Log truck operations face unique risks that standard commercial vehicle insurance simply can’t handle. Timber transport requires specialized coverage for high-value cargo, dangerous routes, and heavy equipment.

We at Insurance Brokers of Arizona® have analyzed the leading commercial log truck insurance companies to help you make an informed decision. The right provider can save you thousands while protecting your logging business from costly claims.

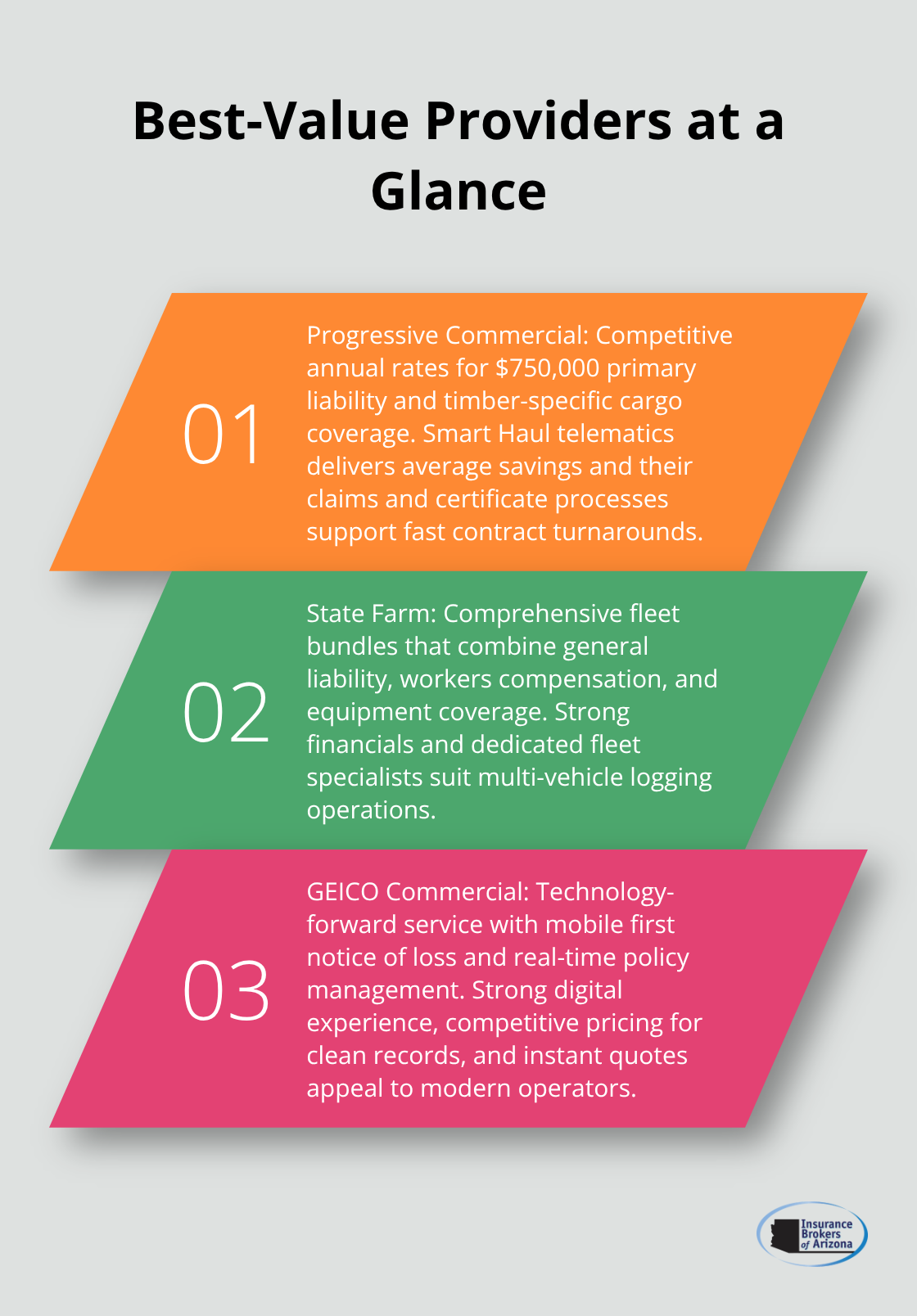

Which Log Truck Insurance Companies Deliver Best Value

Progressive Commercial Leads Cost Competition

Progressive Commercial dominates log truck insurance with rates that average $8,000 to $12,000 annually for $750,000 primary liability coverage. Their Smart Haul program cuts premiums by an average of $1,056 when operators use electronic devices for logs. Progressive holds an A+ rating from AM Best and has served commercial truckers since 1937.

The company processes claims 24/7 and offers same-day certificate issuance, which logging operations need for quick contract turnarounds. Their cargo coverage extends to timber-specific risks that include load shifts and environmental damage during transport. Progressive’s specialized approach addresses the unique challenges that timber haulers face on dangerous routes.

State Farm Provides Comprehensive Fleet Solutions

State Farm excels at coverage for large fleets with bundled policies that reduce administrative complexity. Their comprehensive packages include general liability, workers compensation, and equipment breakdown coverage in single policies. State Farm offers umbrella coverage up to $5 million (essential for high-severity timber transport accidents).

The company maintains strong financial ratings and provides dedicated fleet specialists who understand risks in the industry. Their coverage includes protection for specialized equipment like log loaders and delimbers that standard commercial policies exclude. State Farm’s fleet approach works particularly well for established operations with multiple vehicles.

GEICO Commercial Streamlines Claims Through Technology

GEICO Commercial transforms log truck insurance through digital claim reports and real-time policy management. Their mobile app allows drivers to report accidents immediately from remote sites, which reduces claim processing time by up to 40%. GEICO offers competitive rates for operators with clean records and provides instant quote comparisons online.

The company covers over 500,000 commercial vehicles nationwide and maintains a complaint rate below industry averages (according to the National Association of Insurance Commissioners). Their technology-first approach appeals to younger operators who prefer digital tools over traditional phone-based service.

These three providers represent different strengths in the log truck insurance market, but coverage types matter just as much as the company you choose.

What Coverage Types Protect Log Truck Operations

Log truck operations need three specific coverage types that standard commercial policies often exclude or provide inadequate limits. Cargo insurance for timber loads must cover the full replacement value of logs, which averages $2,000 to $8,000 per load depending on species and market prices. This coverage protects against theft, environmental damage, and load shifts that can destroy entire shipments during transport.

Cargo Insurance Addresses Timber-Specific Risks

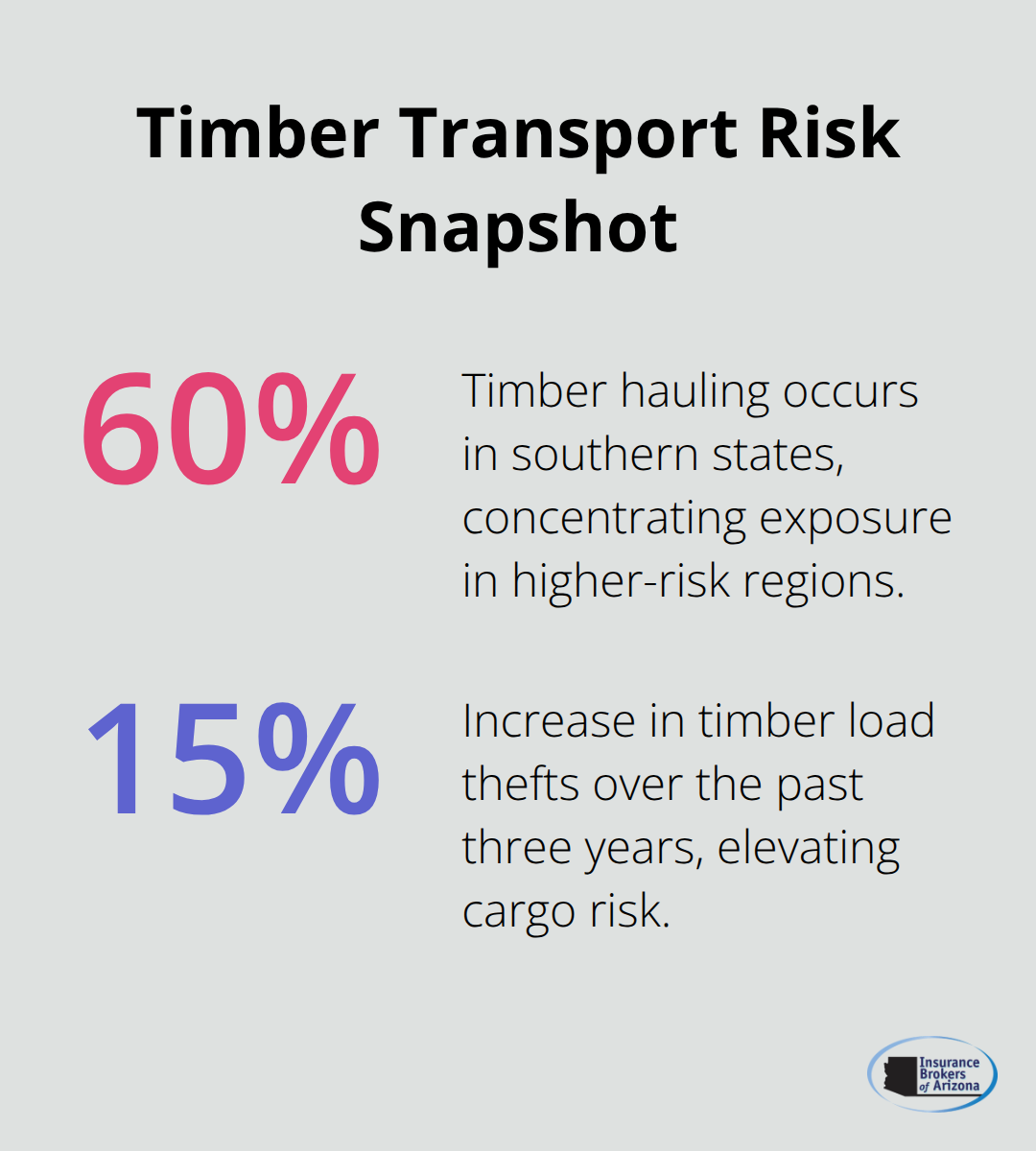

Timber cargo faces unique hazards that standard freight coverage cannot handle. Load shifts during sharp turns or sudden stops can damage entire shipments worth thousands of dollars. Environmental factors like rain, snow, and extreme temperatures affect wood quality and market value. Theft rates for timber loads have increased 15% over the past three years (according to cargo theft statistics), making comprehensive cargo coverage essential for profitable operations.

Equipment Coverage Protects Specialized Machinery

Equipment coverage for logging machinery extends far beyond basic commercial vehicle insurance. Log loaders, delimbers, and specialized trailers require separate coverage because their replacement costs range from $150,000 to $500,000 per unit. Standard commercial policies typically cap equipment coverage at $50,000, which leaves massive gaps for logging operations. The Federal Motor Carrier Safety Administration requires specific equipment standards that can void coverage if not met.

General Liability Handles Catastrophic Damage Claims

General liability coverage for log truck operations must account for the catastrophic damage potential of 80,000-pound vehicles carrying shifting loads. Timber haulers face liability claims averaging $850,000 per incident according to National Association of Insurance Commissioners data, significantly higher than standard commercial trucking. Log trucks cause more severe injuries in collisions due to their weight, with approximately 60% of timber hauling occurring in southern states where accident rates peak during wet seasons.

Understanding these coverage requirements helps logging operators identify gaps in their current policies, but several factors determine how much these protections will cost your operation.

What Drives Your Log Truck Insurance Costs

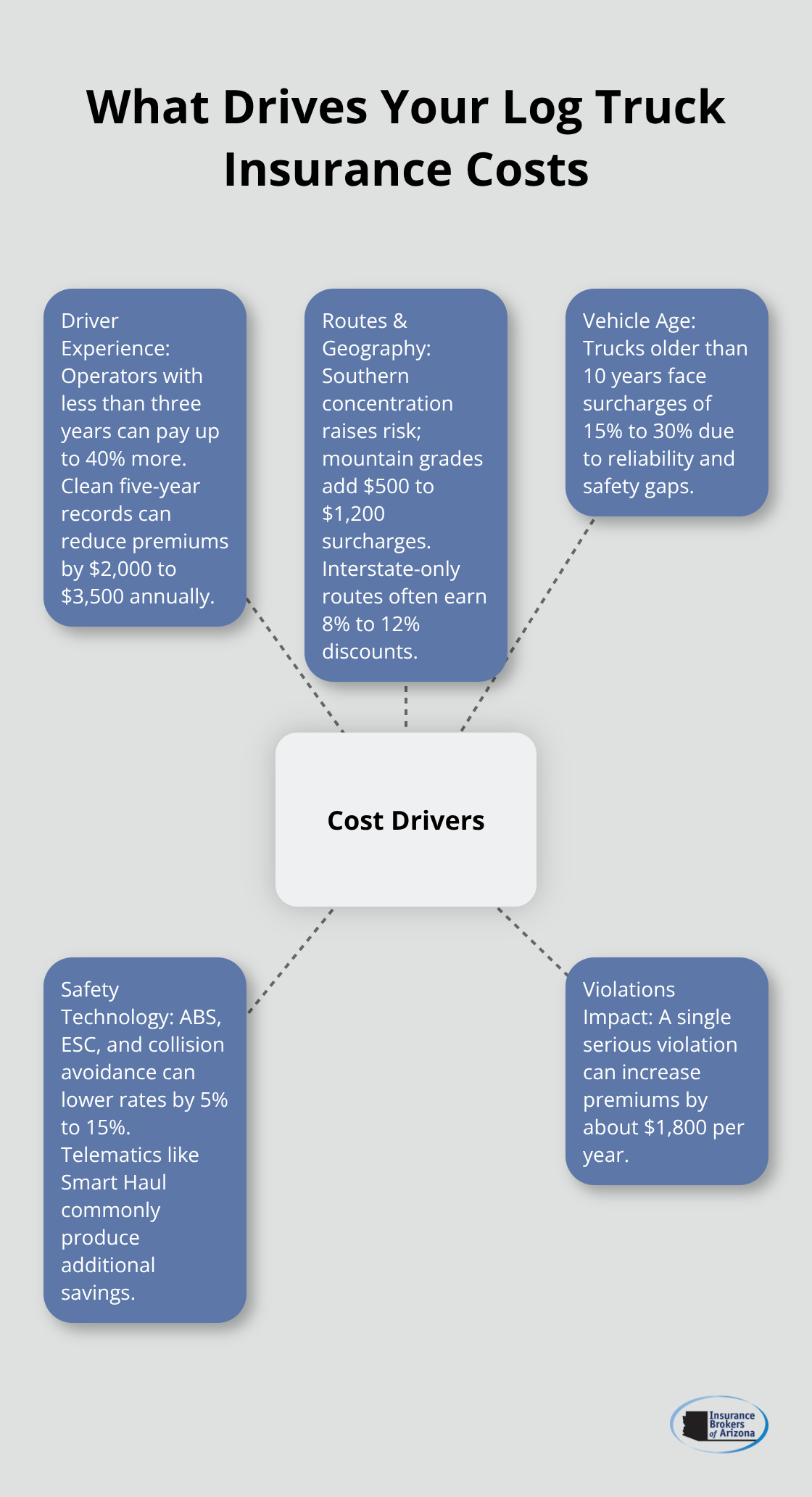

Driver experience creates the largest variance in log truck insurance premiums. Operators with less than three years of commercial experience pay up to 40% more than seasoned drivers. Insurance carriers examine Commercial Driver License records for violations, weight infractions, and hours-of-service penalties. Clean records over five years reduce premiums by $2,000 to $3,500 annually (according to Progressive Commercial data), while single serious violations increase costs by an average of $1,800 per year.

Geographic Routes Determine Risk Multipliers

Southern states where 60% of timber transport occurs face higher premiums due to wet season accident spikes and terrain challenges. Alabama, Florida, Georgia, Mississippi, and South Carolina show the highest claim frequencies for log truck operations, with rates 25% above national averages. Mountain routes with steep grades and curves trigger additional surcharges of $500 to $1,200 annually, while interstate-only operations receive discounts of 8% to 12%. Insurance carriers analyze specific route data (elevation changes, weather patterns, and historical accident frequencies) to calculate location-based adjustments.

Vehicle Age and Safety Technology Impact Rates

Trucks older than 10 years face surcharges of 15% to 30% due to higher breakdown risks and outdated safety systems. Electronic devices reduce premiums through programs like Progressive’s Smart Haul, which offers average savings of $1,056 annually. Anti-lock brakes, electronic stability control, and collision avoidance systems lower rates by 5% to 15% depending on the carrier. Newer trucks with comprehensive safety packages often qualify for fleet discounts even with single-vehicle operations, which makes equipment upgrades financially beneficial beyond operational improvements.

Final Thoughts

Progressive Commercial, State Farm, and GEICO Commercial represent the strongest options among commercial log truck insurance companies, each with distinct advantages for different operation types. Progressive leads with competitive rates and specialized timber transport coverage, State Farm excels at comprehensive fleet solutions, while GEICO streamlines claims through advanced technology. These carriers understand the unique risks that timber haulers face daily.

Specialized coverage remains non-negotiable for timber transport operations. Standard commercial policies cannot address the unique risks of timber transport, from cargo shifts worth thousands to catastrophic liability claims that average $850,000. The combination of proper cargo insurance, equipment coverage, and adequate liability limits protects your business from industry-specific hazards that generic policies exclude.

We at Insurance Brokers of Arizona® work with multiple reputable carriers to find competitive options tailored to your specific needs (including the three providers discussed above). Our expertise in commercial insurance helps timber transport operations secure comprehensive protection while they manage costs effectively. Contact Insurance Brokers of Arizona® today to get personalized quotes that address your timber transport risks and operational requirements.