Professional General Liability Insurance: What You Need to Know

Professional general liability insurance is a critical safeguard for businesses across various industries. At Insurance Brokers of Arizona®, we’ve seen firsthand how this coverage can protect companies from potentially devastating financial losses.

This type of insurance shields businesses from claims of bodily injury, property damage, and personal and advertising injury. In this post, we’ll break down the key aspects of professional general liability insurance and why it’s essential for your business.

What Is Professional General Liability Insurance?

Definition and Purpose

Professional general liability insurance protects businesses from financial losses due to third-party claims. This coverage shields companies against lawsuits alleging bodily injury, property damage, or personal and advertising injury caused by their operations, products, or services.

Businesses That Need This Coverage

Almost every business can benefit from professional general liability insurance. It’s especially important for:

- Contractors and construction companies

- Retail stores and restaurants

- Professional service providers (lawyers, accountants, consultants)

- Manufacturing businesses

- Technology companies

Small businesses often face higher risks due to limited resources to handle potential lawsuits. A study by the U.S. Chamber Institute for Legal Reform revealed that the cost of the U.S. tort system for small businesses reached $105.4 billion in 2008. This statistic underscores the significant financial impact a single lawsuit can have on a small company.

Common Risks Covered

Professional general liability insurance typically covers:

- Bodily Injury: This covers medical expenses and potential lawsuits if a customer sustains injuries on your premises (e.g., slipping and falling in your store).

- Property Damage: If your employee accidentally damages a client’s property while working, this insurance can cover repair or replacement costs.

- Personal and Advertising Injury: This includes claims of libel, slander, copyright infringement, or invasion of privacy in your advertising.

Real-World Application

To illustrate the importance of this coverage, consider a case where a small marketing agency faced a $250,000 lawsuit from a client who claimed the agency’s campaign damaged their reputation. Without professional general liability insurance, this could have led to bankruptcy. Instead, their policy covered legal fees and the settlement, allowing the business to continue operations.

The specific coverage a business needs depends on its unique risks. Working with an experienced insurance broker (such as Insurance Brokers of Arizona®) can help assess these needs and recommend the right policy. A knowledgeable broker can also explain policy limits, exclusions, and strategies to maximize coverage.

As we move forward, let’s examine the key components of professional general liability policies to understand the full scope of protection they offer.

What Does Professional General Liability Insurance Cover?

Bodily Injury and Property Damage Protection

Professional general liability insurance forms the backbone of business protection. It shields companies from claims of bodily injury and property damage. When a customer falls in your store or an employee accidentally breaks a client’s equipment, this coverage activates. It doesn’t just pay for medical bills or repairs; it also covers legal expenses in case of a lawsuit.

A U.S. Chamber Institute for Legal Reform study revealed tort costs hit $429 billion in 2020 (2.1% of U.S. GDP). This statistic underscores the potential financial impact of lawsuits on businesses and the necessity of adequate coverage.

Personal and Advertising Injury Coverage

This component protects against claims related to libel, slander, copyright infringement, and invasion of privacy in advertising. In our digital era, where a single tweet can reach millions, this coverage proves more essential than ever.

The Internet Advertising Bureau reported U.S. digital advertising spending reached $189 billion in 2021. With such high stakes in advertising, the risk of unintentional infringement or offense looms large.

Medical Payments Provision

Many professional general liability policies include a medical payments provision. This covers immediate medical expenses for injuries sustained on your property, regardless of fault. It acts as a goodwill gesture that can prevent minor incidents from escalating into costly lawsuits.

Legal Defense and Settlement Cost Coverage

The most valuable aspect of professional general liability insurance is coverage for legal defense and settlement costs. A Chubb survey found 43% of small businesses faced at least one lawsuit in the past five years. The average cost of these lawsuits? A whopping $160,000.

Without insurance, these costs could bankrupt a small business. Professional general liability insurance protects you not just from the settlement itself, but also from the often-overlooked expenses of legal representation.

Policy limits and exclusions can vary. An experienced broker can help ensure you have the right coverage for your specific needs. They can guide you through the intricacies of policy language and help you understand exactly what’s covered (and what’s not).

As we move forward, let’s examine the factors that influence the cost of professional general liability insurance. Understanding these elements will help you make informed decisions about your coverage.

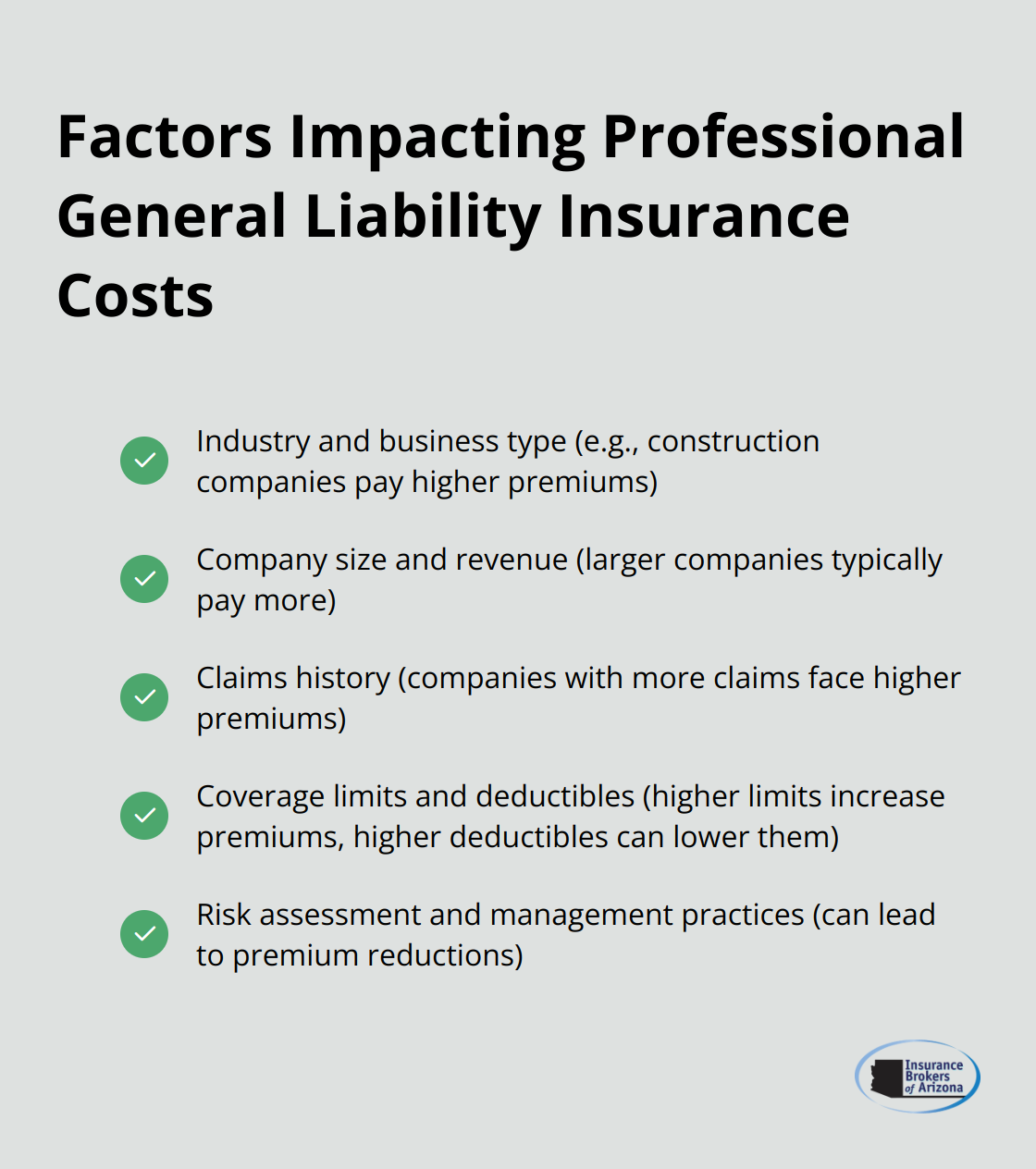

What Impacts Your Professional General Liability Insurance Costs?

Industry and Business Type

Your industry plays a significant role in determining your insurance costs. High-risk industries like construction face higher premiums due to the increased likelihood of accidents or property damage. A construction company might pay $1,000 to $3,000 annually for $1 million in coverage, while a consulting firm might pay $400 to $1,000 for the same coverage.

Company Size and Revenue

Larger companies with higher revenues typically pay more for insurance. This stems from their increased exposure to potential claims. A study by AdvisorSmith found that companies with $1 million in revenue paid an average of $742 annually for general liability insurance, while those with $5 million in revenue paid $1,287.

Claims History and Risk Management

Your claims history significantly influences your premiums. Companies with a history of claims are viewed as higher risk and face higher premiums. The implementation of strong risk management practices can help reduce your premiums over time. For instance, a retail store that implements a rigorous slip-and-fall prevention program might see a 10-15% reduction in their premiums.

Coverage Limits and Deductibles

Higher coverage limits naturally lead to higher premiums. However, the selection of a higher deductible can lower your premium. For example, increasing your deductible from $1,000 to $2,500 could potentially reduce your premium by 10-20%.

Risk Assessment and Management

A comprehensive risk assessment can identify potential hazards specific to your business. This allows you to implement targeted risk management strategies. For example, a manufacturing company might invest in advanced safety equipment and training programs. These measures not only reduce the likelihood of accidents but can also lead to lower insurance premiums (sometimes by up to 25%).

Final Thoughts

Professional general liability insurance protects businesses from financial losses due to third-party claims. This coverage shields companies against lawsuits alleging bodily injury, property damage, or personal and advertising injury. At Insurance Brokers of Arizona®, we offer guidance to ensure your coverage aligns with your business needs.

To select the right professional general liability insurance, assess your business’s unique risks and determine appropriate coverage limits. Evaluate your industry, company size, and potential exposure to claims. Review your current risk management practices, as improvements can often lead to lower premiums.

Professional general liability insurance provides peace of mind, allowing you to focus on growing your business. It serves as a vital shield in an unpredictable business landscape (ensuring your company’s longevity and success). With the right policy, you can confidently pursue new opportunities, knowing you’re protected against unforeseen risks.