How to Find the Best Auto and Home Insurance Bundle

Finding the best auto and home insurance bundle can save you hundreds of dollars annually while simplifying your coverage management.

Most carriers offer bundle discounts ranging from 5% to 25%, but the cheapest option isn’t always the smartest choice. We at Insurance Brokers of Arizona® see clients make costly mistakes by focusing solely on price rather than comprehensive protection.

The right bundle strategy requires careful evaluation of coverage limits, deductibles, and potential gaps between policies.

What Does Insurance Bundling Actually Include

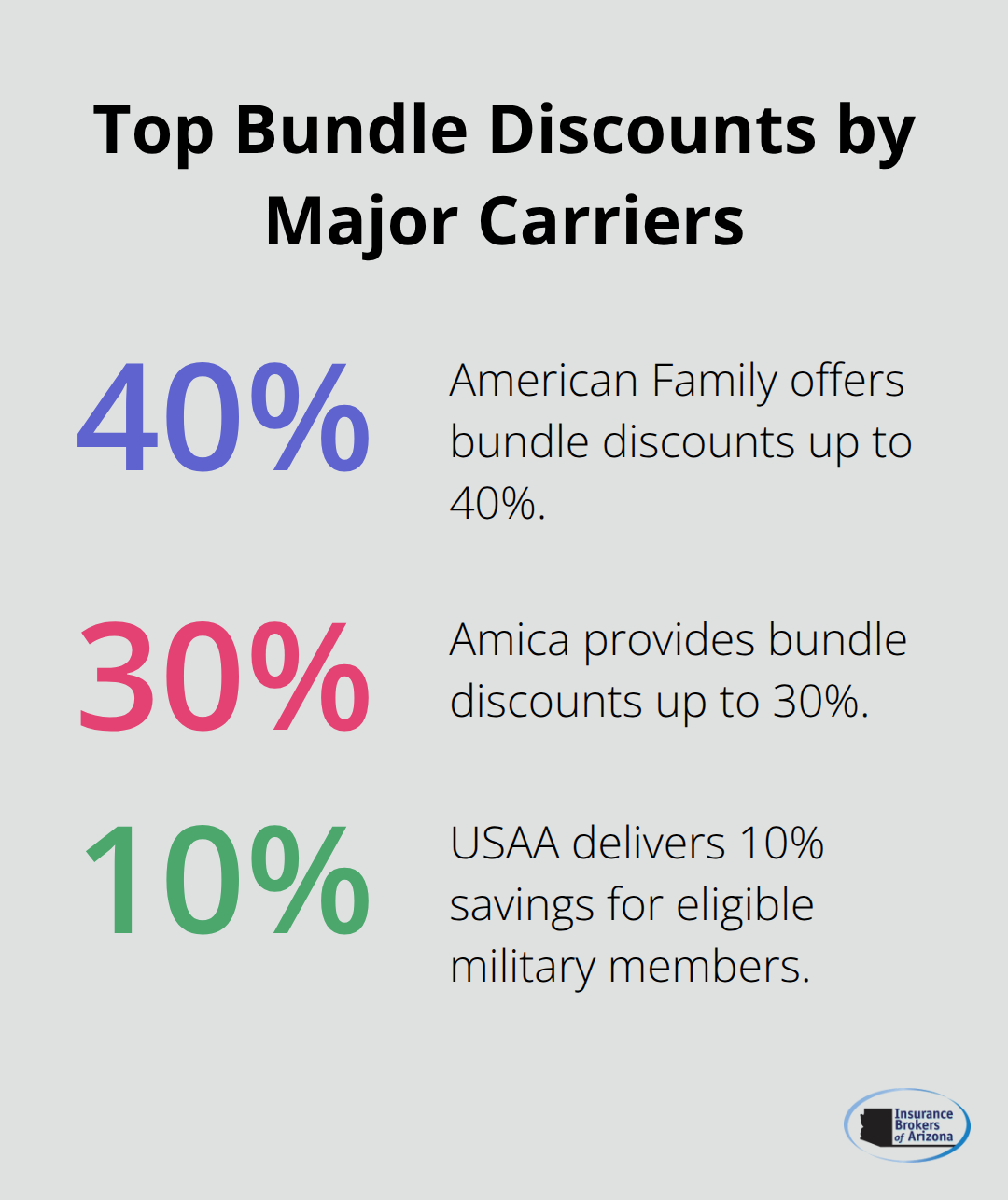

Insurance bundling combines your auto and home policies under one carrier to receive multi-policy discounts. American Family leads with bundle discounts up to 40%, while State Farm offers savings that reach $1,356 annually according to industry analysis. Amica provides discounts up to 30%, and USAA delivers 10% savings for eligible military members.

Progressive offers over 20% discounts for new customers who purchase bundled policies.

Standard Bundle Components

Most bundles include comprehensive auto coverage with liability, collision, and comprehensive protection alongside homeowners insurance that covers your home, personal property, and liability protection. Carriers often add roadside assistance, rental car coverage, and identity theft protection as bundle perks. Some insurers like Nationwide allow single deductibles when both home and auto claims stem from the same incident (which streamlines the claims process significantly).

Hidden Bundle Limitations

Bundles restrict your ability to shop individual policies with specialized carriers that might offer superior coverage for specific needs. Classic car insurance, high-value home coverage, or specialty vehicle protection often requires separate specialized policies that bundled carriers cannot match. Additionally, some multi-policy discounts only apply during the first policy year (which makes long-term savings less predictable than advertised rates suggest).

Real Savings vs Marketing Claims

Industry data shows bundles save 5% to 25% on premiums, but individual policies sometimes cost less than bundles depending on your risk profile. Travelers and USAA consistently rank highest for bundle value, while some carriers inflate bundle discounts after they raise individual policy prices first. Compare separate policy quotes from at least three providers against bundle offers to identify genuine savings rather than marketing manipulation.

Coverage Gaps in Standard Bundles

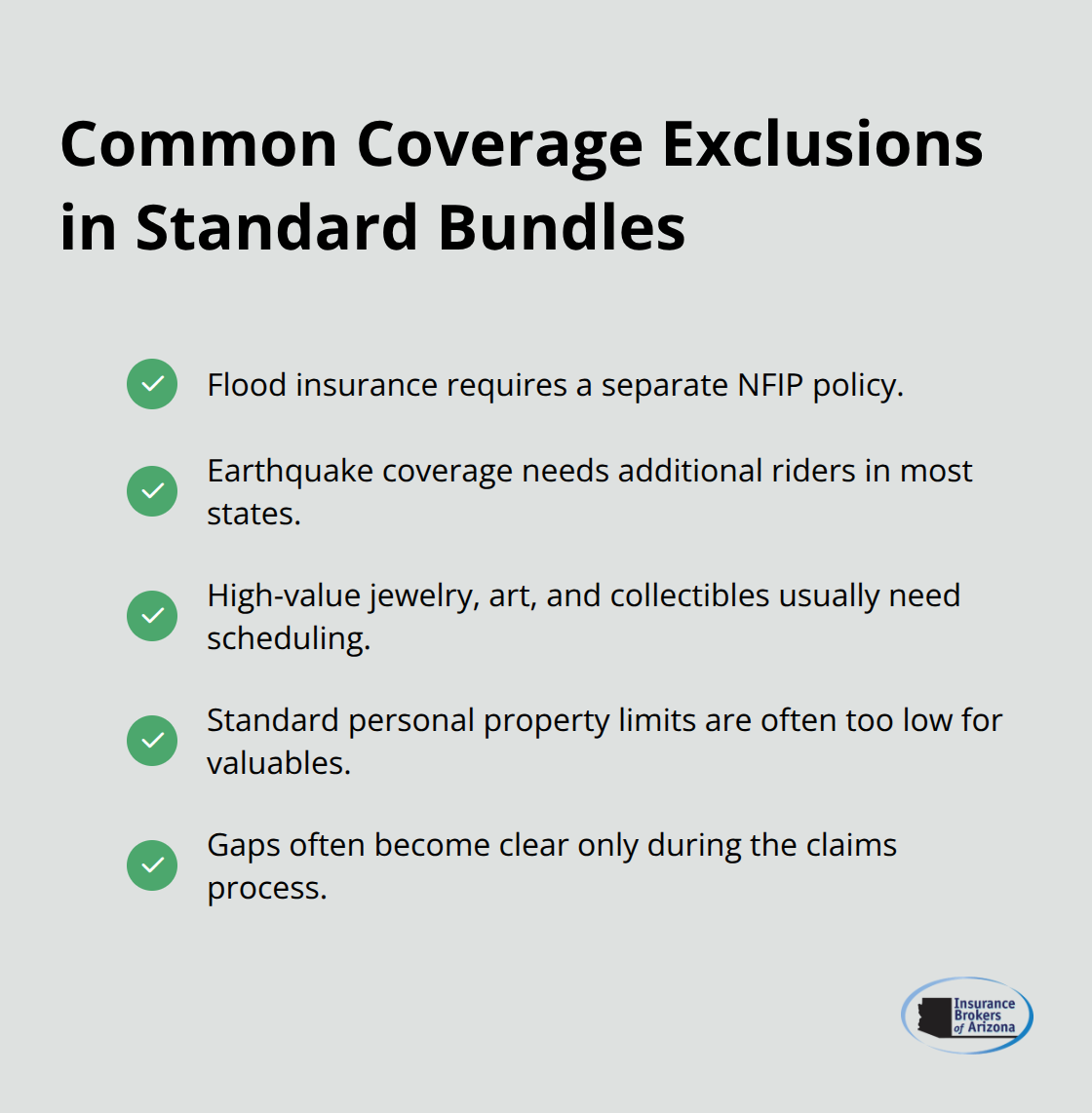

Standard bundles often exclude specialized coverage that many homeowners need. Flood insurance requires separate policies through the National Flood Insurance Program, while earthquake coverage needs additional riders in most states. High-value items like jewelry, art, or collectibles typically exceed standard personal property limits (requiring scheduled personal property endorsements).

These gaps become apparent only when you file claims and discover your bundle doesn’t cover specific losses.

Now that you understand what bundles include and exclude, the next step involves comparing these options effectively across multiple carriers.

How Do You Compare Bundle Options Properly

Effective bundle comparison requires systematic evaluation of coverage limits, deductibles, and claims procedures across multiple carriers. Start with coverage limits analysis since many insurers offer different liability amounts and dwelling coverage caps within their bundle packages. State Farm’s bundle analysis shows their liability limits often exceed competitors by $100,000 to $300,000, while Amica provides replacement cost coverage as standard where others offer actual cash value. Request detailed declarations pages from each carrier to compare identical coverage rather than rely on marketing summaries that obscure important differences.

Critical Questions That Expose Bundle Quality

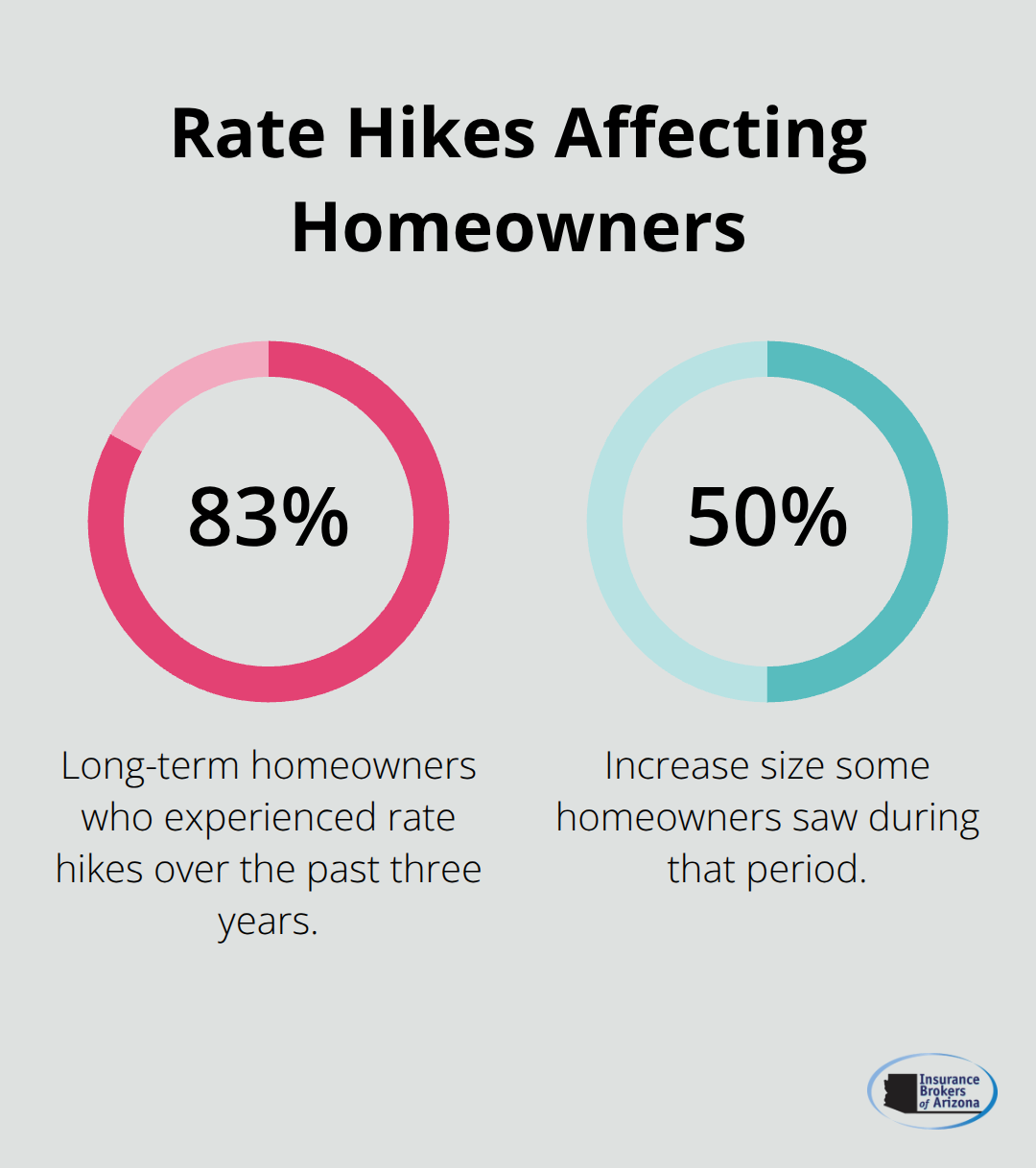

Ask each insurer about their claims timeline and whether they use third-party administrators for bundled policies, since some carriers outsource home claims while they manage auto claims internally. Progressive uses different claim adjusters for home versus auto (which can complicate coordination during incidents that affect both policies). Demand specific information about rate increase patterns over the past three years, as Consumer Reports data shows 83% of long-term homeowners experienced rate hikes with some seeing 50% increases. Question whether bundle discounts remain consistent after the first year or if they decrease over time, since many carriers reduce multi-policy savings during renewals.

Comparison Tools That Actually Work

Use your state’s insurance department website for complaint ratios and financial strength ratings rather than rely on company-sponsored comparison sites. J.D. Power ratings provide objective customer satisfaction scores, showing Amica consistently ranks highest for homeowners satisfaction while USAA provides exceptional bundling discounts for eligible members. Request quotes from independent agents who can access multiple carriers simultaneously, as they often identify better individual policy combinations than bundled options. Compare total annual costs that include all fees and surcharges, not just base premiums, since some carriers add administrative fees that negate advertised bundle savings.

Red Flags That Signal Poor Bundle Value

Watch for carriers that require higher deductibles on bundled policies compared to individual coverage options. Some insurers inflate bundle discounts after they raise individual policy prices first (making the savings appear larger than they actually are). Avoid companies that cannot provide clear explanations of coverage differences between their bundle and individual policies. Question any insurer that pressures you to decide immediately or claims their bundle discount expires within days, as legitimate carriers maintain consistent discount structures throughout their quote periods.

Even the most thorough comparison process can lead to expensive mistakes if you overlook common bundling pitfalls that trap many policyholders.

What Bundle Mistakes Cost You the Most Money

Price-focused decisions without coverage examination lead to expensive surprises during claims. Consumer Reports analysis reveals that 24% of homeowners who prioritized price over protection discovered critical gaps when they filed claims, with flood damage as the most common exclusion that costs property owners $15,000 to $40,000 out of pocket. Many carriers advertise bundle discounts while they simultaneously reduce coverage limits or increase deductibles on individual policy components (which makes the apparent savings misleading). State Farm and Progressive frequently bundle policies with higher auto deductibles than their standalone options, while Allstate often reduces dwelling coverage limits in bundled homeowners policies compared to individual purchases.

Coverage Gaps That Drain Your Savings Account

Standard bundles exclude earthquake coverage in 42 states, flood protection nationwide, and scheduled personal property coverage for items that exceed $2,500 in value. Travelers bundles typically cap jewelry coverage at $1,500 per item while their individual homeowners policies allow $5,000 limits, which creates a $3,500 exposure gap for engagement rings or watches. Auto portions of bundles often exclude rideshare coverage, gap insurance, and new car replacement benefits that standalone policies include as standard features. These exclusions become costly when you need rental car coverage for 30 days after an accident but your bundle only provides 10 days, which forces you to pay $600 out of pocket for extended transportation.

Annual Review Mistakes That Compound Over Time

Homeowners insurance premiums increased 24% over three years according to the Consumer Federation of America, but many bundled customers never compare alternatives because they assume their multi-policy discount still provides value. Amica customers who reviewed their bundles annually saved an average of $400 when they switched individual policies to specialized carriers while they maintained their auto coverage (which proves that bundle loyalty costs money when market conditions change). Rate increases affect bundle components differently, with home insurance often rising faster than auto coverage, which makes your original bundle calculation obsolete within two years.

Price Manipulation Tactics That Hide True Costs

Carriers inflate individual policy prices before they offer bundle discounts, which creates artificial savings that disappear when you compare quotes from multiple companies. Progressive and Allstate frequently raise standalone auto rates by 15% to 20% before they introduce bundle promotions that appear to save money. Some insurers require annual payment in full for bundled policies while they allow monthly payments for individual coverage, which increases your upfront costs despite advertised savings. These tactics work because most consumers compare bundle prices against the same carrier’s individual rates rather than shop across multiple companies for the best standalone options.

Final Thoughts

Experienced insurance brokers eliminate the guesswork from your search for the best auto and home insurance bundle. We at Insurance Brokers of Arizona® compare genuine bundle savings against individual policy options across multiple carriers. This approach prevents the price manipulation tactics that cost consumers thousands annually.

Professional guidance becomes valuable when you need specialized coverage that standard bundles exclude. Insurance Brokers of Arizona® tailors coverage to specific needs while we secure competitive rates through carrier relationships. We analyze your risk profile to determine whether a bundle provides genuine value or if separate policies from different carriers offer superior protection at lower costs.

Start your bundle evaluation when you gather current policy declarations and identify coverage requirements that matter most to your situation. Compare total annual costs across at least three carriers (including all fees), then review coverage limits and exclusions carefully. Professional brokers streamline this process when they present pre-screened options that match your needs rather than force you to navigate complex policy language independently.