Vacant properties face unique insurance challenges that standard homeowners policies simply don’t address. Most insurers consider homes vacant after 30-60 days, automatically voiding coverage.

We at Insurance Brokers of Arizona® see property owners struggle with finding adequate vacant home insurance coverage. The right policy protects against vandalism, theft, and liability risks that empty properties attract.

What Makes Vacant Properties So Risky

The insurance industry draws a sharp line between vacant and unoccupied properties, and this difference determines whether your claim gets paid or denied. Vacant homes contain no personal belongings and remain completely empty, while unoccupied properties still have furniture, utilities, and the appearance that someone could return at any time. Standard homeowners insurance policies contain vacancy clauses that automatically suspend coverage after 30-60 days of vacancy, which leaves property owners exposed to significant financial losses.

Why Standard Policies Exclude Vacant Properties

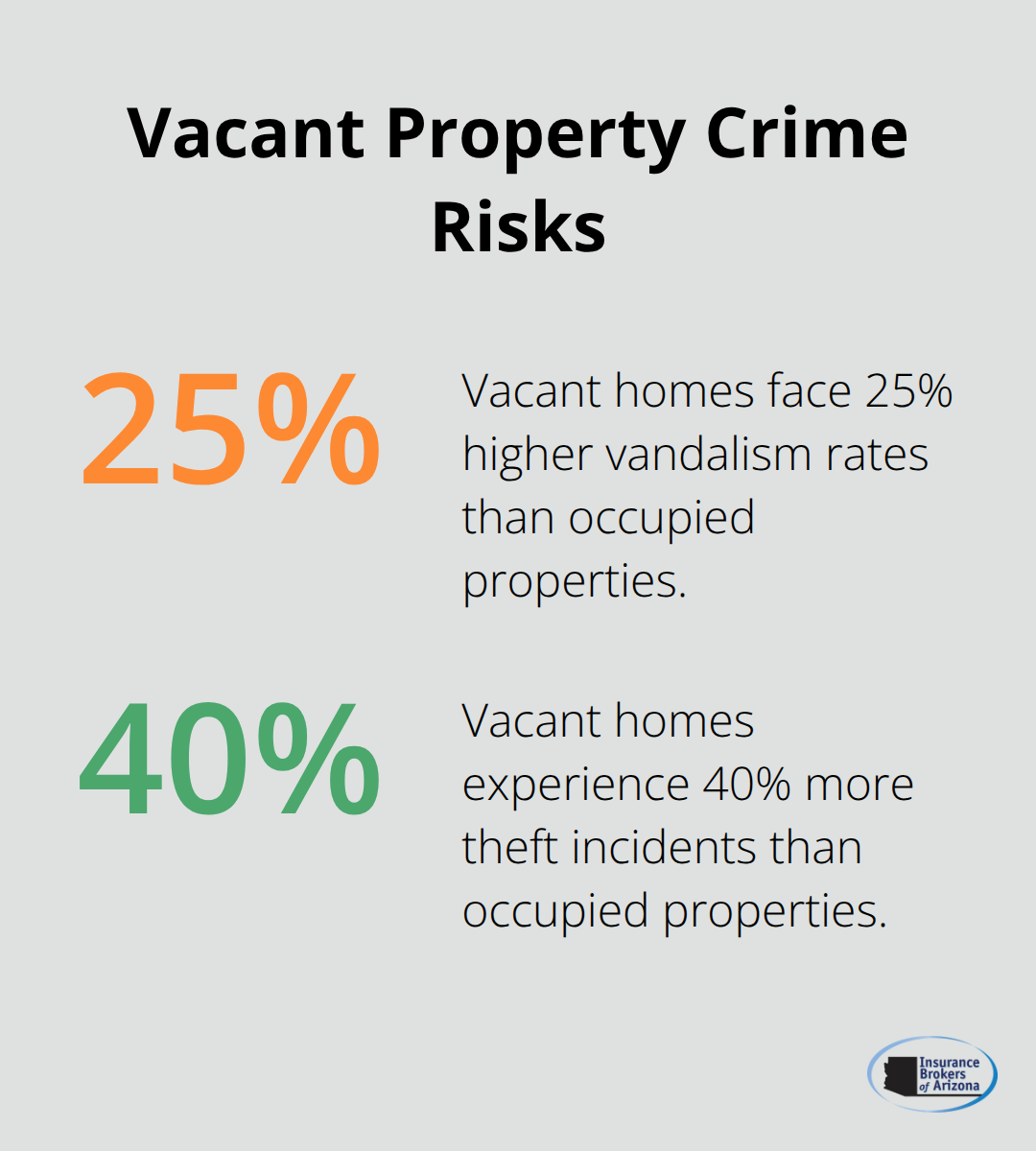

Insurance companies refuse to cover vacant homes under standard policies because the risk profile changes dramatically when properties sit empty. The National Association of Insurance Commissioners reports that vacant homes face 25% higher vandalism rates and 40% more theft incidents compared to occupied properties. Water damage from burst pipes becomes catastrophic without anyone present to shut off water sources, while electrical fires can burn for hours before detection. Standard homeowners policies cost an average of $2,728 annually, but vacant home insurance premiums jump 25-50% higher due to these elevated risks.

Arizona State Requirements for Vacant Properties

Arizona law requires property owners with mortgages to maintain continuous insurance coverage on vacant properties (making specialized vacant home insurance mandatory rather than optional). Lenders can force-place expensive coverage if owners fail to secure adequate protection, often costing three times more than voluntary policies. Arizona’s extreme heat creates additional risks like HVAC system failures and roof damage that vacant home policies must specifically address.

Risk Factors That Drive Premium Costs

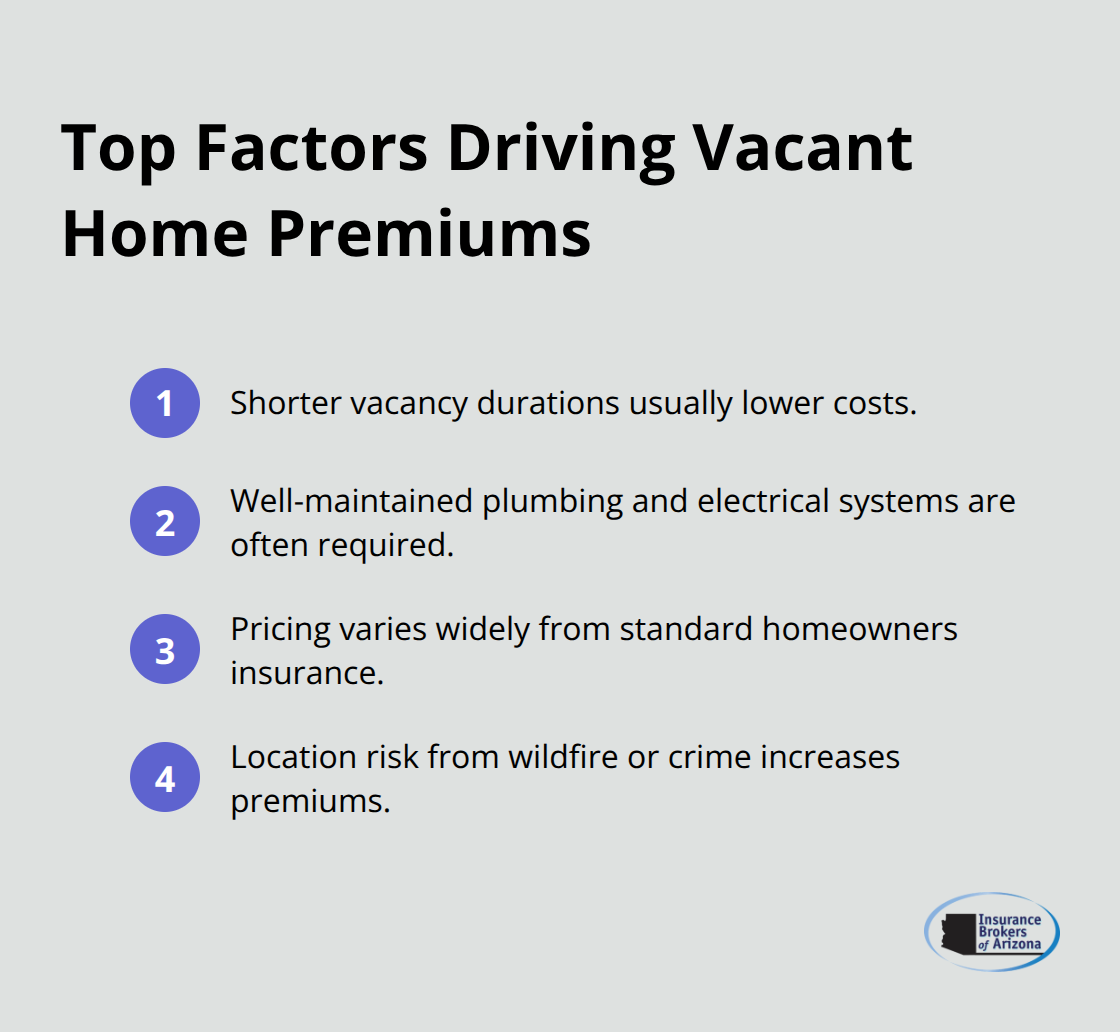

Location significantly affects insurance costs, with properties in high-risk areas prone to wildfires or crime incurring higher premiums. The expected duration of vacancy influences the cost structure (shorter vacancy periods usually result in lower insurance premiums). Property condition plays a major role, as insurers require well-maintained plumbing and electrical systems to qualify for coverage. These factors combine to create a complex pricing structure that varies dramatically from standard homeowners insurance.

Now that you understand why vacant properties require specialized coverage, the next step involves finding the right insurer and policy features that match your specific property needs.

Finding the Right Vacant Home Insurance Policy

Specialized vacant property insurers operate differently than traditional homeowners insurance companies, with only a handful providing comprehensive coverage in Arizona. Progressive, Farmers, and American Family lead the market with dedicated vacant home policies, while USAA serves military families exclusively. Foremost Insurance provides competitive rates for properties vacant 30-365 days, with coverage limits that reach $5 million for property and $1 million for liability. These insurers require properties to be within six miles of fire protection services and maintain good repair standards to qualify for coverage.

Coverage Features That Matter Most

The best vacant home policies include fire, lightning, wind, hail, smoke, and water intrusion damage as standard coverage, but vandalism and theft protection requires special endorsements. Basic form policies cover vandalism for older properties, while special form policies provide broader coverage for newer or recently renovated homes. Theft protection demands active central alarm systems, and liability coverage excludes high-risk features like pools or trampolines. Multi-location policies benefit investors with multiple vacant properties and consolidate coverage under one policy with potential discounts.

Premium Costs and Payment Options

Vacant home insurance costs 150-300% more than standard homeowners policies, with annual premiums that exceed $3,410 for high-risk properties. Insurers offer three, six, or twelve-month policy terms (with longer terms that provide better rates but less flexibility). Properties in wildfire-prone areas face premium surcharges of 40-60%, while crime-heavy neighborhoods add 25-35% to base rates. Temperature monitors, security cameras, and weekly property inspections can reduce premiums by 10-15%, which makes these investments worthwhile for long-term vacant properties.

Quote Comparison Strategies

Property owners should obtain quotes from multiple insurers to secure the best rates and coverage options. Each insurer evaluates risk factors differently, with some specializing in specific property types or geographic areas. The application process requires detailed property information, vacancy duration, and security measures already in place. Smart property owners compare not just premiums but also coverage limits, deductibles, and claim settlement procedures before they make their final decision.

Once you select the right insurer and policy features, the focus shifts to property maintenance and security measures that keep your coverage active and reduce claim risks.

Tips for Maintaining Coverage and Reducing Risks

Property maintenance and security protocols directly determine whether your vacant home insurance remains valid and claims get approved. Insurers require temperature monitoring with smart thermostats set to minimum 55°F to prevent frozen pipes, which cause 37% of vacant property water damage claims according to the Insurance Information Institute. Weekly property inspections become mandatory for most policies, with documented evidence that utilities remain connected and security systems stay operational. Professional property management services cost $150-300 monthly but reduce claim denials by 60% compared to self-managed properties.

Security Systems That Insurers Actually Require

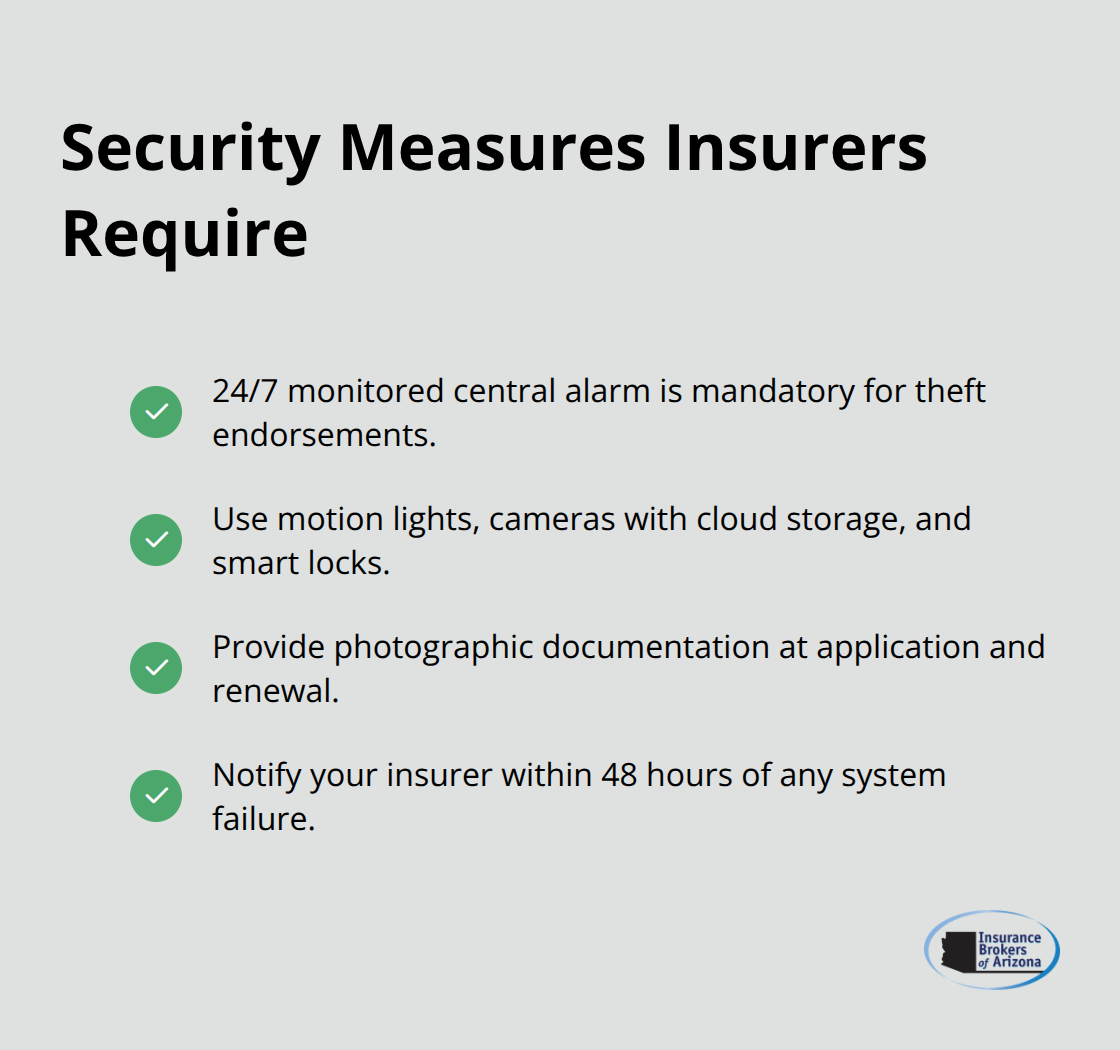

Central alarm systems with 24/7 monitoring reduce premiums by 15-20% and become mandatory for theft coverage endorsements.

Motion sensor lights, security cameras with cloud storage, and smart locks provide additional premium discounts while meeting specific policy requirements. Insurers demand photographic documentation of all security measures during application and annual renewals. Property owners must notify insurers within 48 hours if alarm systems fail or security features become inoperative, as coverage suspends immediately without proper notification.

Temperature Control and Utility Management

Smart thermostats with internet connectivity send alerts when temperatures drop below safe levels (preventing costly pipe freeze damage that destroys vacant properties). Utility companies must maintain active service connections for electricity, gas, and water to satisfy policy requirements. Property owners should test backup generators weekly to verify they operate during power outages. Winterization procedures include draining water lines and insulating exposed pipes in crawl spaces and basements.

Documentation Standards for Claims Protection

Insurers require monthly photographic documentation of property condition, focusing on roof integrity, foundation stability, and HVAC functionality. Temperature logs from smart monitors provide evidence of proper climate control, while utility bills prove continuous service connections. Professional inspection reports every six months satisfy most policy requirements and strengthen claim positions when losses occur. Implementing robust risk management practices helps reduce insurance costs while digital folders with timestamped photos and maintenance records help insurers access documentation during claim investigations.

Final Thoughts

Property owners must act immediately once their home sits empty for more than 30 days to secure vacant home insurance coverage. Standard homeowners policies automatically void after this period, which leaves owners exposed to significant financial risks. Arizona’s extreme heat and wildfire exposure create additional challenges that specialized insurers like Progressive, Farmers, and American Family address through dedicated vacant property policies.

Professional insurance guidance proves invaluable when property owners navigate complex coverage requirements and application processes. We at Insurance Brokers of Arizona® help clients compare multiple carrier options to find optimal protection for their specific situations. Our team understands Arizona’s unique vacant property risks and works to prevent coverage gaps that result in denied claims.

Property owners face time-sensitive decisions when homes become vacant, as delays can create expensive coverage lapses. Specialized insurers require detailed documentation of security systems, maintenance protocols, and property condition before they approve applications. Quick action protects property investments and prevents costly mistakes that standard homeowners insurance cannot cover.