Commercial General Liability Insurance Cost Factors

At Insurance Brokers of Arizona®, we often get asked: “How much does commercial general liability insurance cost?” The truth is, there’s no one-size-fits-all answer.

Several factors influence the price of this essential coverage for businesses. In this post, we’ll break down the key elements that impact your commercial general liability insurance premiums.

How Your Business Type Impacts Insurance Costs

At Insurance Brokers of Arizona®, we understand that different business types and industries significantly affect commercial general liability insurance costs. The nature of your business operations directly influences your risk profile and, as a result, your insurance premiums.

High-Risk vs. Low-Risk Industries

Industries with a higher likelihood of accidents or injuries typically face steeper insurance costs. Construction companies, for example, often pay more for their coverage due to the inherent dangers of their work environment. A 2024 report by the National Association of Insurance Commissioners revealed that construction businesses paid an average of 2.3 times more for general liability insurance compared to retail stores.

Office-based businesses (such as accounting firms or software companies) typically enjoy lower premiums. These industries have fewer physical risks associated with their day-to-day operations, which results in fewer claims and lower insurance costs.

Specific Hazards in Business Operations

The unique hazards associated with your business activities also influence your insurance costs. Restaurants face risks related to food safety and potential customer injuries on the premises. Consulting firms, on the other hand, might worry more about professional errors or omissions.

A study by the Insurance Information Institute found that slip-and-fall accidents account for over 20% of general liability claims for retail businesses. This statistic highlights why insurers carefully examine the specific risks associated with each business type when calculating premiums.

Historical Claims Data

Insurance companies rely heavily on historical claims data when they assess risk and set premiums. If your industry has a track record of frequent or costly claims, you can expect this to reflect in your insurance costs.

The manufacturing sector, for instance, has historically seen higher claim frequencies due to product liability issues. A 2023 analysis by AM Best showed that the manufacturing industry experienced a 15% higher claim frequency compared to the overall business average.

Industry-Specific Regulations

Certain industries face stricter regulations, which can impact insurance requirements and costs. Healthcare providers, for example, must comply with HIPAA regulations, which can increase their liability exposure and, consequently, their insurance premiums.

Technological Advancements

The rapid pace of technological change can also affect insurance costs for certain industries. Cybersecurity risks, for instance, have become a significant concern for businesses across various sectors (particularly those handling sensitive data). This evolving risk landscape can lead to adjustments in insurance premiums.

As we move forward, it’s important to consider how coverage limits and deductibles can further shape your insurance costs. These factors, combined with your business type, create a comprehensive picture of your insurance needs and expenses.

How Coverage Limits and Deductibles Shape Your Premiums

The Power of Higher Coverage Limits

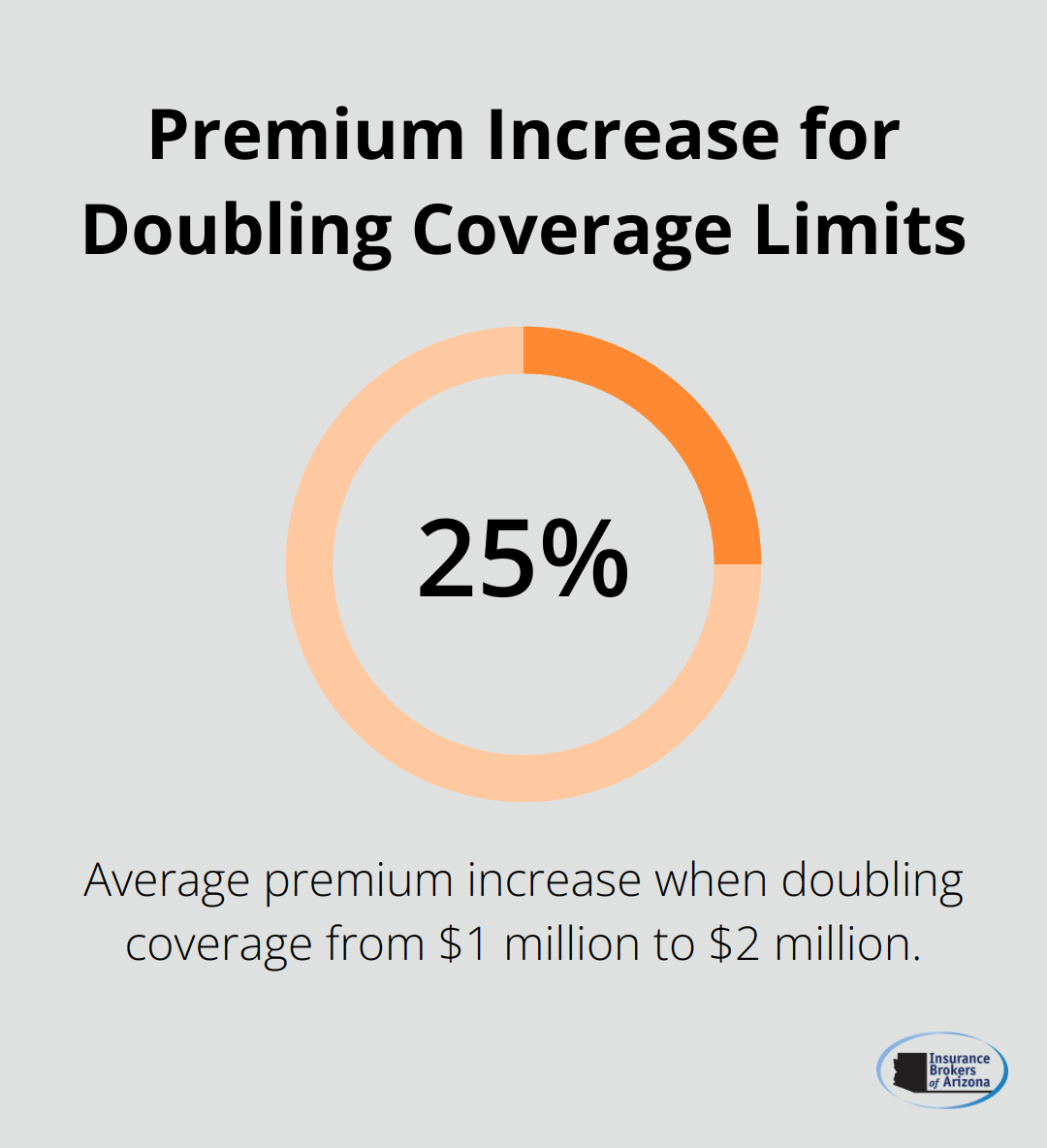

Higher coverage limits increase premiums, but not always proportionally. A 2024 Insurance Information Institute study revealed that doubling coverage from $1 million to $2 million typically raises premiums by 20-30% (not 100%). This extra protection can safeguard your business from financial ruin in severe cases, such as a major slip-and-fall accident with medical bills and legal fees exceeding $1 million.

Deductible Choices: A Balancing Act

Your deductible selection significantly impacts premium costs. The National Association of Insurance Commissioners reports that increasing a deductible from $1,000 to $5,000 can reduce premiums by 10-20% for many businesses. However, you must weigh potential savings against your ability to cover higher out-of-pocket expenses during a claim. Your cash flow and risk tolerance should guide this decision.

Additional Coverages: Extra Protection at a Price

Standard commercial general liability policies cover many risks, but additional coverages offer enhanced protection. For example:

- Product liability coverage for manufacturers can increase premiums by 5-15%, depending on product type and sales volume.

- Cyber liability insurance costs vary widely, but small businesses typically pay $1,000 to $3,000 annually for $1 million in coverage (Advisen, 2023).

- Professional liability (errors and omissions) insurance often costs 1-3% of a company’s annual revenue (MarketScout data).

While these additions increase overall insurance costs, they provide vital protection against specific risks that could otherwise devastate your business.

Tailoring Your Coverage: A Strategic Approach

Finding the right balance of coverage limits and deductibles requires careful consideration of your business’s unique needs and risk profile. Insurance professionals can help you navigate these choices to create a cost-effective and comprehensive insurance package.

The impact of coverage limits and deductibles on your premiums is clear, but your company’s size and revenue also play a significant role in determining insurance costs. Let’s explore how these factors influence your commercial general liability insurance premiums in the next section.

How Company Size and Revenue Influence Insurance Costs

Employee Count and Insurance Premiums

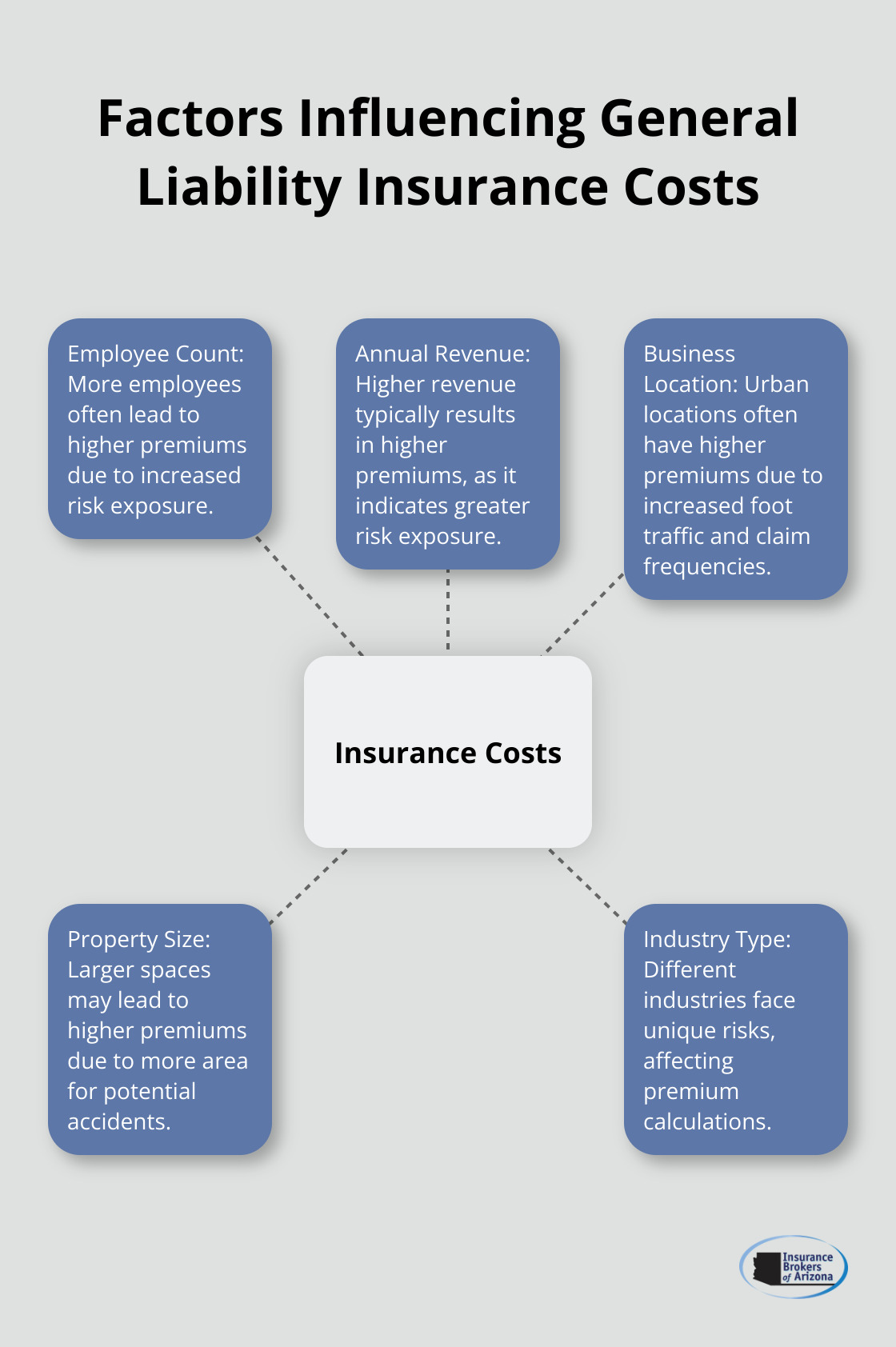

The number of employees in a company directly affects commercial general liability insurance costs. A 2024 study by the National Association of Insurance Commissioners revealed that businesses with 1-10 employees paid an average of $500 annually for general liability insurance. In contrast, those with 50-100 employees paid around $3,000. This increase doesn’t solely result from higher headcount; more employees often lead to more customer interactions and a greater likelihood of accidents or mistakes.

Revenue’s Impact on Premium Calculation

Annual revenue plays a significant role in determining insurance premiums. Insurers view higher revenue as an indicator of increased exposure to risk. The Insurance Information Institute reports that businesses typically pay between $300 to $1,000 per million dollars of revenue for general liability insurance. However, this can vary widely based on industry and other risk factors (such as claims history and safety measures).

Location Matters

Where a business operates affects its insurance costs. Urban locations often come with higher premiums due to increased foot traffic and higher claim frequencies. The Insurance Services Office (ISO) data shows that businesses in major cities pay up to 25% more for general liability insurance compared to rural areas.

Property Size Considerations

The size of a business’s physical space impacts premiums. Larger spaces mean more area for potential accidents. A retail store occupying 5,000 square feet will likely pay more than a similar store in a 1,000 square foot space (assuming all other factors remain equal).

Industry-Specific Factors

Different industries face unique risks, which insurers consider when calculating premiums. For example, construction companies often pay higher premiums due to the inherent dangers of their work environment. In contrast, office-based businesses (such as accounting firms) typically enjoy lower premiums due to fewer physical risks associated with their day-to-day operations.

Business size and revenue significantly impact your general liability insurance costs. Larger companies with more employees and higher revenues generally pay more for their insurance coverage.

Final Thoughts

Commercial general liability insurance costs depend on various factors, including business type, coverage limits, and company size. These elements significantly impact premiums, making it essential for businesses to understand their specific needs. Insurance Brokers of Arizona® specializes in tailoring coverage to meet unique requirements across industries, partnering with over 40 reputable carriers to offer competitive options.

Regular policy reviews ensure coverage aligns with evolving business needs as companies grow or face changing risks. The true value of insurance lies in the protection it provides, safeguarding businesses from potentially devastating financial losses. Insurance Brokers of Arizona® offers personalized solutions and exceptional customer service to help navigate the complexities of commercial general liability insurance.

We commit to helping you secure the right coverage at competitive rates. Our team has earned the trust of businesses throughout Arizona (with thousands of positive reviews). Contact Insurance Brokers of Arizona® to explore your options and protect your business’s future.