Commercial auto insurance is a vital safeguard for businesses that rely on vehicles. At Insurance Brokers of Arizona®, we often field questions about the cost of commercial auto insurance.

Understanding the factors that influence premiums can help you make informed decisions for your business. This post will break down the key elements affecting costs and provide practical tips to potentially lower your rates.

What Drives Commercial Auto Insurance Costs?

Commercial auto insurance costs depend on several key factors. Let’s explore the main drivers of these costs.

Vehicle Type and Fleet Size

The type and size of vehicles in your fleet significantly impact insurance costs. Larger vehicles, such as trucks or vans, typically result in higher premiums due to their increased potential for damage in accidents. The Insurance Information Institute found that commercial trucks can cost up to three times more to insure than passenger vehicles.

Fleet size also affects costs. While insuring multiple vehicles increases overall expenses, it often leads to lower per-vehicle rates. Many insurers offer fleet discounts (which can result in savings of up to 15% for businesses with five or more vehicles).

Industry-Specific Risks

Your business’s industry and vehicle usage significantly impact insurance costs. High-risk industries like construction or transportation often face steeper premiums. Data from Progressive Commercial shows that for-hire transport trucks pay an average of $1,068 per month for insurance, while contractors typically pay $172 per month.

Driver History and Experience

The driving records and experience of your employees are critical factors. The National Association of Insurance Commissioners revealed that businesses with drivers who have clean records can save up to 25% on their premiums compared to those with accident-prone drivers.

Coverage Choices

Your chosen coverage limits and deductibles directly affect your premiums. Higher coverage limits provide better protection but come with increased costs. Opting for higher deductibles can lower your monthly premiums but requires more out-of-pocket expenses in the event of a claim.

For example, increasing your deductible from $500 to $1,000 could potentially reduce your premium by 10-20%. However, it’s important to balance this with your business’s financial capacity to cover higher out-of-pocket costs.

These factors play a significant role in determining your commercial auto insurance costs. The next section will explore the average costs across different business types and regions, providing a clearer picture of what you might expect to pay for your coverage.

What’s the Average Cost of Commercial Auto Insurance?

Commercial auto insurance costs vary widely based on several factors. We’ll break down the average costs and variations you might encounter.

National Average Costs

Recent data from Insureon shows the average monthly cost of commercial auto insurance in 2024 is approximately $150. This translates to an annual premium of $1,800. However, this figure serves only as a baseline. Your actual costs could be significantly higher or lower based on your specific circumstances.

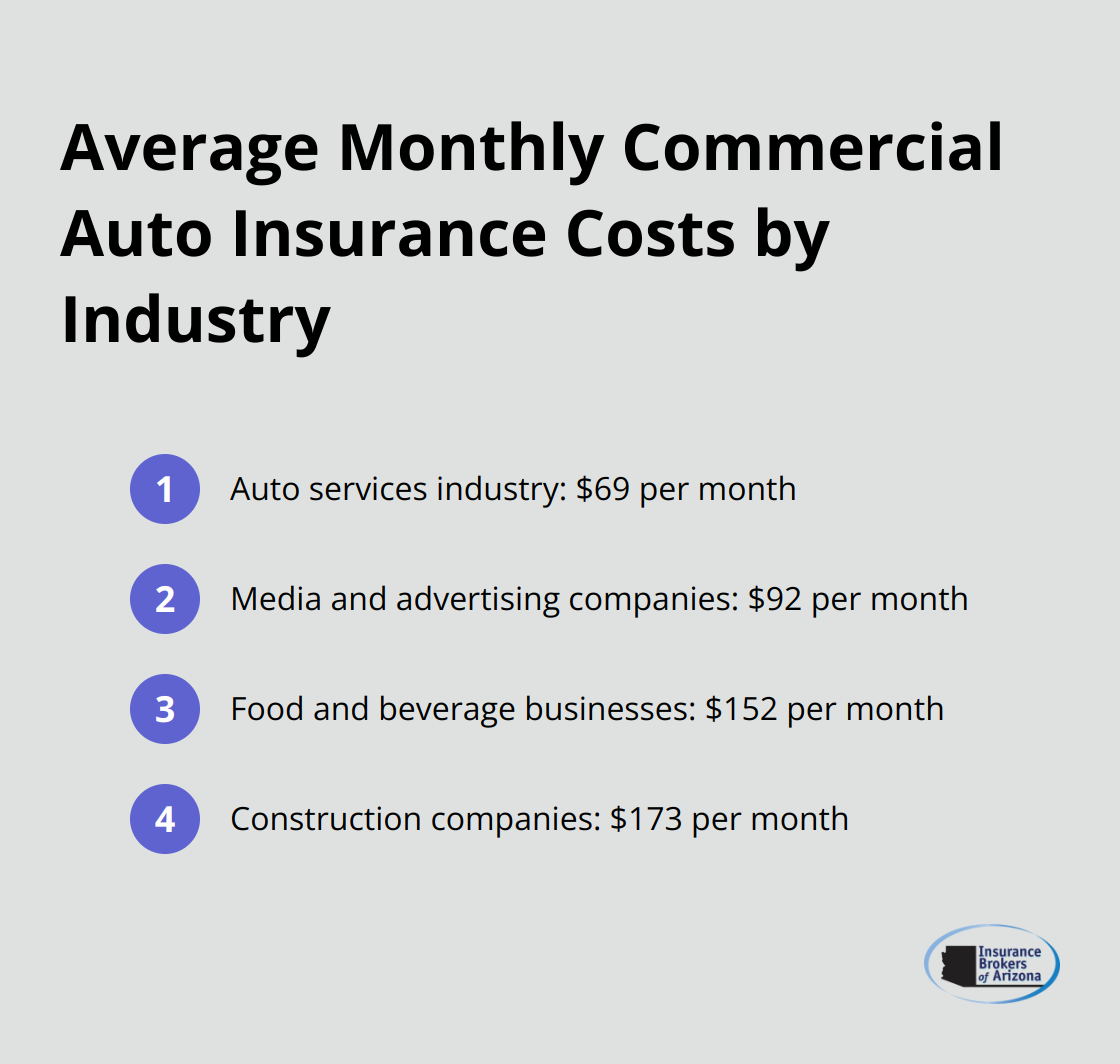

Industry-Specific Cost Variations

Different industries face varying levels of risk, which directly impacts insurance costs. Data from Progressive Commercial reveals:

These differences stem from the unique risks associated with each industry. For example, construction companies often operate larger vehicles and face higher accident risks, resulting in higher premiums.

Regional Cost Differences

Your location plays a significant role in determining your commercial auto insurance costs. States with higher population densities, more frequent accidents, or stricter insurance requirements often have higher premiums.

For example, businesses operating in urban areas like Phoenix or Tucson might face higher rates compared to those in rural Arizona (due to increased traffic and accident risks). The difference can be substantial, sometimes reaching up to 30% or more.

Vehicle Type and Usage

The type of vehicles you insure and how you use them also affect your premiums. Larger vehicles, such as trucks or vans, typically result in higher premiums due to their increased potential for damage in accidents. The Insurance Information Institute found that commercial trucks can cost up to three times more to insure than passenger vehicles.

Coverage Limits and Deductibles

Your chosen coverage limits and deductibles directly affect your premiums. Higher coverage limits provide better protection but come with increased costs. Opting for higher deductibles can lower your monthly premiums but requires more out-of-pocket expenses in the event of a claim.

For instance, increasing your deductible from $500 to $1,000 could potentially reduce your premium by 10-20%. However, it’s important to balance this with your business’s financial capacity to cover higher out-of-pocket costs.

These factors all contribute to the final cost of your commercial auto insurance. To get an accurate estimate for your business, you’ll need to obtain personalized quotes based on your specific needs and circumstances. Insurance Brokers of Arizona® can help you navigate this process and find competitive rates tailored to your unique situation. In the next section, we’ll explore strategies to potentially lower your commercial auto insurance premiums without compromising on coverage.

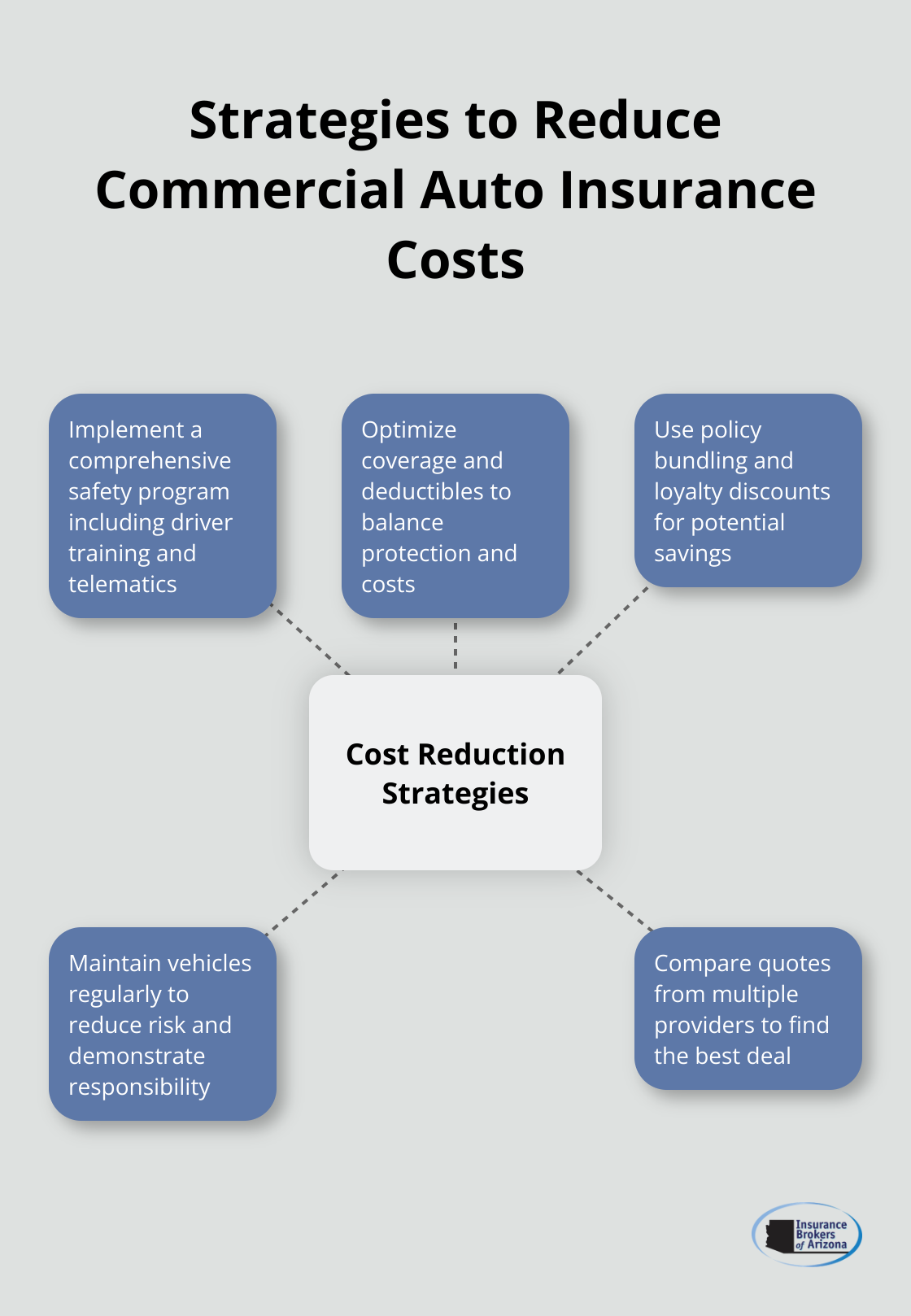

How to Reduce Commercial Auto Insurance Costs

Implement a Comprehensive Safety Program

You can reduce your commercial auto insurance costs by implementing a robust safety program. This approach protects your employees and shows insurers that you minimize risks.

Start with regular safety training sessions for all drivers. Cover defensive driving techniques, proper vehicle maintenance, and company safety policies. Many insurers offer discounts (up to 10%) for businesses with formal safety programs.

Install telematics devices in your vehicles. These devices track driving behavior such as speed, harsh braking, and acceleration. The National Association of Insurance Commissioners reports that businesses using telematics can see premium reductions of up to 25%.

Optimize Your Coverage and Deductibles

Review your policy to avoid over-insurance. While adequate coverage is important, you might pay for unnecessary extras. For newer vehicles, you might not need comprehensive coverage on all of them.

Higher deductibles can lead to lower premiums. Raising your deductible from $500 to $1,000 could reduce your premium by 10-20%. Ensure your business can afford the higher out-of-pocket expense in case of a claim.

Use Policy Bundling and Loyalty Discounts

Many insurers offer discounts when you bundle multiple policies. Combining your commercial auto insurance with general liability or property insurance could save you up to 15%.

Long-term relationships with insurers can result in loyalty discounts. Some companies offer reductions of up to 5% for each claim-free year, up to a maximum of 25%.

Maintain Your Vehicles Regularly

Regular vehicle maintenance helps lower your insurance costs. Well-maintained vehicles are less likely to break down or cause accidents due to mechanical failures.

Keep detailed records of all maintenance and repairs. These records demonstrate to insurers that you’re proactive about vehicle upkeep, potentially leading to lower premiums.

Compare Quotes from Multiple Providers

Don’t accept the first quote you receive. Different insurers use varying criteria to calculate premiums, so prices can vary significantly. Obtain quotes from multiple providers to ensure you get the best deal.

Focus on more than just price. Consider the coverage limits, deductibles, and the insurer’s reputation for customer service and claims handling. Insurance Brokers of Arizona® can help you navigate this process, using our relationships with over 40 reputable carriers to find the best coverage and cost combination for your business.

Final Thoughts

Commercial auto insurance costs depend on various factors, including vehicle types, industry risks, and coverage choices. Your specific premiums may differ significantly from average benchmarks based on your unique circumstances. The cheapest option isn’t always the best; tailored coverage that addresses your business’s specific risks provides better long-term financial protection.

Safety programs, optimized coverage, and regular vehicle maintenance can help lower your premiums. However, navigating the complexities of commercial auto insurance can challenge many business owners. Working with an experienced insurance broker proves invaluable in finding the right balance between comprehensive coverage and cost-effective premiums.

Insurance Brokers of Arizona® specializes in finding suitable coverage options for businesses. Our partnerships with numerous carriers allow us to offer a wide range of options tailored to your specific needs (including competitive rates for commercial auto insurance). We provide personalized guidance to ensure you have the protection your business requires while effectively managing costs.