Your commercial truck insurance down payment is often the first hurdle when securing coverage. The amount you’ll pay upfront depends on several factors-from your vehicle type to your driving record.

At Insurance Brokers of Arizona®, we’ve helped countless truck operators understand what drives these costs and how to reduce them. This guide walks you through the key factors affecting your down payment and practical strategies to lower it.

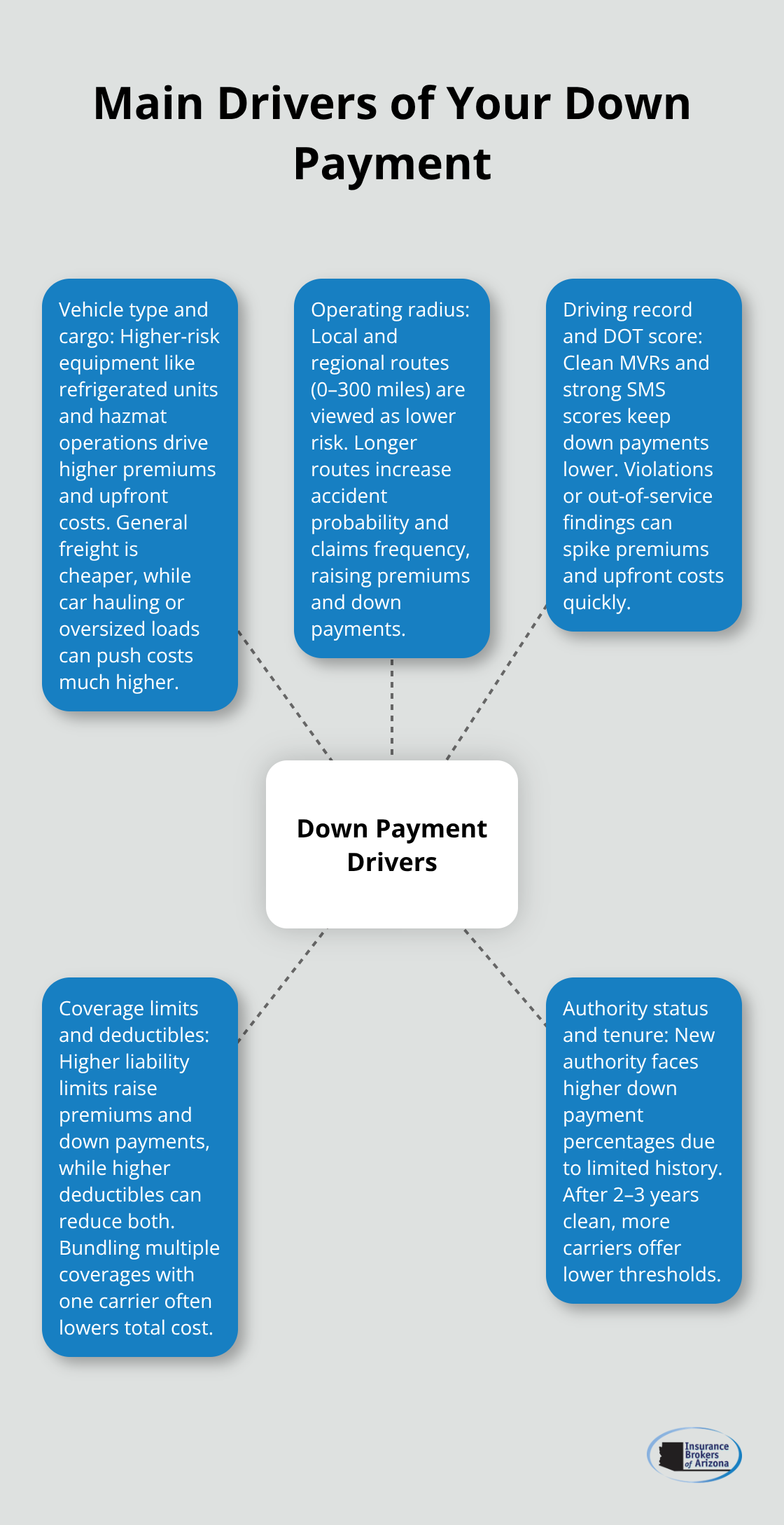

What Drives Your Down Payment

Vehicle type matters far more than most operators realize. A newer refrigerated truck with advanced safety technology will command a lower down payment than an older dry van, even if both operators have identical driving records. Refrigerated units typically cost 15–25% more in annual premiums than standard equipment, which means your down payment scales accordingly. Hazmat carriers face the steepest upfront costs because the FMCSA requires $5 million in liability coverage for hazardous materials, pushing annual premiums into the $18,000–$25,000 range and down payments to $3,000–$6,000. The cargo type you haul also influences risk assessment: general freight costs less, while oversized loads or car hauling can nearly double your insurance costs since they expose insurers to higher liability exposure. If you operate within a 0–300 mile radius, your down payment will be substantially lower than someone running 500+ miles, because longer routes increase accident probability and claims frequency.

How Your Driving Record Shapes What You Pay Upfront

Your motor vehicle record is the single most predictive factor for down payments. New authority operators typically face down payments of 15–25% of annual premiums because underwriters view them as unproven, while experienced drivers with clean records pay closer to 10–15%. A single violation or out-of-service finding from roadside inspections can spike your entire premium by thousands of dollars in a single renewal cycle. This means your down payment can jump by $500–$1,500 overnight if your safety record deteriorates. Conversely, operators with 3+ years of clean operation unlock access to carriers like Great West, Northland, and National Indemnity that offer substantially lower down payments than Progressive or OOIDA. Your DOT safety score matters year-round, not just at renewal, so maintaining your SMS score directly protects your down payment from unexpected increases.

Coverage Choices and Their Upfront Cost Impact

The deductibles you select have immediate consequences for your initial payment. Raising your collision deductible from $1,000 to $2,500 can reduce your annual premium by 15–25%, which proportionally lowers your down payment. A $1,500–$3,000 annual savings translates directly into $150–$450 less due upfront. Coverage limits also matter: most owner-operators carry $1 million in liability even though FMCSA minimums are $750,000, because shippers and brokers increasingly require the higher limit. That $250,000 extra in liability coverage will add roughly $400–$800 to your annual premium and $40–$120 to your down payment. Combining multiple coverages with a single carrier yields measurable savings that reduce your overall down payment; operators who combine primary liability, cargo, physical damage, and bobtail coverage with one insurer often save 10–15% on the total package compared to splitting coverage across multiple carriers.

Why Operating Radius Affects Your Initial Costs

Your operating radius directly influences how underwriters assess your risk profile. Carriers that restrict you to local or regional routes (0–300 miles) view you as lower risk than operators who cross state lines or run nationwide. This difference translates into down payment reductions of 10–20% for local operators. If you shift your operations or expand your service area, you must update your FMCSA filings and verify your ELD data to avoid surcharges or disputes at renewal. Underwriters will recalculate your premium and down payment based on your new radius, so transparency about your actual routes matters significantly.

How New Authority Status Impacts Your Upfront Costs

New authority operators face a distinct penalty in the insurance market. Underwriters lack a track record to evaluate, so they apply higher down payment percentages and stricter underwriting standards. After two to three years of clean operation, you gain access to more carriers and lower down payment thresholds. This progression means your down payment can drop by 30–40% once you move from new authority status to established operator status. The carriers that accept new authority business (Progressive and OOIDA) typically require higher down payments than the carriers that emerge after year three (Great West, Northland, National Indemnity). Understanding this timeline helps you plan your cash flow and anticipate when your down payment obligations will decrease.

Your down payment is just the first step toward securing the right coverage. The next section explores practical strategies to reduce that initial payment and find the coverage that actually matches your operation.

How to Cut Your Down Payment Without Cutting Coverage

Bundle Your Policies for Immediate Savings

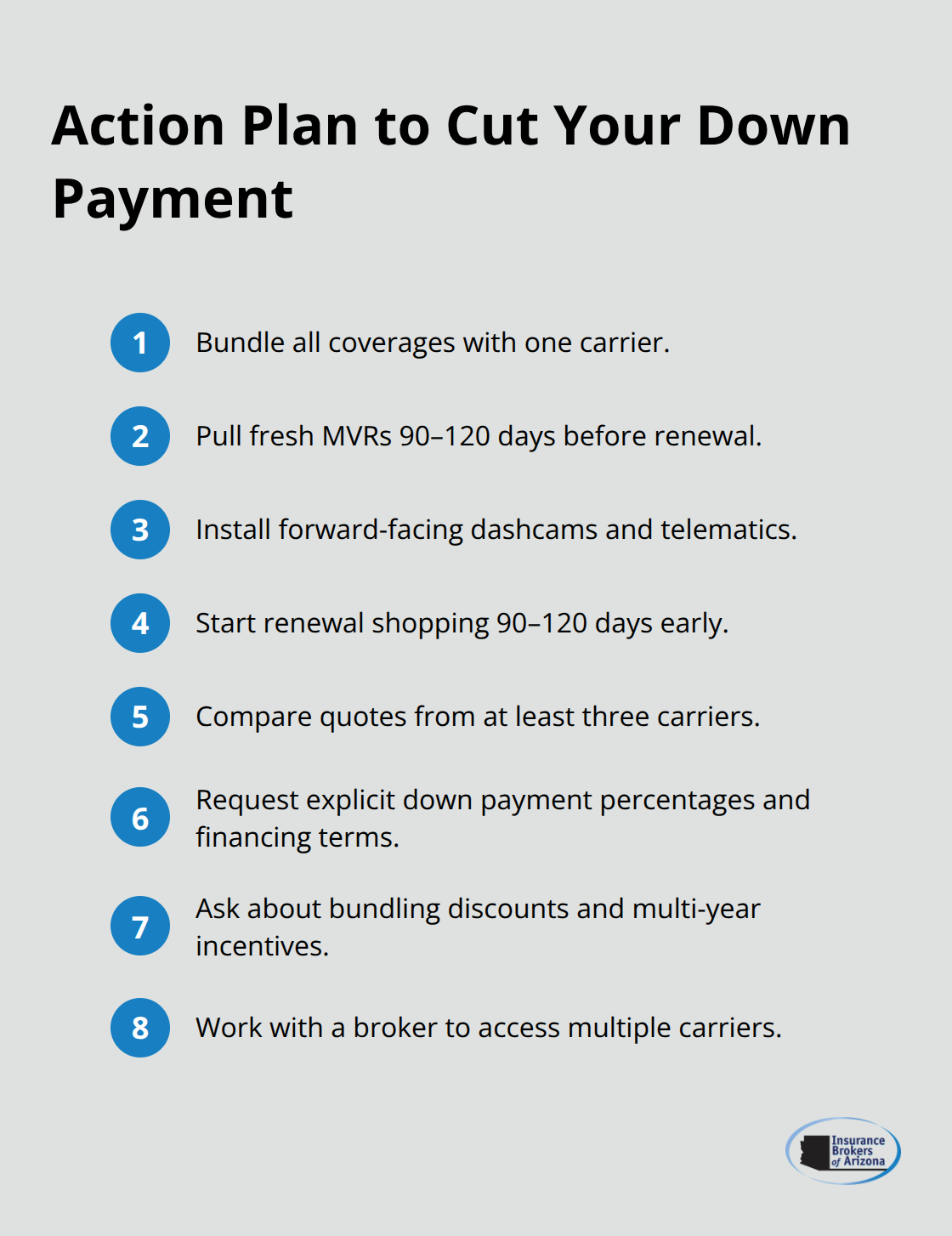

Bundling your policies with a single carrier reduces your down payment immediately. Operators who combine primary liability, cargo, physical damage, and bobtail coverage under one insurer typically save 10–15% on their total annual premium, which translates directly into a lower upfront payment. A $12,000 annual premium becomes roughly $10,200 after bundling, dropping your down payment from $1,800 to $1,530 if you pay 15% upfront.

Lock in the relationship for at least two years, because carriers reward multi-year commitments with stability and better renewal terms. When you shop for quotes, ask carriers explicitly whether they offer bundling discounts and what the total cost looks like across all coverages combined, not just primary liability in isolation.

Many operators waste money by pricing liability separately from cargo and physical damage, then assembling coverage piecemeal across three different insurers. That fragmented approach costs more upfront and at renewal because you lose the bundling advantage entirely.

Strengthen Your Safety Record Before Renewal

Your motor vehicle records and driver qualification files are the second lever you control. Pull fresh MVRs for every driver 90–120 days before renewal and conduct a mini-audit of your driver files (medical cards, employment verification, drug and alcohol testing records). This signals to underwriters that you take compliance seriously. Fleets that document this proactive approach often qualify for safety discounts of 2–5% on liability premiums, which reduces your down payment by $200–$600 annually.

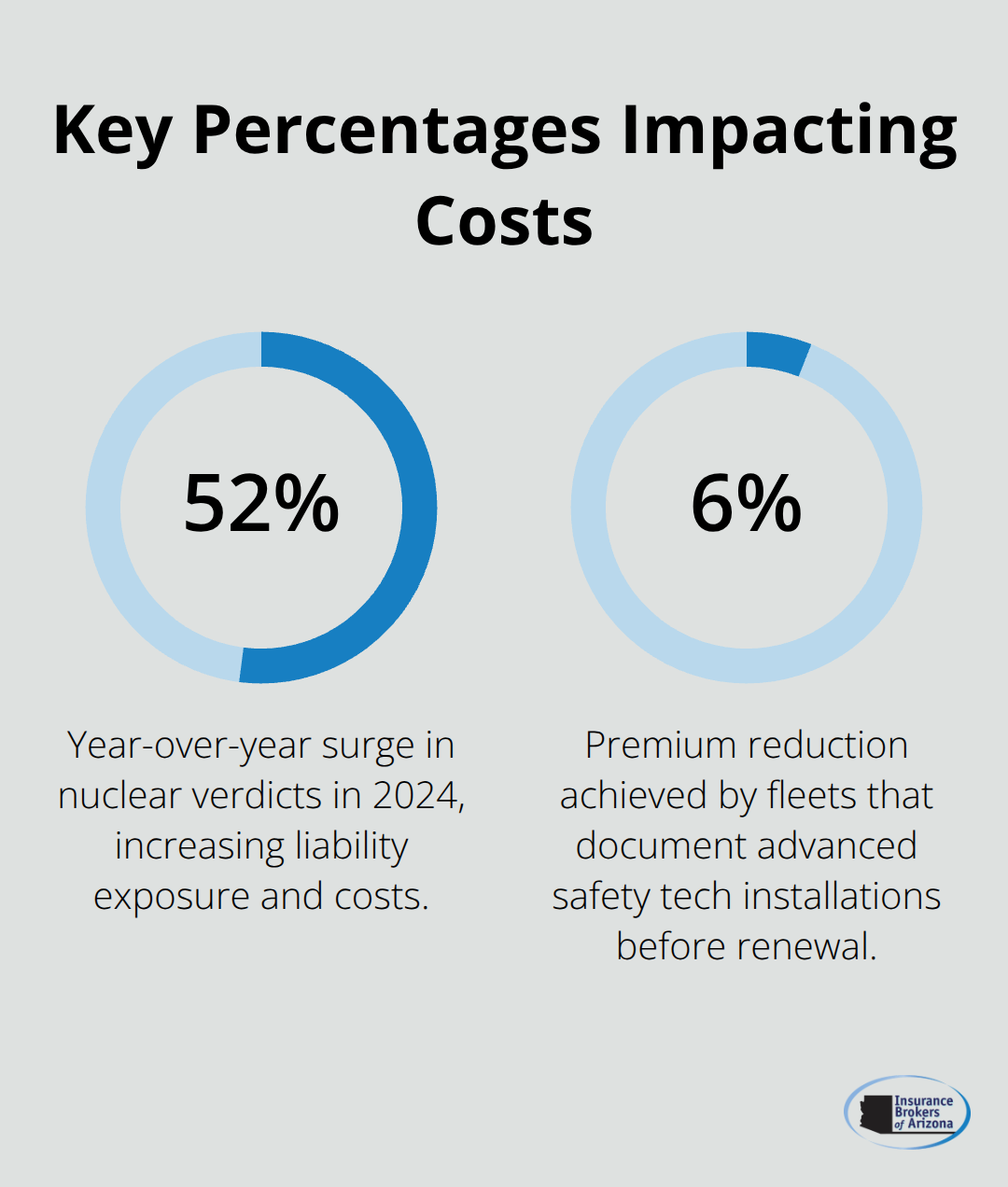

Installing forward-facing dashcams, telematics systems, automatic braking, or lane departure warnings can lower liability premiums by up to 6% because you demonstrate measurable risk reduction. One fleet cut liability premiums by 6% specifically by documenting forward collision avoidance system installations to their carrier before renewal. These investments cost $2,000–$5,000 upfront but pay for themselves within a year through lower premiums and smaller down payments.

Plan Your Renewal Timeline to Gain Negotiating Power

Start your renewal planning 90–120 days ahead rather than waiting until the last 30 days. This gives you negotiating leverage because carriers know you’re not desperate. Waiting until the final month forces you to accept overpriced offers and higher down payment requirements because underwriters recognize you have no alternatives.

Compare Quotes from Multiple Carriers

Comparing quotes from at least three carriers is non-negotiable, yet most operators solicit only one or two quotes before committing. Each carrier weights your risk factors differently, meaning the same driver, truck, and operation can generate vastly different premium quotes and down payment structures. One carrier might require 20% down while another accepts 10% down for identical coverage, simply because their underwriting appetite differs.

Progressive and OOIDA dominate the new authority market but rarely offer the lowest down payments once you have 2–3 years of clean operation. After that threshold, carriers like Great West, Northland, and National Indemnity become available and frequently quote 15–30% lower premiums than the carriers that initially accepted your new authority business. The down payment savings compound over time, so a $2,000 reduction in annual premium saves you $300 in down payment costs immediately and $300 annually thereafter.

Request explicit down payment percentages and financing options from each carrier, not just total premium figures, because some carriers offer 10% down while others demand 25% regardless of credit or driving history. An experienced broker can access multiple carriers simultaneously and present side-by-side comparisons that show total cost of ownership, not just the monthly payment or annual premium in isolation.

Your down payment strategy sets the foundation for sustainable coverage costs, but the coverage itself must match your actual operation. The next section examines the specific liability requirements and specialized coverages that protect your business from the risks you actually face.

What Coverage Do You Actually Need

FMCSA minimums exist as a legal baseline, not as adequate protection for your operation. The federal requirement sits at $750,000 in liability for general freight over 10,001 lbs, but most shippers and brokers now require $1 million as a condition of load acceptance. That $250,000 gap matters: it adds roughly $400–$800 to your annual premium, which translates to $40–$120 on your down payment. Hazmat carriers face a completely different threshold at $5 million in liability coverage because the risk exposure is exponentially higher. New authority operators commonly carry $1 million in liability even when $750,000 would satisfy FMCSA requirements, because carriers know that a single nuclear verdict can exceed federal minimums by millions. In 2024, nuclear verdicts surged 52% year-over-year, with median verdicts reaching $51 million and thermonuclear awards exceeding $100 million in 49 cases. This means the $250,000 difference between federal minimum and industry standard is not optional-it is the difference between catastrophic personal liability and manageable risk.

Physical Damage Protects Your Equipment Investment

Physical damage coverage splits into collision and comprehensive, and your choice depends on whether you own or finance your truck. If your rig is financed, the lender requires physical damage coverage as a loan condition. Owner-operators typically pay $1,000–$3,000 annually for physical damage, with collision deductibles ranging from $500 to $2,500. Raising your collision deductible from $1,000 to $2,500 cuts your annual premium by 15–25%, saving $150–$450 upfront on your down payment. However, this strategy works only if you have cash reserves to cover the higher deductible after a loss. Comprehensive coverage protects against theft, weather, and vandalism and costs significantly less than collision-often $400–$800 annually. Many operators skip comprehensive on older paid-off trucks, but if you operate in high-theft urban areas or park overnight in exposed lots, that decision can backfire. Garage storage reduces your comprehensive premium by 10–15% because insurers view secure facilities as lower risk than outdoor parking, so if you have access to a covered lot, inform your carrier before renewal.

Specialized Coverage Matches Your Actual Cargo and Operations

Cargo insurance cost depends entirely on freight value and load type. General freight runs $400–$800 annually, but refrigerated units cost 15–25% more because temperature-controlled equipment represents higher equipment value and spoilage risk. Hazmat cargo requires separate underwriting and pushes annual premiums to $18,000–$25,000 or higher depending on the hazard class. The FMCSA defines nine hazmat classes-explosives, gases, flammable liquids, flammable solids, oxidizers, poison, radioactive materials, corrosives, and miscellaneous-and each class carries different underwriting scrutiny and premium structures. Car hauling nearly doubles insurance costs in some cases because vehicles represent high-value cargo with elevated loss frequency. Oversized load permits trigger additional coverage requirements and premium adjustments because they increase your liability exposure on public roads.

Additional Coverages That Close Protection Gaps

Non-trucking liability covers you during personal use when you operate without dispatch, and costs $350–$480 annually-this coverage is critical because your primary liability policy excludes personal use. Bobtail coverage applies when you operate a tractor without a trailer and costs $350–$480 annually. Many owner-operators skip bobtail coverage until they need it, then discover they have operated illegally. Occupational accident insurance provides income replacement if you suffer injury and cannot work, costing $1,600–$2,200 annually, and is strongly recommended for independent operators since you lack workers compensation protection. Uninsured and underinsured motorist coverage protects you if another driver causes an accident without adequate insurance. Downtime coverage reimburses lost income while your truck sits in the shop after a covered loss. Rental reimbursement covers the cost of a substitute vehicle during repairs. Trailer interchange coverage protects you when you haul trailers you do not own. Umbrella liability extends your protection beyond standard policy limits and typically costs $500–$700 annually for $1 million in additional coverage.

Bundle Coverage to Reduce Total Cost

Bundling cargo, bobtail, and occupational accident with your primary liability saves 10–15% compared to purchasing these coverages separately, so request combined pricing from your carrier before committing to a single policy. A $12,000 annual premium drops to roughly $10,200 after bundling, which reduces your down payment proportionally. Lock in the relationship for at least two years, because carriers reward multi-year commitments with stability and better renewal terms. When you shop for quotes, ask carriers explicitly whether they offer bundling discounts and what the total cost looks like across all coverages combined, not just primary liability in isolation. Many operators waste money by pricing liability separately from cargo and physical damage, then assembling coverage piecemeal across three different insurers. That fragmented approach costs more upfront and at renewal because you lose the bundling advantage entirely.

Final Thoughts

Your commercial truck insurance down payment hinges on three controllable factors: your safety record, your coverage choices, and your renewal timeline. New authority operators typically pay 15–25% down because underwriters lack a track record, but this penalty disappears after two to three years of clean operation. Experienced drivers with solid motor vehicle records qualify for down payments as low as 10–15%, while violations or out-of-service findings spike your upfront costs by $500–$1,500 overnight.

Reducing your down payment without sacrificing protection requires three concrete actions. Bundle your policies with a single carrier to save 10–15% on total premiums, which translates directly into lower upfront payments. Strengthen your safety record by pulling fresh motor vehicle records 90–120 days before renewal and install forward-facing dashcams or telematics-these investments cut liability premiums by 2–6% and signal reduced risk to underwriters.

Start your renewal process 90–120 days early and compare quotes from at least three carriers, because each underwriter weights your risk differently and may offer substantially lower down payment percentages for identical coverage. Contact Insurance Brokers of Arizona® to access partnerships with over 40 reputable carriers and receive side-by-side comparisons that show total cost of ownership. Request explicit down payment percentages and financing options from each carrier, then ask about bundling discounts and multi-year commitment rewards.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.