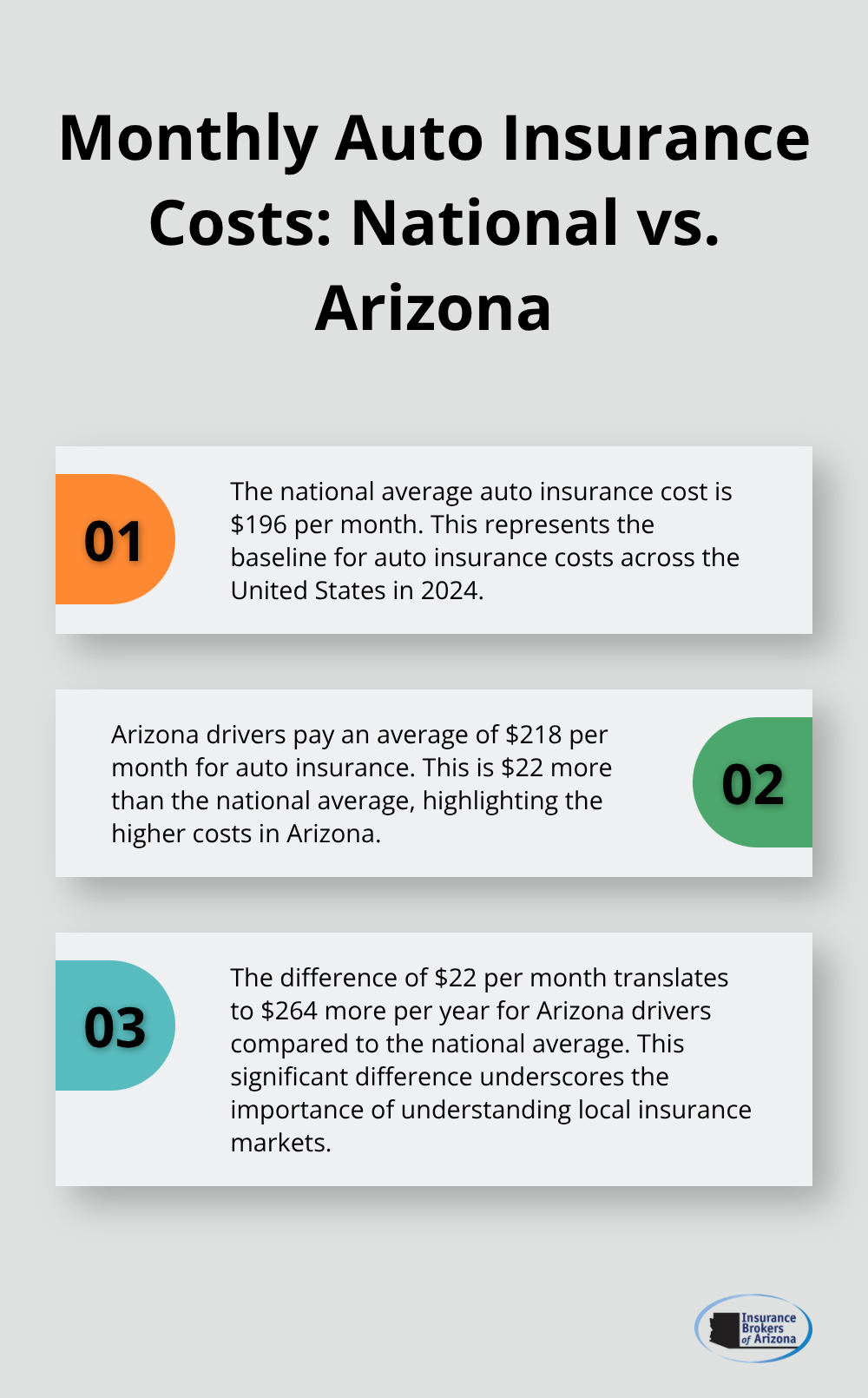

Auto insurance premiums hit record highs in 2024, with the average auto insurance cost per month reaching $196 nationwide. This represents a 26% increase from just two years ago.

We at Insurance Brokers of Arizona® see Arizona drivers paying even more, with monthly premiums averaging $218. Understanding these costs helps you make smarter coverage decisions.

How Much Do Americans Really Pay for Auto Insurance

Louisiana drivers face the harshest reality with monthly premiums that average $358, while Wyoming residents enjoy the lowest costs at just $92 per month according to NerdWallet’s October 2025 analysis. Florida follows Louisiana closely at $350 monthly, which makes geography the biggest factor in what you pay. New Hampshire and Vermont round out the cheapest states with monthly costs under $120, creating a massive $266 gap between the most and least expensive markets.

Premium Increases Hit Every State Hard

Auto insurance costs jumped 8% in the first half of 2025 compared to 2024, with some states that saw even steeper increases according to Bankrate data. The Bureau of Labor Statistics confirms this upward trend started in December 2021 and shows no signs that it will slow. Nevada, Florida, and Louisiana now all exceed $290 monthly for full coverage, while New York drivers pay over $335 monthly. Predictions from Insurify suggest tariffs could push premiums up another 8% by year-end, which means today’s rates represent the floor, not the ceiling.

Western States Lead Affordability Rankings

Western mountain states consistently offer the lowest premiums, with Idaho that averages 46% below national rates and Wyoming that leads affordability nationwide. These states benefit from lower population density, fewer accidents per capita, and reduced weather-related claims. Hawaii surprises many with premiums 38% lower than the national average (attributed to high public transport usage and fewer licensed drivers per capita).

Southern and Coastal Markets Drive High Costs

Southern and coastal states dominate the expensive end, driven by hurricane risks, high uninsured motorist coverage rates, and costly court environments. Michigan stands out as an expensive outlier in the Midwest due to its unique no-fault insurance requirements, while Massachusetts surprises with rates 22% below average despite high costs of daily life. These differences stem from measurable factors like weather patterns, traffic density, and state insurance laws rather than arbitrary price decisions.

Understanding these state-by-state variations helps you see the bigger picture, but your personal rate depends on factors you can actually control.

What Determines Your Auto Insurance Rate

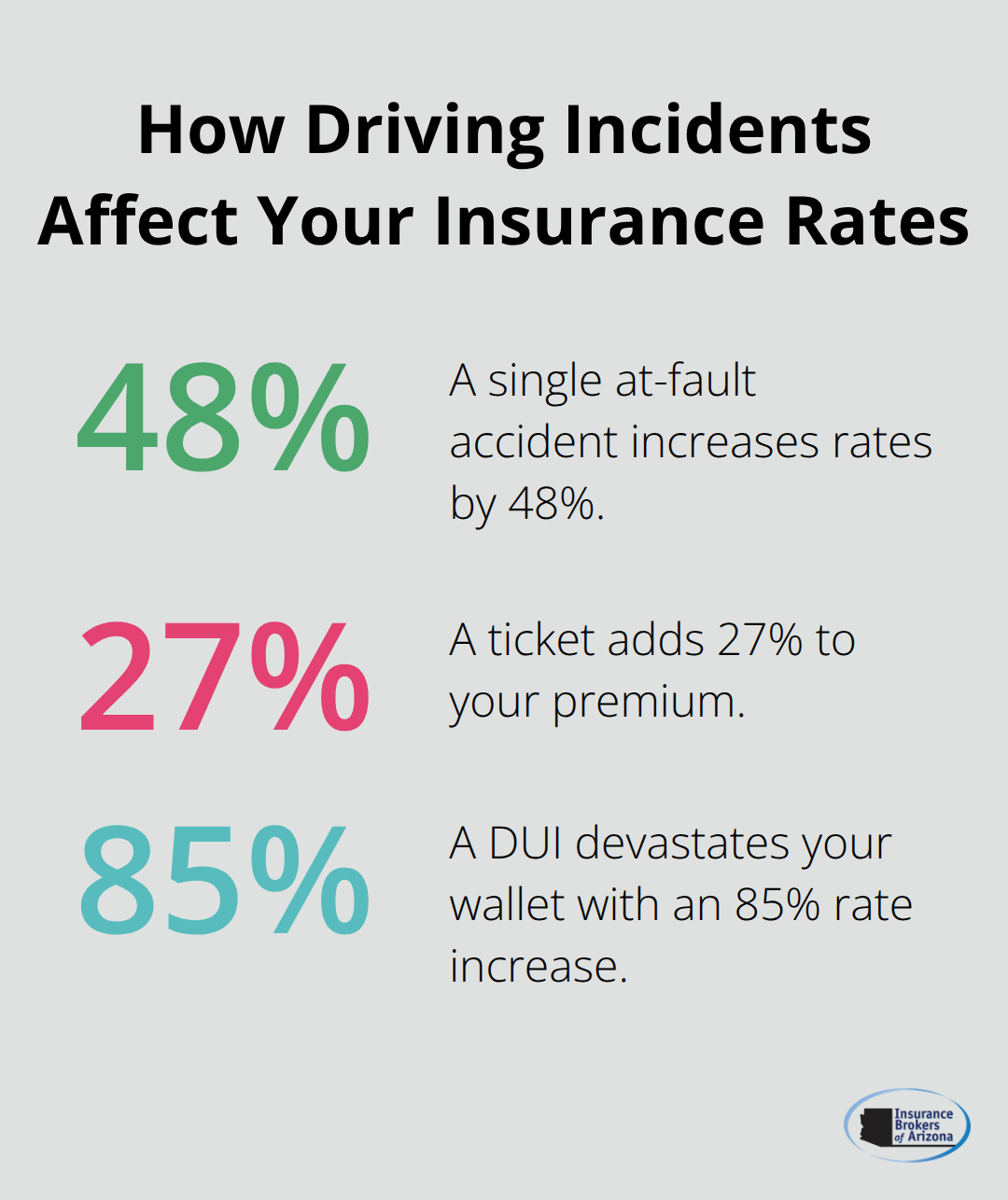

Your age alone can make or break your budget. Drivers under 25 face the steepest costs, with 20-year-olds who pay $4,686 annually for full coverage according to NerdWallet data. Men pay more than women, especially at younger ages, though this gap narrows after 30. Your record matters more than any other factor – a single at-fault accident increases rates by 48%, while a ticket adds 27% to your premium. A DUI devastates your wallet with an 85% rate increase (annual costs jump to $4,274). Poor credit scores punish drivers with 67% higher premiums compared to those with good credit, which makes your financial history as important as your record.

Vehicle Choice Controls Your Premium

Sports cars and luxury vehicles cost significantly more to insure due to higher repair costs and theft rates. Advanced safety features like automatic emergency braking and blind spot monitoring can reduce your premium through safety discounts. The age and value of your vehicle affects comprehensive and collision coverage costs – older cars with lower values make these coverages optional, which saves approximately $1,165 annually according to Consumer Reports data.

Coverage Decisions Shape Your Monthly Bill

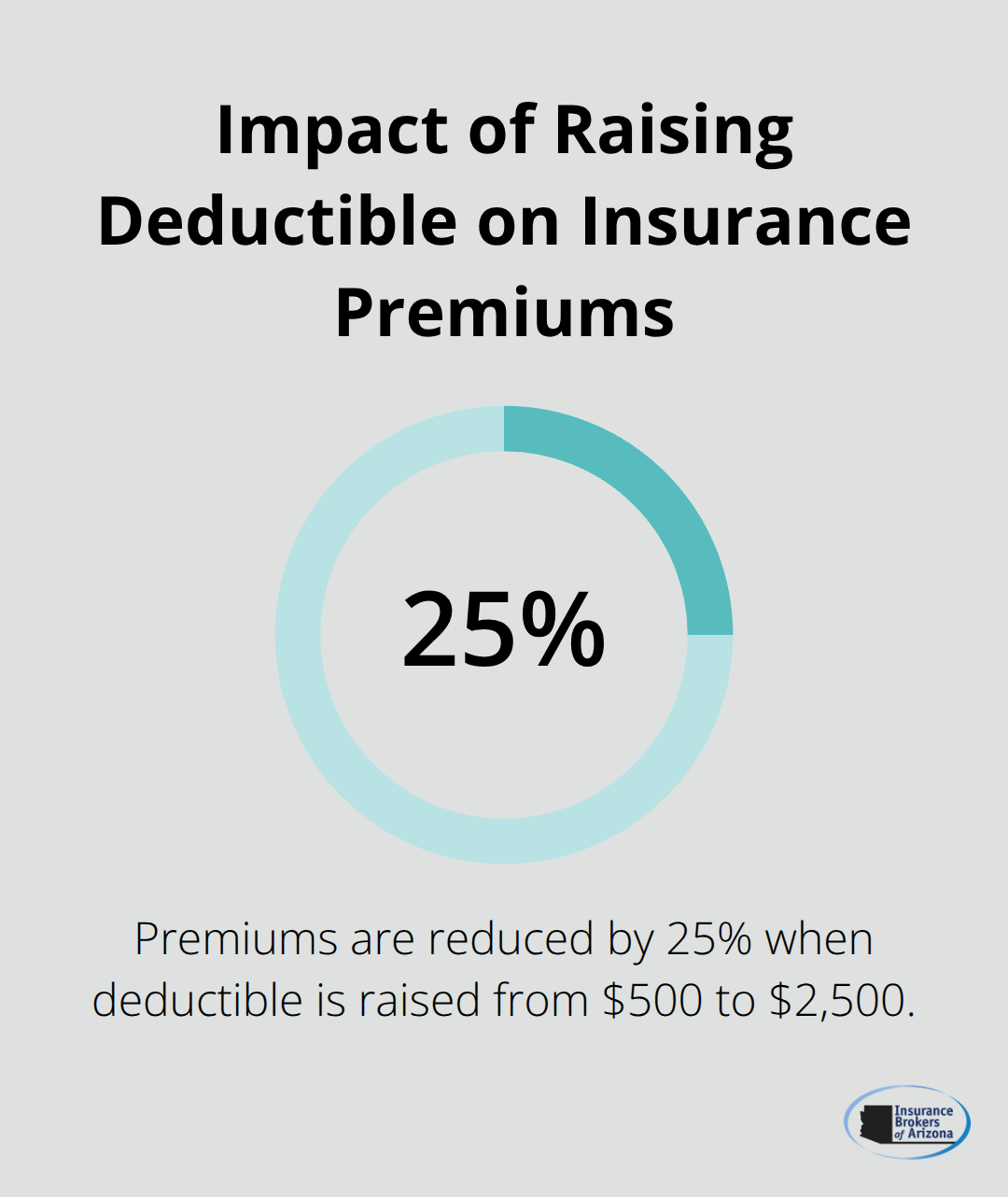

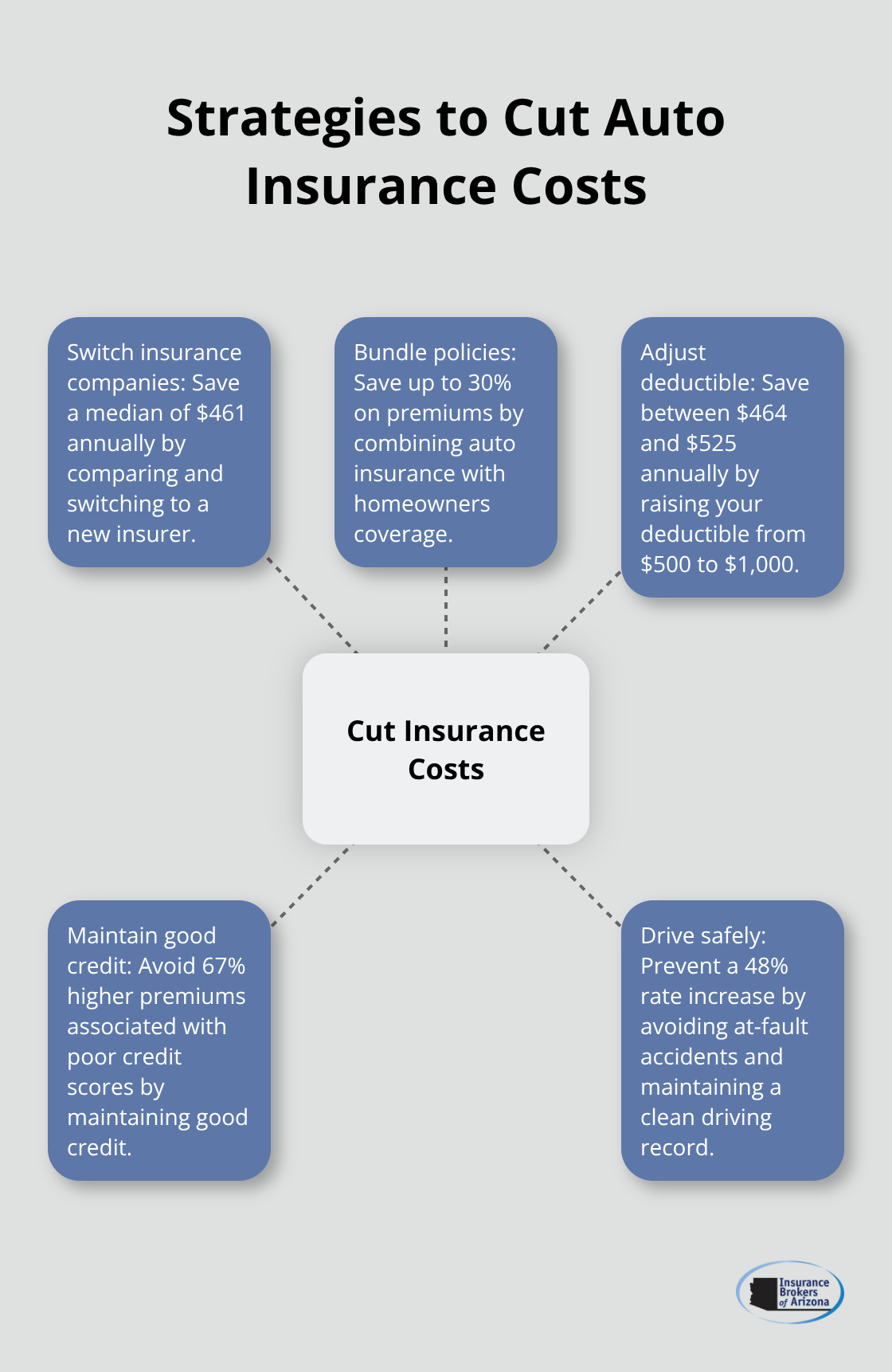

You cut your annual premium by $464 to $525 when you raise your deductible from $500 to $1,000 (Insurance Information Institute data). Full coverage costs three times more than minimum liability, but experts recommend at least $100,000/$300,000/$100,000 limits for adequate protection. You save up to 30% on premiums when you bundle auto insurance with homeowners coverage, while annual mileage under 10,000 miles reduces costs by approximately $116 yearly.

These rate factors work together to create your unique premium, but smart shoppers know how to minimize their impact through strategic choices and comparison tactics.

How to Cut Your Auto Insurance Costs

Consumers who switch insurance companies save a median of $461 annually according to Consumer Reports data. Thirty percent of consumers changed insurers in the last five years, and those who shop annually find better rates consistently. We at Insurance Brokers of Arizona® work with over 40 reputable carriers, which means you get competitive options without the hassle of multiple phone calls. Independent agents compare rates across carriers to find your best deal, while direct insurers show you only their own prices.

Stack Multiple Discounts for Maximum Savings

Auto insurance bundled with homeowners coverage saves up to 30% on premiums (Consumer Federation of America data), while good student discounts, military service discounts, and defensive course completion reduce premiums by approximately $233 annually. Automated driver programs save a median of $120 on premiums, though privacy-conscious drivers might skip this option. Annual mileage under 10,000 miles cuts costs by around $116 yearly, and dividend policies from certain insurers offer cashback benefits worth $116 or more.

Adjust Your Deductible and Coverage

You save between $464 and $525 annually when you raise your deductible from $500 to $1,000 according to Insurance Information Institute data. Older cars with lower values make comprehensive and collision coverage optional, which saves approximately $1,165 annually. Full coverage costs three times more than minimum liability, but experts recommend at least $100,000/$300,000/$100,000 limits for adequate protection.

Improve Your Credit Score and Record

Poor credit costs you 67% more in premiums compared to good credit, which makes credit improvement a financial priority beyond just loan rates. Pay bills on time, reduce credit card balances, and check your credit report for errors that drag down your score. Keep your record clean – even minor violations stay on your record for three to five years and increase costs significantly. Pay out of pocket for minor accidents instead of claims when possible, as this avoids potential premium increases worth up to $348 according to Consumer Reports research.

Final Thoughts

Auto insurance costs vary dramatically across states, with Wyoming drivers who pay $92 monthly while Louisiana residents face $358 monthly premiums. Arizona drivers pay $218 monthly, which exceeds the national average auto insurance cost per month of $196. These rates continue to climb with 8% increases in 2025 and additional tariff-driven hikes predicted ahead.

Your personal rate depends on factors you control like your record, credit score, and coverage decisions. Smart shoppers who switch carriers save $461 annually, while strategic deductible changes and discount combinations cut hundreds more from premiums. Clean records prevent the 48% rate increases that follow accidents (Consumer Reports data confirms this impact).

Arizona drivers benefit from experienced professionals who understand local market conditions. We at Insurance Brokers of Arizona® work with multiple reputable carriers to find competitive rates for your specific situation. Our approach helps individuals, families, and businesses secure appropriate coverage at affordable prices.