Does Home Insurance Cover Fire Damage?

House fires devastate families across America every year, leaving homeowners wondering about their financial protection. Does home insurance cover fires? The answer affects millions of property owners nationwide.

We at Insurance Brokers of Arizona® see these questions daily from concerned homeowners. Understanding your fire coverage prevents costly surprises when disaster strikes.

What Does Home Insurance Actually Cover for Fire Damage

Standard homeowners insurance policies cover three major categories of fire damage, and the numbers show why this protection matters. Fire ranks as the second leading cause of homeowners insurance claims according to the Insurance Information Institute, with the average fire damage claim reaching $79,000 per the National Association of Insurance Commissioners.

Structural Damage Protection

Your dwelling coverage handles repairs to walls, ceilings, floors, and foundations that flames, smoke, or heat damage. This includes attached structures like garages and porches. Most policies also cover other structures on your property, such as detached sheds or fences, typically at 10% of your dwelling coverage amount. The key difference lies between replacement cost and actual cash value policies – replacement cost covers the full repair amount without depreciation, while actual cash value factors in wear and tear.

Personal Property Coverage

Personal property coverage protects your belongings inside the home, but standard policies limit certain items to $1,000-$2,500. Electronics face caps of $1,000-$2,000, while firearms get theft-only coverage up to $2,500. High-value items need scheduled property endorsements for full protection. Standard policies often fall short when homeowners lose valuable collections, jewelry, or expensive electronics in fires.

Additional Living Expenses

Additional living expenses coverage pays for temporary housing, meals, and relocation costs while contractors repair your home. This coverage typically ranges from 10-30% of your dwelling coverage and can last 12-24 months (depending on your policy terms). The National Fire Protection Association reports that U.S. fire departments respond to a fire every 24 seconds, making this temporary housing benefit essential for many families.

However, not all fire damage receives coverage, and certain exclusions can leave homeowners with significant out-of-pocket expenses.

What Fire Damage Gets Denied

Insurance companies deny fire damage claims more often than homeowners expect, and these exclusions can leave property owners with devastating financial losses. Claims face rejection when insurers suspect arson, find evidence of neglect, or discover business property mixed with personal belongings.

Arson and Intentional Fire Setting

Insurance fraud investigators examine every fire claim for signs of intentional fire setting. The Insurance Information Institute reports that insurers deny claims when they find accelerants, multiple ignition points, or suspicious circumstances around the fire. Homeowners face claim denials if family members deliberately start fires, even without the policyholder’s knowledge.

Insurance companies also reject claims when homeowners fail to cooperate with investigations or provide inconsistent statements about the fire’s origin. Documentation from fire department reports becomes critical evidence in these cases. Any indication of arson leads to automatic claim rejection plus potential criminal charges against the responsible parties.

Neglected Maintenance Issues

Electrical fires from faulty wiring that homeowners ignored for months get denied regularly. Insurance adjusters look for maintenance records and previous inspection reports to determine if negligence caused the fire. Policies exclude damage that results from the homeowner’s failure to maintain their property in reasonable condition.

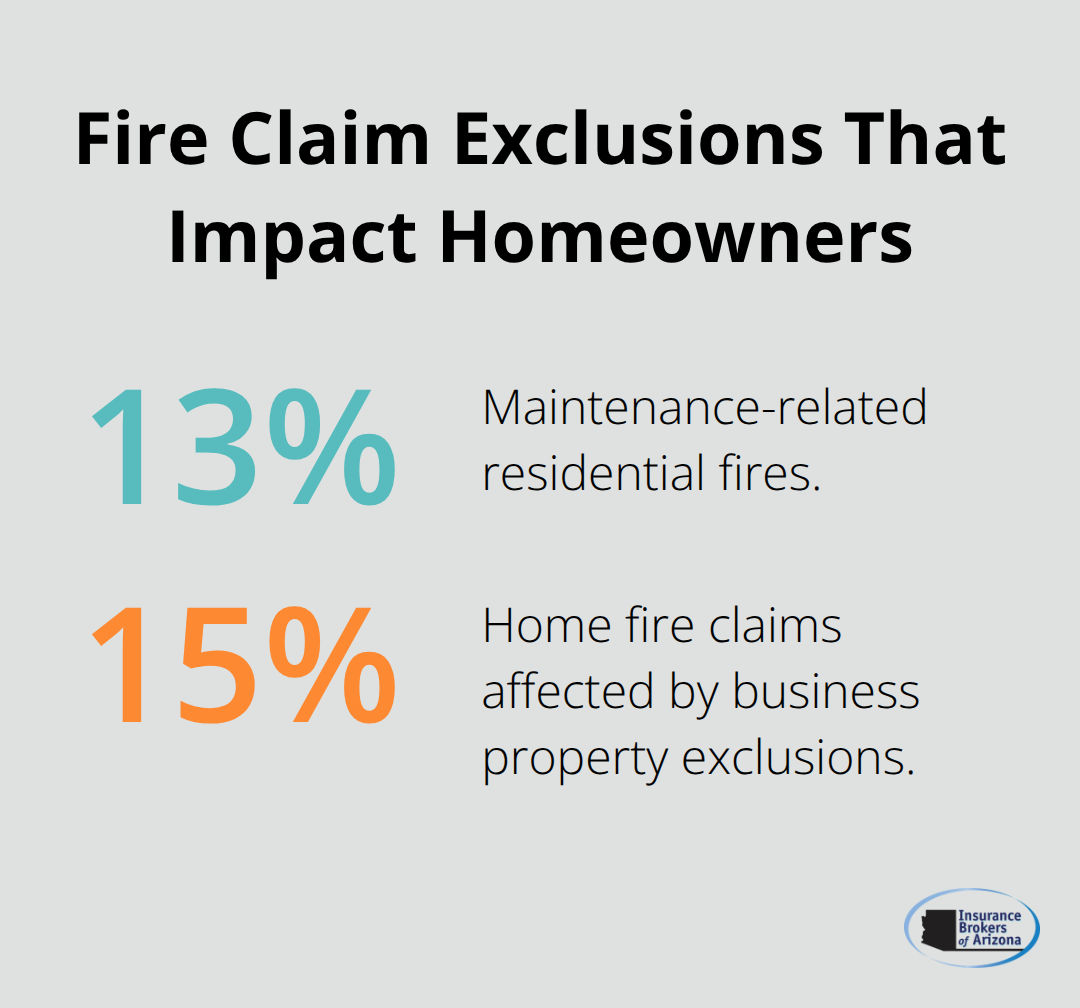

Smoke detectors with dead batteries, overloaded electrical circuits, and blocked chimney flues all represent maintenance issues that can void coverage. The National Fire Protection Association found that maintenance-related fires account for 13% of all residential fire incidents, yet these claims often face denial due to negligence clauses.

Business Property Exclusions

Home-based businesses face particular challenges because standard homeowners policies exclude business property from coverage. A home office computer worth $3,000 receives no compensation under personal property coverage if used primarily for business purposes. Professional equipment, inventory, and business documents require separate commercial coverage or specific endorsements to receive protection.

The National Association of Insurance Commissioners found that business property exclusions affect 15% of home fire claims. Even part-time business activities can trigger these exclusions, leaving entrepreneurs with significant uncompensated losses after fires.

Successful fire damage claims require proper documentation and prompt action, which makes the claims process your next priority after the flames are out.

How to File a Fire Damage Insurance Claim

Fire damage claims require immediate action to protect your financial interests and prevent further losses. The first 24 hours after a fire determine whether your claim gets approved quickly or faces months of delays.

Contact Your Insurance Company Immediately

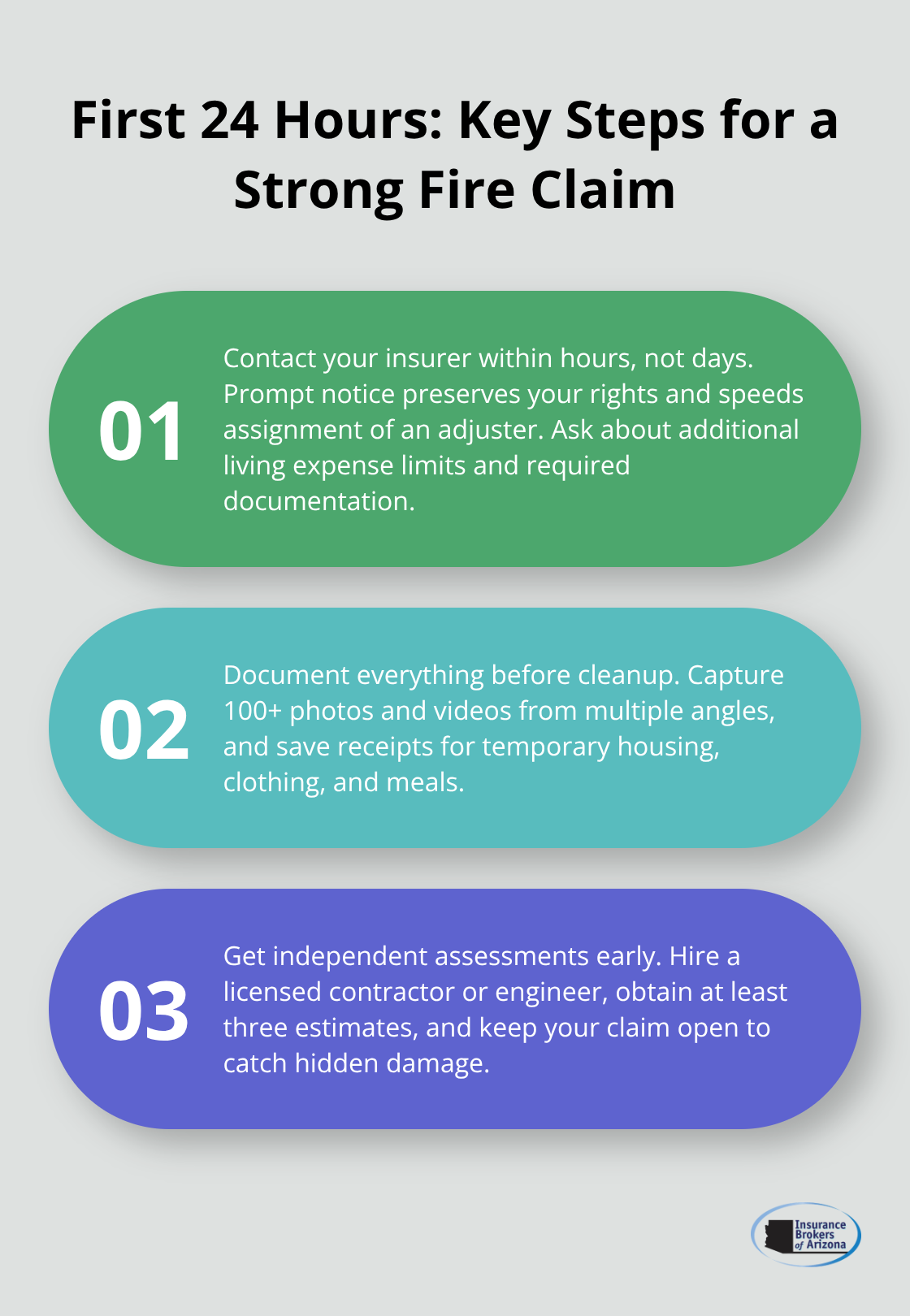

Call your insurance company within hours of the fire, not days later. Most policies require prompt notification, and delays can give insurers grounds to reduce or deny your claim. The National Fire Protection Association data shows that homeowners who report claims within 24 hours receive settlements 40% faster than those who wait longer.

Your insurance company will assign an adjuster and provide initial guidance on emergency expenses. Ask about your policy’s additional living expenses coverage limits and what documentation you need for reimbursement. Get your claim number and adjuster’s contact information during this first call.

Document Everything Before Cleanup Begins

Take extensive photos and videos of all damage before you touch anything or allow cleanup crews to start work. Insurance adjusters need visual evidence of the fire’s path, smoke patterns, and structural damage to process your claim accurately.

Photograph damaged personal property, burned areas, and water damage from firefighting efforts. The Insurance Information Institute recommends taking at least 100 photos from multiple angles to capture the full extent of damage. Save all receipts for emergency expenses like temporary housing, clothing, and meals (additional living expenses coverage reimburses these costs).

Professional fire damage restoration companies often arrive quickly, but never let them start work without documenting the scene first.

Get Multiple Professional Assessments

Insurance adjusters work for the insurance company, not for you, which creates an inherent conflict of interest in damage assessments. Hire your own licensed contractor or structural engineer to inspect hidden damage that adjusters might miss.

Professional inspections typically cost $500-$1,500 but can identify thousands of dollars in additional damage. The National Association of Insurance Commissioners reports that independent assessments find 25% more damage on average than insurance company estimates.

Obtain at least three repair estimates from licensed contractors to establish fair market pricing for restoration work. Keep your claim open for at least six months after initial settlement, as fire damage often reveals itself gradually through issues like foundation settling, electrical problems, or delayed smoke damage effects. Understanding home insurance terms helps you navigate the claims process more effectively.

Final Thoughts

Fire coverage forms the backbone of standard homeowners insurance policies across America. The Insurance Information Institute confirms that fire protection comes automatically with most policies, which makes it one of the most reliable forms of property protection available to homeowners. Does home insurance cover fires? Yes, but exclusions create significant gaps that catch homeowners off guard.

Arson investigations, maintenance neglect, and business property restrictions account for thousands of denied claims annually. The National Association of Insurance Commissioners data shows that homeowners who understand these exclusions prevent 60% of claim disputes before they start. Documentation separates successful claims from rejected ones (homeowners who photograph damage immediately and obtain independent assessments receive settlements averaging 25% higher than those who rely solely on insurance company evaluations).

We at Insurance Brokers of Arizona® help Arizona homeowners find policies that match their specific fire risk profile. Our experience shows that proper coverage selection and policy understanding make the difference between financial recovery and devastating loss after fires strike your property. The claims process rewards preparation and thorough record-keeping above all other factors.