How to Find Affordable Commercial Auto Insurance Rates

Commercial auto insurance rates can drain your business budget faster than you think. The average company spends $1,200 per vehicle annually on coverage.

We at Insurance Brokers of Arizona® see businesses overpaying by 30% or more because they don’t know the right strategies. Smart shopping and risk management can cut your premiums significantly.

What Drives Your Commercial Auto Insurance Rates

Your vehicle choices impact your premiums more than any other factor. Insurers charge construction companies with heavy trucks 40% more than consulting firms with passenger cars. The Insurance Information Institute reports that delivery vehicles face rates 25% higher than office commuter cars due to increased road exposure. Businesses save $800 annually per vehicle when they switch from cargo vans to standard sedans for sales teams.

Driver History Sets Your Base Rate

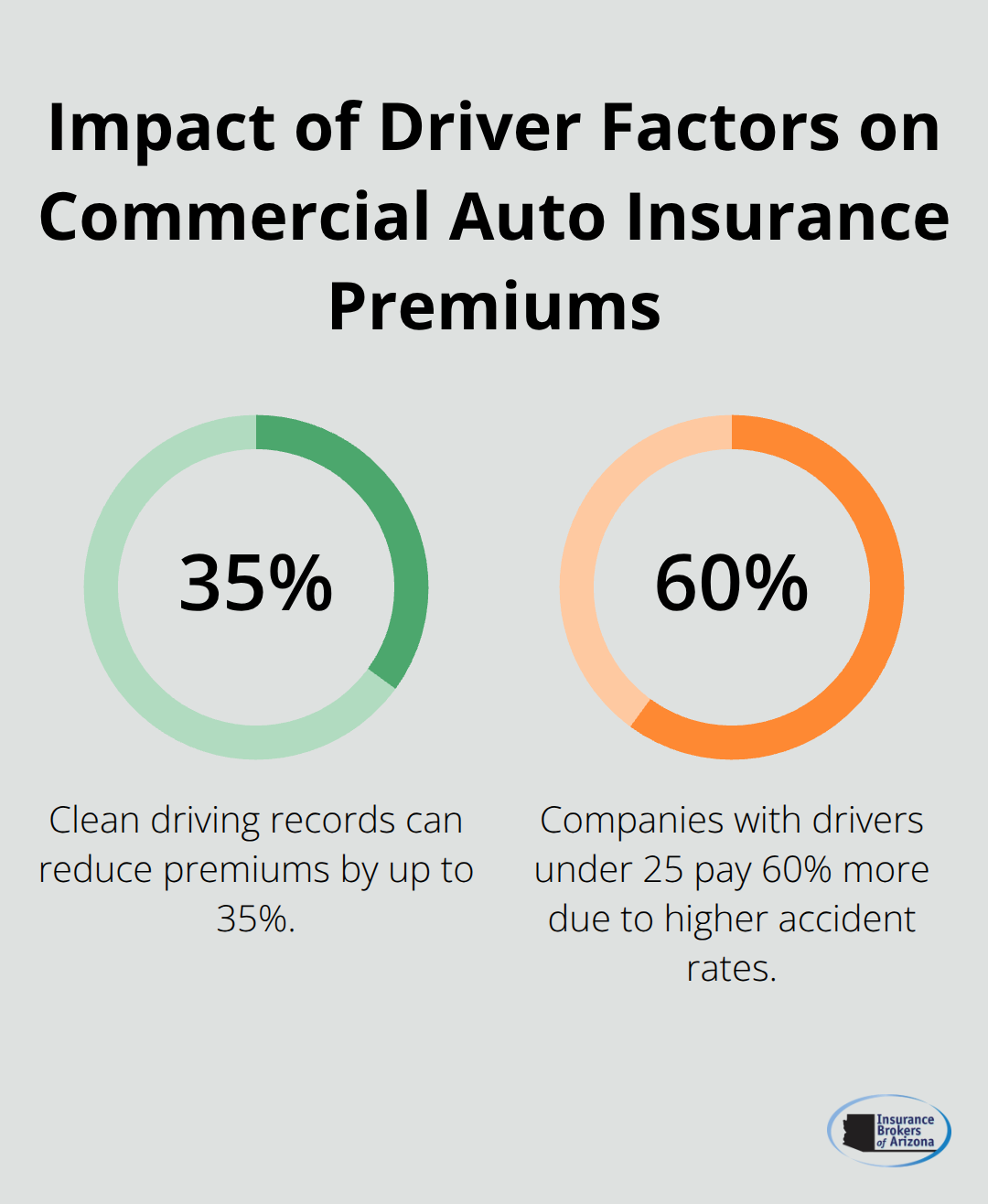

Clean records cut premiums by up to 35%, while accidents within three years increase costs by $1,200 per incident according to NAIC data. Companies with drivers under 25 pay 60% more due to higher accident rates in this age group (statistics show this demographic has triple the crash rate of experienced drivers). Motor vehicle record checks catch violations early – quarterly reviews work better than annual assessments. Businesses that hire only drivers with five-year clean records qualify for preferred rates that average 20% below standard rates.

Coverage Choices Control Your Budget

Higher deductibles slash premiums dramatically. Companies that raise deductibles from $500 to $2,500 reduce costs by 25% on average. State minimum liability coverage costs $400 annually while $1 million limits reach $2,800 per vehicle. Location matters significantly – urban Arizona businesses pay 30% more than rural operations due to higher claim frequencies (Phoenix sees twice the accident rate of Flagstaff). Construction and transportation companies face the steepest rates, often double what professional service firms pay for identical coverage limits.

These rate factors work together to create your final premium, but smart businesses know how to manage each element strategically to reduce costs.

How to Cut Your Commercial Auto Insurance Costs

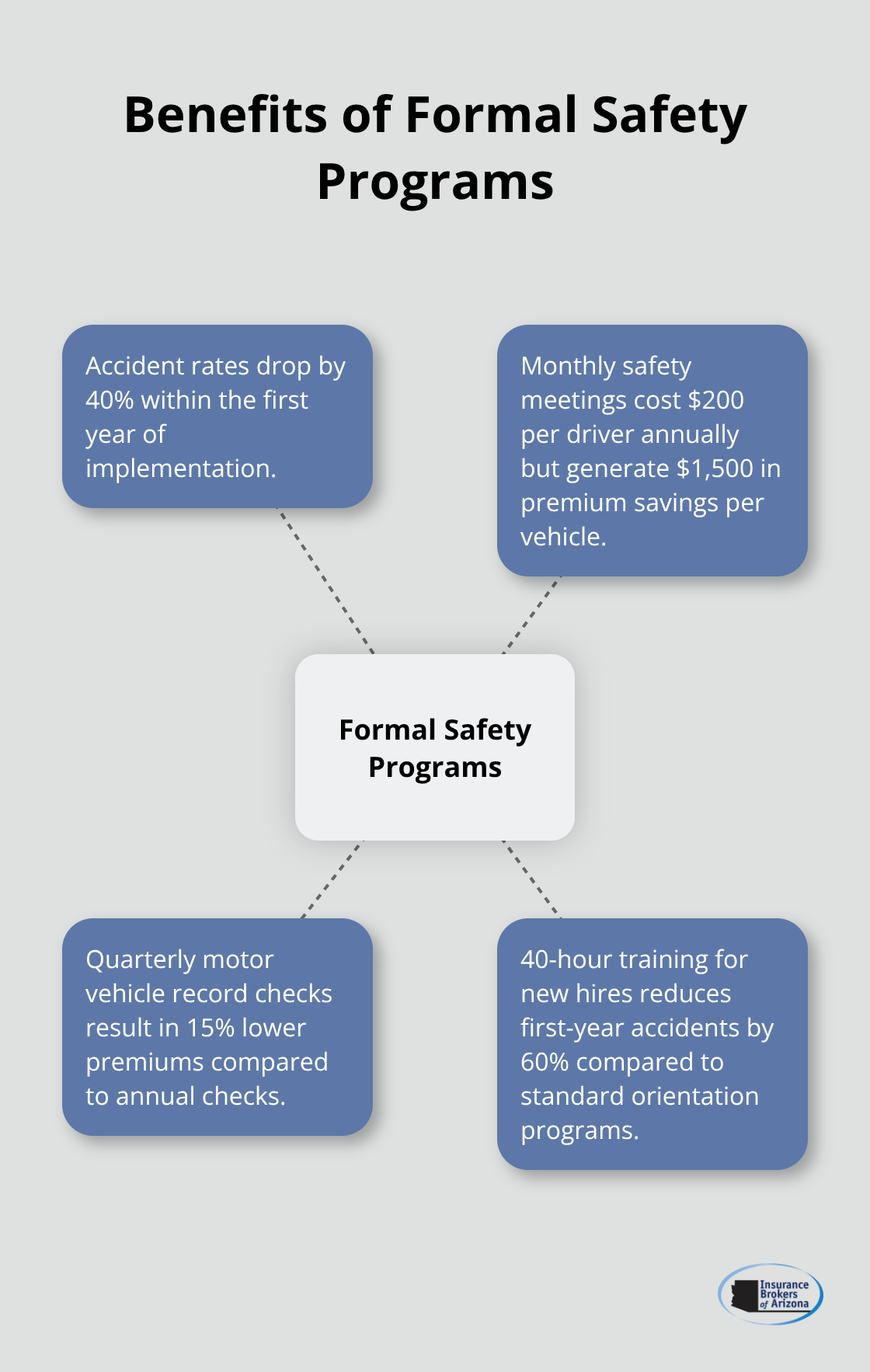

Driver safety programs deliver the fastest premium reductions available to businesses today. Companies that implement formal safety programs see accident rates drop by 40% within the first year, according to Federal Motor Carrier Safety Administration data. Monthly safety meetings cost $200 per driver annually but generate $1,500 in premium savings per vehicle. Quarterly motor vehicle record checks catch violations before renewal time – businesses that monitor drivers monthly pay 15% less than those who check annually. Training new hires for 40 hours reduces first-year accidents by 60% compared to standard orientation programs.

Strategic Deductible Management Cuts Premiums Fast

Raising deductibles from $1,000 to $5,000 reduces premiums by 35% immediately. Companies with strong cash flow should consider $10,000 deductibles to save up to 50% on coverage costs. The National Association of Insurance Commissioners reports that businesses with fewer than two claims annually benefit most from higher deductibles. Self-insure minor incidents below $3,000 while you maintain higher deductibles for major losses to create optimal savings.

Fleet Technology Reduces Risk and Costs

Fleet tracking technology reduces accidents by 30% and qualifies businesses for usage-based insurance discounts that average 20% off standard rates. GPS systems with driver behavior monitoring cost $30 monthly per vehicle but generate $400 annual savings through safer driving habits (dash cameras provide accident evidence that speeds claims processing). These systems reduce fraudulent claims by 25% while giving insurers the data they need to offer better rates.

Policy Bundling Creates Compound Savings

Combining commercial auto with general liability and property insurance generates multi-policy discounts that average 12% across all coverage types. Businesses that consolidate five policies with one carrier save 18% more than single-policy purchasers. Annual policy reviews identify coverage gaps and eliminate redundant protection that wastes money. Companies that change carriers every three years maintain competitive rates while those who stay with the same insurer for five years pay 22% above market rates on average.

Smart cost reduction strategies work best when you combine them with effective shopping techniques that compare multiple carriers and coverage options.

How to Shop for Commercial Auto Insurance

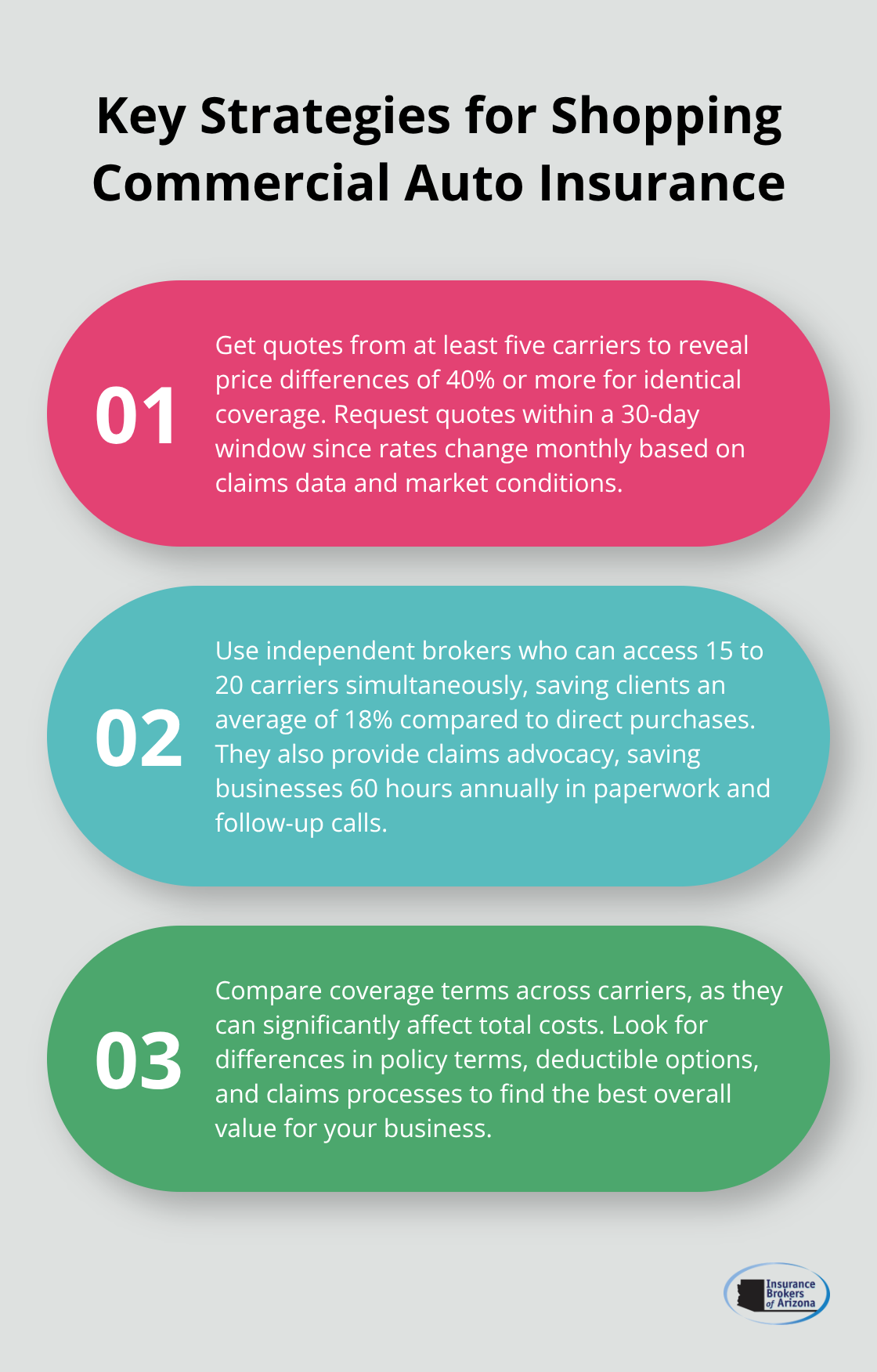

Quotes from at least five carriers reveal price differences of 40% or more for identical coverage, according to National Association of Insurance Commissioners data. Progressive charges construction companies $3,200 annually while State Farm quotes the same business $2,100 for equivalent limits. Request quotes within a 30-day window since rates change monthly based on claims data and market conditions. Submit identical information to each carrier – different details skew comparisons and waste time. The top three carriers by market share control 47% of commercial auto business, but regional insurers often beat their rates by 15% to 25% for local businesses.

Independent Brokers Access More Markets

Independent agents quote 15 to 20 carriers simultaneously while captive agents sell only one company’s products. Insurance Brokers of Arizona® works with over 40 carriers to find optimal rates that direct writers cannot match. Brokers negotiate better terms because they bring volume business to insurers – this leverage saves clients an average of 18% compared to direct purchases. Independent agents also handle claims advocacy, which saves businesses 60 hours annually in paperwork and follow-up calls. Choose brokers who specialize in commercial lines rather than personal insurance generalists since commercial coverage requires specific expertise.

Policy Details Determine Real Value

Replacement cost coverage costs 30% more than actual cash value but pays full vehicle replacement without depreciation deductions. Commercial policies with hired and non-owned auto coverage protect against lawsuits when employees use personal vehicles for business – this $200 annual add-on prevents $500,000 exposures. Gap coverage eliminates loan balances that exceed vehicle values (this saves businesses from paying $15,000 deficits after total loss claims). Annual policy reviews catch coverage changes that affect rates – businesses that skip reviews pay outdated premiums that average 12% above current market rates.

Compare Coverage Terms Across Carriers

Different insurers offer varying policy terms that affect your total cost beyond the premium price. Some carriers include roadside assistance at no extra charge while others charge $150 annually for identical service. Deductible options vary significantly – one insurer might offer $500 minimums while another starts at $1,000 (this difference affects both premium costs and out-of-pocket expenses). Review each carrier’s claims process since some require pre-authorization for repairs while others allow direct payment to shops.

Final Thoughts

Commercial auto insurance rates drop significantly when you combine smart risk management with strategic shopping. Driver safety programs and higher deductibles reduce base premiums by 35% or more. Multi-policy discounts with one carrier add another 12% in savings across all coverage types.

Price differences of 40% between insurers make comparison shopping essential within a 30-day window. Regional carriers beat national companies by 15% to 25% for local businesses. Annual policy reviews prevent outdated premiums that average 12% above current market rates (companies that skip reviews miss opportunities to optimize coverage).

Professional guidance delivers optimal protection at competitive rates. Insurance Brokers of Arizona® provides access to multiple carriers and handles claims advocacy. Independent brokers save clients an average of 18% compared to direct purchases while reducing administrative burdens significantly.