How to Get New Venture Commercial Truck Insurance

Starting a trucking business requires navigating complex insurance requirements that can make or break your venture. New venture commercial truck insurance isn’t just a legal requirement-it’s your financial lifeline.

At Insurance Brokers of Arizona®, we’ve helped hundreds of trucking startups secure the right coverage at competitive rates. The process involves understanding DOT compliance, comparing carriers, and selecting coverage that protects your investment without breaking your budget.

What Insurance Requirements Must New Trucking Companies Meet?

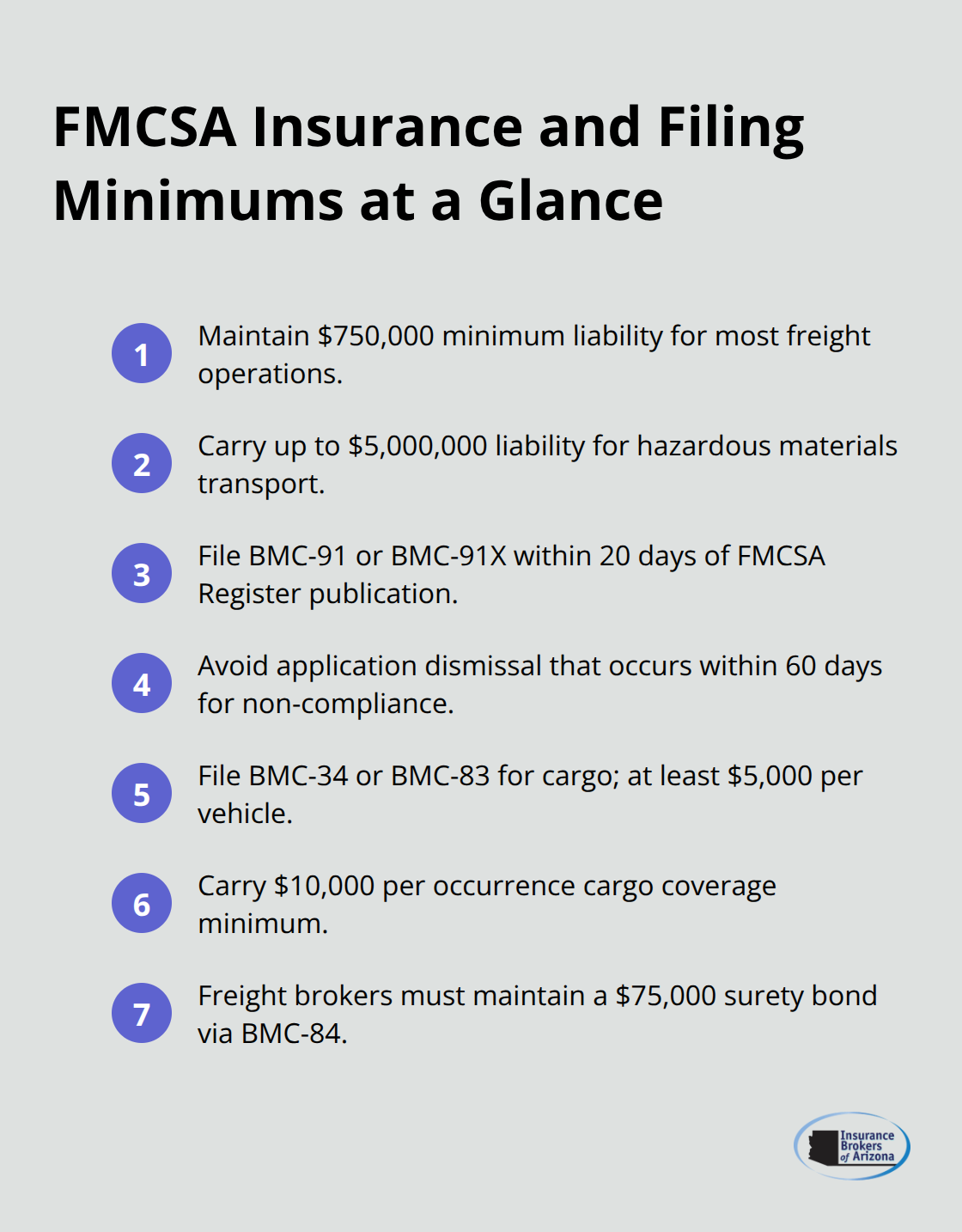

The Federal Motor Carrier Safety Administration mandates that new trucking ventures maintain minimum liability coverage of $750,000 for most freight operations, though this requirement increases to $5,000,000 for hazardous materials transport. Motor carriers must file BMC-91 or BMC-91X forms for public liability within 20 days of FMCSA Register publication. Companies that fail to comply face application dismissal within 60 days.

Cargo insurance requires BMC-34 or BMC-83 forms with mandatory coverage of $5,000 per vehicle and $10,000 per occurrence. Freight brokers need a $75,000 surety bond through BMC-84 forms to maintain their operating authority.

State Requirements Exceed Federal Minimums

Most states demand coverage above federal minimums, with many states requiring $1,000,000 in combined single limit liability. Arizona trucking companies face additional state requirements beyond federal compliance, which makes proper documentation management essential for maintaining operating authority.

New ventures that operate across state lines must meet the highest requirements of all states in their territory (not just their home state registration requirements). This multi-state compliance creates complex paperwork demands that catch many startups off guard.

New Companies Pay Premium Rates

New trucking companies pay significantly higher premiums during startup years due to lack of claims history. Some face 50-100% higher rates than established carriers with proven safety records. Limited insurance markets accept new ventures, which forces startups to work with specialized high-risk carriers that charge premium rates.

The average monthly cost for commercial truck insurance reached $746 for specialty truckers and $954 for transport truckers in 2024. New ventures typically pay above these averages due to their unproven track record.

Safety Technology Reduces Initial Costs

Smart startups invest in safety technology like dashcams and GPS systems before they apply for coverage. These tools demonstrate risk management commitment that can reduce initial premiums by 10-15% according to industry data. Electronic logging devices (ELDs) through programs like Smart Haul® provide average savings of $1,056 for participating truckers.

Companies that install comprehensive safety systems position themselves better when they shop for coverage. This preparation becomes even more important when you start the process of gathering documentation and comparing carriers.

How Do You Secure Your New Trucking Company’s Insurance Coverage?

Prepare Your Business Documentation Package

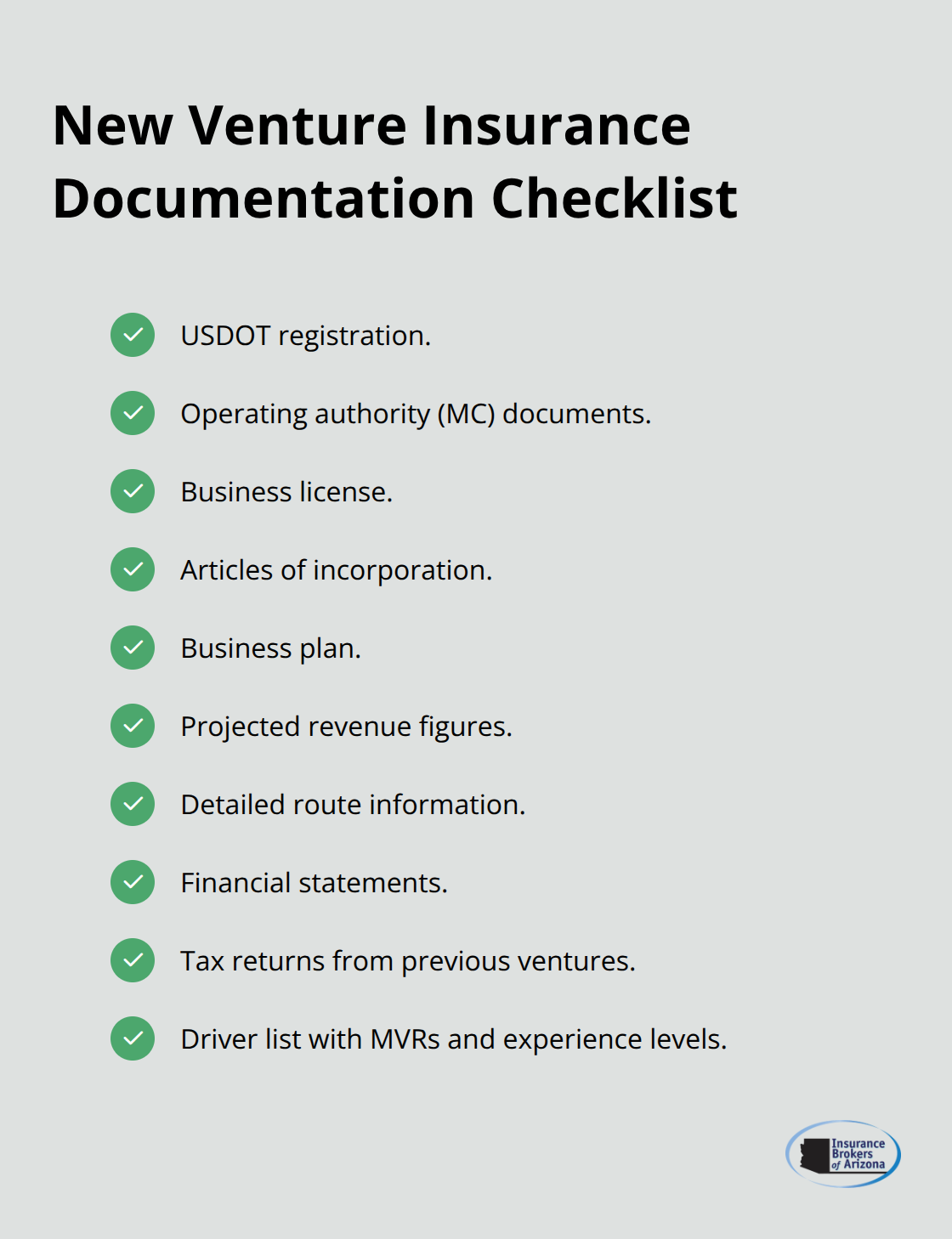

Your insurance application requires specific business documents that carriers use to assess risk and determine rates. Gather your USDOT registration, operating authority documents, business license, and articles of incorporation before you start the application process. Include your business plan, projected revenue figures, and detailed route information that shows where your trucks will operate.

Carriers want to see financial statements, tax returns from any previous business ventures, and a complete list of all drivers with their motor vehicle records and experience levels. Missing documentation delays approval and forces you to work with higher-priced carriers that accept incomplete applications.

Target Carriers That Specialize in New Ventures

Skip mainstream carriers that reject new ventures and focus on insurers that specialize in startup companies. Progressive Commercial, National General, and Canal Insurance accept new ventures but charge premium rates for unproven businesses. Request quotes from at least five specialized carriers since rates vary dramatically between companies for identical coverage.

Some carriers offer new venture programs with graduated rates that decrease after 12-24 months of claims-free operation. Compare not just premium costs but also payment plans, since annual payments can reduce total costs by over 13% compared to monthly installments (a significant savings for cash-strapped startups).

Work with Brokers Who Know Commercial Markets

Experienced commercial insurance brokers access multiple carriers through single applications and know which insurers accept new ventures. They understand the nuances between BMC requirements and can expedite the FMCSA registration process that new operators find complex. Professional brokers also negotiate better rates than individual applications since they represent multiple clients to each carrier.

The right broker relationship saves weeks of application time and often secures rates 15-20% lower than direct carrier applications for new ventures. This professional guidance becomes even more valuable when you need to understand the specific coverage types that protect your investment.

What Coverage Types Protect Your New Trucking Venture

Primary Liability Forms Your Insurance Foundation

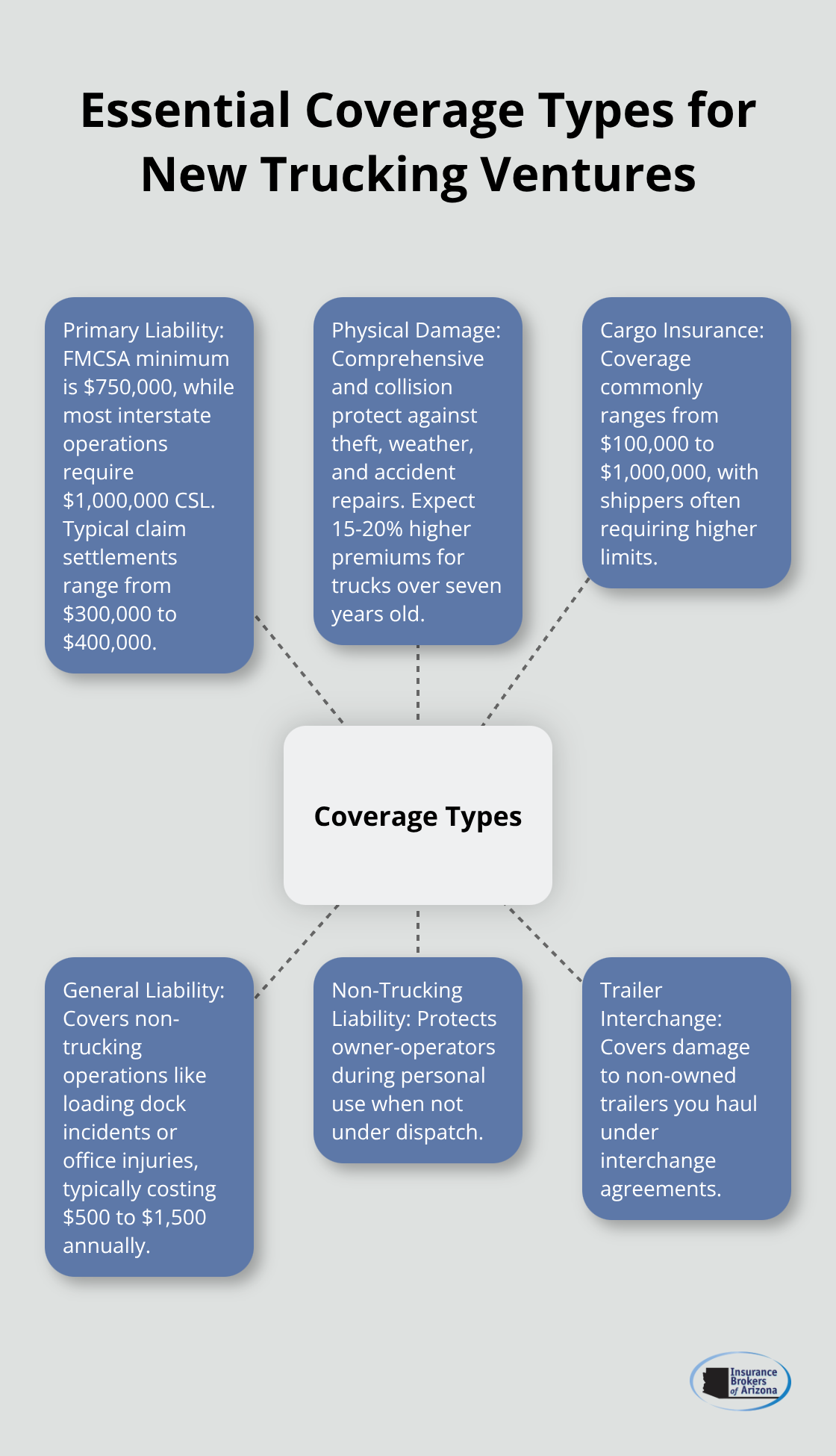

Primary liability coverage forms the foundation of your commercial truck insurance package and represents the largest portion of your premium budget. The FMCSA requires $750,000 minimum coverage, but most carriers demand $1,000,000 combined single limit for interstate operations. This coverage handles bodily injury and property damage claims when your drivers cause accidents, with average claim settlements now reaching $300,000 to $400,000 according to industry analyses.

Physical damage coverage protects your truck investment through comprehensive and collision protection. Comprehensive covers theft, vandalism, and weather damage while collision handles accident repairs. New trucks typically cost less to insure due to advanced safety features, but expect to pay 15-20% higher premiums for older equipment over seven years old.

Cargo Insurance Protects Your Freight Investment

Motor truck cargo insurance protects freight you transport with coverage that ranges from $100,000 to $1,000,000 (depending on cargo value and contract requirements). The BMC-34 filing requires minimum $5,000 per vehicle coverage, though most shippers demand much higher limits. Cargo type dramatically affects rates, with hazardous materials and high-value electronics commanding premium prices compared to standard freight loads.

General liability coverage protects against non-trucking business operations like loading dock accidents or office injuries. This coverage typically costs $500 to $1,500 annually but prevents devastating lawsuits from business activities that auto liability policies don’t cover.

Owner-Operators Need Specialized Coverage Options

Owner-operators require non-trucking liability coverage for personal use of commercial vehicles when not under dispatch. This coverage fills gaps when trucks are used for personal errands or deadheading without loads. Fleet operations skip this coverage since company trucks stay in commercial use exclusively.

Trailer interchange insurance becomes essential for owner-operators who pull trailers they don’t own, covering damage to borrowed equipment. Fleet operations often self-insure this exposure or negotiate coverage through trailer leasing agreements that transfer liability to the trailer owner.

Final Thoughts

New venture commercial truck insurance demands methodical preparation and professional guidance. Start with complete business documentation, understand DOT compliance requirements, and target carriers that accept startup operations. New companies face limited insurance markets and premium rates that exceed established carriers by 50-100%.

Safety technology investments before you apply for coverage demonstrate risk management commitment that reduces initial premiums. Electronic logging devices, dashcams, and GPS systems position your application favorably with underwriters who evaluate new ventures carefully. These tools show insurers that you take risk management seriously from day one.

Professional insurance brokers provide access to multiple specialized carriers through single applications and negotiate rates typically 15-20% lower than direct applications. They understand BMC requirements and expedite the complex FMCSA registration process that challenges new operators. We at Insurance Brokers of Arizona® help trucking startups navigate specialized insurance markets while protecting your investment with comprehensive coverage tailored to your specific operations.