Arizona Homeowners Insurance Rates: What They Mean for Your Budget

Arizona homeowners insurance rates have climbed significantly in recent years, and understanding why matters for your wallet. At Insurance Brokers of Arizona®, we’ve helped countless homeowners navigate these increases and find ways to keep their premiums manageable.

This guide walks you through the factors pushing rates up, practical strategies to lower your costs, and how to plan your insurance budget for the long term.

Why Arizona Premiums Keep Rising

Arizona homeowners insurance premiums jumped 71% between 2020 and 2025, far outpacing the 26.4% inflation rate during the same period, according to LendingTree analysis reported by KTAR News. That gap matters because it means your insurance costs are climbing faster than your paycheck. Three concrete factors drive these increases, and understanding them helps you anticipate future changes and plan accordingly.

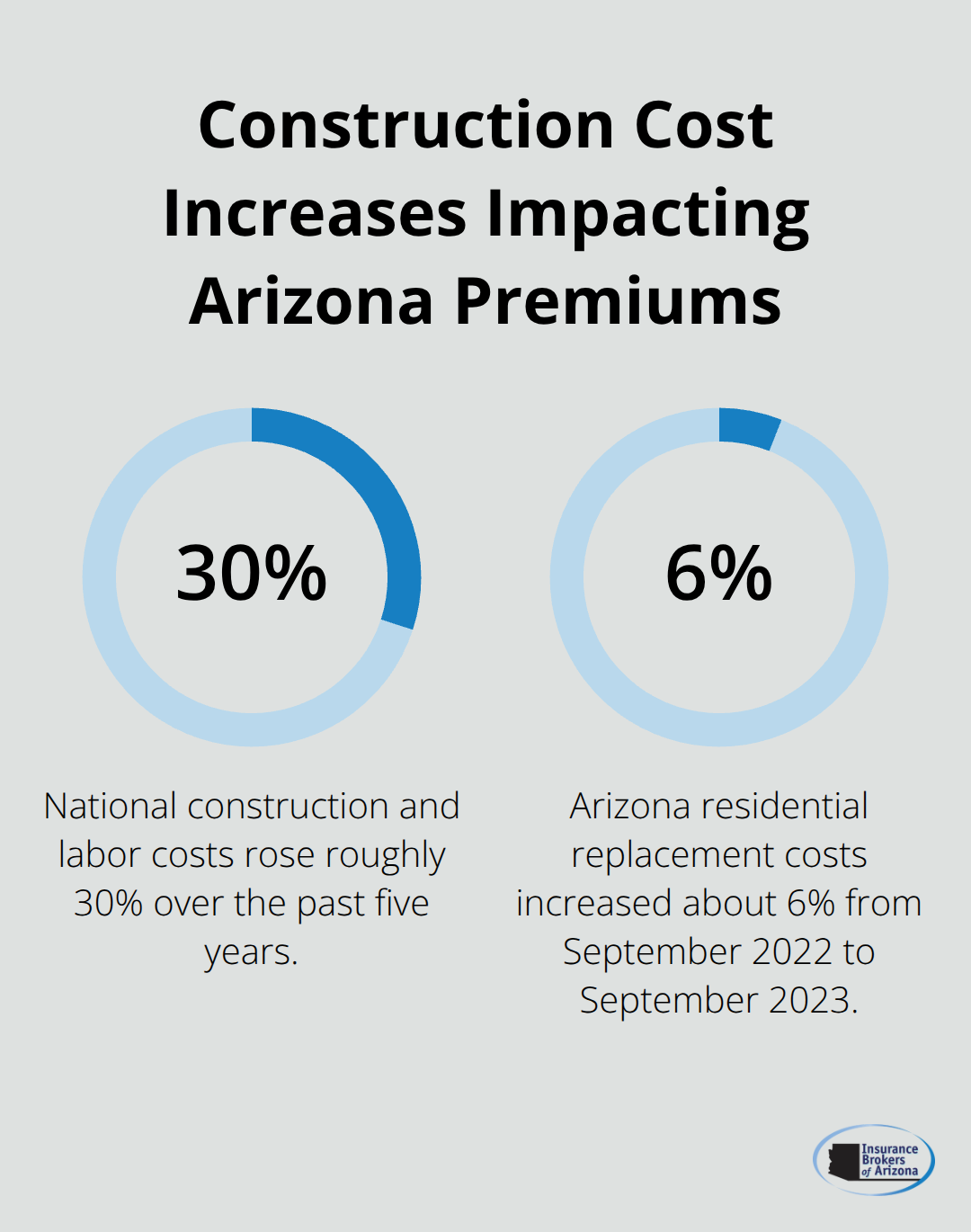

Construction Costs Have Surged Nationwide

Rebuilding your home after a loss costs significantly more than it did five years ago. National construction and labor costs have risen roughly 30% over the past five years, with Arizona specifically seeing residential replacement costs jump about 6% just between September 2022 and September 2023, according to Verisk data cited by the Arizona Department of Insurance and Financial Institutions.

When insurers calculate your dwelling coverage limit, they price in these higher rebuilding expenses. A home valued at $300,000 in Phoenix costs around $2,811 annually to insure, while the same home in nearby Gilbert runs about $2,087, partly reflecting different construction cost assumptions across the state. If your home is older or uses materials that are expensive to replace today, your premium reflects that reality. Insurers also factor in the cost to meet updated building codes during reconstruction, which can add thousands to repair bills after a major loss.

Wildfire and Weather Claims Drive Regional Pricing

Wildfire risk stands as the dominant force pushing Arizona premiums higher, especially for homes in wildland-urban interface areas. Beyond Arizona’s own fire losses, reinsurance costs for out-of-state fires also get passed to Arizona policyholders because insurers spread catastrophic risk across regions. Monsoon-induced flash floods and convective storms create similar pressure. In 2024, Arizona insurers paid out 55 cents for every dollar earned in claims, below the 66-cent industry average, suggesting aggressive pricing tied to wildfire exposure. The state’s ISO Public Protection Classifications show that 38 Arizona communities rank Class 8B or worse for fire protection capabilities, which raises premiums for homes in those zones. Fire mitigation matters here: homes with defensible space, fire-resistant materials, and proximity to reliable water sources cost less to insure. The Arizona Department of Insurance encourages participation in Firewise USA certification and FEMA preparedness programs to demonstrate lower risk and potentially negotiate better rates.

Market Structure Allows Carriers to Adjust Rates Quickly

Arizona’s use-and-file regulatory system lets insurers change rates immediately and file paperwork within 30 days, giving carriers flexibility to respond to loss experience and reinsurance costs faster than states with prior-approval rules. The state has over 100 licensed homeowners insurers, which sounds competitive but hasn’t prevented rate spikes because all carriers face similar wildfire and construction cost pressures. Rate increases in high-risk areas are common and justified by loss data, not just wildfire alone. This means shopping around matters more than ever, since different carriers price wildfire risk differently based on their claims history and reinsurance strategy. Understanding these rate drivers sets the stage for what you can actually control-and that’s where practical cost-reduction strategies come into play.

How to Cut Your Arizona Insurance Costs

Knowing why rates climb doesn’t lower your premium, but taking action does. The gap between Arizona’s 71% rate increase and the 26.4% inflation spike means you need a deliberate strategy to protect your budget. Three concrete moves reduce what you actually pay without sacrificing protection.

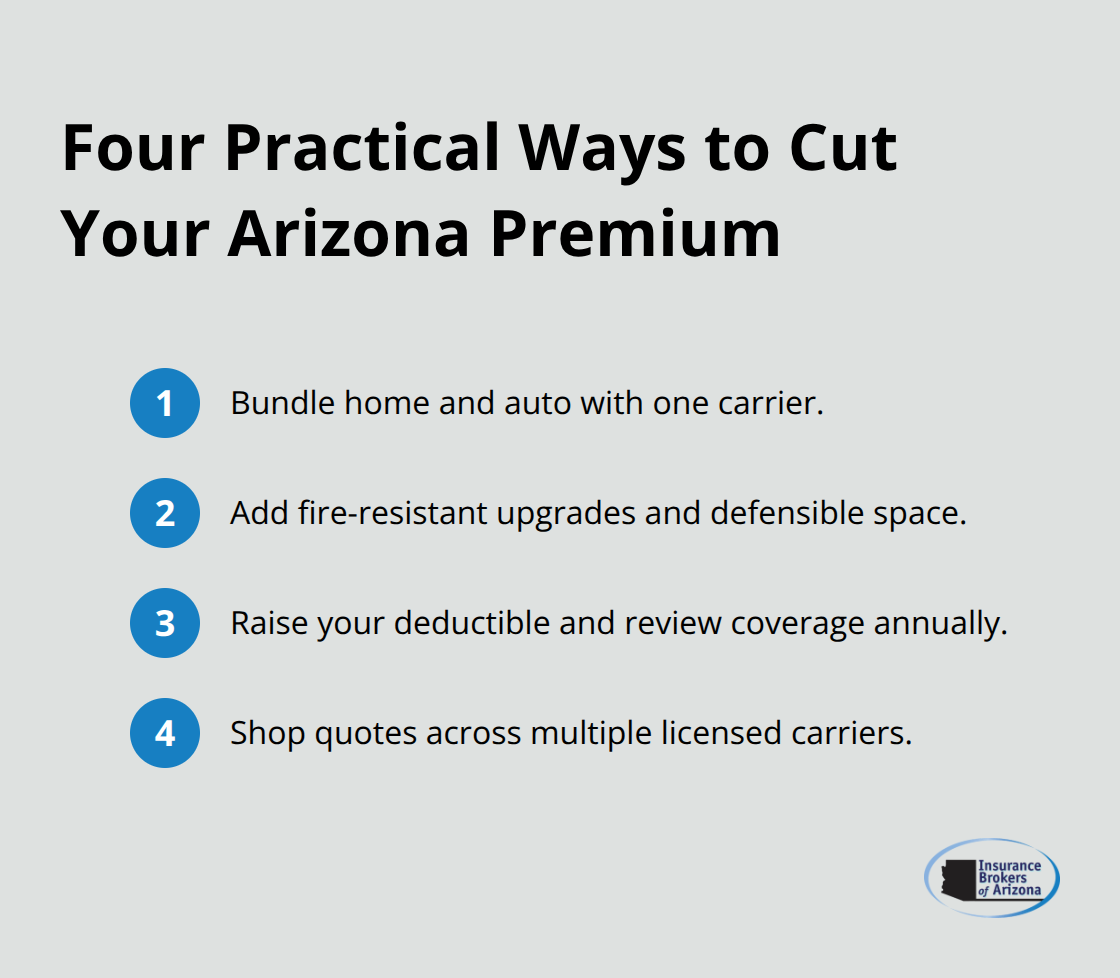

Bundle Your Policies for Immediate Savings

Combining your home and auto policies with the same carrier typically cuts your homeowners premium by 10% to 25%, depending on the insurer and your driving record. Most Arizona carriers offer multi-policy discounts automatically, but you need to ask and confirm the savings apply to your renewal. If you’ve been insuring your car and home separately, switching to one carrier can save hundreds annually. Insurance Brokers of Arizona® partners with over 40 reputable carriers, giving you access to multiple bundling options and competitive rates across different insurers.

Invest in Home Features That Lower Risk

Your home itself becomes a cost-reduction tool when you make strategic upgrades. Installing fire-resistant roofing materials, establishing defensible space around your property by clearing vegetation within 30 feet, and upgrading to impact-resistant doors and windows send clear signals to underwriters that you’re a lower-risk customer. The Arizona Department of Insurance notes that homes with these features qualify for discounts, and Firewise USA certification can further reduce your premium. These aren’t optional upgrades for wealthy homeowners; they’re practical investments that pay for themselves through lower insurance costs over time. A $2,000 roof upgrade that cuts your annual premium by $150 to $300 breaks even in seven to ten years while also protecting your home from actual fire damage.

Adjust Your Deductible and Review Coverage Annually

Your deductible choice and annual coverage review determine whether you leave money on the table. Raising your deductible from $500 to $1,000 typically reduces your annual premium by 15% to 20%, according to guidance from the Arizona Department of Insurance. That means a homeowner paying $2,400 annually could drop to roughly $1,920 by accepting a higher out-of-pocket cost when filing a claim. This works if you have savings to cover the deductible; if you don’t, stick with the lower deductible.

Review your dwelling coverage annually because Arizona replacement costs rose 6% between September 2022 and September 2023 alone, and skipping this step leaves you underinsured. Many carriers offer inflation guard endorsements that automatically increase your dwelling limit by 3% to 5% each year, preventing the slow drift into underinsurance that forces expensive increases later. Check whether your personal property coverage limits match your actual belongings; overinsuring low-value items wastes premium dollars. For high-value items like jewelry, firearms, or art, add a scheduled endorsement rather than relying on the standard personal property limit, which typically caps jewelry at $1,500 to $2,500.

Shop Quotes Across Multiple Carriers

Shopping quotes every two years matters more in Arizona’s volatile market than in stable states. Different carriers price wildfire risk differently based on their own claims experience, so your current insurer might be 20% to 30% higher than a competitor for the same coverage. The Arizona Department of Insurance and Financial Institutions maintains a license search tool where you can verify any carrier before getting a quote, ensuring you’re comparing prices from legitimate, regulated companies. This comparison process reveals which insurers value your specific risk profile most favorably and which ones have priced you out of the market.

Understanding Arizona’s Rate Volatility and Budget Planning

Arizona homeowners face a stark reality: premiums rose 71% from 2020 to 2025, creating a 44.6 percentage point gap between rate hikes and inflation, according to LendingTree analysis reported by KTAR News. This gap means your insurance costs accelerate faster than your income, which demands a shift in how you approach budgeting. The 2025 rate increase slowed to 3.6%, ranking 33rd nationally, suggesting the five-year surge may not continue at the same pace. However, this modest relief shouldn’t fool you into complacency.

Arizona’s market remains volatile because wildfire risk, reinsurance costs, and rising replacement expenses create unpredictable pressure on rates year to year.

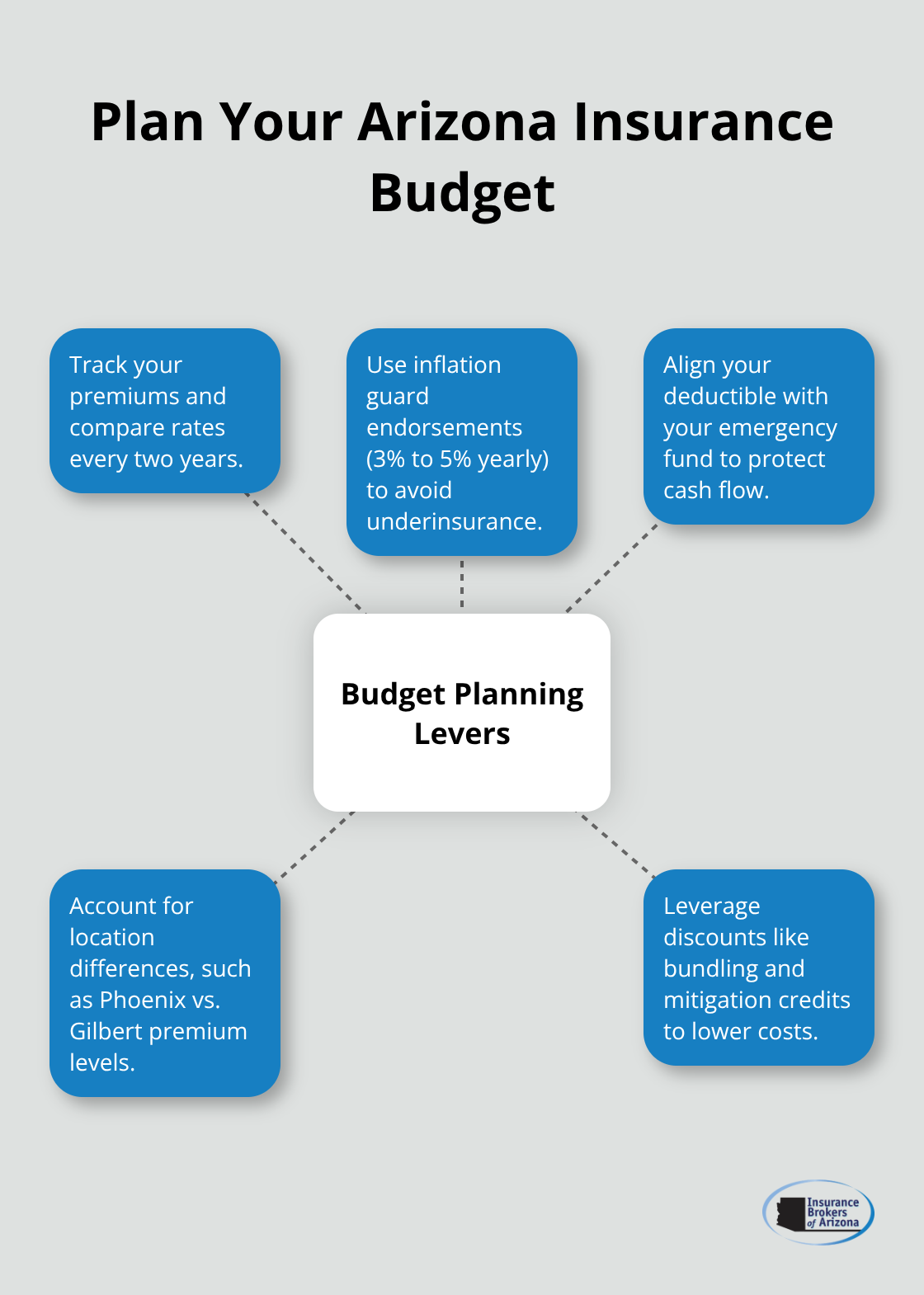

Track Premium Changes and Shop Regularly

The best defense is treating your insurance budget as dynamic, not static. Track your premium changes as renewal notices arrive, and compare what you pay against current market rates at least every two years. Different carriers price wildfire exposure differently based on their own claims history, meaning the insurer charging you $2,400 today might be 20% to 30% higher than a competitor offering identical coverage. This variance exists because some carriers accept more wildfire risk in Arizona than others, and some have experienced worse losses in recent years. Shopping quotes doesn’t mean switching carriers constantly; it means validating whether your current rate remains competitive in the market. Many homeowners stay with the same insurer for years without realizing they pay a premium for loyalty rather than receiving a fair price.

Account for Location-Based Premium Differences

Arizona costs vary significantly by location within the state. Phoenix typically runs higher than neighboring areas like Gilbert or Chandler because of different fire protection classifications and rebuilding cost assumptions. For a $300,000 home, annual premiums range from around $2,087 in Gilbert to $2,811 in Phoenix, according to Bankrate rate data from November 2025. These figures represent baseline estimates; your actual premium depends on your roof age, construction type, claims history, and specific ZIP code. The practical step is calculating what percentage of your annual housing budget insurance consumes, then setting that figure as your ceiling. If insurance costs more than 1.5% of your home’s value annually, you’re paying above the Arizona average and should investigate whether rate reductions are available through coverage adjustments or carrier changes.

Use Inflation Protection to Prevent Underinsurance

Inflation guard endorsements automatically increase your dwelling coverage by 3% to 5% yearly, protecting you against underinsurance without requiring annual policy reviews (though they add slightly to your premium). The math works in your favor: a $150 annual increase from inflation guard prevents the shock of discovering you’re underinsured by $50,000 when you file a claim after five years of rising replacement costs. Arizona replacement costs rose 6% between September 2022 and September 2023 alone, and skipping this step leaves you exposed to significant gaps in coverage.

Align Your Deductible with Your Financial Capacity

Long-term budget planning means accepting that deductible choices change as your financial situation evolves. The $1,000 deductible that saves you $300 annually only makes sense if you have liquid savings to cover it; if an unexpected claim would strain your finances, the lower deductible protects your cash flow despite the higher premium. Review this decision annually alongside your emergency fund balance to ensure your choice matches your actual financial capacity.

Final Thoughts

Arizona homeowners insurance rates have climbed faster than inflation, and that reality demands action rather than acceptance. The 71% increase from 2020 to 2025 shows that waiting for rates to stabilize wastes money you could save today. Your budget improves when you treat insurance as an active decision, not a passive bill you pay annually without question.

Start by reviewing your dwelling limit to confirm it matches today’s replacement costs, not what your home was worth five years ago. Check whether your deductible aligns with your financial capacity to handle a claim without hardship. Confirm that bundling your home and auto policies applies to your renewal quote, since many carriers require you to request this discount explicitly. These steps take a few hours but often reveal $300 to $600 in annual savings.

We at Insurance Brokers of Arizona® understand that navigating Arizona homeowners insurance rates feels overwhelming when premiums keep climbing. We partner with over 40 reputable carriers, which means we handle the comparison process and identify which carriers offer the best rates for your specific situation. Contact Insurance Brokers of Arizona® to review your current policy and explore how much you could save by switching carriers or adjusting your coverage.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.