Most drivers ask “how much auto insurance do I need?” after they’ve already purchased a policy. This backwards approach often leaves gaps in protection when accidents happen.

We at Insurance Brokers of Arizona® see clients discover their coverage shortfalls only after filing claims. The difference between minimum state requirements and adequate protection can cost you thousands of dollars.

Why Arizona’s Minimum Coverage Won’t Protect You

Arizona requires only $25,000 per person and $50,000 per accident for bodily injury liability, plus $15,000 for property damage. These numbers haven’t changed in decades, while medical costs and vehicle values have soared. The average bodily injury liability claim reached $26,501 in 2023 according to the Insurance Information Institute, which means Arizona’s minimum already falls short for typical accidents.

When Minimum Coverage Creates Maximum Problems

A single emergency room visit after a car accident costs $15,000 to $25,000 on average. Arizona’s $25,000 per person limit vanishes quickly when someone requires surgery, physical therapy, or extended treatment. Property damage limits prove equally inadequate when the average new car costs $48,000.

Drivers who hit luxury vehicles or cause multi-car accidents can generate repair bills that exceed $50,000 within minutes.

The True Cost of Underinsurance

Drivers face lawsuits after they exceed their coverage limits. One recent case involved a driver who caused an accident that required $75,000 in medical treatment while they carried only state minimums. The victim’s insurance company pursued the remaining $50,000 directly from the driver’s personal assets (including wages and bank accounts). Courts can garnish wages, freeze bank accounts, and place liens on homes when coverage falls short.

What Financial Experts Actually Recommend

Financial experts recommend liability limits of at least $100,000 per person and $300,000 per accident to protect against these scenarios. Many suggest $250,000/$500,000/$250,000 for drivers with substantial assets. These higher limits cost only $200 to $400 more annually but protect against catastrophic financial loss.

Beyond basic liability coverage, several other protection types can shield you from gaps that state minimum requirements leave wide open.

Key Coverage Types You Should Consider

Comprehensive and Collision Coverage

Comprehensive and collision coverage protect your vehicle investment when liability coverage cannot help. Collision pays for repairs after accidents you cause, while comprehensive covers theft, vandalism, weather damage, and animal strikes. Drivers who finance or lease vehicles must carry both types, but even owners of paid-off cars should consider these coverages if their vehicle exceeds $4,000 in value.

The Insurance Information Institute reports the average collision claim costs $5,992, while comprehensive claims average $2,365. Smart drivers choose deductibles between $500 and $1,000 to balance premium costs with manageable out-of-pocket expenses.

Uninsured and Underinsured Motorist Protection

Arizona has approximately 13% uninsured drivers according to the Insurance Research Council, which means one in eight drivers lacks coverage entirely. Uninsured motorist coverage pays for your medical bills and property damage when hit by drivers with no insurance, while underinsured coverage kicks in when the at-fault driver carries insufficient limits.

These coverages cost roughly $100 to $200 annually but can save tens of thousands when accidents involve uninsured drivers. The protection becomes even more valuable when you consider that many drivers carry only state minimums (which we’ve already established fall short of real-world costs).

Medical Payments and Personal Injury Protection

Medical payments coverage supplements uninsured motorist protection by covering immediate medical expenses for you and passengers regardless of fault. Limits typically range from $1,000 to $10,000, and this coverage pays quickly without waiting for fault determination.

Personal injury protection (PIP) goes further by covering lost wages and essential services in addition to medical bills. Arizona doesn’t require PIP, but it provides broader protection than medical payments coverage alone.

Your specific coverage needs depend on several personal factors that go beyond these standard protection types. For business owners who use vehicles for work purposes, commercial auto insurance may be necessary alongside personal coverage.

Factors That Determine Your Coverage Needs

Your coverage requirements depend on three concrete financial calculations rather than generic recommendations. Vehicle value drives your collision and comprehensive decisions, while personal assets determine liability limits, and your patterns of travel influence risk exposure.

Vehicle Value Sets Your Physical Damage Coverage

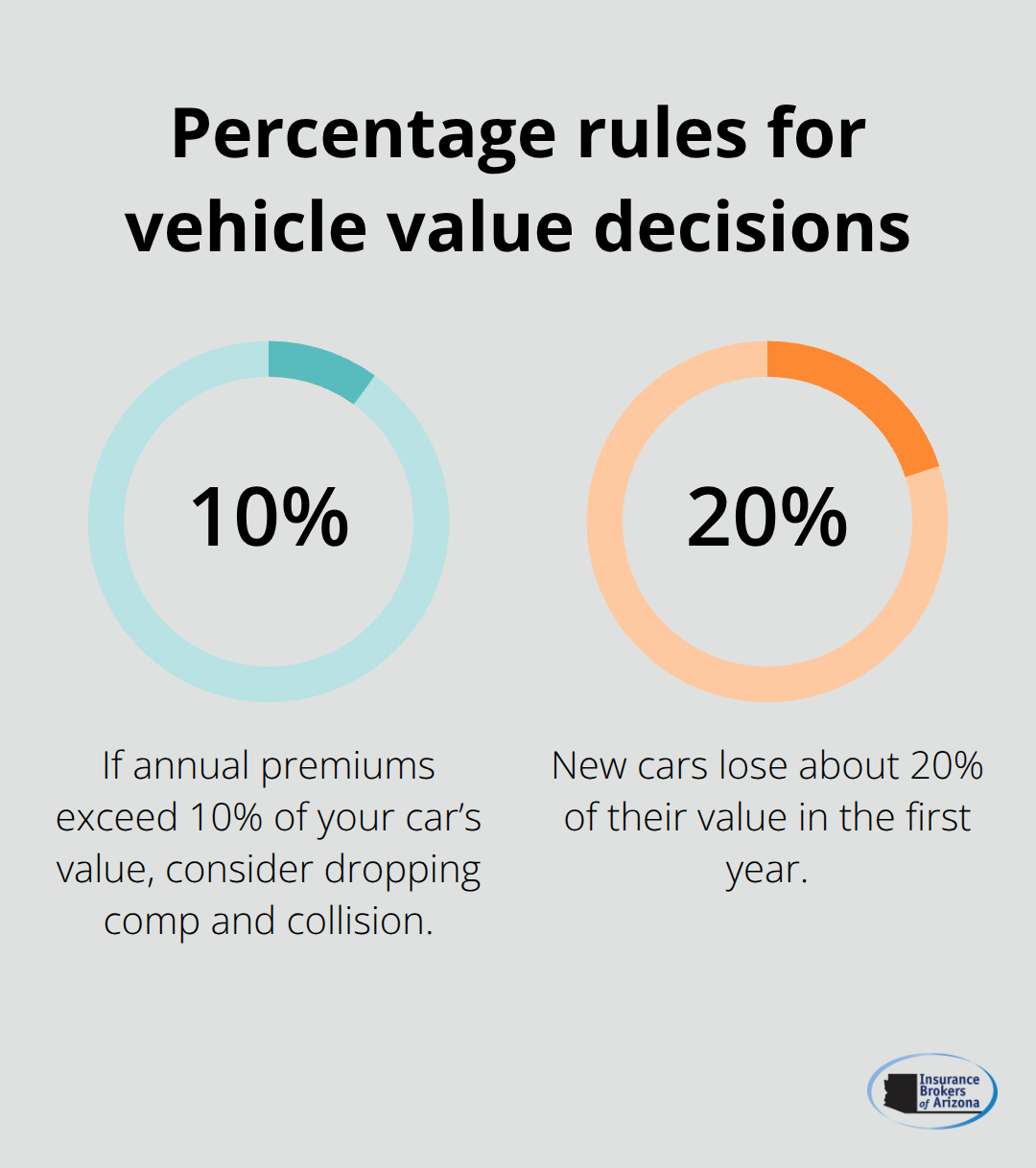

Drop collision and comprehensive coverage when annual premiums exceed 10% of your car’s current value. A vehicle worth $8,000 should not carry collision coverage that costs more than $800 yearly. The Insurance Information Institute confirms most drivers should eliminate physical damage coverage on vehicles older than 10 years or worth under $4,000.

Financed vehicles require comprehensive and collision coverage regardless of value because lenders protect their investment through mandatory coverage requirements. Gap insurance becomes essential for new car buyers since vehicles lose 20% of their value within the first year.

Personal Assets Drive Liability Limit Decisions

Calculate your net worth (home equity, retirement accounts, and savings) to determine necessary liability limits. Drivers with assets that exceed $300,000 need liability coverage of at least $250,000 per person and $500,000 per accident. Those with net worth above $500,000 should add umbrella policies that provide $1 million in additional liability protection.

The National Association of Insurance Commissioners reports that inadequate liability coverage leads to personal asset seizure in 23% of major accident cases. Courts can garnish wages and freeze bank accounts when coverage falls short of actual damages.

Travel Patterns Affect Your Risk Profile

Commuters who drive over 15,000 miles annually face 40% higher accident rates than occasional drivers according to Federal Highway Administration data. Long-distance commuters need higher uninsured motorist limits because highway accidents involve multiple vehicles and severe injuries.

Drivers with teenage children should maximize liability and uninsured motorist coverage since teen drivers cause accidents at triple the rate of experienced drivers. Urban drivers require comprehensive coverage for theft and vandalism risks that rural drivers rarely face.

Age and Credit Score Impact Premium Costs

Insurance companies use age and credit scores to calculate premiums, with drivers under 25 and over 65 paying the highest rates. Poor credit scores can increase premiums by 50% to 100% in states that allow credit-based pricing. Drivers with excellent credit often qualify for discounts that reduce premiums by 10% to 15%.

Final Thoughts

The question “How much auto insurance do I need?” demands concrete financial analysis rather than guesswork. Arizona drivers need liability coverage of at least $100,000 per person and $300,000 per accident to protect against real-world accident costs. Add comprehensive and collision coverage for vehicles worth over $4,000, plus uninsured motorist protection given Arizona’s 13% uninsured driver rate.

Your coverage decisions should reflect your net worth and travel patterns. Drivers with assets that exceed $300,000 need higher liability limits, while those with teenage drivers or long commutes require maximum uninsured motorist coverage. The additional cost of adequate coverage typically runs $200 to $600 annually but prevents catastrophic financial loss.

Review your current policy by comparing coverage limits against your vehicle value and personal assets. Calculate whether your liability limits exceed your net worth and verify that your comprehensive and collision deductibles remain manageable. We at Insurance Brokers of Arizona® help you balance protection needs with premium costs through access to multiple carriers.