Commercial auto insurance is one of the biggest expenses for any business with vehicles. At Insurance Brokers of Arizona®, we know that finding low cost commercial auto insurance doesn’t mean cutting corners on coverage.

This guide walks you through the real factors that drive your rates, proven strategies to reduce them, and how to compare quotes effectively.

What Actually Drives Your Commercial Auto Insurance Costs

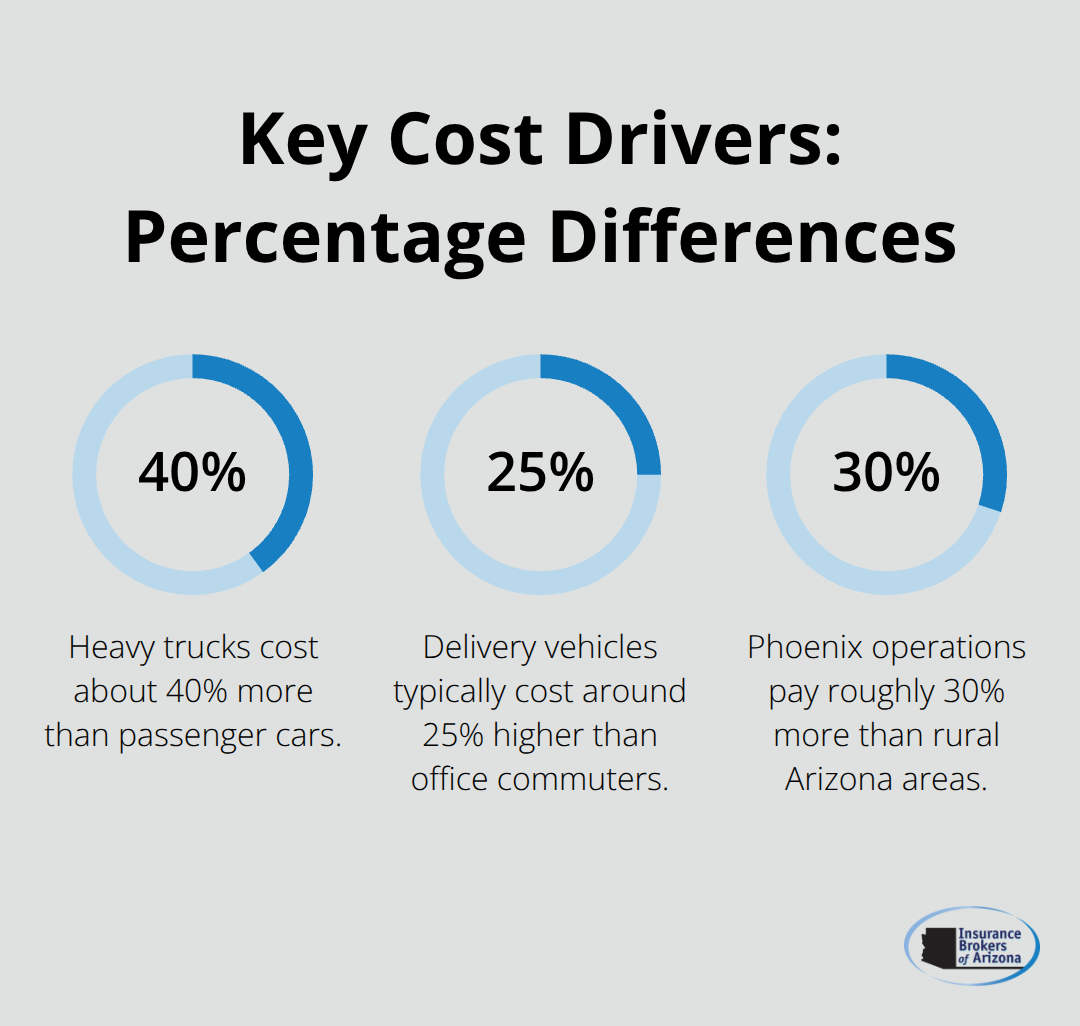

Vehicle type is the single biggest factor determining what you pay for commercial auto insurance, and it’s not even close. Heavy trucks cost about 40% more than passenger cars according to the Insurance Information Institute, while delivery vehicles typically cost around 25% higher than office commuters. If your operation uses a mix of vehicle types, this matters enormously for your budget. Switching from cargo vans to standard sedans for sales teams can save roughly $800 per vehicle annually, which adds up fast across a fleet.

Location compounds these costs dramatically. Phoenix operations pay roughly 30% more than rural Arizona areas, with some urban centers running twice the rates of smaller towns. Your drivers’ records are the next major lever. Clean driving records can reduce premiums by up to 35% according to the National Association of Insurance Commissioners, while a single accident within the last three years adds approximately $1,200 to your annual premium per incident. Drivers under 25 face premiums around 60% higher due to accident statistics.

Industry type also matters significantly. Construction and transportation businesses often face rates double those of professional services firms with identical coverage limits. These aren’t theoretical differences-they reflect actual claim history data that insurers use to price risk.

How Deductibles Shape Your Bottom Line

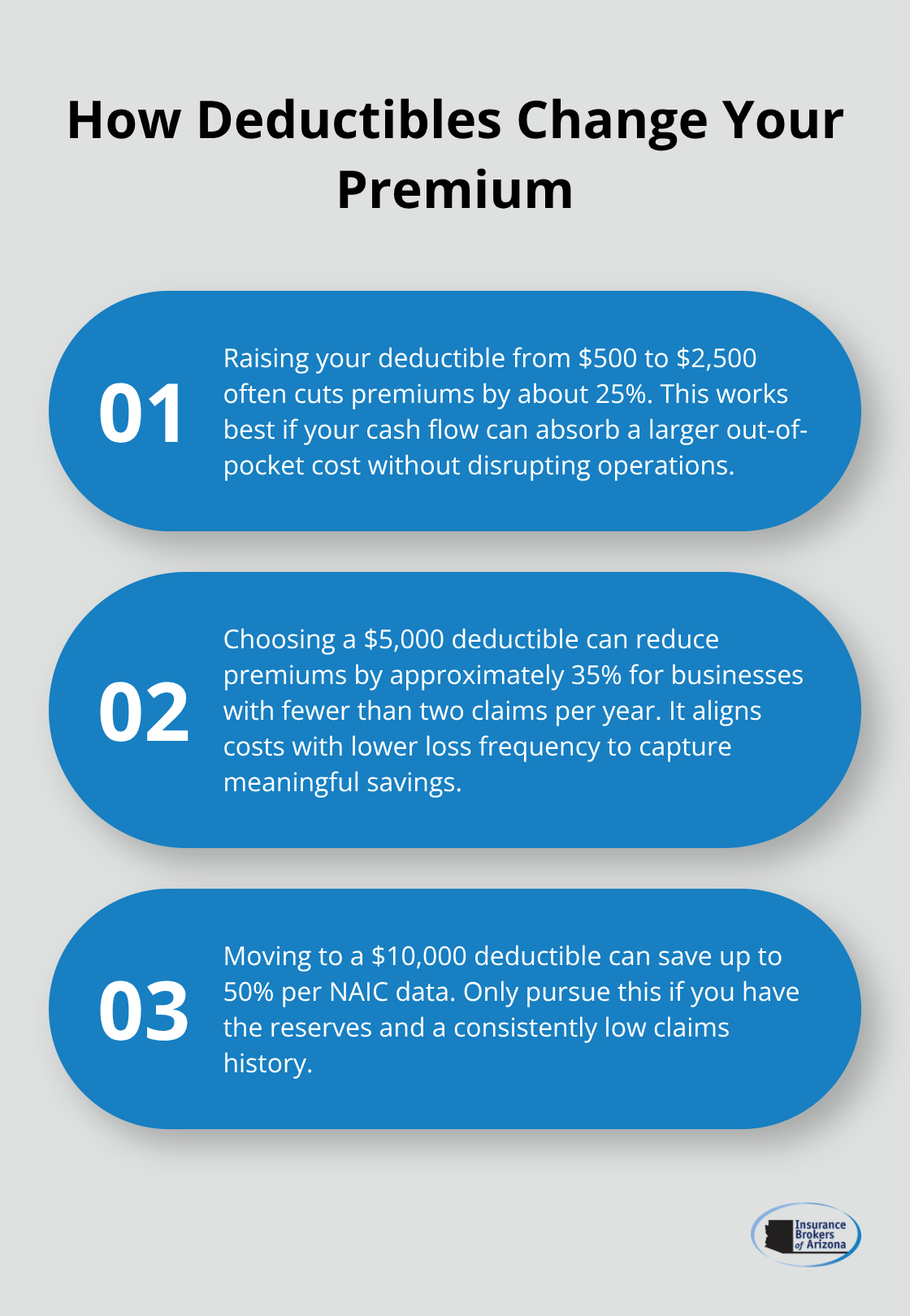

Raising your deductible from $500 to $2,500 typically cuts your premium by about 25%, making this one of the fastest ways to lower costs if your cash flow can handle larger out-of-pocket expenses. For businesses with fewer than two claims per year, raising deductibles to $5,000 can cut premiums approximately 35%, and going to $10,000 deductibles can save up to 50% according to NAIC data.

Most business owners keep low deductibles out of habit rather than analyzing their actual claim frequency. If your fleet goes three years without a claim, a higher deductible makes financial sense. Coverage limits also directly impact what you pay-minimum liability coverage runs around $400 yearly, while $1 million limits can reach about $2,800 per vehicle. The mistake here is choosing limits based on price rather than your actual exposure. A construction company hauling equipment faces vastly different liability risks than a consulting firm with a company car.

Where Telematics and Safety Programs Pay Off

Fleet tracking and telematics systems reduce accidents by approximately 30% and typically offer around 20% usage-based discounts according to industry data. GPS tracking costs roughly $30 per month per vehicle but can save approximately $400 annually in reduced premiums. Dash cameras reduce fraudulent claims by about 25%, protecting you from false damage claims.

Driver safety programs deliver rapid results. FMCSA data show accident rates drop about 40% in the first year after implementation. Monthly safety meetings cost roughly $200 per driver annually but yield about $1,500 in premium savings per vehicle. Training new hires with approximately 40 hours of structured instruction reduces first-year accidents by around 60%. Quarterly motor vehicle record checks reduce premiums by roughly 15% compared to annual checks, catching problem drivers faster and demonstrating your commitment to risk management to insurers.

The Real Cost of Inaction

These cost drivers don’t operate in isolation-they compound. A construction company in Phoenix with young drivers and low deductibles pays substantially more than an identical operation in rural Arizona with experienced drivers and higher deductibles. The gap between what you pay and what you could pay often reaches 30% or more when you account for all these factors together.

This is where shopping across multiple carriers becomes essential. Quotes from at least five carriers often show price differences of 40% or more for identical coverage. Progressive might quote $3,200 while State Farm quotes $2,100 for the same limits-that’s $1,100 in annual savings from a single comparison. Regional insurers frequently beat national carriers by 15% to 25% for local Arizona businesses, which means your location advantage can work in your favor if you know where to look.

How to Actually Cut Your Commercial Auto Insurance Costs

Bundle Policies to Stack Discounts Across Coverage Types

Bundling policies with a single carrier cuts what you pay faster than almost any other strategy, and the savings compound significantly. Bundling commercial auto with general liability and property coverage generates around 12% in discounts, but bundling five policies with one carrier boosts savings to approximately 18% according to industry data. Most businesses treat their commercial auto policy as a standalone expense when they could stack discounts across multiple coverages. The math works clearly: if your combined policies cost $10,000 annually, an 18% discount saves $1,800 per year. Carriers won’t advertise this aggressively, so you need to explicitly ask about multi-policy discounts when shopping. Some insurers structure their bundling to reward loyalty, meaning your renewal premium drops further if you’ve kept all policies with them for multiple years.

Manage Driver Records and Safety Programs for Measurable Rate Reductions

Your drivers’ records directly determine whether you qualify for the best rates available. A clean employee driving record reduces premiums by up to 25% compared with drivers carrying accidents or violations, and a claim-free history spanning three years can save as much as 30% on premiums according to the National Association of Insurance Commissioners. This isn’t just about hiring safer drivers-it’s about actively managing the ones you have. Quarterly motor vehicle record checks cost nothing and catch problems before they hit your renewal. Implement mandatory driver training for new hires with approximately 40 hours of structured instruction, which reduces first-year accidents by around 60%. Safety programs that include monthly meetings (averaging $200 per driver annually) generate about $1,500 in premium savings per vehicle through documented accident reduction. Install dash cameras and GPS tracking systems to deliver dual benefits: they reduce fraudulent claims by about 25% while providing the 20% usage-based discounts that many carriers now offer. GPS tracking costs roughly $30 monthly per vehicle but recovers that investment through approximately $400 in annual premium reductions. These aren’t optional add-ons for safety-conscious operations-they’re rate reduction tools that insurers actively reward because they demonstrably lower claims frequency by approximately 30%.

Strategic Deductible Selection Requires Honest Analysis of Your Claim History

The deductible conversation matters far more than most business owners realize. Raising your deductible from $500 to $2,500 cuts your premium by about 25%, but only if your cash reserves can absorb a larger out-of-pocket expense without operational strain. For businesses with fewer than two claims per year, NAIC data show that $5,000 deductibles cut premiums approximately 35%, and $10,000 deductibles can save up to 50%. Most owners choose a deductible based on what sounds manageable rather than analyzing their actual three-year claim history. If your fleet hasn’t filed a claim in three years, keeping a $500 deductible is financially irrational-you’re paying extra premium for protection you don’t need while carrying risk you could self-insure. The decision flips if your operation experiences regular claims. A construction company averaging one claim every two years should maintain lower deductibles because the premium savings from higher deductibles don’t offset the frequency of actual losses you’ll face.

Technology and Safety Programs Compound Savings Over Multiple Years

Fleet tracking and telematics systems reduce accidents by approximately 30% while offering around 20% usage-based discounts, making them among the highest-ROI investments in your insurance strategy. FMCSA data show accident rates drop about 40% in the first year after implementing structured safety programs, which means these tools pay for themselves through reduced premiums while simultaneously protecting your employees and assets. The combination of dash cameras, GPS tracking, and driver monitoring creates a documented safety record that insurers use to justify lower renewal rates year after year. This compounds over time: a business that implements these systems in year one sees immediate premium reductions, and those reductions deepen in year two and three as loss history improves. Carriers recognize that businesses investing in these technologies are serious about risk management, and they price accordingly. This separates operations that treat insurance as a line item to minimize from those that view it as a business optimization tool.

Once you’ve optimized your internal costs through bundling, driver management, and deductible strategy, the real savings emerge when you shop around and compare what different carriers actually charge for identical coverage.

How to Compare Quotes and Find Real Savings

Request Quotes from Multiple Carriers to Uncover Real Price Differences

Quotes from at least five carriers reveal price differences that reach 40% or more for identical coverage. Progressive might quote $3,200 while State Farm quotes $2,100 for the same limits-that’s $1,100 in annual savings from comparison shopping alone. Most business owners collect one or two quotes, assume they’re competitive, and move forward without realizing what they’re leaving on the table. Regional insurers beat national carriers by 15% to 25% for Arizona operations because they understand local risk factors better and carry less overhead than massive national companies.

Progressive currently offers the lowest average rates at around $293 monthly across all vehicle types according to MoneyGeek’s analysis, followed by The Hartford at $315 and Nationwide at $324. Your actual quote depends entirely on your specific industry, location, vehicle mix, and driver history. When you request quotes, provide identical information to each carrier within a 30-day window because rates change monthly and insurers adjust pricing constantly based on market conditions.

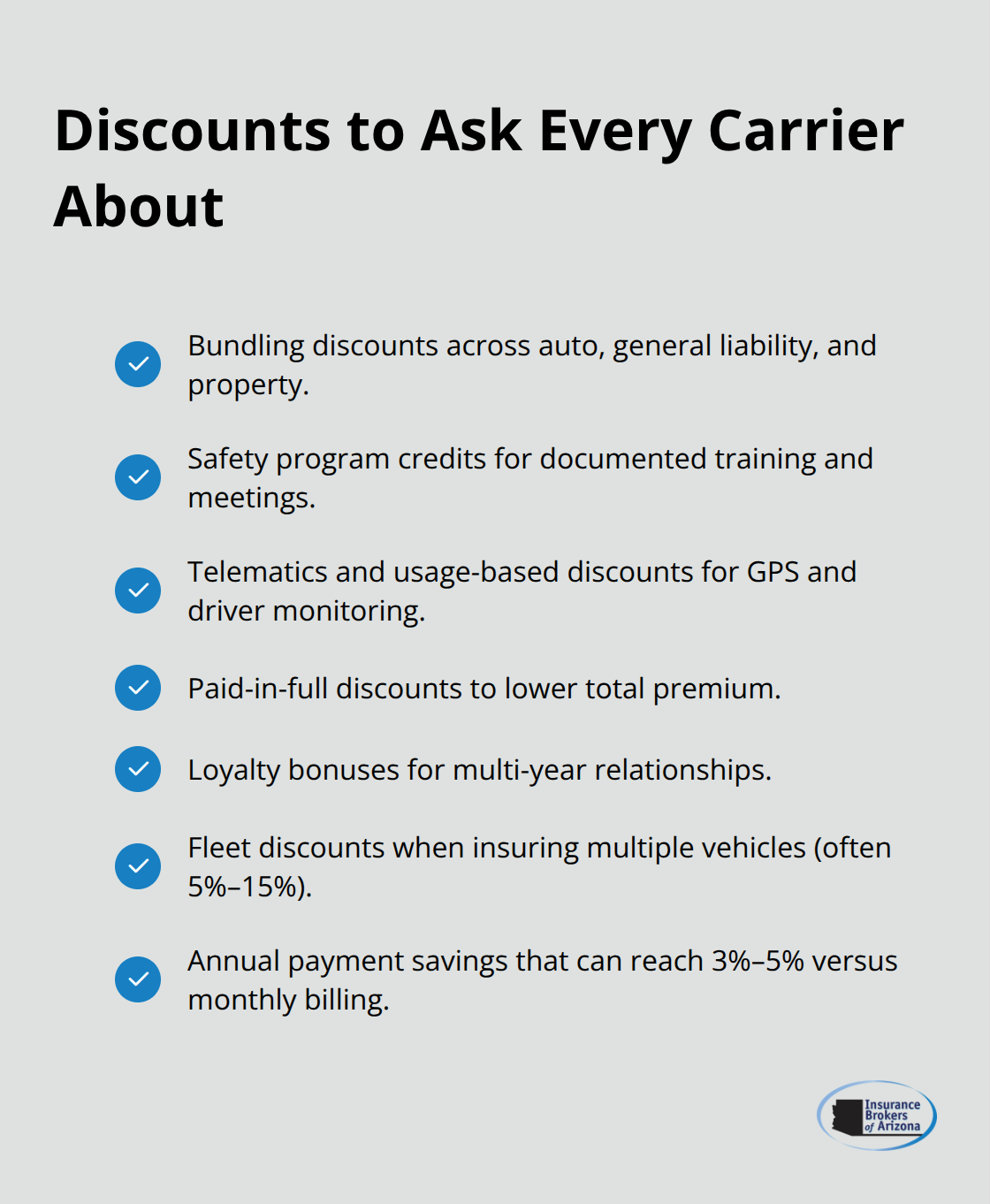

Extract Every Available Discount from Your Quotes

Carriers won’t volunteer their full discount structure, so you must explicitly ask about every reduction available: bundling discounts, safety program credits, telematics discounts, paid-in-full discounts, and loyalty bonuses. The difference between what you’re quoted and what you actually pay after discounts often reaches 15% to 20%, which means a carrier’s base quote doesn’t tell the full story.

Many businesses leave thousands on the table simply because they fail to ask what discounts apply to their specific operation.

Compare Coverage Specifications, Not Just Premium Amounts

Coverage limits and deductible combinations create enormous variation in what different carriers charge. Minimum liability coverage costs around $400 yearly while $1 million limits reach approximately $2,800 per vehicle, but comparing only the premium ignores whether each quote includes the same underlying coverage. State minimum liability costs substantially less than full coverage-Progressive’s state minimum averages $137 monthly versus full coverage around $354 monthly for identical vehicles.

Review what each quote actually covers: do collision and comprehensive apply, what medical payments limits exist, does the policy cover hired and non-owned vehicles if your operation uses rental equipment, and what’s the actual replacement cost versus actual cash value for physical damage? Some carriers structure their pricing to reward annual payment over monthly installments, saving 3% to 5% when you pay upfront rather than in monthly chunks. If you operate multiple vehicles, expect 5% to 15% fleet discounts versus insuring vehicles separately, though this varies dramatically by carrier.

Negotiate Terms Beyond the Initial Quote

Once you’ve collected five solid quotes with identical coverage specifications, the negotiation begins. Carriers often have flexibility on pricing, especially if you’re bundling multiple policies or committing to multi-year terms. Don’t accept the first quote as final; push back on rate increases at renewal, ask if new safety programs qualify for additional credits, and remind carriers of your clean claims history if applicable.

Insurance Brokers of Arizona® works with over 40 reputable carriers to access options that individual shopping never uncovers, providing access to regional specialists and niche carriers that often undercut national competitors by significant margins. This partnership approach expands your options far beyond what you’d find through direct carrier shopping.

Final Thoughts

Finding low cost commercial auto insurance requires three distinct actions working together. First, optimize your internal costs through policy bundling, driver record management, safety program implementation, and deductible selection based on your actual claim history. Second, request quotes from at least five carriers to uncover price differences that routinely reach 40% or more for identical coverage. Third, extract every available discount and negotiate terms beyond the initial quote before you commit.

The real savings emerge when you combine all three approaches. A construction company in Phoenix might reduce premiums by 25% through bundling and safety programs, then discover an additional 30% savings by comparing five carriers instead of two. That compounds to meaningful annual reductions that improve your bottom line year after year.

We at Insurance Brokers of Arizona® partner with over 40 reputable carriers to access options that individual shopping never uncovers, often revealing regional specialists and niche carriers that undercut national competitors by significant margins. Contact us to access competitive options tailored to your specific operation and secure the best rate available for your fleet.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.