How Much Does General Liability Insurance Cost?

General liability insurance price is a crucial factor for businesses of all sizes. At Insurance Brokers of Arizona®, we understand that cost concerns often top the list when it comes to insurance decisions.

This blog post will break down the key factors that influence general liability insurance costs and provide insights into average pricing across different industries and business sizes. We’ll also share practical tips to help you potentially lower your premiums without sacrificing essential coverage.

What Drives General Liability Insurance Costs?

General liability insurance costs vary widely based on several key factors. Let’s explore the main drivers of general liability insurance pricing.

Business Size and Revenue

The size of your business and its annual revenue significantly impact your general liability insurance costs. Larger companies with higher revenues typically face higher premiums due to increased exposure to potential claims. A small local shop with $100,000 in annual revenue might pay around $500 per year for general liability insurance, while a medium-sized business with $1 million in revenue could see premiums closer to $2,000 annually.

Industry and Risk Level

Your industry and associated risk level heavily influence insurance costs. High-risk industries (like construction or manufacturing) often face higher premiums due to the increased likelihood of accidents or property damage. A construction company might pay $3,000 to $5,000 annually for $1 million in coverage, while a low-risk business (such as a consulting firm) might only pay $500 to $1,000 for the same coverage limits.

Coverage Limits and Deductibles

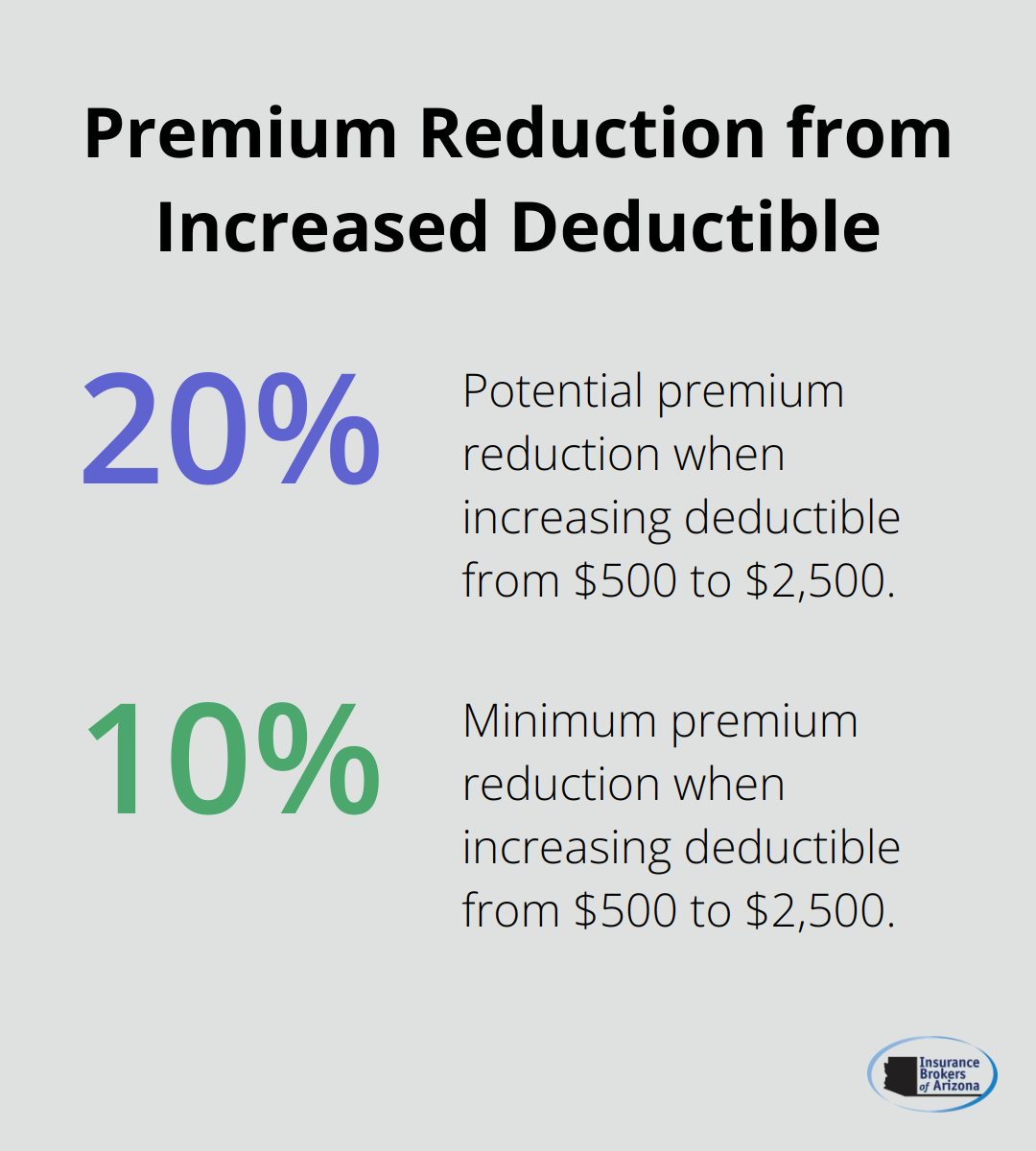

The amount of coverage you choose and your deductible directly affect your premiums. Higher coverage limits provide more protection but come with higher costs. Similarly, opting for a higher deductible can lower your premiums but increases your out-of-pocket expenses in the event of a claim. Increasing your deductible from $500 to $2,500 could potentially reduce your premium by 10-20%.

Claims History and Experience

Your claims history and years of experience in business also impact your insurance costs. A clean claims record often leads to lower premiums, as insurers view you as a lower risk. Conversely, a history of frequent claims can significantly increase your costs. New businesses without an established track record might also face higher initial premiums until they prove their risk management capabilities.

Businesses with similar profiles in the same industry can face vastly different premiums due to their claims history. Two retail stores of similar size might see a 30-40% difference in premiums if one has a history of multiple liability claims while the other has a clean record.

Understanding these factors can help you better anticipate and manage your general liability insurance costs. However, it’s important to note that each business is unique, and these factors interact in complex ways. Working with experienced insurance professionals proves essential for obtaining the most accurate and competitive quotes for your specific situation. Now, let’s examine the average costs of general liability insurance across different business sizes and industries.

What’s the Average Cost of General Liability Insurance?

General liability insurance costs vary significantly across businesses. Let’s examine the average costs for different business sizes and industries.

Small Business Costs

Small businesses typically pay between $300 and $1,000 annually for general liability insurance. This range can extend based on specific risk factors. A small consulting firm might pay as little as $250 per year, while a small construction company could see premiums of $2,000 or more.

Medium-sized Business Expenses

Medium-sized businesses often face annual premiums ranging from $2,000 to $5,000. This increase reflects the higher exposure that comes with more employees, larger revenues, and potentially more complex operations. A medium-sized retail store might pay around $3,000 annually, while a similarly sized manufacturing company could see costs closer to $5,000 or more.

Large Corporation Premiums

Large corporations typically pay $5,000 to $15,000 or more per year for general liability insurance. These higher costs reflect the increased complexity and potential risks associated with larger operations. Some large corporations in high-risk industries might even see premiums exceeding $100,000 annually.

Industry-Specific Costs

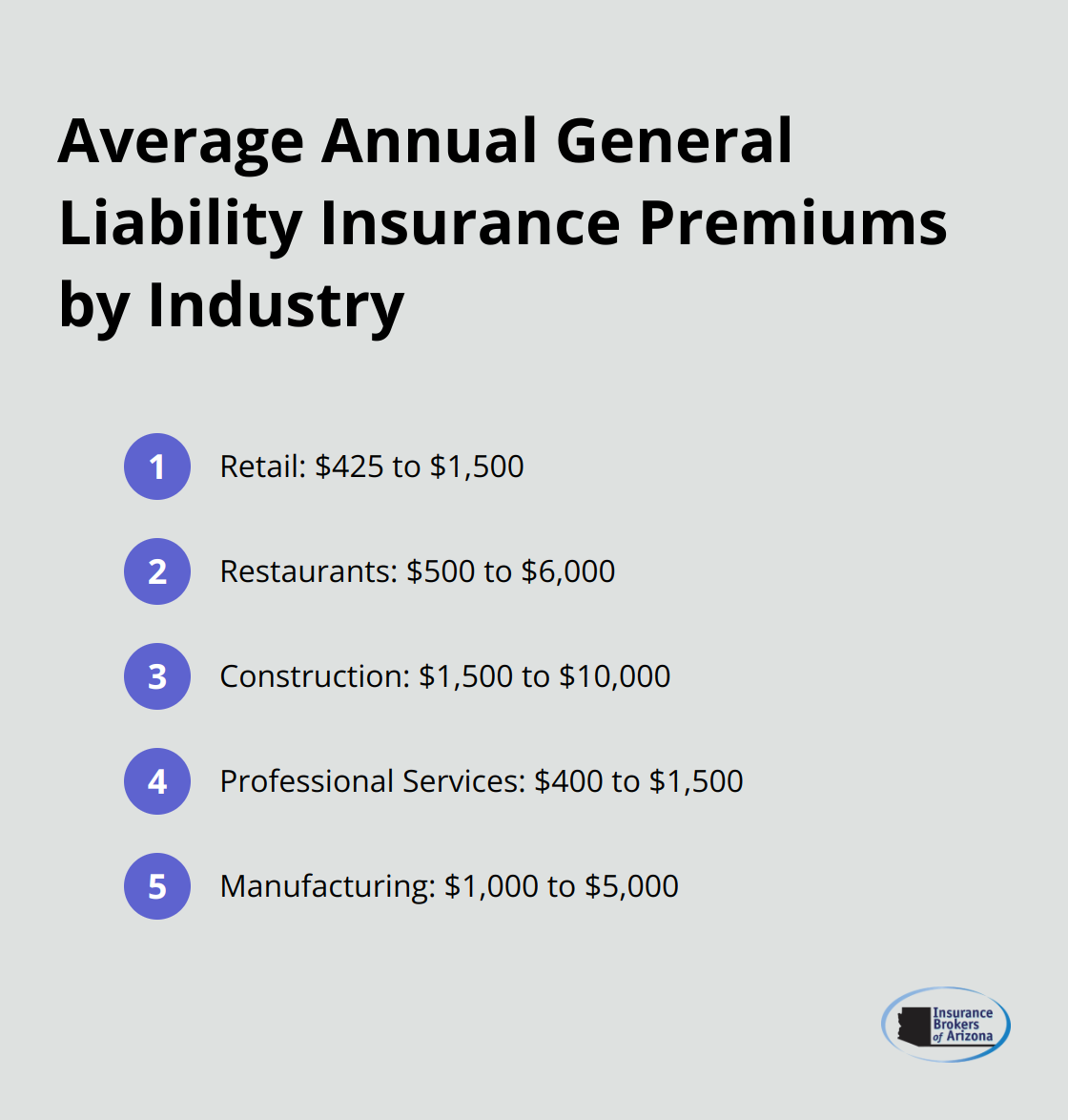

Industry plays a key role in determining insurance costs. Here are some examples of average annual premiums by industry:

- Retail: $425 to $1,500

- Restaurants: $500 to $6,000

- Construction: $1,500 to $10,000

- Professional Services: $400 to $1,500

- Manufacturing: $1,000 to $5,000

These figures come from industry reports and reflect general trends. However, individual businesses within these industries may face significantly different costs based on their specific risk profiles.

For example, a high-end jewelry store might pay more than a small bookshop due to the higher value of goods on premises. Similarly, a restaurant with a full bar might face higher premiums than a small café due to the increased liability associated with alcohol service.

Understanding these average costs can help you benchmark your own insurance expenses. However, the most accurate way to determine your specific costs is to get a personalized quote (which takes into account all the unique aspects of your business).

Now that we’ve explored the average costs of general liability insurance, let’s look at some strategies to potentially lower your premiums without compromising on essential coverage.

How to Reduce Your General Liability Insurance Costs

At Insurance Brokers of Arizona®, business owners often ask us about ways to lower their general liability insurance premiums without compromising essential coverage. While no single solution fits all businesses, several strategies can help reduce costs. Let’s explore some effective approaches to potentially lower your general liability insurance expenses.

Implement Strong Risk Management

One of the most impactful ways to reduce your insurance costs is to implement robust risk management strategies. This proactive approach can significantly lower the likelihood of claims, making your business more attractive to insurers.

A retail store that installs security cameras and conducts regular staff safety training might see a 10-15% reduction in their premiums. Similarly, a construction company that enforces strict safety protocols and provides ongoing education to workers could potentially save 20-30% on their insurance costs.

Bundle Your Policies

Many insurers offer discounts when you combine multiple policies. This approach, often called a Business Owner’s Policy (BOP), typically combines general liability with property insurance and can lead to substantial savings.

Industry data shows that businesses can save an average of 10-20% by bundling their policies. For instance, a small restaurant owner might save $500 annually by combining their general liability and property insurance into a single BOP.

Increase Your Deductible

Choosing a higher deductible can lower your monthly or annual premiums. While this means you’ll pay more out-of-pocket if a claim occurs, it can result in significant long-term savings for businesses with a strong financial position and good risk management practices.

An increase in your deductible from $500 to $2,500 could potentially reduce your premium by 10-20% (but ensure you can comfortably afford the higher deductible if needed).

Keep a Clean Claims History

A clean claims history shows insurers that your business is low-risk, which can lead to lower premiums over time. Focus on preventing incidents that could lead to claims and address potential hazards promptly.

Businesses with no claims for three to five years often see premium reductions of 5-15%. For example, a consulting firm that maintains a claim-free record for five years might see their annual premium drop from $1,000 to $850.

Compare Multiple Quotes

Insurance markets are competitive, and rates can vary significantly between providers. Comparing quotes from multiple insurers can often lead to substantial savings.

Working with an independent agency gives you access to quotes from multiple carriers, increasing your chances of finding the best rate. Clients often save 15-30% on their premiums by leveraging relationships with numerous reputable carriers.

Final Thoughts

General liability insurance prices depend on various factors such as business size, industry risk, and claims history. Companies can reduce their premiums through effective risk management, policy bundling, and maintaining a clean claims record. The right coverage balances cost with adequate protection for your business.

Insurance Brokers of Arizona® offers personalized solutions to help businesses find the optimal balance between cost and coverage. Our partnerships with numerous carriers allow us to provide a wide range of options that fit specific needs and budgets. We pride ourselves on our tailored approach and deep understanding of the Arizona insurance market.

Our expertise in navigating general liability insurance complexities benefits our clients significantly. We help businesses understand their risk profiles, explore cost-saving opportunities, and secure comprehensive coverage that protects without excessive expense. Insurance Brokers of Arizona® strives to provide the best value for your business, ensuring you receive the protection you need at a competitive price.