Many homeowners think home insurance and home warranties are the same thing-they’re not. At Insurance Brokers of Arizona®, we see this confusion all the time, and it costs people money.

Home insurance protects against disasters like storms and theft. Home warranty covers appliance and system breakdowns. Understanding the difference between home warranty vs home insurance means you can protect your property properly.

What Home Insurance Actually Covers

Home insurance protects the physical structure of your home and your belongings from specific disasters. According to the Insurance Information Institute, homeowners insurance covers the dwelling itself, other structures on your property like sheds or detached garages, your personal belongings, and liability protection if someone gets hurt on your property. The policy pays for damage from covered perils such as fire, theft, windstorms, hail, and lightning. If a tree falls through your roof during a storm or a fire destroys your kitchen, homeowners insurance covers the repair or replacement costs after you pay your deductible. Most mortgage lenders require you to carry homeowners insurance as a condition of the loan.

How Much Homeowners Insurance Costs

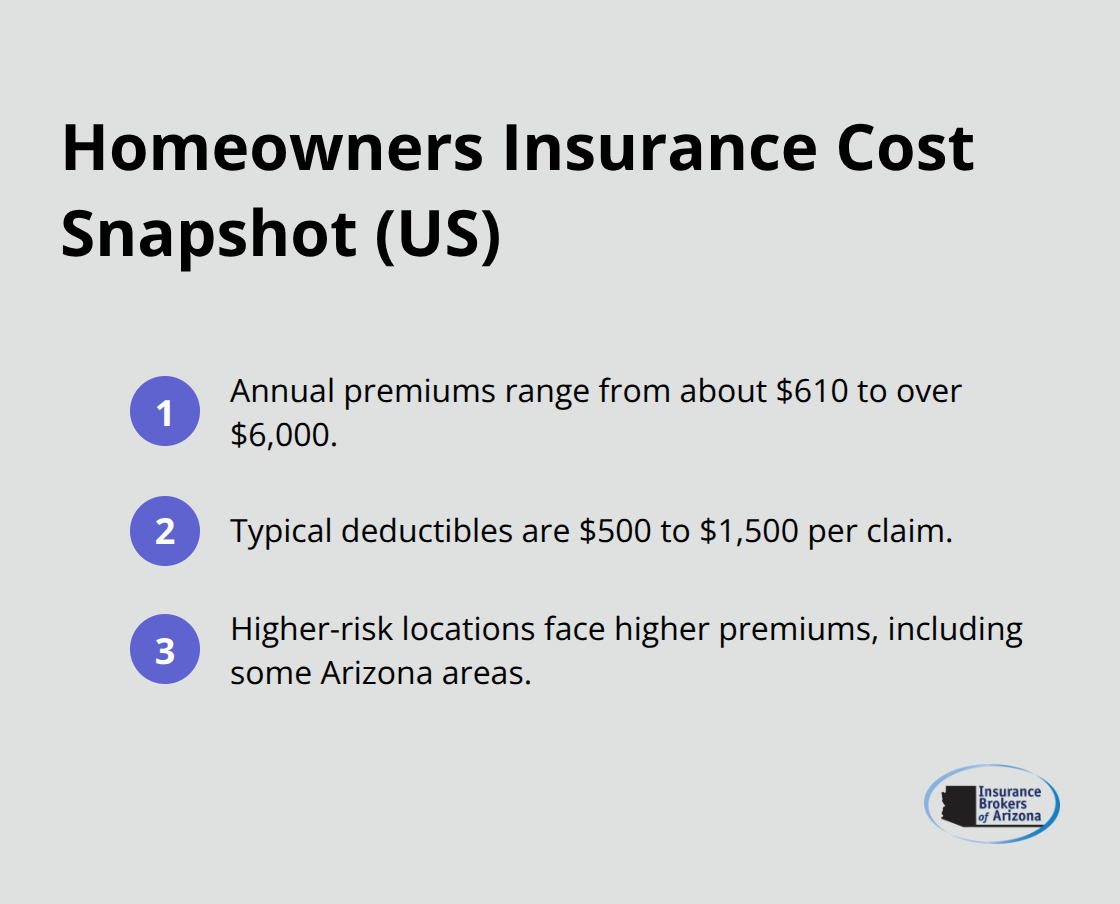

Your homeowners insurance premium depends on several factors including your home’s location, age, construction type, and the coverage limits you choose. According to NerdWallet, homeowners insurance costs range from roughly $610 to over $6,000 per year, with most policies including a deductible of $500 to $1,500. Homes in areas prone to severe weather or natural disasters cost more to insure. If you live in Arizona, your rates depend on your specific location since some areas face higher risks from monsoons or dust storms.

When disaster strikes, you pay your deductible first, then your insurance covers the rest up to your policy limits. If your home is destroyed in a fire, homeowners insurance pays for rebuilding costs, temporary housing through additional living expenses coverage, and replacing your belongings.

Liability Coverage Protects You From Lawsuits

Homeowners insurance includes liability coverage that protects you if someone gets injured on your property and sues you. If a guest slips on your icy driveway and breaks their leg, or a neighbor’s child falls from your deck and requires surgery, your liability coverage pays for their medical bills and legal fees up to your policy limit. Most policies include at least $100,000 in liability coverage, though you can increase this to $300,000 or more. Medical bills and legal judgments can exceed your home’s value, which makes this protection essential. Your homeowners insurance also covers damage your family members cause to other people’s property, such as accidentally breaking a neighbor’s window with a baseball or damaging their vehicle.

What Happens Without This Coverage

A single disaster can wipe out your financial security without homeowners insurance. Your home represents your largest investment, and one fire, flood, or major theft could leave you unable to rebuild or replace your belongings. Liability claims pose an even greater threat-a serious injury on your property could result in a judgment that exceeds your home’s value and follows you for years. This is why lenders make homeowners insurance non-negotiable for mortgaged properties. Now that you understand what homeowners insurance covers, you need to know how home warranties work differently and why many homeowners need both types of protection.

What Home Warranty Actually Covers

A home warranty covers what homeowners insurance refuses to touch: the slow death of your appliances and systems. When your air conditioner stops working in July or your water heater fails without warning, homeowners insurance won’t pay a dime. Home warranties exist specifically for these mechanical failures. According to the FTC, a home warranty commonly covers items like HVAC systems, plumbing, electrical systems, and major appliances for normal wear and tear. AHS, one of the largest warranty providers, reports paying $4 billion in home warranty claims over the last seven years, which shows just how often these breakdowns happen.

What You Pay for a Home Warranty

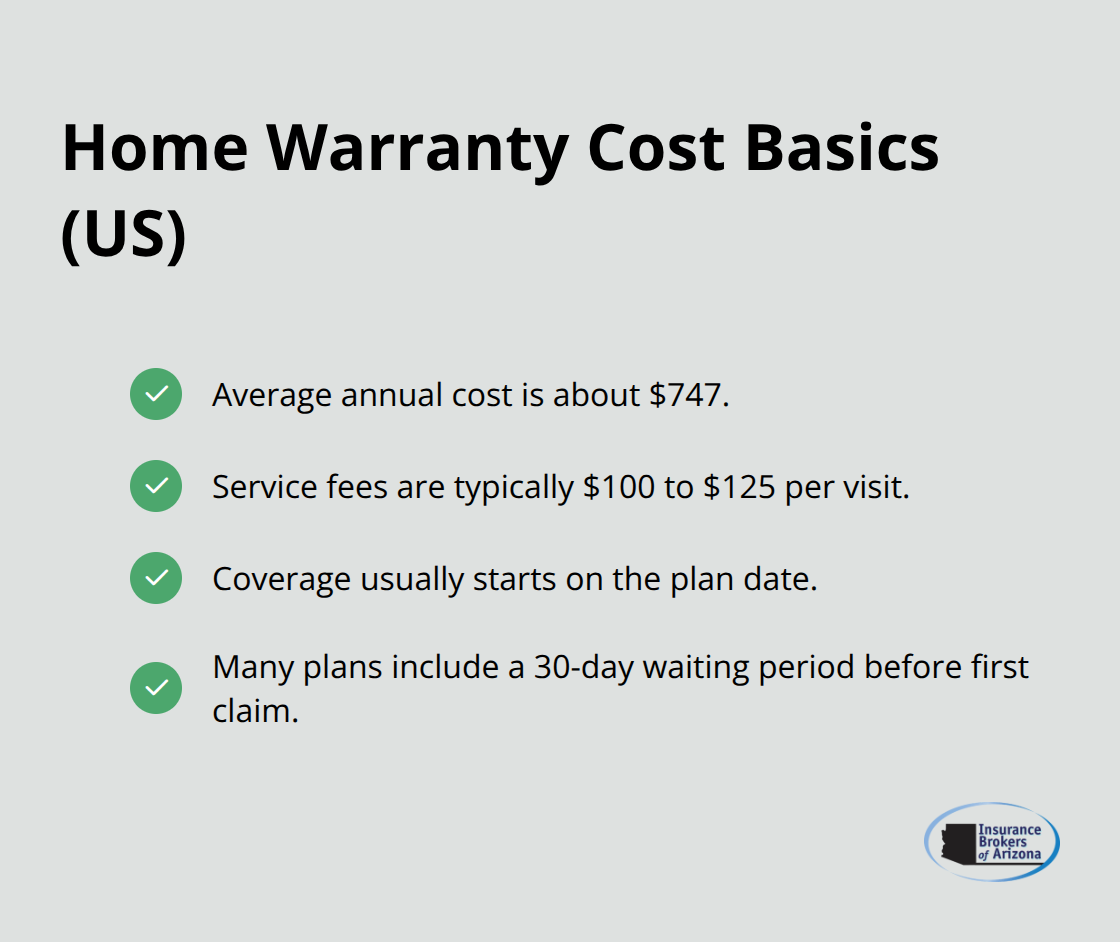

The average home warranty costs about $747 per year according to NerdWallet, plus you pay a service fee each time you call for repairs, typically between $100 and $125. This predictable cost structure makes budgeting easier than facing a $3,000 furnace replacement or $2,000 water heater emergency with no warning. Coverage typically starts on your plan date, though many plans include a 30-day waiting period before you can file your first claim.

Older appliances and systems receive coverage regardless of age, which matters significantly if you own an older home where systems fail more frequently.

How the Claims Process Works

When you file a claim, a technician from the warranty company’s network arrives at your home, diagnoses the problem, and either repairs or replaces the covered item. You pay your service fee upfront, and the warranty covers the rest. The real power of a home warranty shows up when your HVAC system fails at midnight or your main water line bursts on a holiday. You call 24/7, a technician gets assigned from a nationwide network of thousands of repair professionals, and your problem gets fixed that day or the next morning. This speed and convenience matter far more than the cost.

Where Home Warranty Fills the Gaps

Your homeowners insurance covers water damage if a pipe bursts, but it won’t cover the pipe repair itself. Your warranty covers the pipe repair. Your homeowners insurance covers fire damage to your kitchen, but it won’t cover your oven replacement. Your warranty covers the oven. This complementary relationship between the two types of coverage explains why many homeowners find both essential. Warranties typically exclude pre-existing conditions, cosmetic damage, and items not listed in your contract, so read your agreement carefully before signing.

Deciding If a Warranty Makes Sense for Your Home

If you own a home built before 1980, systems and appliances fail more often, making a warranty investment logical. If you own a newer home with recently installed systems, a warranty might be less valuable. The decision depends on your home’s age, the condition of your major systems, and how much cash you have available for emergency repairs without financial stress. Understanding these differences between warranties and insurance sets the stage for examining the key distinctions that determine which coverage you actually need.

How Insurance and Warranties Differ in Practice

Different Triggers, Different Payouts

Home insurance and home warranties operate on completely different triggers, which means they pay for completely different problems. Insurance pays when something unexpected happens to your home-a fire, theft, storm damage, or liability claim. A warranty pays when something you own breaks down from normal use. This distinction matters enormously because it determines whether you receive payment or nothing at all.

If your dishwasher leaks and destroys your kitchen cabinets, homeowners insurance covers the water damage to the structure and cabinets, but your warranty covers the dishwasher itself. Without both, you lose money either way.

Cost Structures Work Completely Differently

The cost structures reflect these different purposes entirely. Homeowners insurance costs between $610 and $6,000 annually according to NerdWallet, with deductibles typically ranging from $500 to $1,500 per claim. Home warranties cost about $747 per year on average, but you pay an additional service fee of $100 to $125 each time a technician visits. This means a warranty visit for a broken refrigerator costs you $100 to $125 upfront, regardless of whether the repair takes an hour or a day. Insurance deductibles only apply when you file a claim, but warranty service fees apply every single time you request service. If you use your warranty twice annually, you pay $200 to $250 in service fees plus your annual premium-which could exceed $1,000 total. This matters significantly when you budget for home maintenance.

Speed Matters for Emergencies

When you call your warranty company, a technician from their network arrives within 24 to 48 hours in most cases, diagnoses the problem, and fixes or replaces the item on the spot. You pay your service fee, the warranty covers the rest, and you move forward. Insurance claims involve a longer process: you report the damage, an adjuster inspects your home, the company assesses coverage and deductibles, and payment arrives days or weeks later. For emergencies like a broken furnace in winter or a burst pipe, warranty service speed wins decisively. However, insurance claims often pay for larger losses. If a fire destroys your home, insurance covers rebuilding costs that can reach hundreds of thousands of dollars. A warranty covers individual appliance or system replacements capped at specific limits per item.

Insurance Handles Catastrophe, Warranties Handle Breakdowns

Insurance adjusters assess damage professionally and write checks for major losses. Warranty technicians fix what breaks, but they won’t rebuild your kitchen after a fire. The response time advantage of warranties-typically 24 to 48 hours versus days or weeks for insurance-makes them invaluable for urgent mechanical failures. But insurance protects your actual financial security when catastrophe strikes. A single disaster can wipe out your financial security without homeowners insurance, while a warranty protects you from the unexpected repair bills that insurance refuses to cover (like a $3,000 furnace replacement or $2,000 water heater emergency). Together, these two types of coverage create a complete protection strategy that addresses both catastrophic events and routine mechanical failures.

Final Thoughts

Home warranty vs home insurance isn’t a choice between one or the other-you need both types of coverage working together. Homeowners insurance protects your financial security when catastrophe strikes, covering fires, theft, and liability claims that can cost hundreds of thousands of dollars. Home warranties protect you from everyday mechanical failures that insurance refuses to cover, sending a technician to your home within 24 to 48 hours when your furnace dies or your water heater fails.

Your home’s age determines whether a warranty makes financial sense for your situation. Homes built before 1980 experience more frequent system and appliance failures, making a warranty investment logical and cost-effective. Newer homes with recently installed systems may not justify the annual warranty cost, but most homeowners still benefit from having both types of protection in place. Evaluate your HVAC system’s age, your water heater’s installation date, and whether you have cash reserves to handle a $2,000 emergency repair without financial stress.

We at Insurance Brokers of Arizona® help homeowners identify coverage gaps and build protection strategies that fit their specific needs. Contact us at insurancebrokersofaz.com to discuss your home’s protection strategy and get quotes on homeowners insurance that actually covers what matters to you.