Professional vs Commercial General Liability Insurance

At Insurance Brokers of Arizona®, we often get questions about the differences between professional liability insurance and commercial general liability coverage.

These two types of insurance serve distinct purposes and protect businesses against different risks.

Understanding the nuances between professional liability insurance vs commercial general liability is essential for ensuring your business has the right protection.

In this post, we’ll break down the key features of each type of insurance and help you determine which one your business needs.

What Is Professional Liability Insurance?

Definition and Purpose

Professional liability insurance (also known as errors and omissions insurance) protects businesses that provide professional services or advice. This coverage shields against claims of negligence, mistakes, or failure to perform professional duties that cause financial losses for clients.

Who Needs This Coverage?

A broad spectrum of professionals requires this insurance:

- Traditional professions: Doctors, lawyers, accountants, architects

- Consultants and advisors

- IT professionals

- Real estate agents

- Freelance writers

A 2023 American Bar Association survey revealed that 34% of law firms faced at least one malpractice claim in the previous year, highlighting the widespread need for this protection.

Key Components of Professional Liability Policies

These policies typically cover:

- Legal defense costs

- Settlements

- Judgments arising from covered claims

Professional liability policies operate on a claims-made basis, which means they only cover incidents that occur and are reported while the policy is active.

The Importance of Retroactive Dates

The retroactive date in a professional liability policy determines how far back in time the policy will cover incidents. For example, a policy with a January 1, 2020 retroactive date will cover claims from incidents on or after that date (as long as the claim is made during the policy period).

Tailoring Coverage to Specific Needs

Professional liability needs vary significantly between industries (and even individual businesses within the same field). A software developer might need coverage for data breaches, while a financial advisor would require protection against claims of poor investment advice.

Understanding these nuances is essential to secure the right coverage for your business. Working with an experienced broker can help you assess your specific risks and tailor a policy accordingly.

As we move forward, let’s examine another critical form of business protection: Commercial General Liability Insurance.

What Is Commercial General Liability Insurance?

Definition and Scope

Commercial General Liability (CGL) insurance forms the foundation of business protection. It shields companies from financial losses due to third-party claims of bodily injury, property damage, and advertising injury.

Coverage Areas

CGL policies typically cover a wide range of incidents:

- Bodily Injury: A customer slips and falls in your store? CGL can cover medical expenses and potential legal costs.

- Property Damage: An employee accidentally damages a client’s equipment on a job site? CGL has you covered.

- Advertising Injury: This protects against claims of libel, slander, copyright infringement, and invasion of privacy in your advertising.

The Insurance Information Institute reports the average cost of a slip and fall claim at around $20,000 (a stark reminder of the importance of adequate CGL coverage).

Who Needs CGL Insurance?

Almost every business benefits from CGL insurance. Retailers, contractors, manufacturers, and service providers all face risks that CGL mitigates. Even home-based businesses should consider this coverage (homeowners insurance often excludes business-related incidents).

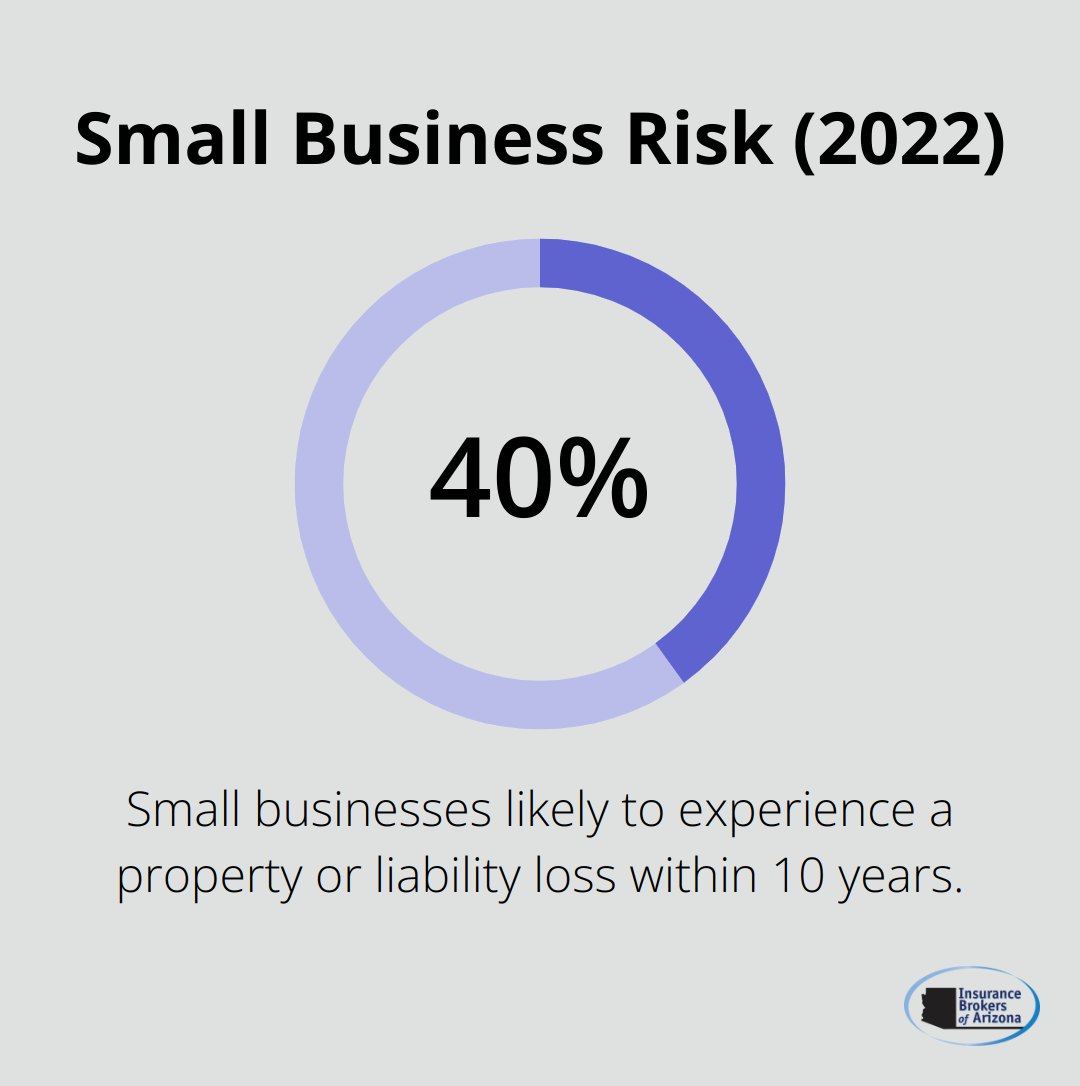

A 2022 National Association of Insurance Commissioners survey found that 40% of small businesses will likely experience a property or liability loss within the next 10 years. This statistic underscores the widespread need for CGL protection across various industries.

Policy Limitations

It’s important to note that CGL policies have limits. They don’t cover:

- Employee injuries (that’s what workers’ compensation is for)

- Damage to your own property

- Professional errors or negligence (professional liability insurance covers this)

Understanding these limitations proves crucial for comprehensive risk management.

Tailoring Your Coverage

Every business has unique risks. A retailer faces different challenges than a construction company. That’s why it’s essential to work with an experienced insurance broker who can help you assess your specific risks and tailor a policy accordingly.

As we move forward, let’s examine the key differences between Professional Liability and Commercial General Liability Insurance to help you determine which type (or combination) best suits your business needs.

How Professional and Commercial General Liability Insurance Differ

Coverage Focus

Professional Liability insurance protects against financial losses from errors or omissions in professional services. For example, an accountant’s mistake on a client’s tax return would fall under Professional Liability coverage.

Commercial General Liability (CGL) insurance addresses physical injuries and property damage. It covers incidents like customer slip-and-falls or employee-caused damage to client property.

Policy Activation

These policies activate differently. Professional Liability uses a claims-made basis, covering only incidents that occur and are reported while the policy is active. This necessitates continuous coverage.

CGL policies typically operate on an occurrence basis. They cover incidents that happen during the policy period, regardless of when the claim is filed (providing long-term protection even after policy expiration).

Industry-Specific Considerations

Different industries face unique risks, influencing coverage needs. Software developers might prioritize Professional Liability to protect against coding errors leading to client financial losses. Restaurant owners would likely focus on CGL to cover potential slip-and-fall incidents or food-related illnesses.

The American Medical Association reports that 34% of physicians have faced lawsuits at least once in their careers (highlighting Professional Liability’s importance in high-risk professions). The National Safety Council estimates that falls in public places result in over 8 million emergency room visits annually (underscoring the need for robust CGL coverage in customer-facing businesses).

Policy Limits and Exclusions

Understanding policy exclusions is vital. Professional Liability won’t protect against bodily injury claims, while CGL doesn’t cover professional mistakes or negligence.

CGL policies often exclude coverage for certain high-risk activities or industries. Many CGL policies, for instance, exclude pollution-related incidents (a significant gap for some sectors).

Professional Liability policies may have retroactive dates, limiting coverage to incidents after a specific date. This makes careful review of policy terms essential when switching insurers.

Tailoring Coverage to Business Needs

The right combination of these policies provides comprehensive protection. Businesses should assess their specific risks and tailor coverage accordingly. Working with experienced insurance professionals (like those at Insurance Brokers of Arizona®) can help identify potential gaps and create a robust insurance strategy.

Final Thoughts

Professional liability insurance vs commercial general liability coverage serve distinct purposes in protecting businesses. Your specific business activities and risk exposure determine which policy, or combination of policies, you need. We recommend a thorough assessment of your business needs to identify potential vulnerabilities and ensure comprehensive protection.

An experienced insurance broker can provide valuable guidance in navigating these complex decisions. Insurance Brokers of Arizona® specializes in tailoring insurance solutions for businesses across various industries. Our team strives to offer comprehensive coverage at competitive rates.

Don’t leave your company’s future to chance. Invest in the right insurance coverage today to protect your business for years to come. Contact us to discuss your professional liability and commercial general liability insurance needs.