High-Risk Home Insurance: What You Need to Know

Owning a home in a flood zone, wildfire area, or aging property can make finding affordable coverage challenging. High-risk home insurance often comes with higher premiums and limited options.

We at Insurance Brokers of Arizona® help homeowners navigate these complex insurance markets daily. Understanding your options can save thousands while protecting your most valuable asset.

What Puts Your Home in the High-Risk Category

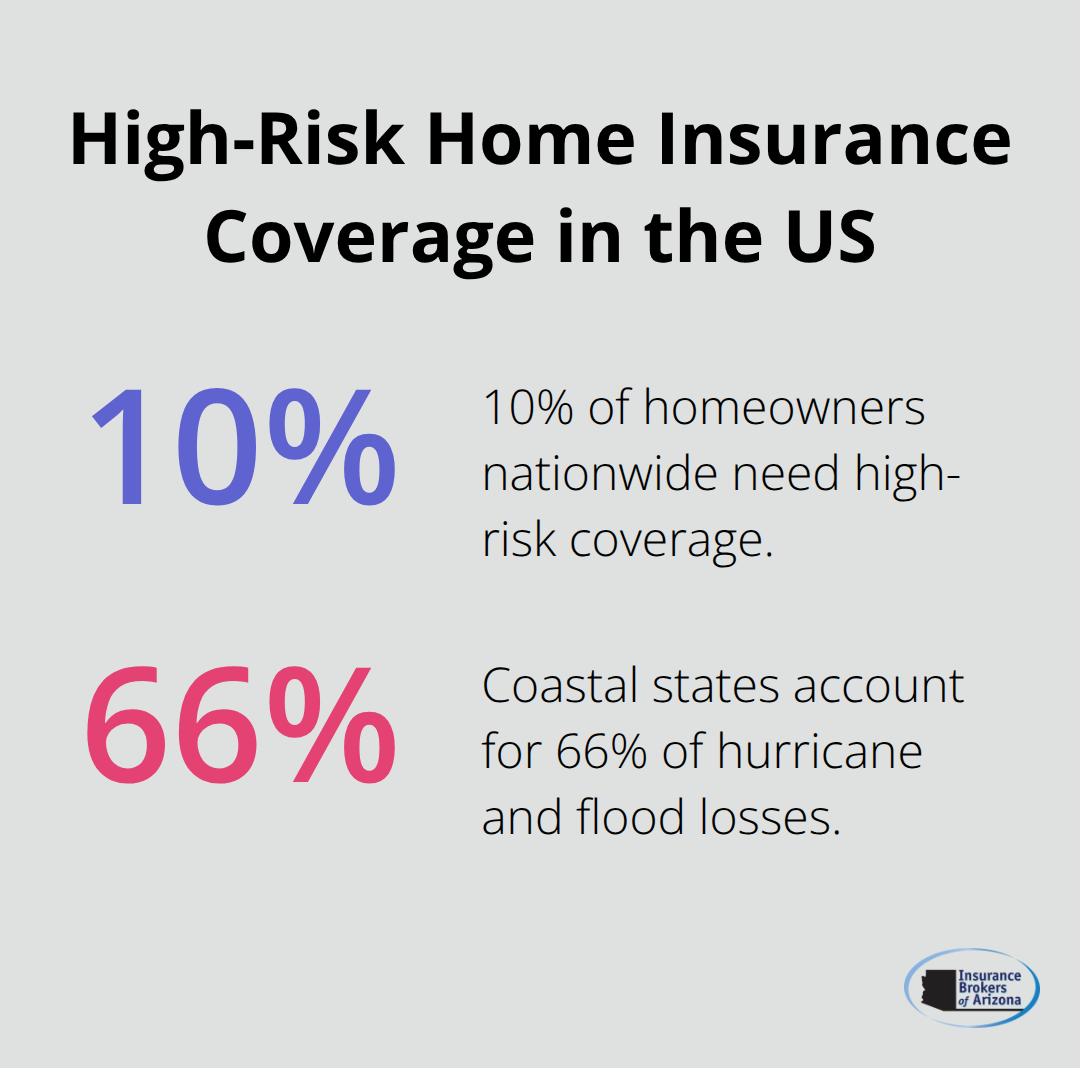

Insurance companies classify homes as high-risk based on three primary factors that significantly impact your ability to get coverage and the premiums you pay. Location tops the list, with properties in flood zones, wildfire areas, and hurricane-prone regions facing automatic high-risk status. The National Association of Insurance Commissioners reports that approximately 10% of homeowners nationwide need high-risk coverage, with coastal states like Florida, Louisiana, and Texas accounting for two-thirds of hurricane and flood losses.

Geographic Location Determines Risk Level

Properties within one mile of wildfire zones or Special Flood Hazard Areas with a 1% annual chance of flooding face premium increases of 20-50% above standard rates. Coastal areas experience the highest risk classifications due to hurricane exposure and storm surge potential. Between 2018-2023, insurers canceled nearly 2 million homeowner policies due to rising climate risks (more than four times the normal rate). Florida alone has had 36 presidential disaster declarations since 2000, with damages exceeding $300 billion in the last seven years according to NOAA.

Property Age Creates Insurance Challenges

Homes built before 1970 often trigger high-risk classifications due to outdated electrical systems, plumbing, and structural components. The Insurance Information Institute found in 2022 that properties with these aging infrastructures face coverage denials or significantly higher premiums. Roof age specifically matters most, with insurers typically requiring replacement for roofs over 20 years old. Credit scores also play a major role, as insurers use them to determine eligibility and rates.

Claims History and Property Features

Previous claims history becomes a permanent red flag, with homeowners who file multiple claims within five years often facing policy cancellations or premium increases of 30-40%. Swimming pools, certain dog breeds, and home-based businesses automatically increase risk classifications. Properties with outdated heating systems, knob-and-tube wiring, or structural damage from previous storms face immediate scrutiny. Insurers evaluate risk mathematically, not emotionally, which means you can address these specific factors through targeted improvements and proper disclosure to improve your coverage options.

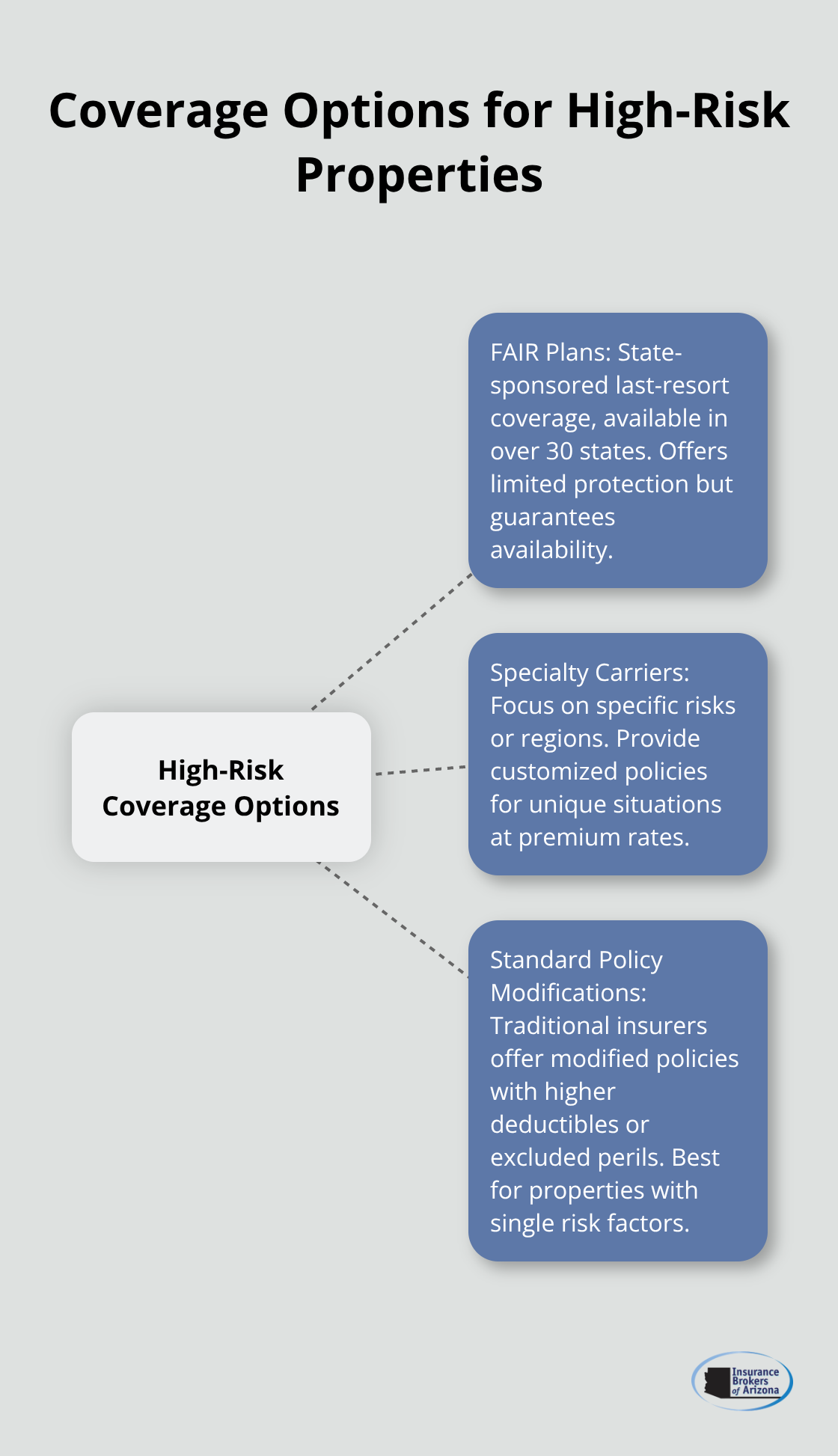

Coverage Options for High-Risk Properties

High-risk homeowners face three distinct insurance pathways, each with specific advantages and limitations. Standard homeowners insurance becomes unavailable once insurers classify your property as high-risk, which forces you into specialized markets with different rules and pricing structures. The average cost difference ranges from 20-50% higher than standard policies according to the National Association of Insurance Commissioners, but understanding your options prevents overpayment for inadequate coverage.

FAIR Plans Serve as Last-Resort Coverage

State-sponsored FAIR Plans operate in over 30 states as insurers of last resort when private companies refuse coverage. California’s FAIR Plan offers maximum coverage of $3 million for combined residential protections, though policies cover only specific perils like fire and smoke. These plans cost significantly more than private insurance but guarantee availability regardless of your property’s risk factors.

Florida homeowners report FAIR Plan premiums that average 40-60% above previous private coverage, yet these programs prevent complete loss of insurability. Difference in Conditions policies can supplement FAIR Plan coverage for broader protection against excluded perils.

Specialty Carriers Target High-Risk Properties

Companies like Foremost specialize in older properties and unusual risks that standard insurers decline, while others focus on specific geographic regions or property types. Surplus lines insurers operate outside standard regulations and offer customized policies for unique situations at premium rates. These carriers often require property inspections and risk mitigation measures before they issue coverage.

Chubb provides up to $100 million in personal liability coverage for high-value properties (demonstrating how specialty markets serve specific niches). Shopping among specialty carriers can reveal coverage options unavailable through traditional channels, though expect higher deductibles and stricter policy terms than standard homeowners insurance.

Standard Policy Modifications Bridge Coverage Gaps

Some traditional insurers offer modified standard policies with higher deductibles or excluded perils rather than complete coverage denial. These hybrid policies maintain relationships with established carriers while accommodating increased risk factors. Wind and hail exclusions commonly appear in coastal areas, while wildfire exclusions affect mountain and forest properties.

Modified policies often cost 15-25% less than specialty carriers but require separate coverage for excluded perils. This approach works best for properties with single risk factors rather than multiple high-risk characteristics. Understanding these cost structures helps you evaluate whether premium savings justify coverage gaps when you move to the next phase of cost analysis and reduction strategies.

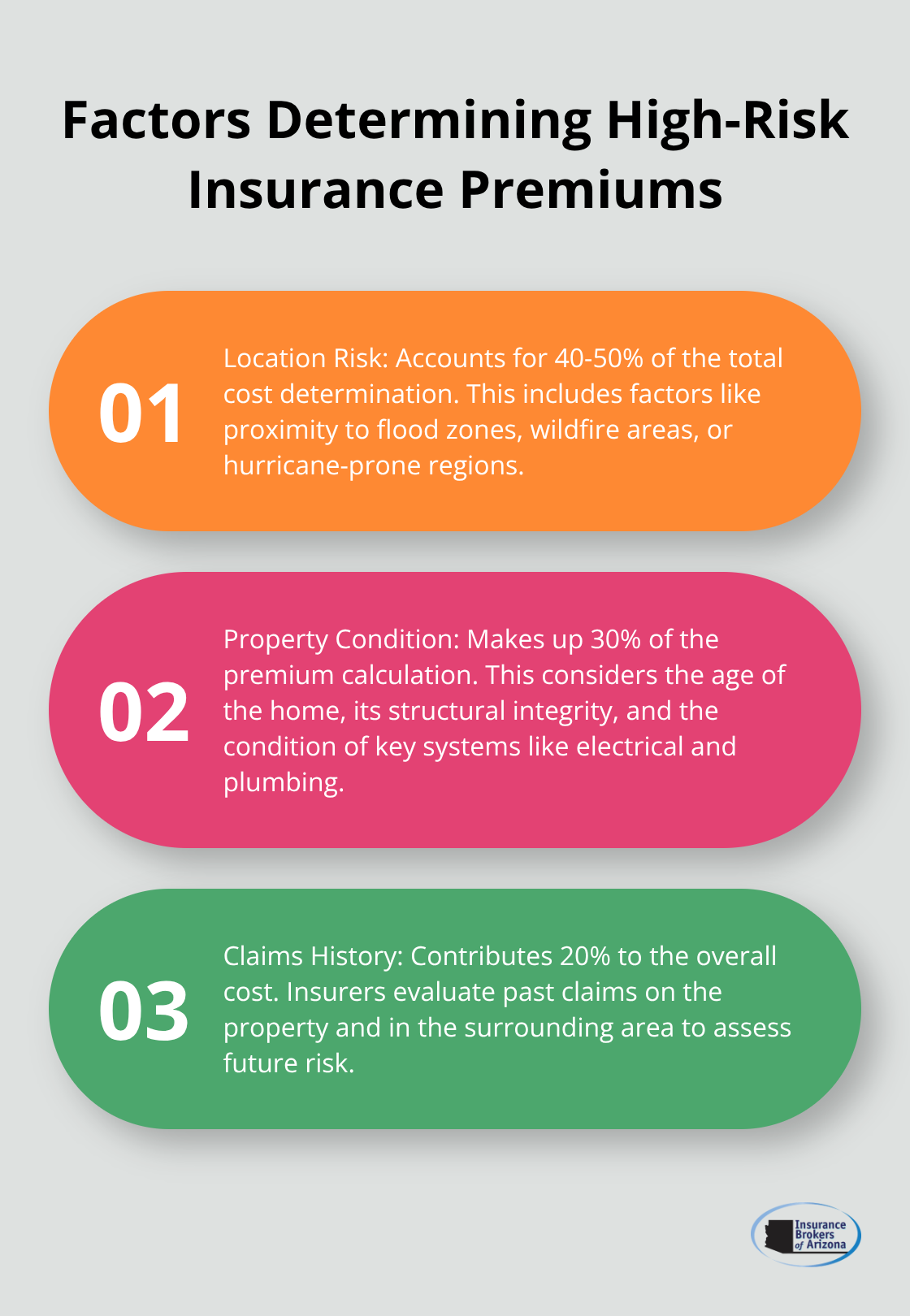

How Much More Will You Pay for High-Risk Coverage

High-risk homeowners face premium calculations that differ dramatically from standard policies. Insurers weigh location risk at 40-50%, property condition at 30%, and claims history at 20% of total cost determination. Florida homeowners report average premium increases of $1,450 from 2020 to 2023, while coastal properties in Special Flood Hazard Areas pay 20-50% above standard rates according to the National Association of Insurance Commissioners.

Your credit score impacts rates significantly, with lower scores that push premiums higher by 15-25% in most states. Insurers calculate replacement costs separately from purchase price, exclude land value but include upgraded materials and labor costs that often exceed original construction expenses.

Premium Calculation Methods Target Specific Risk Factors

Insurers use catastrophe models that analyze historical weather patterns, geological data, and property characteristics to determine rates. Properties within wildfire zones face automatic surcharges of 25-40% above base premiums, while flood zone locations trigger additional assessments through FEMA flood maps. Age-based pricing penalizes homes built before 1970 with rate increases of 15-30% due to outdated infrastructure.

Claims frequency models track neighborhood loss patterns over 10-year periods, which means your neighbors’ claims affect your rates even without personal claims history. Credit-based insurance scores (different from credit scores) incorporate payment history and debt levels to predict claim likelihood, with poor scores that add 20-35% to base premiums in states where this practice remains legal.

Strategic Home Improvements Cut Premiums Immediately

New roof installation reduces premiums by 10-20% instantly, while electrical system upgrades from knob-and-tube wiring lower rates by 15-30%. Storm shutters and reinforced materials qualify for disaster resistance discounts of 5-15% in hurricane zones. Security systems with monitored alarms provide discounts of 5-20% based on system sophistication.

Deductible increases from $500 to $2,500 can save up to 25% on premiums, though you must afford higher out-of-pocket costs when claims occur. Home and auto insurance bundles with the same carrier typically yield 5-15% discounts, while six-year loyalty with one insurer provides discounts up to 10%. Fire-resistant landscaping and defensible space maintenance can reduce wildfire premiums by 10-15% in high-risk areas.

Multiple Carrier Quotes Reveal Price Variations

Surplus lines insurers often provide competitive rates for unique properties that standard carriers reject outright. Specialty carriers like Foremost target older homes with customized rates that can beat traditional insurers by 15-25%. Price variations of hundreds or thousands of dollars exist between carriers for identical coverage, which makes comparison essential.

The Comprehensive Loss Underwriting Exchange report shows your property’s claim history to all insurers, so transparency about past issues prevents policy cancellations after discovery. Experienced brokers who understand high-risk markets identify carriers that write policies others decline and negotiate better terms than direct applications typically achieve.

Final Thoughts

High-risk home insurance demands strategic action and professional expertise to secure adequate coverage at fair rates. Properties in flood zones, wildfire areas, or with older infrastructure face premium increases of 20-50% above standard policies, yet coverage options exist through multiple channels. The solution centers on understanding your specific risk factors and addressing them systematically.

New roofs, electrical upgrades, and security systems deliver immediate premium reductions of 10-30%. FAIR Plans guarantee coverage when private insurers refuse applications, while specialty carriers often offer competitive alternatives for unique properties. Multiple carrier quotes reveal price variations of hundreds or thousands of dollars for identical coverage (making comparison shopping essential for cost savings).

We at Insurance Brokers of Arizona® help Arizona homeowners navigate complex high-risk markets and secure coverage that others cannot obtain independently. Document your property improvements and obtain quotes from multiple carrier types before making decisions. Professional guidance through specialized high-risk home insurance markets saves time and money while protecting your most valuable investment.