Auto Insurance for the Elderly: Complete Guide

Turning 65 shouldn’t mean paying through the nose for auto insurance. Yet many seniors face premiums that jump significantly once they hit a certain age, even if they’re safer drivers than they were decades ago.

At Insurance Brokers of Arizona®, we’ve helped hundreds of older drivers find policies that actually fit their budgets and driving patterns. This guide walks you through why rates climb, what discounts you qualify for, and how to lock in real savings.

Why Elderly Drivers Cost More to Insure

Insurance companies don’t raise rates on senior drivers out of spite. The numbers tell a story that insurers take seriously. According to Bankrate data from Quadrant Information Services, a 70-year-old male driver pays around $2,663 annually for full-coverage auto insurance, compared to roughly $2,455 for a 60-year-old. That’s a noticeable jump.

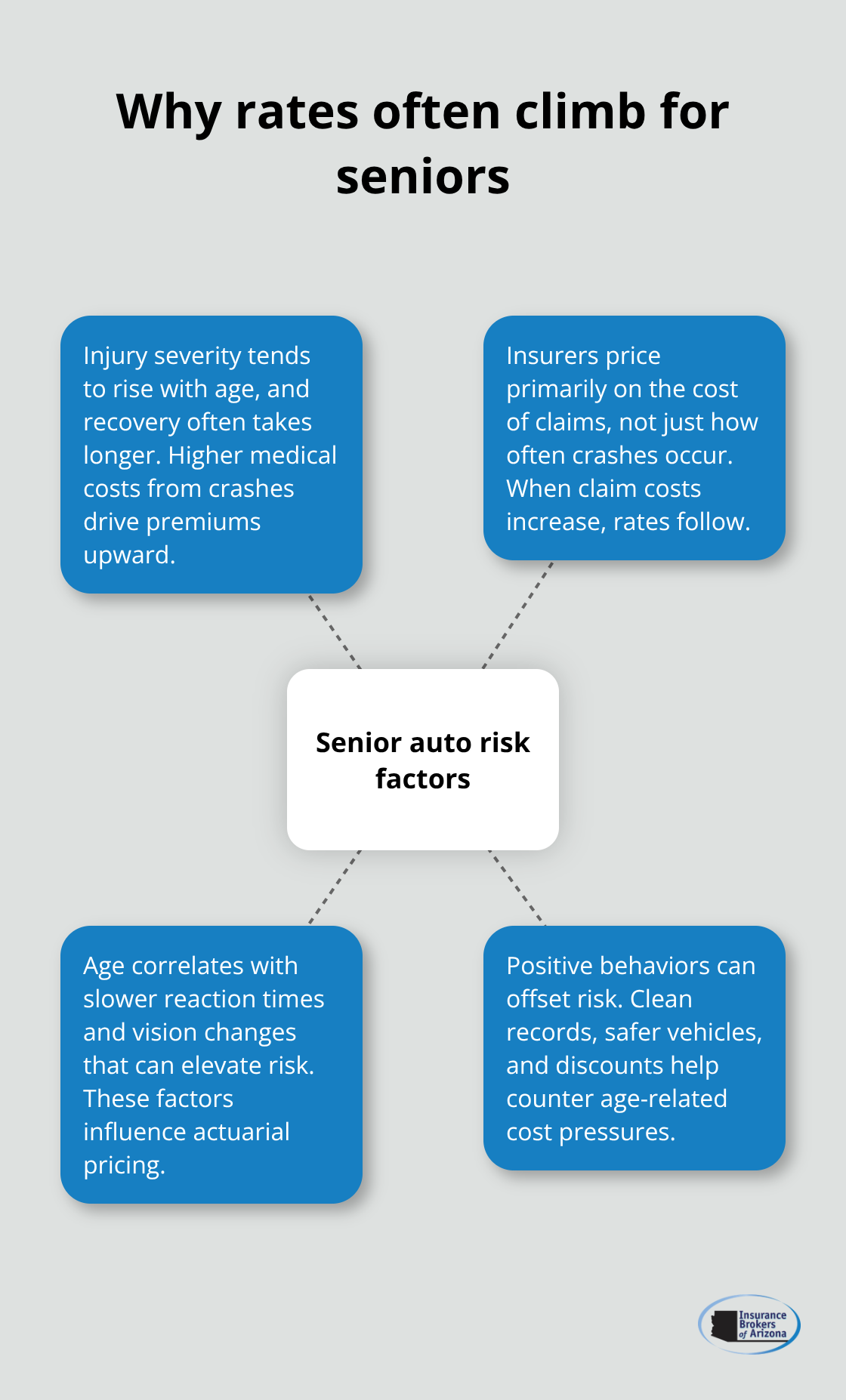

The Insurance Institute for Highway Safety reports that while seniors are involved in fewer fatal crashes per capita, they do experience higher injury severity when accidents occur. This matters because insurers price risk based on the cost of claims, not just accident frequency. A 70-year-old involved in a collision faces longer recovery times and potentially higher medical expenses, which translates directly into higher premiums. Consumer Reports surveyed over 40,000 policyholders and found that more seniors reported rate increases in the past 12 months than younger drivers, underscoring how age factors into pricing decisions.

Physical changes that come with aging-slower reaction times, reduced vision, and decreased mobility-affect how insurers assess your driving profile. These aren’t character judgments; they’re actuarial reality. The data shows that drivers over 80 face the steepest increases, with premiums climbing more sharply than in any other age bracket.

The Real Reason Rates Jump at Certain Ages

Insurers don’t apply a blanket senior surcharge. Instead, they track specific risk factors that correlate with age. Medical claims from accidents involving older drivers tend to be costlier because recovery is slower and complications are more common. Additionally, vision changes and medication side effects that accompany aging can influence claim patterns. In six states-California, Hawaii, Massachusetts, Michigan, North Carolina, and Pennsylvania-insurers cannot use age as a direct rating factor, yet premiums still vary based on accident history and other measurable factors. This shows that age itself isn’t the whole story; it’s the underlying risks age brings.

A clean driving record remains your strongest defense against rate increases, regardless of your age. Bankrate’s analysis shows that maintaining a spotless record for five years can qualify you for meaningful discounts that offset age-related increases. The Hartford reports that seniors aged 70 and older average $1,450 annually for car insurance, which suggests that proper discounts and policy choices can keep costs reasonable even as you age.

What Senior Drivers Get Wrong About Their Rates

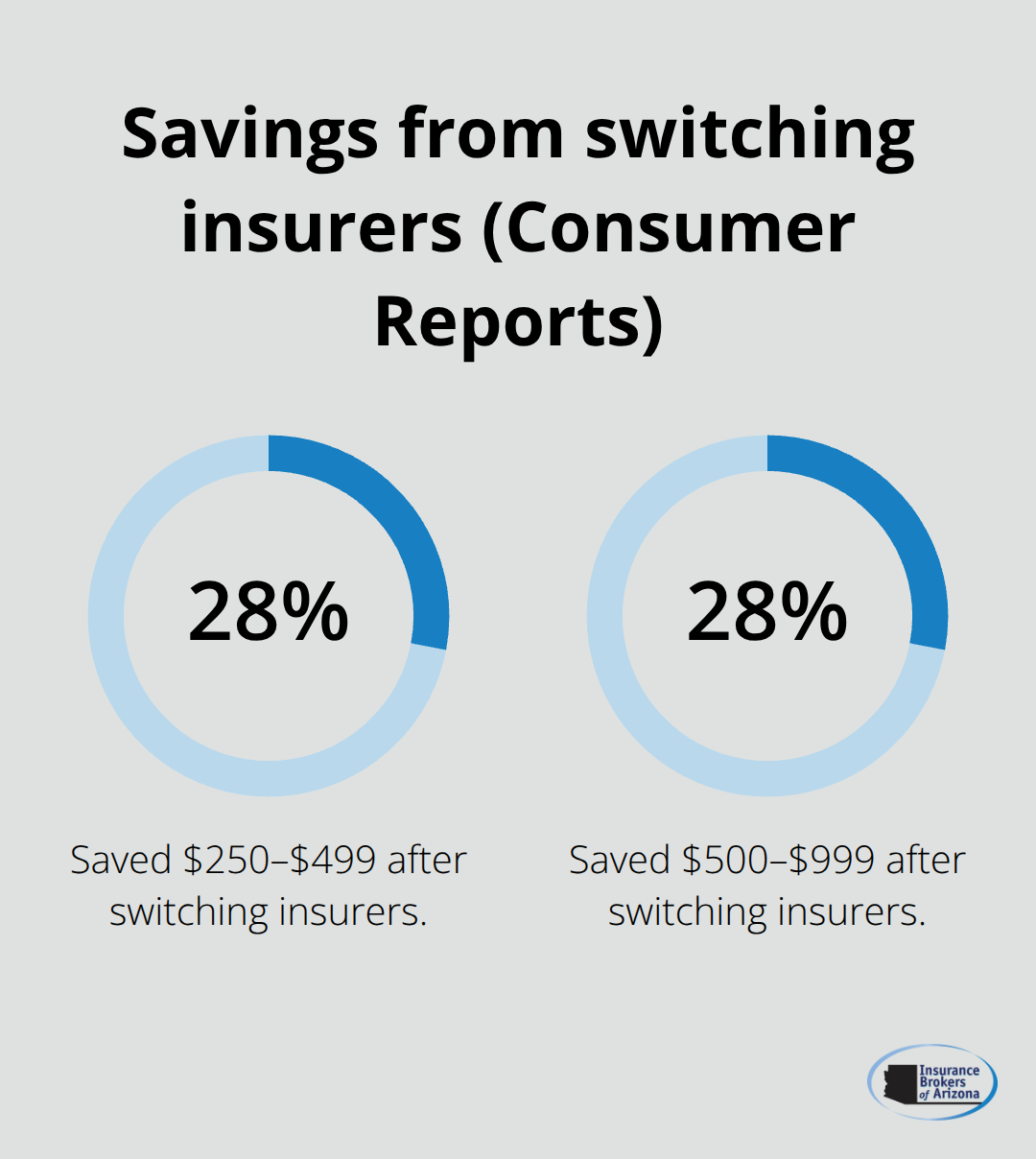

The biggest misconception is that you’re helpless against age-based pricing. Many seniors accept rate increases without shopping around, assuming all insurers charge roughly the same. This is false. Consumer Reports found that drivers who switched insurers in the past year saved a median of $461, with 28 percent saving between $250 and $499 and another 28 percent saving $500 to $999. Some saved $1,000 or more.

Your age is just one variable in a complex pricing formula. Your ZIP code, vehicle type, driving history, bundling options, and selected discounts matter enormously. A senior with a clean record and multiple policies bundled together will pay far less than a younger driver with accidents on their record.

Shopping annually isn’t optional if you want fair pricing. The Hartford’s data shows that premiums for seniors aged 50 to 59 average $1,942 annually, dropping to $1,517 for those 60 to 69, then to $1,450 for those 70 and older. This pattern reveals that aggressive discounting and policy adjustments can actually lower your costs as you age, contradicting the assumption that getting older always means paying more. The real issue is inaction, not age.

How Insurers Assess Your Individual Risk

Insurers evaluate each driver’s profile through multiple lenses beyond age alone. Your medical history, current medications, and vision test results (required during license renewal in many states) all influence how carriers price your policy. Some insurers use telematics programs that monitor your actual driving behavior, which can work in your favor if you drive safely. These programs reward cautious habits with discounts that offset age-related increases. Your vehicle choice also matters significantly. Newer cars equipped with automatic emergency braking, blind spot warnings, and rear cross-traffic alerts reduce claim costs, and insurers recognize this through lower premiums. The combination of a safe vehicle, clean driving record, and active participation in discount programs can substantially reduce what you pay, regardless of your age.

Understanding these assessment methods helps you take control of your rate. The next section explores the specific discounts and strategies that senior drivers can use to lower their premiums and find coverage that truly fits their needs.

How to Cut Your Auto Insurance Costs as a Senior

Discounts That Actually Reduce Your Premiums

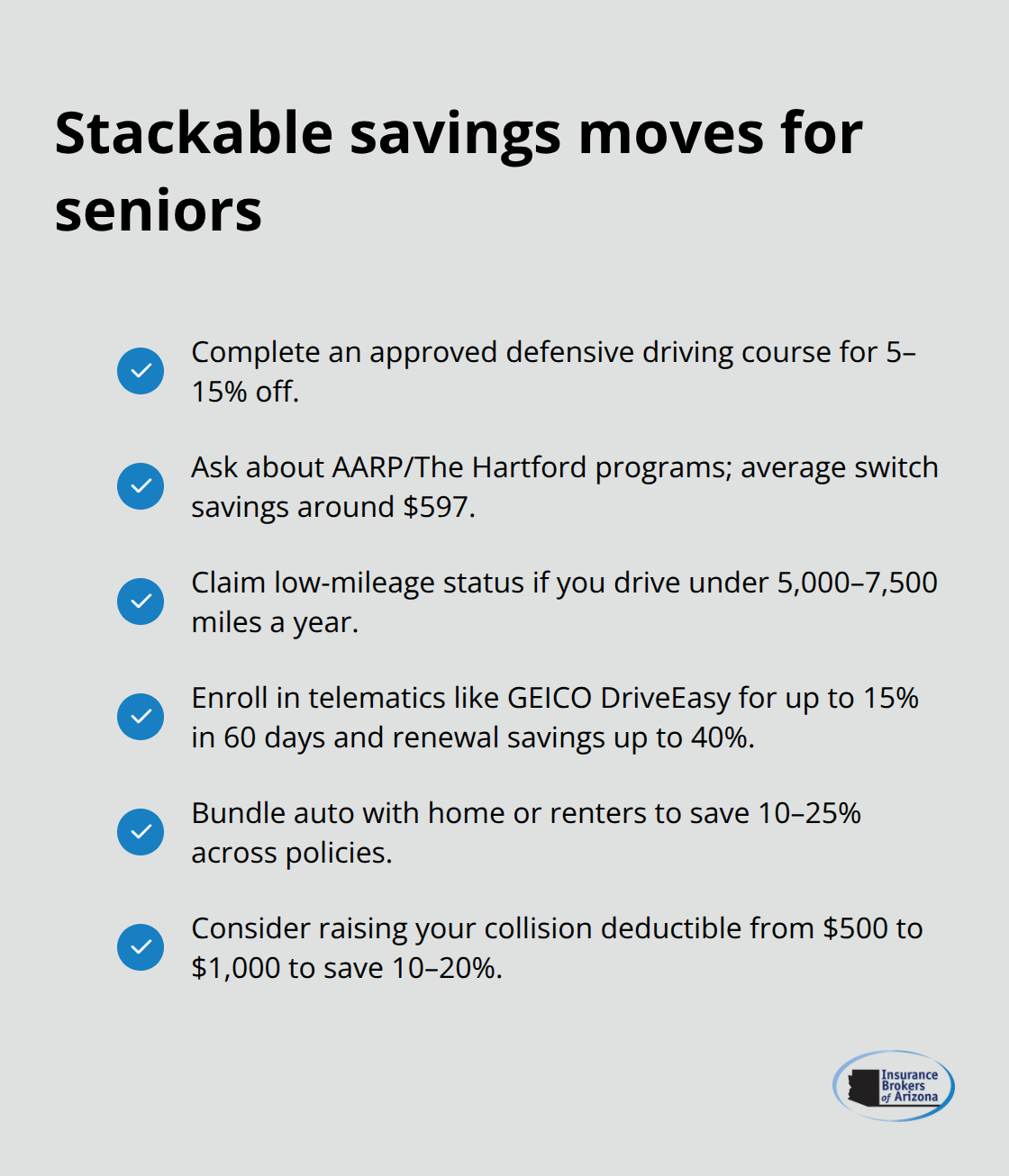

Discounts exist for senior drivers, but most fail to pursue them actively. That’s money left on the table. GEICO offers seniors over 50 a defensive driving discount for completing an approved course, which reduces premiums by 5 to 15 percent. The Hartford provides a similar benefit, allowing seniors to earn discounts for up to three years after finishing a defensive driving course. AARP members access exclusive programs through The Hartford, with average savings around $597 when switching from other carriers. These aren’t small numbers. If you pay $1,500 annually for full coverage, a 15 percent discount saves you $225 per year. The key is actually applying for them. Most insurers won’t volunteer these discounts; you must ask.

A five-year clean driving record qualifies you for loyalty discounts at most carriers, and some offer retirement discounts specifically for fully retired drivers. Low-mileage discounts apply if you drive fewer than 5,000 to 7,500 miles annually, which describes many retirees. Usage-based programs like GEICO’s DriveEasy track your actual driving behavior and reward safe habits with discounts up to 15 percent within 60 days, plus potential renewal discounts reaching 40 percent. These programs work because they measure what actually matters: how you drive, not your age.

Shopping Around Reveals Hidden Savings

Shopping around annually is non-negotiable if you want fair pricing. Consumer Reports data shows the median savings when switching insurers is $461, but that’s just the average. Nearly 30 percent of switchers saved between $500 and $999, and 13 percent saved over $1,000. Getting three to five quotes from different carriers takes less than an hour online and reveals price differences of 30 to 50 percent for identical coverage. The Hartford’s data confirms this variation, showing seniors aged 70 and older average $1,450 annually, but that figure masks significant variation by carrier and location.

Vehicle Choice and Coverage Adjustments

Your vehicle choice influences premiums substantially. Newer cars with automatic emergency braking, blind spot warnings, and rear cross-traffic alerts cost less to insure because insurers pay fewer claims on vehicles equipped with these features. If you drive an older vehicle worth only a few thousand dollars, dropping collision or comprehensive coverage often makes financial sense. Raising your deductible from $500 to $1,000 typically saves 10 to 20 percent on collision premiums.

Bundling and Combined Strategies

Bundling auto with homeowners or renters insurance yields 10 to 25 percent discounts across policies. The combination of a safe vehicle, clean driving history, multiple discounts, and bundled policies creates substantial savings that offset any age-related increases. These strategies work together to lower what you pay, but selecting the right coverage for your specific situation requires careful evaluation of your actual needs and driving patterns.

Specialized Auto Insurance Options for Seniors

Most seniors don’t drive like they did at 40. Fewer miles, shorter trips, daytime driving only-these patterns define retirement for many. Yet standard auto insurance policies ignore this reality and charge you as though you commute 40 miles daily. This mismatch between your actual driving and your premium is where real savings hide.

Low-Mileage and Usage-Based Programs

Low-mileage and usage-based insurance programs align what you pay with how you actually drive. If you drive under 5,000 to 7,500 miles annually, a low-mileage policy reduces your premium by 10 to 25 percent compared to standard coverage. GEICO’s DriveEasy program tracks your driving behavior through your smartphone or a plug-in device and rewards safe habits with discounts up to 15 percent within 60 days, plus potential renewal discounts reaching 40 percent. The Hartford’s TrueLane program offers similar flexibility, rewarding cautious driving patterns that most seniors naturally exhibit.

Pay-per-mile programs like OCHO take this further, charging a base rate plus mileage fees with no down payment required, making them ideal for retirees who drive sporadically. The math works strongly in your favor. If you drive 3,000 miles annually instead of the national average of 12,000 to 15,000 miles, your risk profile drops significantly. Insurers recognize this through lower premiums, but only if you select a program designed to capture it. Standard policies penalize you for being low-mileage because they’re structured for average drivers.

Coverage Tailored to Your Vehicle and Situation

Coverage options for seniors require different thinking than coverage for younger drivers. If you own a vehicle worth only $3,000 to $5,000, carrying collision and comprehensive coverage costs more than the potential payout, making it financially illogical. Dropping collision coverage on older vehicles while maintaining full liability protection is standard practice for many seniors.

Raising your deductible from $500 to $1,000 saves 10 to 20 percent on collision premiums without meaningfully increasing your out-of-pocket risk, especially if you drive cautiously. However, never sacrifice liability limits to save money. Your state’s minimum requirements exist because liability claims from accidents can exceed $100,000 in medical costs alone. This protection matters more than any premium reduction.

Finding the Right Coverage for Your Needs

Your specific vehicle values, driving patterns, and financial situations determine what coverage actually protects you without wasting money on unnecessary protection. This requires understanding your actual cash value for each vehicle, your annual mileage, your driving habits, and your ability to cover a higher deductible if needed.

A 75-year-old driving 4,000 miles yearly in a 2015 Honda Civic worth $8,000 needs fundamentally different coverage than someone driving 15,000 miles annually in a newer vehicle. Getting this right requires evaluating your situation against available options from multiple carriers, then selecting programs and coverage levels that fit your specific circumstances rather than accepting default options designed for average drivers. Insurance Brokers of Arizona® works with seniors to evaluate these factors and design coverage that protects them without wasting money on unnecessary protection.

Final Thoughts

Senior auto insurance doesn’t have to drain your retirement budget. The path forward is straightforward: stop accepting rate increases without question, actively pursue available discounts, and align your coverage with how you actually drive. A 70-year-old paying $2,663 annually for full coverage can reduce that significantly through defensive driving courses, bundling policies, and switching to carriers that reward safe driving habits. The Hartford’s data shows seniors aged 70 and older average $1,450 annually, proving that aggressive cost management works.

Pull your last renewal notice and note your annual premium, coverage limits, and deductibles. Then obtain quotes from at least three carriers using identical coverage levels-you’ll likely discover significant price differences for the same protection. Check whether you qualify for senior discounts, defensive driving course reductions, low-mileage programs, or bundling savings. If you drive fewer than 7,500 miles annually, usage-based programs like GEICO’s DriveEasy or The Hartford’s TrueLane could save you 15 to 40 percent.

This process takes time, and many seniors skip it because shopping for auto insurance for the elderly feels overwhelming. We at Insurance Brokers of Arizona® partner with multiple carriers to find coverage that fits your specific situation, not generic templates. Contact us to review your current coverage and discover what you’re likely overpaying.

Disclaimer: The information provided in this blog is for general informational purposes only and does not constitute legal, financial, or insurance advice. Coverage options, terms, and availability may vary. Please consult with a licensed professional for advice specific to your situation.