Choosing the best commercial auto insurance is a critical decision for any business that relies on vehicles. At Insurance Brokers of Arizona®, we understand the complexities involved in selecting the right coverage for your fleet.

This guide will walk you through the essential factors to consider, from understanding different types of coverage to assessing your specific business needs. We’ll help you navigate the process of securing comprehensive protection for your commercial vehicles.

What Is Commercial Auto Insurance?

Definition and Purpose

Commercial auto insurance protects businesses that use vehicles for work-related purposes. This specialized policy offers more extensive coverage than personal auto insurance. It safeguards companies of all sizes against potential financial losses related to their vehicle operations.

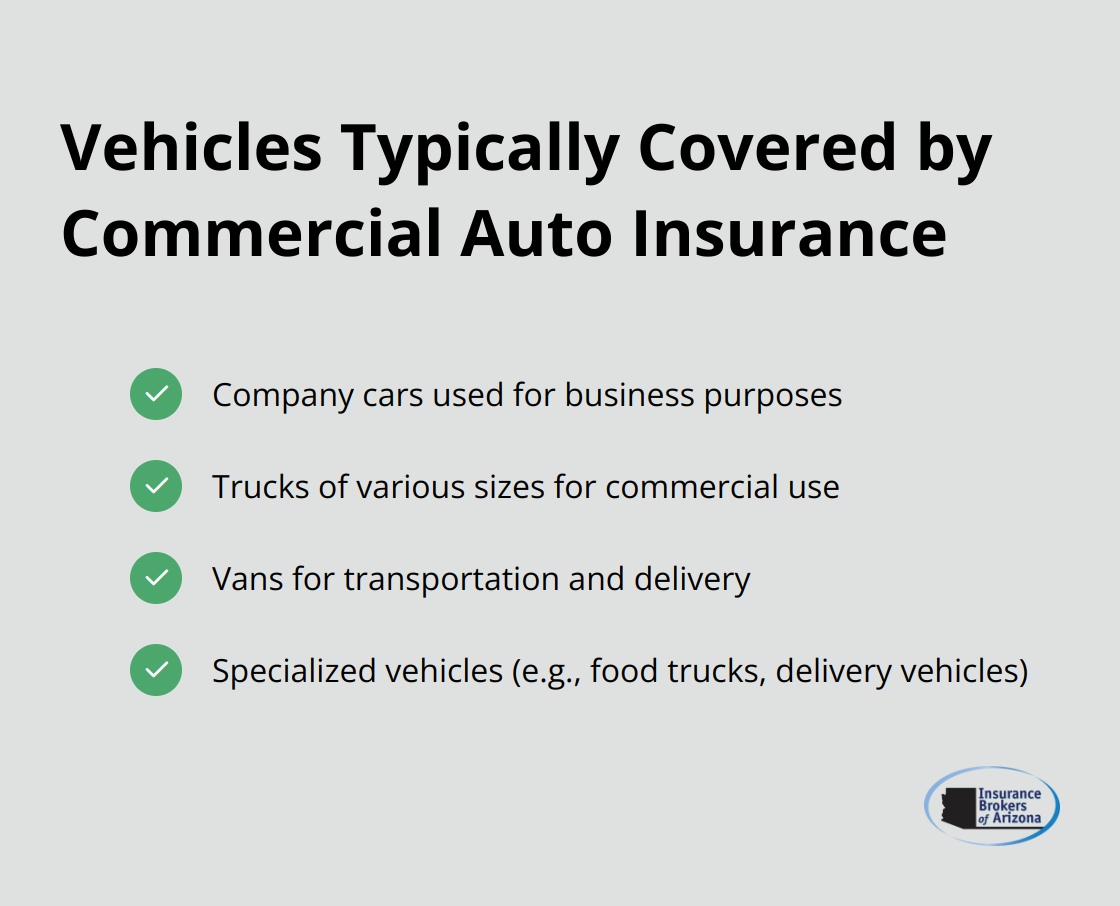

Types of Vehicles Covered

Commercial auto policies typically cover a wide range of vehicles used for business purposes, including:

- Company cars

- Trucks

- Vans

- Specialized vehicles (e.g., food trucks, delivery vehicles)

The Insurance Information Institute states that any vehicle used primarily for business operations should have commercial coverage.

Key Differences from Personal Policies

Commercial auto insurance differs from personal policies in several ways:

- Higher liability limits: Commercial policies often provide coverage in the millions, compared to personal policies that might cap at $300,000.

- Broader coverage scope: These policies address specific business risks and operations.

- Multiple vehicle coverage: A single policy can cover an entire fleet of vehicles.

Tailoring Coverage to Business Needs

Different businesses require different types of coverage. For example:

- A construction company might need coverage for heavy equipment transport.

- A catering business would focus on protection for food delivery vehicles.

The National Association of Insurance Commissioners reports that tailored policies can significantly reduce the risk of underinsurance for businesses.

Importance of Professional Guidance

Selecting the right commercial auto insurance requires careful consideration of your business’s unique needs. Working with experienced insurance professionals (like those at Insurance Brokers of Arizona®) can help ensure you get appropriate coverage without paying for unnecessary extras. These experts can analyze your specific operations and recommend a policy that provides comprehensive protection for your commercial vehicles.

As we move forward, let’s examine the critical factors you should consider when choosing your commercial auto insurance coverage.

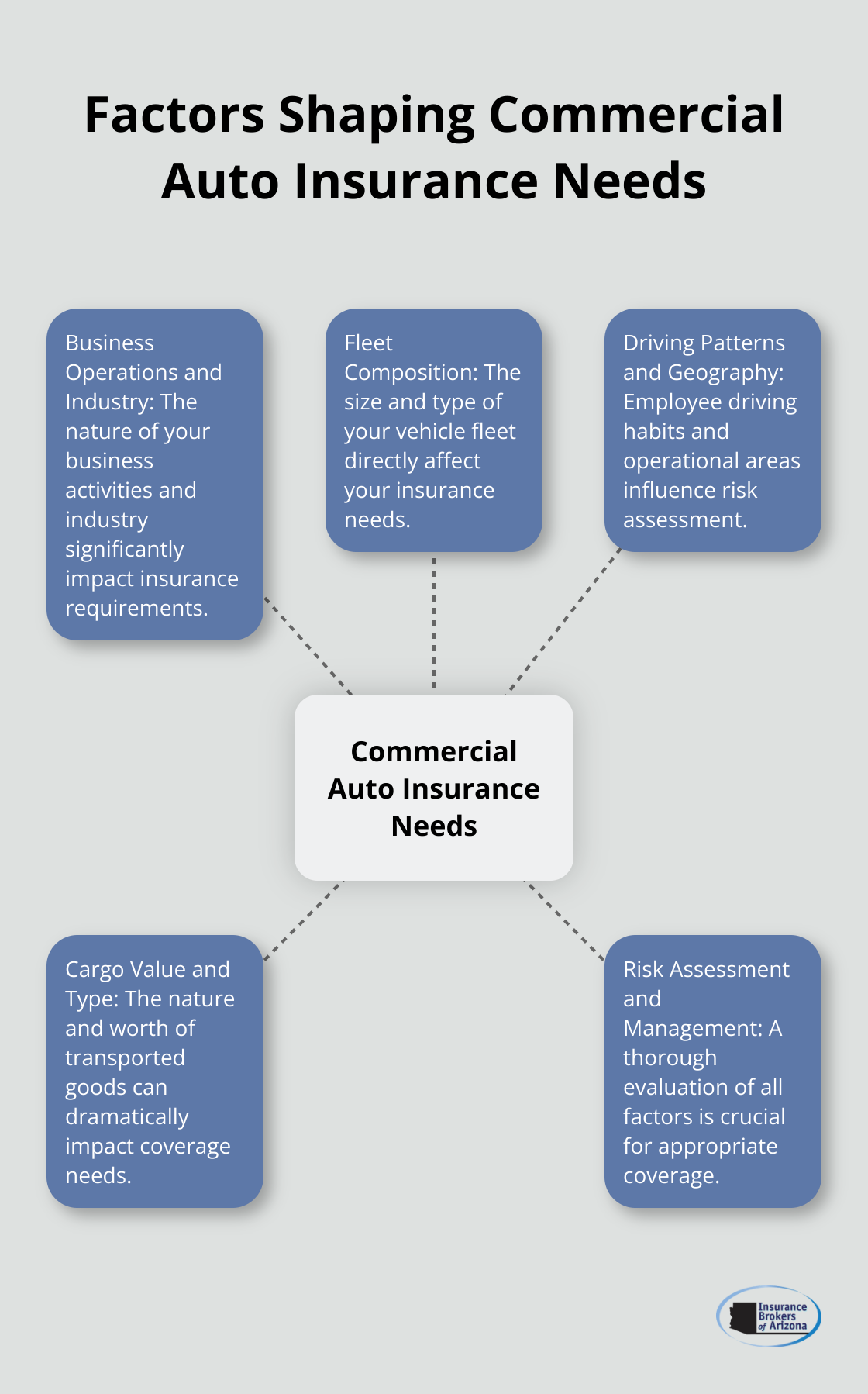

What Shapes Your Commercial Auto Insurance Needs?

Business Operations and Industry

Your industry and specific business activities significantly influence your insurance needs. A construction company that transports heavy equipment faces different risks than a florist making local deliveries. The Insurance Information Institute reports that businesses in high-risk industries (such as transportation or construction) often require more comprehensive coverage and may face higher premiums.

Fleet Composition

The size and makeup of your vehicle fleet directly affect your insurance requirements. A company with a single delivery van will have vastly different needs compared to a logistics firm managing a fleet of 50 semi-trucks. The National Association of Insurance Commissioners recommends that businesses conduct regular fleet audits to ensure their coverage aligns with their current vehicle inventory.

Driving Patterns and Geography

Your employees’ driving habits and the areas they frequent are significant factors. Urban deliveries in high-traffic areas present different risks than long-haul interstate trucking. The Federal Motor Carrier Safety Administration notes that businesses operating in multiple states may need to meet varying insurance requirements, potentially necessitating a more complex policy.

Cargo Value and Type

The value and nature of the cargo you transport can dramatically impact your insurance needs. Transporting hazardous materials or high-value goods requires specialized coverage. The American Trucking Associations emphasizes the importance of cargo insurance, especially for businesses moving expensive or sensitive items.

Risk Assessment and Management

A thorough assessment of these elements is essential for securing the right coverage. We recommend you work closely with an experienced insurance professional who can help you navigate these complexities and tailor a policy that truly fits your business needs. Insurance Brokers of Arizona® (with partnerships with over 40 reputable carriers) can provide competitive options for your commercial auto insurance needs.

As we move forward, let’s examine the essential coverage options you should consider including in your commercial auto insurance policy.

Essential Coverage Options for Commercial Auto Insurance

Liability Coverage: The Core of Your Policy

Liability coverage forms the foundation of any commercial auto insurance policy. It protects your business if your vehicles cause injury or property damage to others. The National Association of Insurance Commissioners suggests a minimum of $1 million in liability coverage for most businesses. Higher limits may be necessary depending on your industry and risk exposure.

Asset Protection: Collision and Comprehensive Coverage

While liability coverage protects against damage you cause to others, collision and comprehensive coverage protect your own vehicles. Collision insurance covers damage from accidents with other vehicles or objects. Comprehensive insurance protects against theft, vandalism, and natural disasters. The American Trucking Associations emphasizes that businesses with valuable fleets should prioritize these coverages to protect their assets.

Protection Against Uninsured Drivers

Uninsured and underinsured motorist coverage is often overlooked but can prove vital. The Insurance Research Council reports that about 1 in 8 drivers on the road lack insurance. This coverage protects your business if your vehicles become involved in accidents with drivers who lack adequate insurance.

Beyond Your Fleet: Non-Owned and Hired Auto Coverage

Non-owned auto liability covers your business when employees use their personal vehicles for work purposes. Hired auto physical damage coverage protects vehicles your business rents or leases. The Risk and Insurance Management Society notes that these coverages are particularly important for businesses that frequently rent vehicles or rely on employee-owned cars for work-related tasks (e.g., sales representatives or consultants).

Specialized Coverage Options

Depending on your business type, you may need specialized coverage options. For example, motor truck cargo coverage protects goods in transit, while garage keepers coverage is essential for businesses that service vehicles. Try to work with an insurance provider (such as Insurance Brokers of Arizona®) that offers a wide range of specialized coverage options to meet your unique needs.

Final Thoughts

Selecting the best commercial auto insurance demands a thorough evaluation of your business’s specific requirements. Your fleet composition, business activities, and cargo value all play a role in determining the ideal policy for your company. Regular policy reviews help maintain comprehensive protection and can lead to cost savings as your operations evolve.

An experienced insurance broker can simplify the process of finding and maintaining the best commercial auto insurance for your business. At Insurance Brokers of Arizona®, we offer competitive options tailored to your specific needs. Our expertise in commercial auto insurance ensures you receive a comprehensive risk management solution for your business vehicles.

The right commercial auto insurance protects your assets, employees, and business’s future. It goes beyond meeting legal requirements to provide peace of mind. Take the time to understand your options and work with knowledgeable professionals to secure a policy that allows you to focus on growing your business.