How to Handle Water Damage with Home Insurance Coverage

Water damage is one of the most common and costly claims homeowners face, yet many people don’t fully understand what their home insurance actually covers. At Insurance Brokers of Arizona®, we’ve seen firsthand how confusion about water damage coverage leads to denied claims and financial hardship.

The difference between covered and excluded water damage can mean thousands of dollars in out-of-pocket costs. This guide walks you through exactly what to do if water damage strikes your home.

What Your Home Insurance Actually Covers for Water Damage

Your standard homeowners policy covers water damage only when it results from sudden, accidental events tied to a named peril. Burst pipes, overflowing appliances, roof leaks from wind damage, and water used to extinguish fires typically qualify for coverage. However, the Insurance Information Institute reports that water damage and freezing claims account for 29.4% of all homeowners insurance claims, yet most homeowners misunderstand what actually triggers coverage. The key distinction is suddenness and accident. A pipe that bursts overnight qualifies; a slow, undetected leak from years of neglect does not. If damage originates inside your home from plumbing or appliances and happens suddenly without warning, you’re likely covered. The average water damage claim costs around $13,954 according to the Insurance Information Institute, which makes understanding these rules essential before disaster strikes.

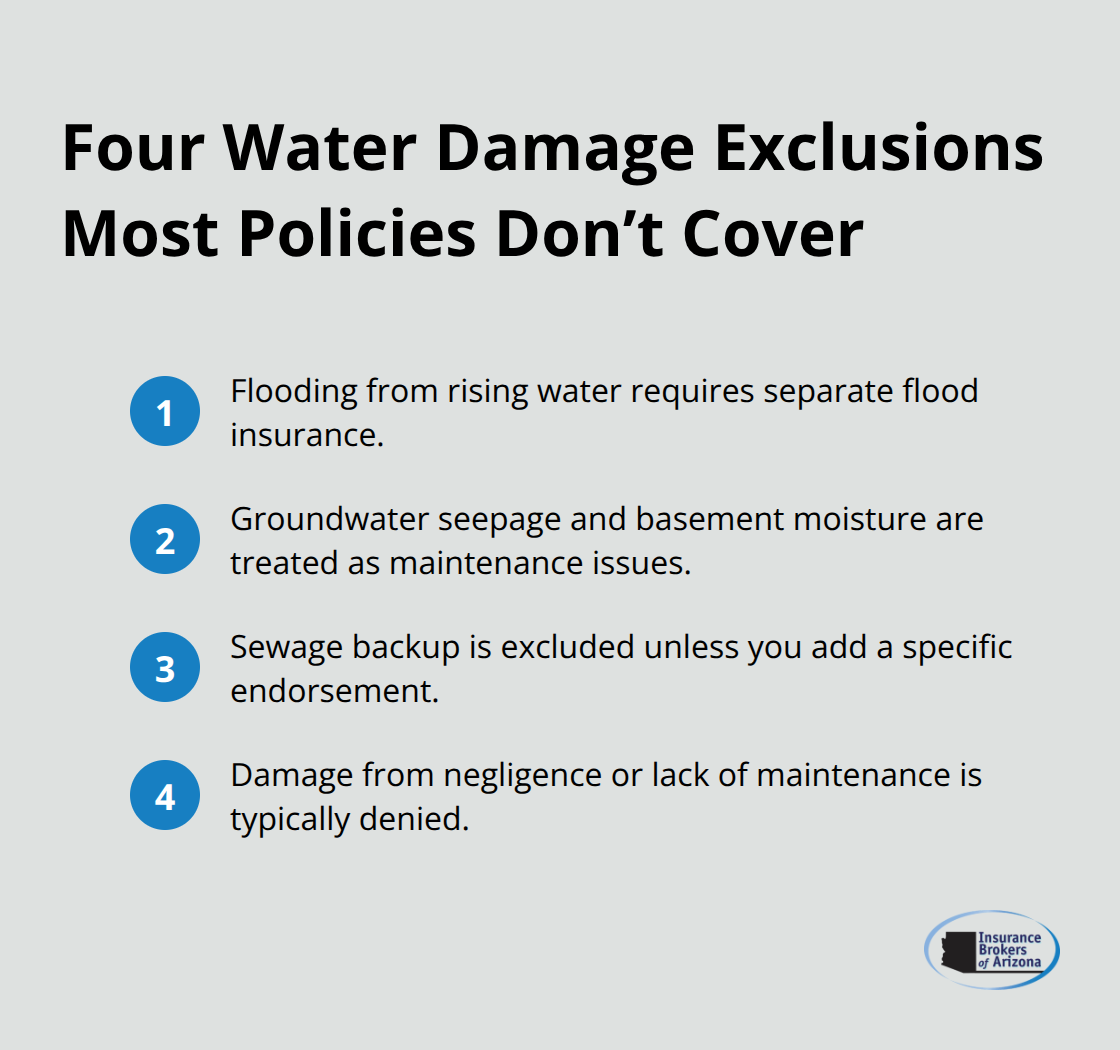

Four Major Exclusions That Catch Most Homeowners Off Guard

Your policy almost certainly excludes four major water damage scenarios. Flood damage stands as the biggest one-standard policies simply do not cover it, which is why roughly 1 in 60 insured homes file water damage claims annually. If you live in a flood zone or near water, you need separate flood insurance through the National Flood Insurance Program or a private insurer. Groundwater seepage and basement moisture fall outside coverage because insurers classify them as maintenance issues, not sudden events. Sewage backup from clogged drains remains excluded unless you add a specific endorsement, yet this scenario can cost $500 to $1,000 per incident. Damage caused by negligence or lack of maintenance-such as frozen pipes because you failed to heat your home in winter-also gets denied.

These exclusions appear in nearly every policy nationwide, so don’t assume your coverage extends beyond what your agent explicitly states.

How Limits and Deductibles Shape Your Actual Payout

Coverage limits determine the maximum your insurer pays, and they vary significantly by policy. Dwelling coverage pays for structural repairs up to your limit; personal property coverage pays for damaged belongings, often with lower sub-limits on specific items like electronics or jewelry. Your deductible is what you pay out of pocket before insurance kicks in, and choosing a higher deductible ($1,000 instead of $500) lowers your premium but increases your financial responsibility. If your dwelling limit is $300,000 but water damage costs $50,000 to repair, you’re covered in full minus your deductible. However, if your limit is only $200,000 and damage reaches $250,000, you absorb the $50,000 shortfall yourself. Review your limits annually with your agent because home values and replacement costs change. Try matching your dwelling limit to current rebuilding costs in your area, not just your home’s market value, since rebuilding often costs more than what you’d sell the house for.

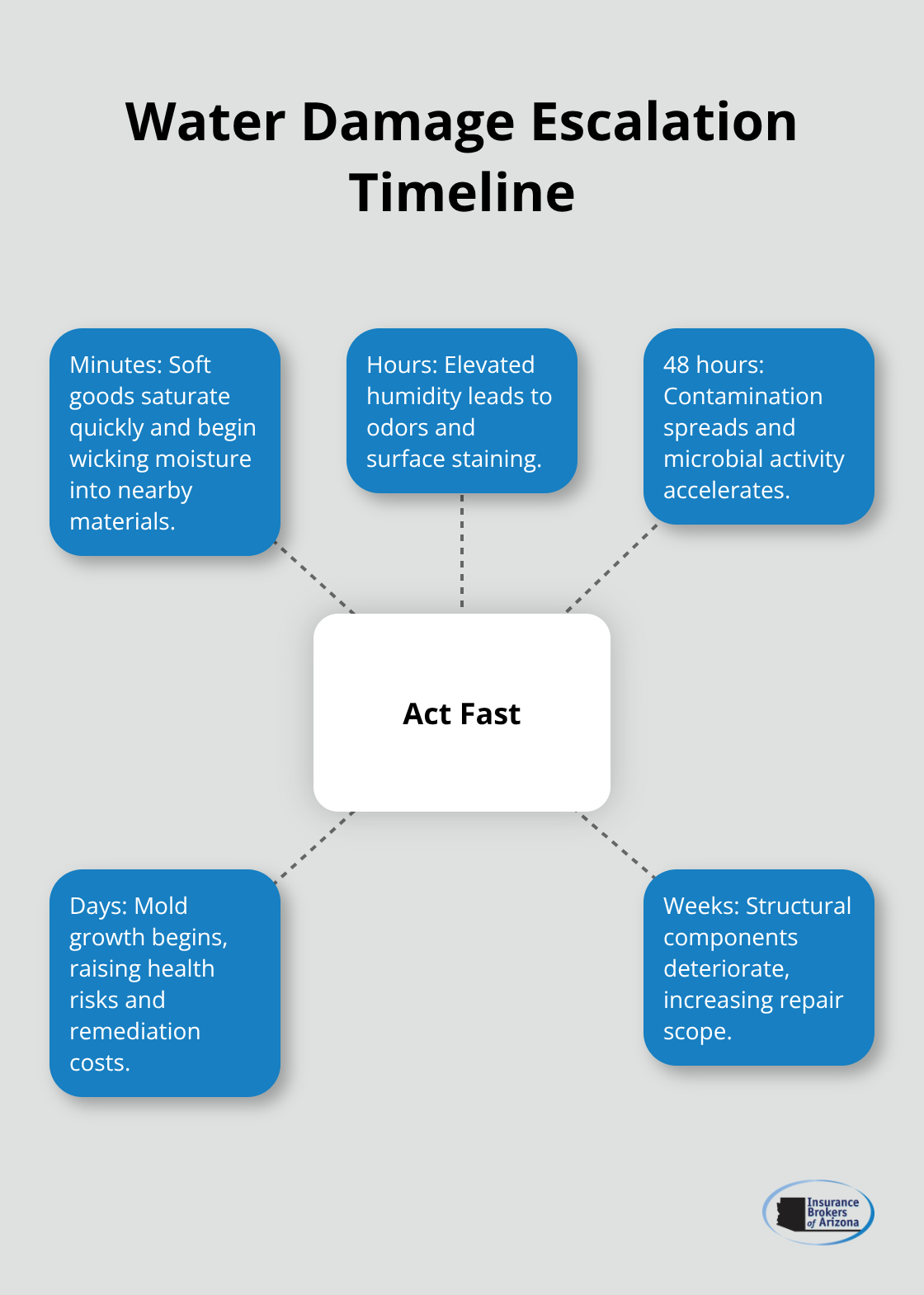

Why You Need to Act Fast After Water Strikes

Water damage escalates rapidly once it occurs. Carpets and furnishings soak within minutes; humidity causes odors within hours; contamination spreads within 48 hours; mold develops within days; structural deterioration follows within weeks. The longer you wait, the more expensive the restoration becomes and the greater the risk of permanent loss.

Contact your insurance agent immediately after water damage occurs-many carriers offer 24/7 claim support-because delays can affect coverage decisions and increase out-of-pocket costs. Your next step involves preventing further damage while waiting for assessment, which protects both your home and your claim.

What to Do Immediately After Water Damage Strikes

The first hours after water damage occurs determine whether you’ll recover most of your losses or face thousands in uninsured costs. Stop the water source immediately if it’s safe to do so-turn off the main water valve or individual supply stops to prevent further flooding. This single action saves far more money than almost anything else you can do when water actively spreads through your home.

Document Damage Before It Worsens

Photograph and video everything before water spreads further or your possessions dry out. Capture wide shots of affected rooms, close-ups of damaged items (including brand names and model numbers), and interior shots showing moisture on walls and floors. Open drawers and cabinets to document contents because your policy covers those items too, though many homeowners forget to photograph them. Document your property and belongings systematically within the first few hours, as this becomes critical evidence if your claim gets questioned later and helps your adjuster assess damage accurately.

Contact Your Insurer Without Delay

Call your insurance agent or carrier immediately after securing these photos. Most major insurers offer 24/7 claim lines because water damage claims genuinely cannot wait until business hours. Delays of even a few hours can affect coverage decisions, especially regarding mold remediation, since mold begins developing within 24 to 48 hours according to FEMA. Provide your agent with the address, description of the damage source, and approximate square footage affected so they can dispatch an adjuster quickly and authorize emergency water removal if needed.

Prevent Additional Damage Without Disturbing Evidence

While waiting for your adjuster, prevent additional damage without disturbing the scene. Turn off electricity to affected areas if water is present, but do not move damaged items or start cleanup yourself. Remove standing water only if it poses a health risk or safety hazard, and do this minimally. Contact a licensed water damage restoration company to remove water and dry surfaces professionally, as this prevents mold growth and structural deterioration far better than DIY efforts. Verify the restoration company holds proper licensing and insurance before hiring them. Move undamaged valuables from nearby areas to prevent secondary damage, but photograph their original locations first.

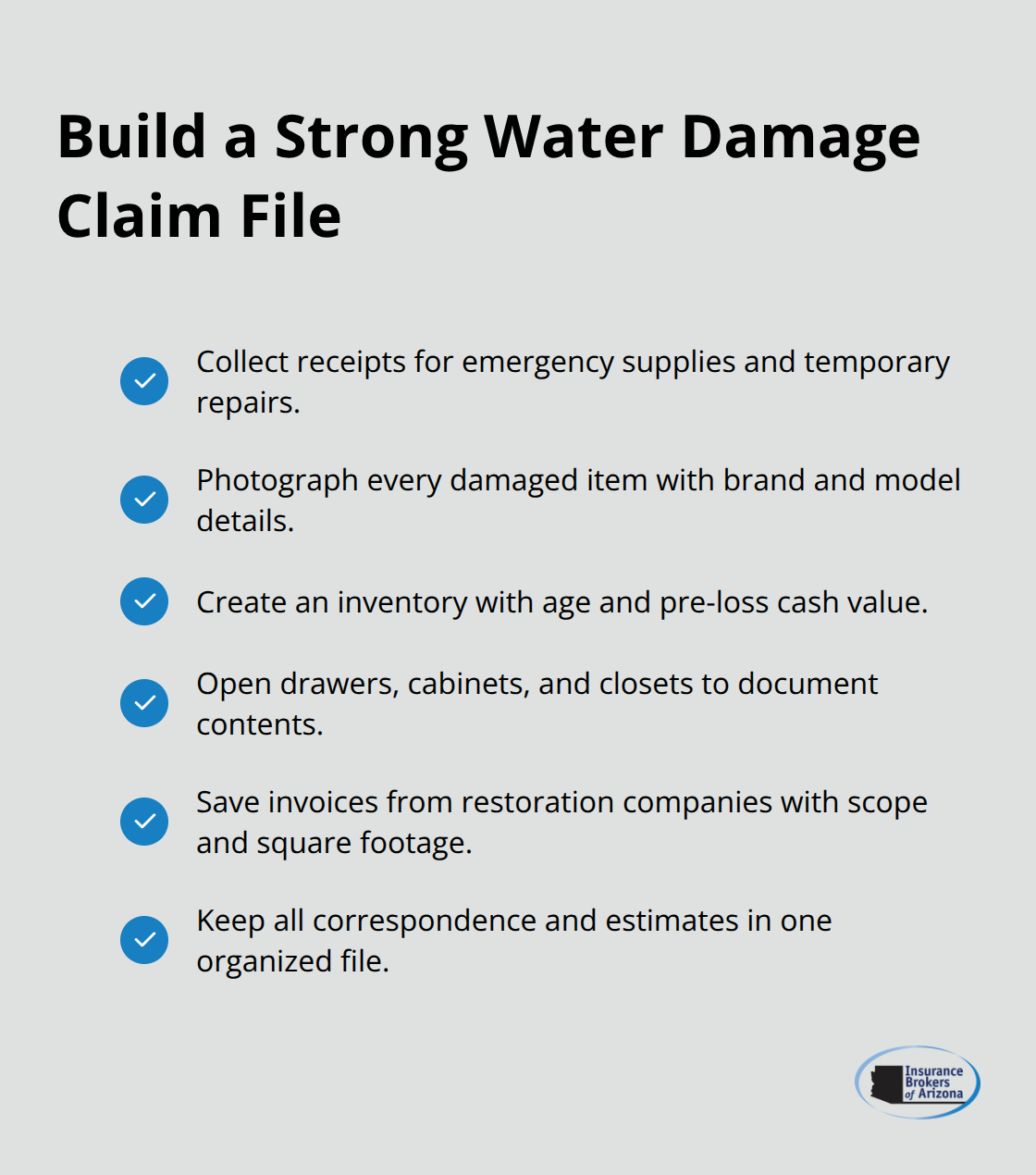

Understand Your Coverage and Organize Records

Some policies cover temporary living expenses if evacuation becomes necessary, so understand your loss-of-use coverage limits and documentation requirements. Do not assume you must use the restoration company your insurer recommends-you can hire your own contractor as long as they’re licensed and insured. Keep receipts for any emergency supplies or temporary repairs you purchase, as these often qualify for reimbursement. Document everything in a claim file with photos, receipts, contractor estimates, and copies of all correspondence with your insurer. This organization streamlines processing and prevents disputes over what was damaged or what repairs cost. Your adjuster will assess the damage, review your documentation, and determine your payout based on your coverage limits and deductible, so thorough documentation strengthens your position throughout the entire claims process.

Filing Your Water Damage Claim

Start building your claim file the moment water damage occurs because disorganized documentation costs you money and delays settlements. Collect receipts for any emergency supplies, temporary repairs, or restoration services you purchase immediately after damage strikes. Photograph damaged items with clear shots showing brand names and model numbers, then create a detailed inventory listing each item, its approximate age, and estimated cash value before damage. Open every drawer, cabinet, and closet to photograph contents because standard homeowners policies cover belongings inside furniture, yet most homeowners miss documenting these items and lose reimbursement. If you hired a water damage restoration company, keep their invoice showing what work they performed and the square footage they treated, as this becomes critical evidence when your adjuster assesses damage severity.

The Insurance Information Institute reports that water damage claims average around $13,954, and thorough documentation directly influences whether you receive full reimbursement or face coverage disputes that drag on for months.

Meet Your Adjuster and Establish Fair Assessment

Your insurance company will assign an adjuster to inspect damage and determine your payout based on your policy limits, coverage type, and deductible amount. Schedule this inspection as soon as possible because delays allow mold to develop and structural damage to worsen, which complicates claims and potentially creates coverage disputes over whether new damage falls within your original claim or represents separate damage. When the adjuster arrives, walk through affected areas with photos and your inventory in hand, pointing out all damaged items and explaining the damage source clearly. Do not accept the adjuster’s initial estimate if it seems low compared to contractor quotes you’ve obtained independently; request a detailed breakdown of their assessment and ask them to explain any discrepancies between their estimate and your own. Some adjusters rush through inspections, so comprehensive documentation forces them to address specific items rather than providing blanket assessments. You hold the right to hire your own independent adjuster at your expense if you believe the insurance company’s assessment is unfair, though this makes sense only for major claims exceeding $10,000 where the additional cost justifies the potential recovery increase.

Understand Deductibles and Settlement Structures

Your deductible is the amount you pay out of pocket before insurance coverage begins, and this directly reduces your settlement check. If your deductible is $1,000 and the adjuster determines your damages total $15,000, your insurance company pays $14,000 and you cover the $1,000 difference. Some policies apply a percentage deductible instead of a fixed dollar amount, meaning you pay a percentage of your home’s insured value rather than a flat fee. Insurance companies often issue settlement checks as loss drafts payable to both you and your mortgage lender simultaneously, requiring your lender’s endorsement before you can access funds. This protects lenders from homeowners who receive settlement money but fail to complete repairs, leaving the property unrepaired while the mortgage continues. If your lender requires a post-repair inspection before releasing final funds, plan for this delay when budgeting your out-of-pocket costs and contractor timeline.

Negotiate Like-Kind Replacement and Challenge Depreciation

Negotiating with your adjuster matters significantly because you can request like-kind replacement rather than accepting depreciation reductions, particularly for items damaged beyond reasonable wear and tear. If your adjuster applies depreciation to items you believe warrant full replacement cost, push back with evidence showing the item’s original purchase price and photos demonstrating it was well-maintained before damage occurred. Many homeowners accept initial estimates without question, but your policy entitles you to fair settlement based on actual replacement costs (not depreciated values) for items that were in good condition before the loss. Request a detailed breakdown of how the adjuster calculated depreciation for each major item, and provide your own estimates from retailers or contractors if their figures seem inflated or unreasonably low.

Final Thoughts

Prevention stops water damage before it starts, which costs far less than filing claims and dealing with repairs. You should schedule roof and gutter inspections twice yearly-once in spring and again in fall-to catch deteriorating flashing, missing shingles, or debris buildup before heavy rains arrive. Clean gutters thoroughly after storms and ensure downspouts direct water at least six feet away from your foundation, as water pooling near your home creates basement moisture and foundation damage that standard policies won’t cover.

Install a sump pump in your basement if you experience any moisture, and pair it with a battery backup system so it operates during power outages when water damage risk peaks. Water detection sensors placed near water heaters, washing machines, and under sinks alert you to leaks within minutes rather than hours or days, giving you time to shut off water before significant damage spreads. Some insurance carriers offer discounts for installing these devices, so ask your agent whether your home insurance and water damage coverage qualifies for premium reductions that offset installation costs.

Review your home insurance coverage annually because property values and replacement costs change constantly. You should verify your dwelling limits match current rebuilding costs in your area, not just your home’s market value, and confirm you have adequate personal property coverage for your belongings. Contact Insurance Brokers of Arizona® to review your current coverage and identify any gaps that could leave you vulnerable to water damage losses.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.