Getting labeled as a high-risk driver can send your insurance premiums skyrocketing by 50% to 200% above standard rates. DUI convictions, multiple accidents, or serious traffic violations typically trigger this classification.

We at Insurance Brokers of Arizona® help drivers navigate the complex world of high risk driver auto insurance every day. The good news is that affordable coverage options exist, even for the riskiest drivers.

What Makes You a High Risk Driver

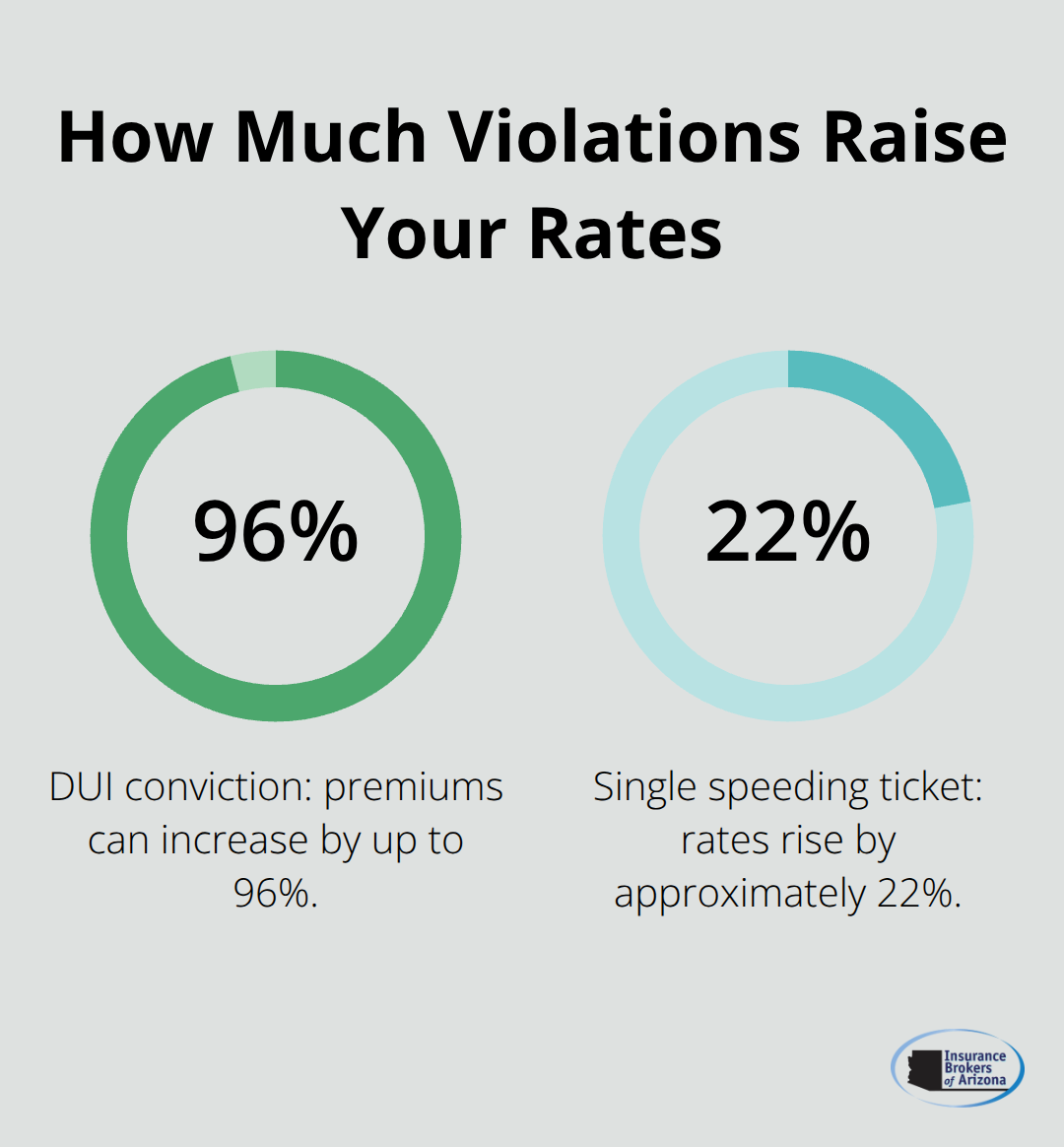

Insurance companies use statistical data to identify drivers who file claims more frequently than average. A DUI conviction increases your premiums by up to 96%, while a single speeding ticket raises rates by approximately 22% according to industry data. At-fault accidents, major violations like reckless driving, and lapses in coverage all trigger high-risk classification.

Poor credit scores also impact your rates significantly, though California, Hawaii, and Massachusetts prohibit this practice. Teen drivers and those with multiple violations within three years face the steepest increases.

How Insurers Calculate Your Risk Score

Insurers analyze your record over the past three to five years and weigh recent violations more heavily than older ones. They examine claim frequency, violation types, and coverage gaps to assign risk scores. Your age, location, and vehicle type also factor into their calculations. Companies like Progressive and Allstate use different criteria, which explains why rates vary dramatically between insurers. Some focus heavily on credit scores while others prioritize violations. This variation means you must shop multiple companies as a high-risk driver.

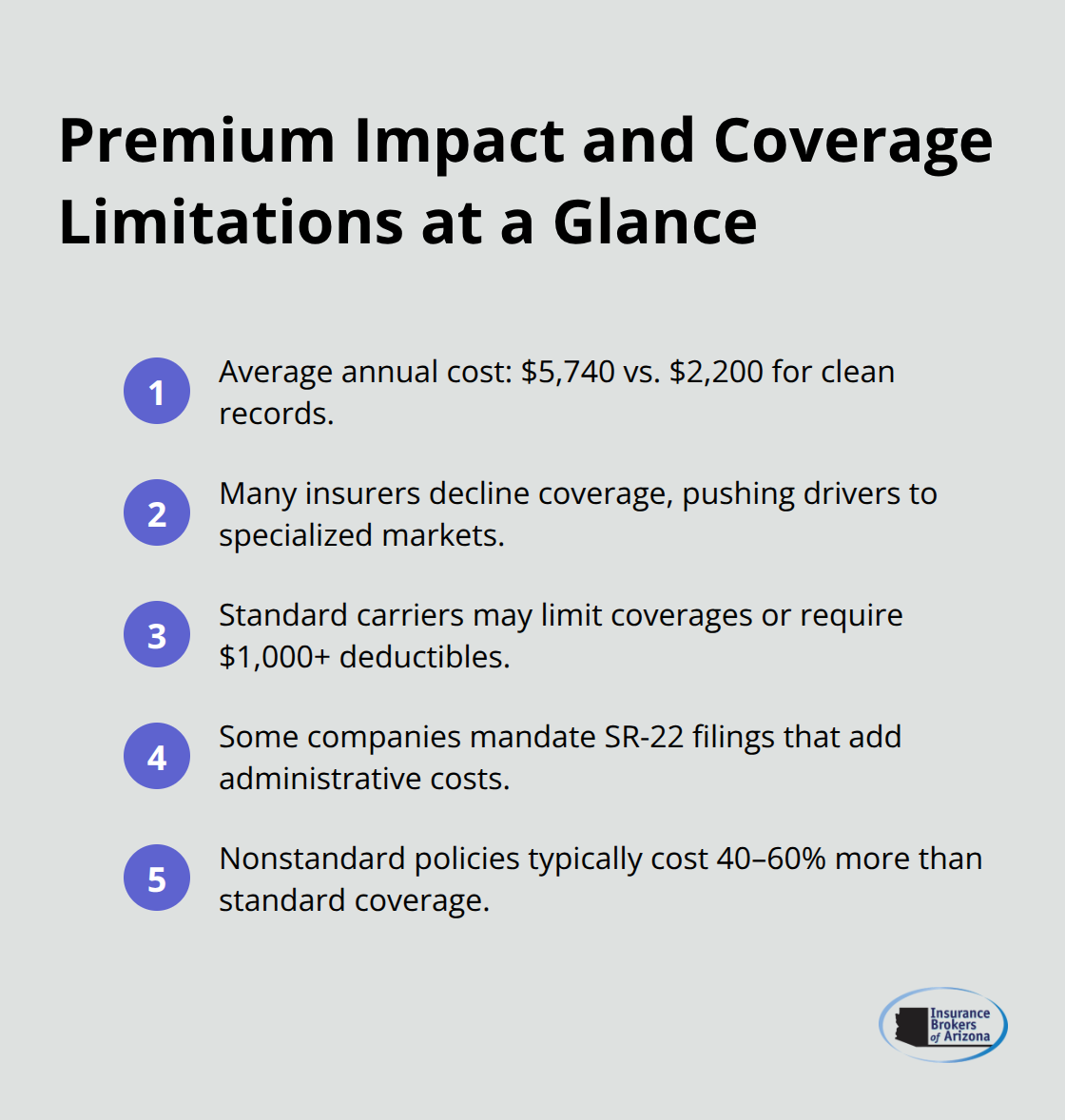

Premium Impact and Coverage Limitations

High-risk drivers pay an average of $5,740 annually for full coverage compared to $2,200 for clean-record drivers. Many insurers refuse coverage entirely and force high-risk drivers into specialized markets with fewer options. Standard insurers may offer limited coverage types or require higher deductibles (often $1,000 or more).

Some companies mandate SR-22 filings, which add administrative costs. The nonstandard insurance market specifically serves high-risk drivers but typically costs 40-60% more than standard coverage.

Timeline for Risk Status Changes

Your risk status typically improves after three violation-free years, which gradually lowers your premiums. Most violations remain on your record for three to five years, though DUIs may impact rates for up to seven years in some states. The length of time varies by violation type and state regulations. Major violations like reckless driving stay longer than minor speeding tickets (typically five years versus three years).

Now that you understand what triggers high-risk classification and how it affects your premiums, let’s explore where you can actually find affordable coverage options.

Where Can High Risk Drivers Actually Get Coverage

Specialized insurers like Progressive, Allstate, and Geico actively write policies for high-risk drivers when standard companies refuse coverage. Progressive stands out as it accepts drivers with DUIs and multiple at-fault accidents, often with rates 15-20% lower than competitors in the high-risk market. State Farm also writes policies for drivers with SR-22 requirements, though their rates typically run higher. The Acceptance Insurance Company specifically targets high-risk drivers and operates in 12 states, while Safe Auto focuses exclusively on minimum liability coverage for budget-conscious high-risk drivers. These companies use different criteria to evaluate risk, so rates can vary by 40-50% between carriers for identical coverage.

State Risk Pools Provide Last Resort Options

Every state maintains assigned risk pools or joint underwriting associations for drivers who cannot obtain coverage in the voluntary market. These programs require insurers that operate in the state to accept their share of high-risk drivers. Florida’s assigned risk plan covers over 900,000 drivers, while California’s plan serves approximately 200,000 policies annually (according to state insurance department data). Rates in these programs typically cost 25-35% more than voluntary market coverage, but they guarantee availability. Massachusetts operates a different system where companies must write policies for any licensed driver, which makes it easier to find coverage without the assigned risk pool.

Smart Tactics Cut Costs Significantly

Compare quotes from at least five insurers that specialize in high-risk coverage, as rates differ dramatically between companies. Request quotes for different deductible amounts – when you raise your collision deductible from $500 to $1,000, premiums can drop by 15-25%. Many high-risk insurers offer telematics programs that monitor behavior and provide discounts up to 30% for safe habits.

Bundle policies when possible, though high-risk drivers may find better deals when they split auto and home insurance between different companies. Apply for defensive course discounts, which can reduce premiums by 5-10% and remain active for three years in most states.

Once you secure coverage through these specialized options, you can take specific steps to improve your record and work toward standard rates again.

How Fast Can You Lower Your Premiums

Defensive courses provide the fastest path to premium reductions for high-risk drivers. These state-approved programs typically cost $50-150 and deliver 5-10% discounts that remain active for three years. The National Safety Council reports that drivers who complete defensive courses reduce their accident rates by 8-12% compared to those who skip this step. Traffic school completion also removes points from your record in 32 states, which directly impacts your risk score. Take courses immediately after violations since insurers apply discounts retroactively in most cases.

SR-22 Requirements Cost Less Than Expected

SR-22 certificates cost only $15-50 annually but require continuous liability coverage without any gaps. Your insurer files this form directly with your state’s DMV, and lapses trigger immediate license suspension. The requirement typically lasts three years from your conviction date (though some states extend this to five years for repeat DUI offenders). Allstate and Progressive both offer SR-22 assistance programs that simplify the process and send automatic renewal notices. Missing payments or switching insurers without transfer creates gaps that restart your three-year clock.

Your Record Improves Faster Than You Think

Most violations drop off your record after three years, with rates decreasing incrementally each year. Speeding tickets typically reduce premium impact by 25% after 12 months, 50% after 24 months, and disappear completely at 36 months according to Insurance Information Institute data. DUI convictions follow a longer timeline – rates drop 15% annually starting in year four and reach standard rates after seven years.

Risk Status Changes Open New Options

Your risk status officially changes from high-risk to standard when you maintain three consecutive violation-free years. This change opens access to competitive standard market rates that average 40-60% lower than specialized high-risk coverage. Standard insurers like State Farm and Geico become available again, often with better coverage options and lower deductibles than high-risk specialists offer.

Final Thoughts

High risk driver auto insurance doesn’t have to destroy your budget when you know where to look and how to improve your situation. The specialized market offers real solutions through companies like Progressive and Allstate, while state risk pools provide guaranteed coverage when other options fail. Your path forward starts with quotes from multiple high-risk specialists, since rates vary by 40-50% between carriers.

Take defensive courses immediately for quick discounts, maintain continuous coverage to avoid SR-22 complications, and know that most violations disappear after three years of clean habits. The transition from high-risk to standard coverage happens faster than most drivers expect. Within three violation-free years, you’ll access competitive rates that cost 40-60% less than specialized coverage (making every safe decision count toward significant long-term savings).

We at Insurance Brokers of Arizona® help drivers find competitive options for high-risk situations across Arizona. Our team works with multiple carriers to help you secure coverage today while you plan your path to better rates tomorrow. Contact us to explore your options and start your journey toward affordable auto insurance.