after the policy period concludes. Request an additional insured endorsement on your policy before submitting certificates to clients-most carriers add this at no charge, and it satisfies client insurance requirements without additional cost. A Certificate of Insurance can be issued the same day your policy activates, allowing you to provide proof of coverage immediately after contract execution.

Insurance Brokers of Arizona® partners with over 40 reputable carriers, allowing us to secure competitive rates and coverage options tailored to your specific trade and project scope.

Final Thoughts

Builder liability insurance in Arizona protects your business from the financial devastation that a single claim can cause. You now understand what your coverage actually protects, how Arizona’s legal framework extends your liability exposure, and how to match your policy limits to your actual project scope and client requirements. The contractors who win competitive bids and protect their assets carry coverage that reflects their real work, not industry averages or competitor benchmarks.

Pull your recent contracts and identify the exact insurance requirements your clients demand, then compare those requirements against your current coverage limits and deductibles. If your limits fall short or your deductible doesn’t align with your cash flow, you lose bids or absorb unnecessary out-of-pocket costs. Request quotes from multiple carriers rather than accepting the first offer, as premium variations of 30 to 50 percent occur frequently for identical coverage in Arizona’s market.

Provide real payroll figures and subcontractor costs upfront to avoid premium audits that increase your final bill after the policy period concludes. Request an additional insured endorsement on your policy before submitting certificates to clients, and confirm that your carrier can issue a Certificate of Insurance the same day your policy activates. Insurance Brokers of Arizona® partners with over 40 reputable carriers to secure competitive rates and builder liability insurance Arizona options tailored to your specific trade and project scope.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.